Key takeaways:

For many people, the mere thought of investing is overwhelming. But you don't need to be a financial expert or have a lot of savings to start investing.

If you're thinking about investing but aren't sure where to begin, you've come to the right place. Read on to learn more about your investment options and how to get started.

Investing doesn't have to be complicated, but there are things you need to consider. Your first step is to take a look at your finances so you know what you can afford to invest. From there, you can set goals and decide what investments best align with them.

Figuring out how much money you can invest requires a simple budget. If you don’t already have one, you can create and then manage your budget using a tool like Scotia Smart Money by Advice+. This free tool for Scotiabank clients1 gives you access to money management features right in the Scotia app, making it easy to track your bills, monitor spending and manage your cash flow.

Don't forget to pay yourself first by committing to put away a certain amount each month into your investments. This can easily be done by setting up Pre-Authorized Contributions (PACs). You choose how much you want to contribute and how often, and then the amount you choose is taken from your chequing or savings account and deposited into your investment account on the schedule you specify.

If you don't already have an emergency fund, it's also a good idea to direct savings toward building one. An emergency fund is a safety net for unexpected expenses, like car repairs, a kitchen appliance breaking down and vet bills.

Once your budget is complete, subtract the combined total of your expenses and savings from your income. This is your discretionary cash flow — meaning money that you can use as you wish without affecting your budget — and it's perfect for investing.

Everyone who invests has a goal in mind, but not everyone has the same risk appetite. When you set your investment goals, look at how long you have to invest (your time horizon) and how much risk you're comfortable with (your risk tolerance).

You also want to consider your stage of life. Generally, new graduates have far more time to invest before needing to access the money than someone who’s close to retirement, for example. Consider other big milestones, such as whether you're looking to buy a home, and spending you foresee in the short-, medium- and long-term. Your investments should work toward these goals, not against them.

Investment recommendations that can help you reach your goals

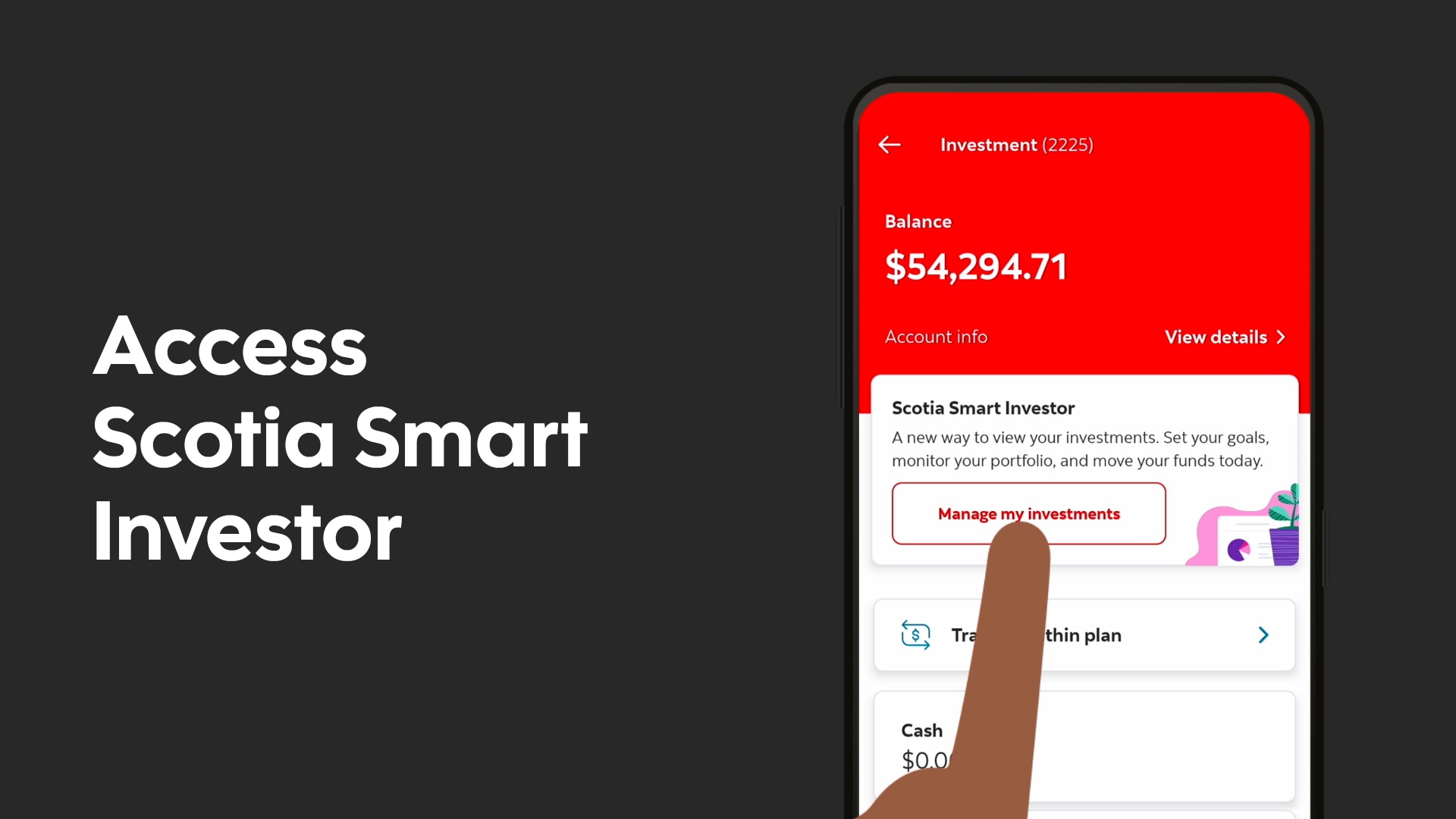

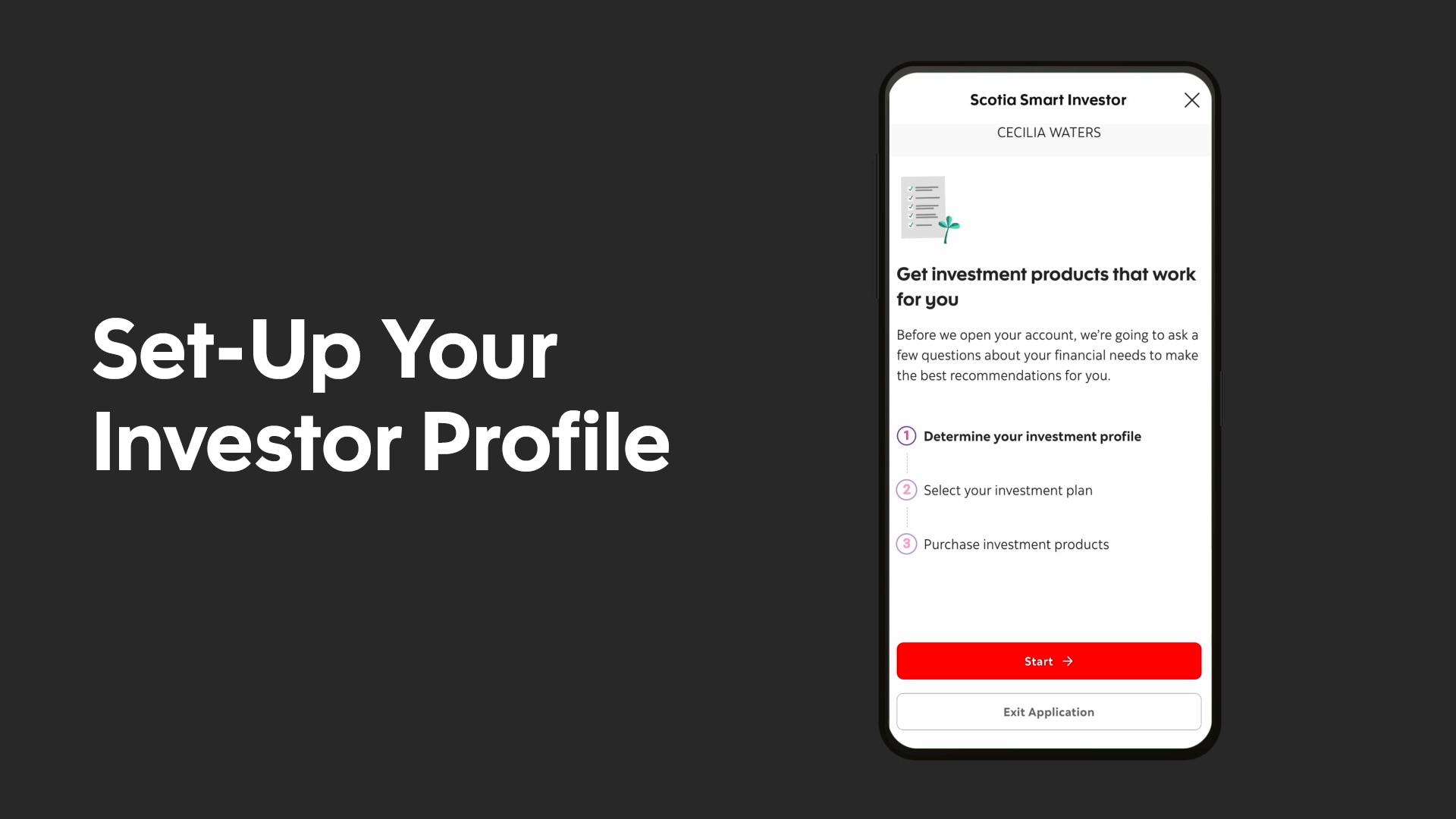

Scotia Smart Investor, which is available to Scotiabank clients with access to online banking, gives you the tools to set, track, and get real-time advice to manage multiple financial goals as your needs evolve. You can even set up RRSPs and TFSAs and purchase select GICs and mutual funds directly on the platform.

Scotia Smart Investor will walk you through the steps to get started with three short videos:

With Scotia Smart Investor, you won't be an investment newbie for long.

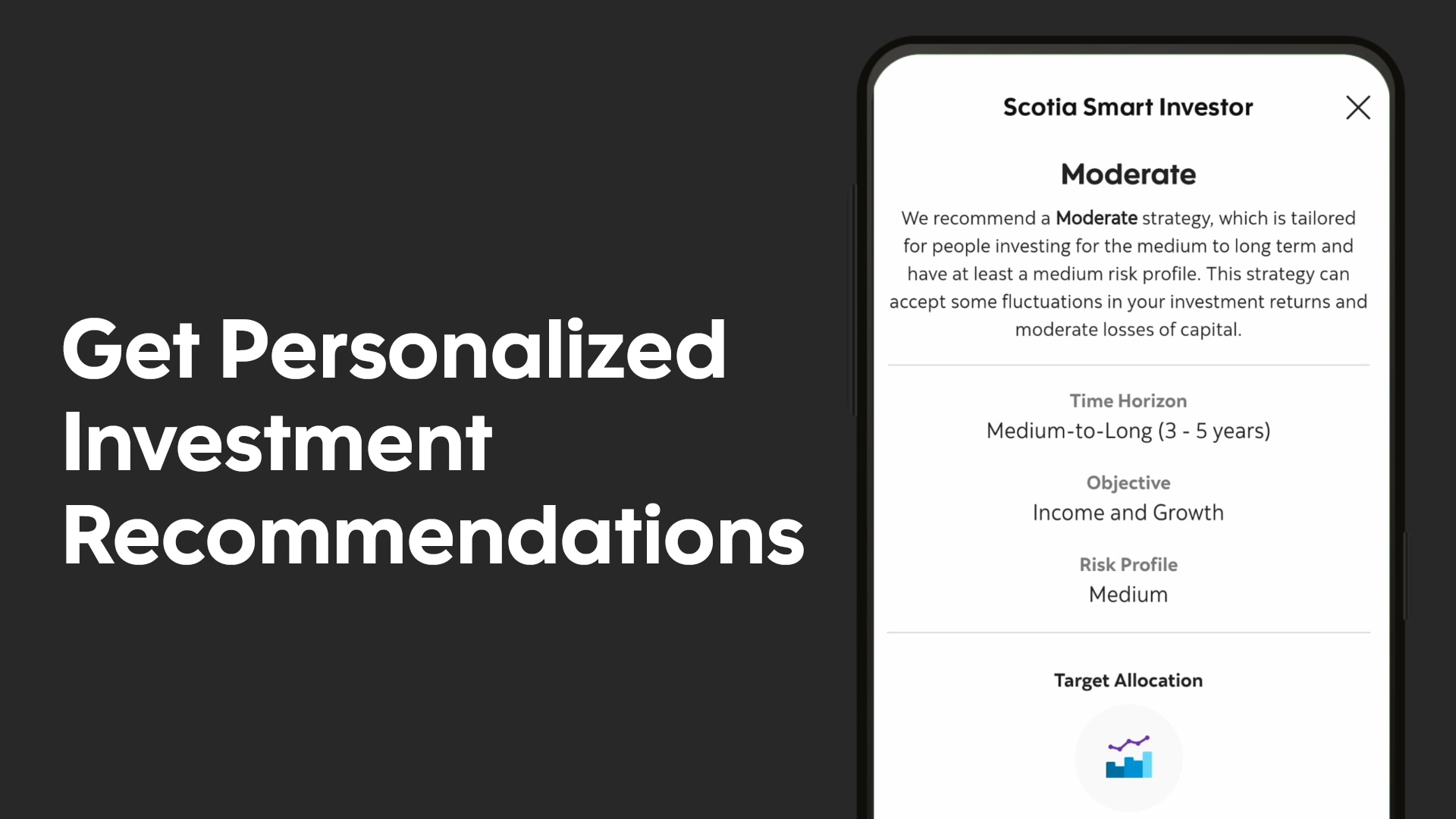

Next up is determining your risk tolerance. Do you feel comfortable with changes in the value of your investments if there's a possibility of higher returns? Or would you prefer to invest in more stable products with lower returns?

There are many factors to consider when you’re trying to find out how you tolerate risk, but the three main ones are:

- Time horizon — When you’ll need to access the money you’re investing

- Investment objectives — What you’re saving for

- Risk appetite – The degree of risk you’re willing to accept when investing

Typically, investing involves taking on some risk to generate higher return potential. Too much risk could mean higher fluctuations in your investment performance. On the other hand, too little risk could result in returns too low to achieve your goals.

If you're unsure about your risk tolerance, you can speak with a Scotiabank advisor. Together, you can work to find the right balance for you and your investments. You can also explore risk tolerance using Scotia Smart Investor.

Once you know how much money you can invest and your investment goals, it's time to learn about the major types of investments available. Here's where to start investing in Canada.

Mutual funds

A mutual fund is a professionally managed investment fund. It pools money from different investors to invest in various asset classes like stocks and bonds. It can also help generate long term growth and manage risk by investing in many different securities which might be difficult or time consuming to manager on your own.

Mutual funds are one of the most popular investment options in Canada. By investing in a range of different asset classes, geographies, industries and company sizes, mutual funds help you manage risk while enhancing long-term return potential.

The expression about not putting all your eggs in one basket exemplifies mutual funds. If one investment is down, another fund may offset those losses.

Guaranteed Investment Certificates (GICs)

Guaranteed Investment Certificates (GICs) work much like savings accounts — you earn interest on your funds without the risk of losing your original principal investment. But unlike many savings accounts, GICs aren’t meant to be touched for a certain amount of time. At Scotiabank, GIC terms range from 30 days to 10 years.

GICs are a secure way to save money and earn interest. You can invest knowing that your principal and, for most GIC types, interest are guaranteed for whatever term length you choose. GICs also offer you flexibility, since you can choose from a variety of options to find what works best for your needs and investment timeline. Learn more about GICs here.

Exchange Traded Funds (ETFs)

Similar to mutual funds, ETFs are pooled investments. The difference is that ETFs are traded on exchanges, like the Toronto Stock Exchange, and priced continuously throughout the day. ETFs can be passively managed to track the performance of traditional market indices, like the S&P/TSX Composite Index, or actively managed to achieve a specific investment objective.

Learn more about Scotia Exchange Traded Funds (ETFs) and investing with Scotia iTRADE.

Stocks

When you buy stock, you become a shareholder.

Put simply, the value of a company is divided and sold as shares — or stock — on the stock exchange. You can buy stocks individually or you might own stock as part of a fund. Buying individual stocks is considered somewhat risky because market fluctuations, current events or even public opinion might affect the value of a company.

Bonds

A bond is a type of investment that represents a loan between a lender (you, the bondholder) and the issuer (a corporation or government). When you buy a bond, you essentially loan money to an entity and receive interest payments in exchange. The riskier the issuer, the higher these payments may be.

Another investment choice is whether to put your money in a registered or non-registered account. Both can hold different types of investments, like mutual funds, GICs and High Interest Savings Accounts (HISAs), but a registered account is registered with the government while a non-registered account isn’t.

Registered accounts have certain terms attached to them, such as maximum contribution amounts. They may also come with benefits, such as helping you to reduce your taxable income and taking advantage of tax-free compound growth and additional government incentives.

You've likely heard of the most common registered accounts in Canada:

- Tax-Free Savings Account (TFSA)

- Registered Retirement Savings Plan (RRSP)

- Registered Education Savings Plan (RESP)

- First Home Savings Account (FHSA)

A non-registered account doesn’t have the same tax-sheltered status as its registered counterpart. This general investment account allows you to invest in a wide range of assets, but you’re required to pay taxes annually on income the account generates. Non-registered accounts can benefit your overall investment strategy, especially if you’ve maxed out a registered account, such as an RRSP or if you do not meet a specific eligibility requirement such as being a first-time home buyer for FHSA.

Once you’re ready to start investing, you can choose to work with an advisor or take part in self-directed trading.

Most financial institutions, like Scotiabank, have advisors who can help you. Together, you’ll create a financial plan with investments based on your goals, time horizon and risk tolerance.

With self-directed trading, you open an account and do the buying and selling of investments yourself. The Scotia iTRADE Learning Centre has tools and resources if you want to learn more.

Once you've set up your investments, it's a good idea to watch how they're performing. If you’re always aware of your financial situation, you can make changes as needed. This is especially important if you have changes to your lifestyle or investment goals, such as buying a home, having a baby or sending your child off to start their post-secondary education.

Now that you know how much money you can invest, your risk tolerance, your investment goals and the types of investment accounts available, you're ready to take the first step. Make an appointment with a Scotia advisor today.