When your budget includes rent, student loans, and car payments, it might be tempting to put off investing until you’ll have less debt or more disposable income. But instead of waiting for a “better time" to build your portfolio, it’s important to start investing now. Even small investments on a regular basis, started early, can increase in value significantly over time thanks to compound growth.

Before you start investing, it's important to understand what it means to invest. We’ll break down the different options available to help you reach your financial goals.

What's the difference between saving and investing?

Whether you say, “saving for retirement” or “investing for the future,” you are referring to the same thing: putting money away now that will grow to support your future dreams.

While the terms investing and saving are often used interchangeably, they mean different things. Investing involves putting your money to work for your goals. That is, shifting it into assets that can gain and lose value over time, which means there’s potential for your money to grow over the long term. Saving, on the other hand, generates small amounts of interest, determined by interest rates, while preserving the original balance.

Investing offers different levels of risk, return potential, and tax treatment. Younger investors also benefit from these six advantages of investing early:

1. Get time on your side

A Pre-Authorized Contribution (PAC) is an easy and convenient way to start building up savings for your goals—and sticking to them. It’s automatic, and you can adjust how much you want to contribute and how often, whether that’s on a weekly, bi-weekly, or monthly basis. It works for almost any budget, and once it’s set up, you’ll be saving money without thinking about it.

Investing in a PAC allows you to take advantage of dollar-cost averaging. That’s when you allocate a specific dollar amount ($100 per month, for example) toward the purchase of investments like mutual funds. With a consistent, long-term investment, dollar-cost averaging allows you to purchase more units when prices are low and fewer units when prices are high, potentially lowering the average cost per unit over time.

When you invest early and over longer periods in more growth-focused investments like stocks, you have more time to ride out the ups and downs that typically accompany these investments.

2. Plan effectively for your future

As a young investor, you want to make sure your investments are right for your goals (short and long term) and risk tolerance.

It’s important to remember that whatever age you are at when you are starting to invest, an advisor will help guide you through the process. Make an appointment with an advisor to learn the basics, create an investment strategy, and develop a plan that will help you work towards your investment goals.

3. Take advantage of employer-sponsored RRSPs and earn more “free money"

If your company offers an employer-sponsored retirement-saving plan with matching contributions, you could be losing out on decades of free money by not contributing.

Let's assume that you earn $50,000 per year and your employer matches your contributions, dollar for dollar, up to 5% of your annual salary. You contribute $2,500 and your employer contributes a $2,500 match every year. If you start making RRSP contributions at age 25, your employer contributions will add up to $100,000 (plus the growth on those contributions by the time you retire at age 65.

The sooner you start contributing to your company plan and taking advantage of the company match, the sooner your investment portfolio will grow with the help of those dollars.

4. Enjoy the benefits of compound growth

Compound growth helps build your savings over time. Investing $1,000 with a 5 percent annual rate of return will add up to $1,050 at the end of the year. With the same rate of return, $1,050 will grow to $1,103 during the second year. The benefits of compounding mean that the balance continues to grow — even if you never invest another dollar.

Remember that saving for your future is a long game: The sooner you start, the more time you have to benefit from compounding. As the investments you make now continue to grow, you're building a more secure financial future.

5. Take control of your future

Younger Canadians aren’t saving enough to fund their retirements. According to a Scotiabank poll of the 32% of Canadians who are not currently saving for retirement, almost half (45%) are between the ages of 18 and 35. Starting down the path toward a more secure financial future is a big advantage of investing early.

Investing isn't just about retirement. You can use other investment vehicles like Tax-Free Savings Accounts (TFSA), Registered Education Savings Plans (RESP), and non-registered investment accounts to help you build an emergency fund or save for big purchases like a car, the down payment on a house, or post-secondary education (for you or your future children).

6. Invest in peace of mind

In the Scotiabank poll, even though 68% of Canadians are currently saving, 70% are worried that they aren’t saving enough. For Canadians in their 20s and 30s, making smart investment decisions now could help you retire sooner.

A 30-year-old who contributes $100 per month to an RRSP can expect to have $160,000 saved for retirement at age 65; waiting until 35 to start investing the same $100 per month drops your total retirement account savings to $113,000; and delaying investing that $100 per month until age 50 will leave you with just $32,000 for retirement.

In another example of the impact of delaying saving for retirement, consider this situation:

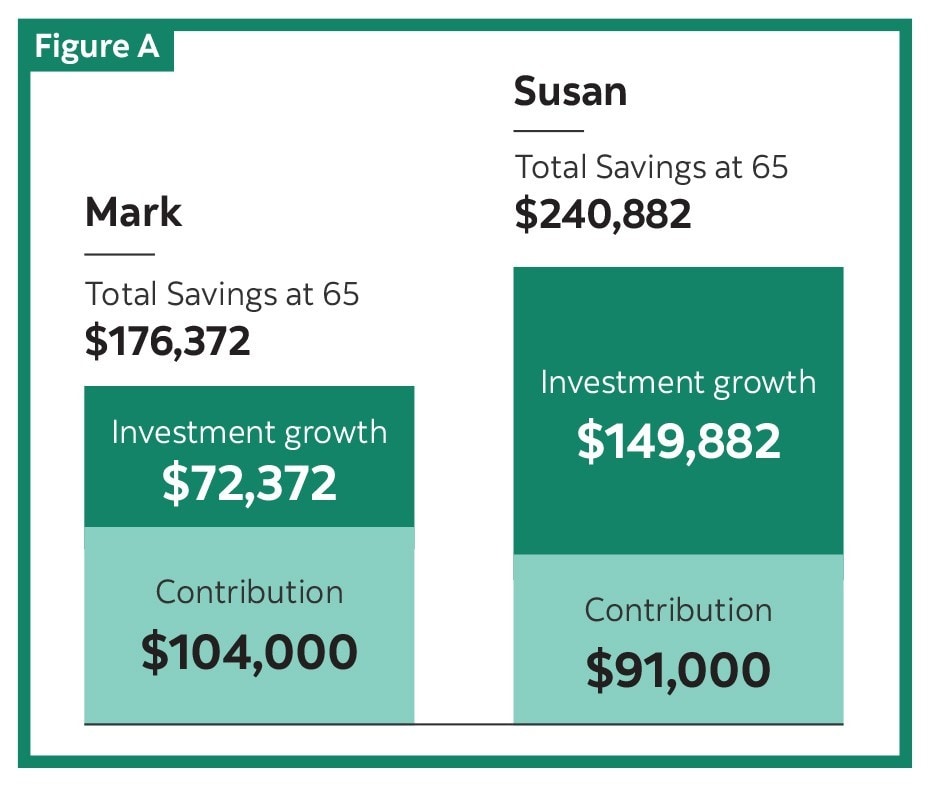

Susan and Mark would both like to retire at age 65. Susan starts saving $100 biweekly when she’s 30. Mark decides to put off saving until he’s 45 but will contribute twice as much – $200 biweekly – to help catch up.

At age 65, Susan will have contributed $91,000 in 35 years, while Mark will have contributed $104,000 in 20 years. However, Susan will actually retire with $64,510 more than Mark – even though she contributed $13,000 less.

With more time on her side to grow her savings (15 years more) and the benefit of compound growth, Susan’s $91,000 contribution grew to $240,882, while Mark’s $104,000 contribution grew to $176,372 ($64,510 less than Susan).

For illustrative purposes only and not intended to reflect an actual rate of return of the future value of an actual mutual fund or any other investment. The calculation assumes reinvestment of all income and no transaction costs or taxes. Illustration assumes a hypothetical rate of return of 5%, compounded annually. Amounts are rounded to the nearest dollar.

The earlier you start, the more time your money has to grow. Use a retirement calculator to determine how much you could save for retirement if you start working toward your long-term goals today.

Ready to start investing?

Make an appointment with a Scotia advisor and follow these six tips to make an investment plan and start investing early. Prioritizing investing when you're young will help put you on the path to a bright financial future.