You've landed in Canada and now it's time to start building your financial future here. The good news is that Canada has a lot of registered accounts and investment products to help you save and invest.

Since they’re likely different from programs that your home country has to help you save, you'll need to take time to learn how to navigate them successfully.

But don't worry! We'll walk you through everything you need to know.

When it comes to investing, the fastest way to reach your financial goals is to be strategic. Here are some factors to consider:

- Think of your tax-advantaged accounts (ex. TFSAs and RRSPs)

- Align with your investment objective, risk tolerance and time horizon (how long you plan to hold an investment to meet a goal)

- Work with an advisor on the right solutions for your plan

- Diversify your portfolio

An important initial move is to make use of the different tax-advantaged savings and investing vehicles Canada offers you as they're designed to help you reach your goals faster. These include things like Registered Retirement Savings Plans (RRSPs), Tax-Free Savings Accounts (TFSAs), First Home Savings Accounts (FHSAs) and Registered Education Savings Plans (RESPs).

You'll also need to understand the investment time horizons those accounts are designed for, when you can take money out of the accounts, and what the penalties could be connected to them if you use them incorrectly (ex. withdrawing early).

Then, you need to match your investment objectives, risk tolerance and the timelines for personal financial goals with how you use various registered accounts. For example, if you're saving for retirement (a long time horizon goal), you might want to consider taking advantage of the tax-deductible savings you'll get in your Registered Retirement Savings Plan (RRSP).

Other accounts that can help you reach your goals include the Tax-Free Savings Account (TFSA) and the First Home Savings Account (FHSA). (We'll define these registered accounts later in this article.)

Note: With accounts like TFSAs and RRSPs, there are a variety of options to hold within your accounts such as cash, guaranteed investment certificates (GICs), exchange-traded funds (ETFs), mutual funds, stocks and bonds.

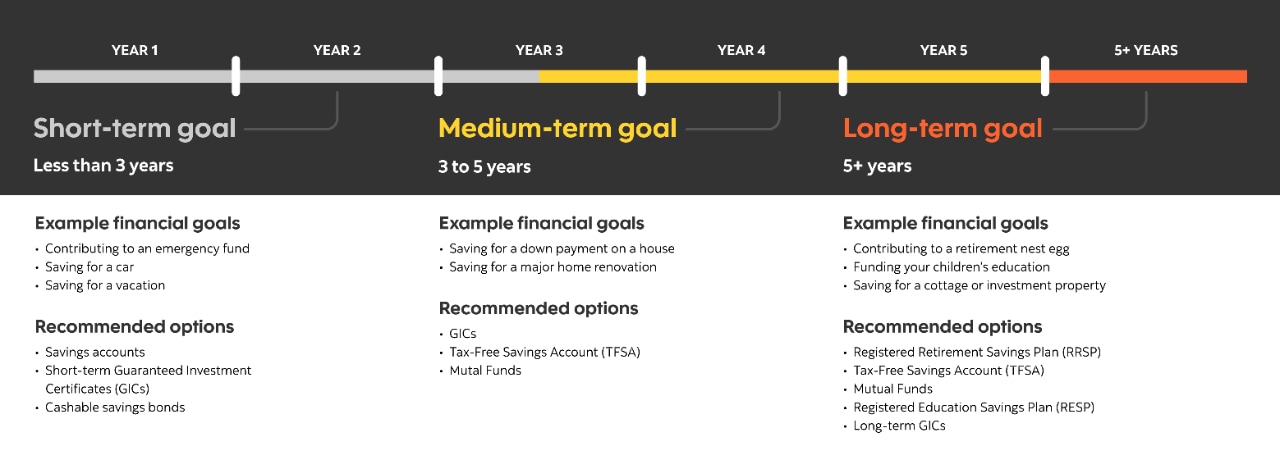

| Time horizon | Example of a financial goal | Recommended options | |

|---|---|---|---|

| Short-term goal | Less than 3 years |

|

|

| Medium-term goal | 3 to 5 years |

|

|

| Long-term goal | 5+ years |

|

|

Finally, you want to find the right provider and product for your investing needs and invest your money into a diversified portfolio.

You should know: You're eligible for all investment accounts in Canada whether you're a permanent resident or a citizen, if you are at least 18 years old. . Learn more.

Canadian banks, such as Scotia, offer a whole suite of savings and investment products, like bank accounts, mutual funds, stocks, guaranteed investment certificates (GICs) in branch. They also have investment advisors and self-directed investing brokerage options for buying stocks, bonds and exchange-traded funds (ETFs) like Scotia iTRADE®.

It's relatively easy to get started investing in Canada. While some investment products or services require minimum investments, many have low minimums — $500 or less, or no minimums at all — and allow you to start investing right away.

The sooner you start investing, the sooner you can start seeing gains towards your emergency fund or child's education fund. Rather than waiting until you feel you have enough money to start, find a product that works for how much you currently have and get started now.

How much you want to invest is something that will be specific to your financial situation. It is key to evaluate your future goals and time horizons for them, look at your income and expenses, and then create a plan to put a certain amount of money towards your investments every paycheque.

If you want to save money quickly to buy a car in six months (a short-term goal) or a home in two years, you might want to put a larger percentage of your income away and cut back in other areas. Or you might decide that right now you can't afford to put money away monthly but will put your annual bonus towards your savings goals. The key is to figure out the best investing strategy for you and your investment goals.

This can sound a bit overwhelming, but your Scotia advisor will work with you to create a financial plan that will work for you and your goals.

You should know: The sooner you start investing, the better off you'll be when you retire due to the power of compound interest. Five or ten years can make a big difference!

It's time to explore the registered savings and investment accounts and products that you can use to make your money grow in Canada.

There are five main types of savings plans with tax benefits:

1. Tax-Free Savings Account (TFSA)

A TFSA is a savings account where every resident over the age of 18 can make an annual contribution. The allowed amount changes over the years, so it’s important to look up your contribution limit. If you aren't able to make a contribution in one year or if your contribution is less than the allowed amount, your contribution room carries over to the next year. You can use a TFSA to invest in options like mutual funds and GICs.

The benefit of a TFSA is that the funds you earn through investment gains, dividends and interest all grow in your account tax-free. That means that you don't have to pay taxes on the earnings when you take them out of your account to use them. Note though that your contributions to a TFSA aren’t deductible on your taxes.

TFSAs are great for short and medium time horizon savings goals because there are no rules around when you can take funds out. However, because the gains aren't taxed, they're also great for long-term investing. For example, they can be used for tax planning purposes in retirement to balance out the taxed retirement income you would be taking out from a Registered Retirement Savings Plan (RRSP), pensions or part-time work.

2. Registered Retirement Savings Plan (RRSP)

RRSPs are retirement savings accounts that you contribute pre-tax funds to. These funds grow tax-free until you withdraw them for your retirement and then you pay taxes on the funds you take out. Contributions are tax-deductible and can result in a tax refund. For that reason, some people get a tax refund because of their RRSP contributions.

Your RRSP contribution limit is 18% of the earned income reported the year before on your tax return, up to a maximum of $32,490 in 2025.

RRSPs are great for saving for retirement. You can also take up to $60,000 out of your RRSP to buy or build a qualifying home for yourself or a person with a disability whom you're related to under the Home Buyers' Plan. You have 15 years to repay those funds into your RRSP. You can also take $10,000 a year, up to $20,000, from your RRSP via the Life Time Learning Plan to pay for full-time training or education for you or your spouse.

3. Registered Education Savings Plan (RESP)

RESPs are education savings accounts that allow families to put after-tax money away for their kids' education. By doing so, families can access certain government grants to accelerate their savings and the funds grow tax-deferred while in the account.

There's no annual contribution limit for RESPs, but they have a lifetime contribution limit of $50,000 per beneficiary. However, the government matches contributions up to a certain amount each year:

- The Canada Education Savings Grant provides a matching grant of 20% of the first $2,500 contributed each year to an RESP, up to a maximum of $500 per year.

- The Canada Learning Bond grant provides an additional contribution for children from low-income families of up to $2,000.

Learn more about RESPs, including what you can do if your child ends up not using it.

4. Registered Disability Savings Plan (RDSP)

RDSPs are a registered savings account designed to help families provide long-term financial security for people with disabilities. Contributions are made after-tax but are able to grow tax-deferred while inside the account. Like an RESP, there's no annual contribution limit, but a lifetime limit. For an RDSP, that's $200,000 per beneficiary.

The government provides two types of grant programs to help families save:

- The Canada Disability Savings Grant (CDSG) provides a matching grant of up to 300% on the first $500 of annual contributions to an RDSP, up to a maximum of $3,500 per year.

- The Canada Disability Savings Bond (CDSB) provides up to $1,000 per year to families with low incomes to help them save for the long-term care of a person with a disability.

RDSP funds can be used to pay for living expenses or expenses related to the beneficiary's disability, such as medical and rehabilitation costs.

5. Tax-Free First Home Savings Account (FHSA)

The Tax-Free First Home Savings Account is a new registered account that first rolled out in 2023. It will let Canadian residents put up to $8,000 per year towards the purchase of their first home, up to a maximum contribution limit of $40,000. These contributions are tax deductible, withdrawals are tax free and unused contribution room can be carried forward — but the maximum you can carry forward is $8,000, even if your contribution room grows past that amount.

You should know: You can use your RRSP, FHSA and TFSA to save for a down payment on your first home. Find out how.

A savings account is a great way to store money safely and accessibly. It also tends to earn higher interest rates than a chequing account. You can easily transfer money between them online, over the phone, through the bank’s app or at a branch. One popular type of savings account to accelerate your savings is a high interest savings account.

If you want to save additional funds after you've maxed out the contribution room in your registered accounts, a high interest savings account could be a good option.

When it comes to saving products, a high interest savings account tends to give you a higher rate of return than regular savings products. While this is usually less than other types of investments, a high interest savings account is a good place to keep your emergency fund.

With the Scotia High Interest Savings Account, you’ll be able to earn higher interest rates than with a regular Scotia savings account, depending on the total balance that you hold with Scotiabank (to earn interest, you’ll need a minimum balance of $10,000 CAD across your eligible accounts). Your interest rate is based on your Total Relationship Balance.1

What’s a Total Relationship Balance?

Your Total Relationship Balance is the combined daily balance in all your eligible accounts, including eligible Scotiabank chequing accounts, savings accounts, guaranteed investment certificates, and mutual funds available through Scotia Securities Inc. You’ll need the minimum Total Relationship Balance to earn interest on your HISA. The higher your Total Relationship Balance, the higher your interest rate that Scotiabank will apply to the funds in your Scotia HISA.

Visit scotiabank.com/totalrelationshipbalance to view all “Eligible Accounts” included in your Total Relationship Balance.

Canada also has a number of financial products that you may recognize from those available in your home country. These can be purchased inside or outside a registered account.

Mutual funds

Mutual funds are investment vehicles where many investors pool their money to buy a diversified portfolio of equity, bonds or other investments. Professional fund managers manage mutual funds, and there are a number of different types for you to choose from.

Guaranteed Investment Certificates (GICs)

GICs are relatively safe investments that offer a guaranteed rate of return with little risk. Typically, if you invest in a GIC, you must commit to putting in your money for an agreed upon term. If you redeem early, you may pay a penalty or lose the interest you earned. This varies by the bank — Scotia's GICs don't charge a penalty for early withdrawal, but you may lose the interest earned.

You should know: Your investments should be calibrated to your age and risk tolerance to ensure that you can balance the need for growth in your investments with the need for security.

There are a lot of great ways to get started with saving and investing in Canada, including a number of registered accounts that will help your money go further.

If you're unsure what your best strategy for saving and investing in Canada is, connect with a Scotia advisor who can help you build your Canadian investment portfolio. They'll help you navigate your options and give you the information you need to build towards your goals.