Key takeaways:

Interested in revving up your savings for your first home? Opening a First Home Savings Account (FHSA) has great benefits. This savings vehicle gives eligible first-time home buyers in Canada a way to contribute up to $40,000 in the account toward their home purchase.

We break down how much you can contribute to an FHSA, including ways to use carry-forward amounts and spousal contributions.

In order to be eligible for an FHSA, you must meet all of the following criteria:

- Be a Canadian resident

- Be at least 18 or 19 years of age (depending on your province or territory)

- Be a first-time home buyer which means you or your spouse can’t own a home in which you lived at any time in the year the account is opened or during the previous four calendar years

You may, however, qualify for an FHSA if you purchased rental or income property and never lived in it.

Only the account holder is eligible to claim the tax deduction for contributions made to an FHSA. A family member can’t contribute to your account and take the tax benefits for themselves.1

Currently, individuals with an FHSA can contribute up to $8,000 annually. If you overcontribute to your account, there are tax consequences. Expect to pay a 1% tax each month on the highest excess FHSA amount in that month until that overcontributed amount is removed from the account.2

For example, if you contribute $6,000 to your FHSA in February, and then $4,000 in March, you'll have contributed $2,000 over the annual $8,000 limit. You'll then need to pay a 1% tax on that $2,000 each month until you correct the over contribution or until the annual contribution limit resets the following January, if you are within the $40,000 lifetime limit.

There are several available options for removing the excess amount. For example, you can make a taxable withdrawal from your FHSA, a designated withdrawal from your FHSA, or a designated transfer from your FHSAs to your RRSP or RRIF. Learn more here.

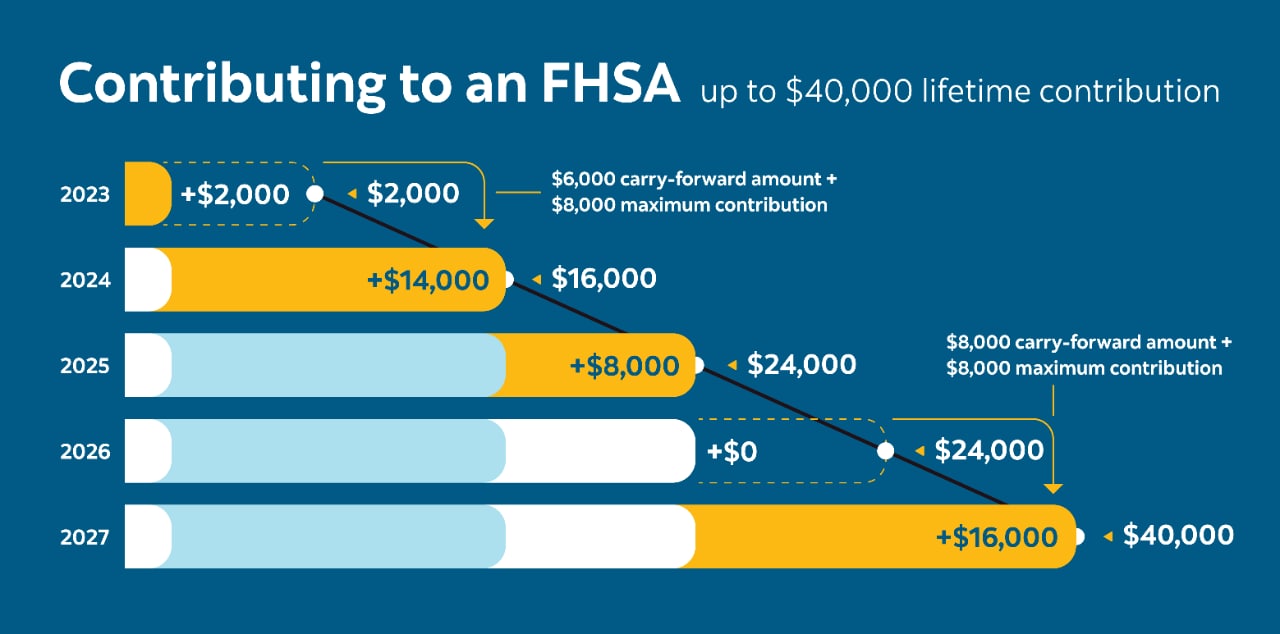

While over-contributing can be a costly, there's no penalty if you can’t contribute the maximum $8,000 each year. In fact, the unused participation room from a previous year can be carried forward and added to your annual contribution limit for subsequent tax years (up to an additional $8,000 per calendar year).2 This means your total contribution room will never exceed more than $16,000 in any given year depending on unused contribution carried forward. This allows you to add extra to your savings in the years when you have more disposable income or receive a tax return or an inheritance.

Here's how that might look: You're only able to contribute $2,000 in your first year of opening an FHSA. The next year you’ll be able to contribute up to $14,000 ($8,000 annual contribution limit plus $6,000 unused participation room from your first year) without penalty or loss of tax benefits.

You can contribute to your FHSA account for 15 years, until you turn 71, or until you reach the $40,000 lifetime contribution limit.1 Even if you don't think you'll reach the $40,000 milestone, the FHSA is still worth considering for saving toward a home purchase. Once you are ready to use your funds, you can withdraw up to $40,000, including any income earned, tax-free and use it towards your home purchase.

You must close your FHSA by December 31 of the year of the 15th anniversary of opening your first FHSA, the year in which you turn 71, or the year following the year in which you made your first Qualifying Withdrawal from your FHSA, whichever happens first.

The best reason to save for a home with the help of an FHSA is the tax benefit. But how much does an FHSA reduce my taxable income?

When you make contributions to your FHSA, you're eligible to claim a deduction on your income tax return for the year or a future year. The amount of the deduction is equal to the total contributions you made to your FHSA within the tax year, within your participation room. This means that your taxable income will be reduced by the amount you contribute to your FHSA.

The same rule applies for unused contributions that can be carried forward, even beyond the closure of your FHSA. Over-contributions to FHSAs, however, can’t be deducted and can impact how much you can deduct altogether.

Keep in mind that unlike an RRSP, contributions made to your FHSA during the first 60 days of the year aren't deductible on your previous year's income tax and benefit return. So, if you contribute on January 1, 2026, you're not able to deduct them on your 2025 tax return. If you wish to write off your contributions, you'll need to make them between January 1 and December 31.3

Yes, you can contribute to both FHSA and RRSP accounts to the maximum annual limits. Transfers made from your RRSP to your FHSA aren’t tax-deductible (since the amount was deductible when you contributed them into your RRSP) and transferring funds from your RRSP to an FHSA doesn't restore your unused RRSP deduction room.

In conjunction with a Qualifying Withdrawal from your FHSA, you'll also be able to withdraw up to $60,000 from your RRSP under the Home Buyers' Plan (HBP) for the same Qualifying Home purchase. However, you'll have to repay this amount back into your RRSP within 15 years. Note that the 15-year period begins in the fifth calendar year after the withdrawal. You don't have to repay your withdrawal from your FHSA.4

Your spouse or common-law partner can contribute to their own FHSA up to the lifetime limit and make a Qualifying Withdrawal toward the same Qualifying Home purchase, but unlike a spousal RRSP, there is no option to open a spousal FHSA. When it's time to buy your first home, you'll both be able to withdraw up to a combined $80,000 plus income earned in the account.

While your spouse or partner can have their own account, you can’t contribute to it or reap tax benefits on it.2 For example, if you make $100,000 per year and want to save $8,000 in your account and another $8,000 in theirs, you can only deduct your $8,000 contribution during tax time. Your taxable income would be $92,000, not $84,000.

You're not able to transfer your funds from your FHSA to a current or former spouse or partner without tax consequences. The only way to avoid tax issues is if the law proves that your spouse or partner is entitled to a portion of your fair market value (FMV) of your FHSA and the funds are transferred directly to that spouse or partner's FHSA, RRSP or RRIF. Withdrawing from your FHSA to give funds to your former spouse or partner will result in taxation.5

Since FHSAs are a newer tax-free savings vehicle started in 2023, it's important to have all of your questions answered so you don't over-contribute or miss out on the tax benefits.

Here are some more common questions and answers that can help you decide how much to contribute and when to withdraw from your FHSA.

The annual FHSA contribution limit is $8,000.

If you opened an FHSA account in 2025, you were able to contribute up to $8,000 for the year, but if you didn't contribute the full amount, you could carry forward the unused contribution room from 2025. Therefore, with the $8,000 contribution limit for 2026 and the $8,000 contribution limit from 2025, the maximum contribution you can make in 2026 is $16,000. The same rule applies for 2024 and 2025.

Yes, however, the annual and lifetime limits remain the same. If you open an FHSA and contribute $5,000, you can only contribute an additional $3,000 to another account that calendar year.

No. This account is only for first-time home buyers. If you sell your current home and rent for the next four years, you'll then be eligible to open an FHSA. If you own a rental property and have never lived in it, you can be eligible for an FHSA.

There's no minimum holding period.

The FHSA is an exciting program that can help turn your home-buying dreams into a reality. Even if you are still deciding if you want to buy a home or unsure you can contribute $8,000 per year, now is still a great time to consider opening an FHSA. Once you open your account, you have 15 years to contribute (or until you turn 71 years old, whichever happens first) and use it for your first home purchase. If you don't use the account toward a Qualifying Home purchase, you can transfer the funds to your RRSP without any tax implications.4

This article is provided for information purposes only. It is not to be relied upon as financial, tax or investment advice or guarantees about the future, nor should it be considered a recommendation to buy or sell. Information contained in this article, including information relating to interest rates, market conditions, tax rules, and other investment factors are subject to change without notice and The Bank of Nova Scotia is not responsible to update this information. References to any third party product or service, opinion or statement, or the use of any trade, firm or corporation name does not constitute endorsement, recommendation, or approval by The Bank of Nova Scotia of any of the products, services or opinions of the third party. All third party sources are believed to be accurate and reliable as of the date of publication and The Bank of Nova Scotia does not guarantee its accuracy or reliability. Readers should consult their own professional advisor for specific financial, investment and/or tax advice tailored to their needs to ensure that individual circumstances are considered properly and action is taken based on the latest available information.

Sources: