It can help you make money decisions with greater clarity, but it works best as a starting point, not a substitute for human advice.

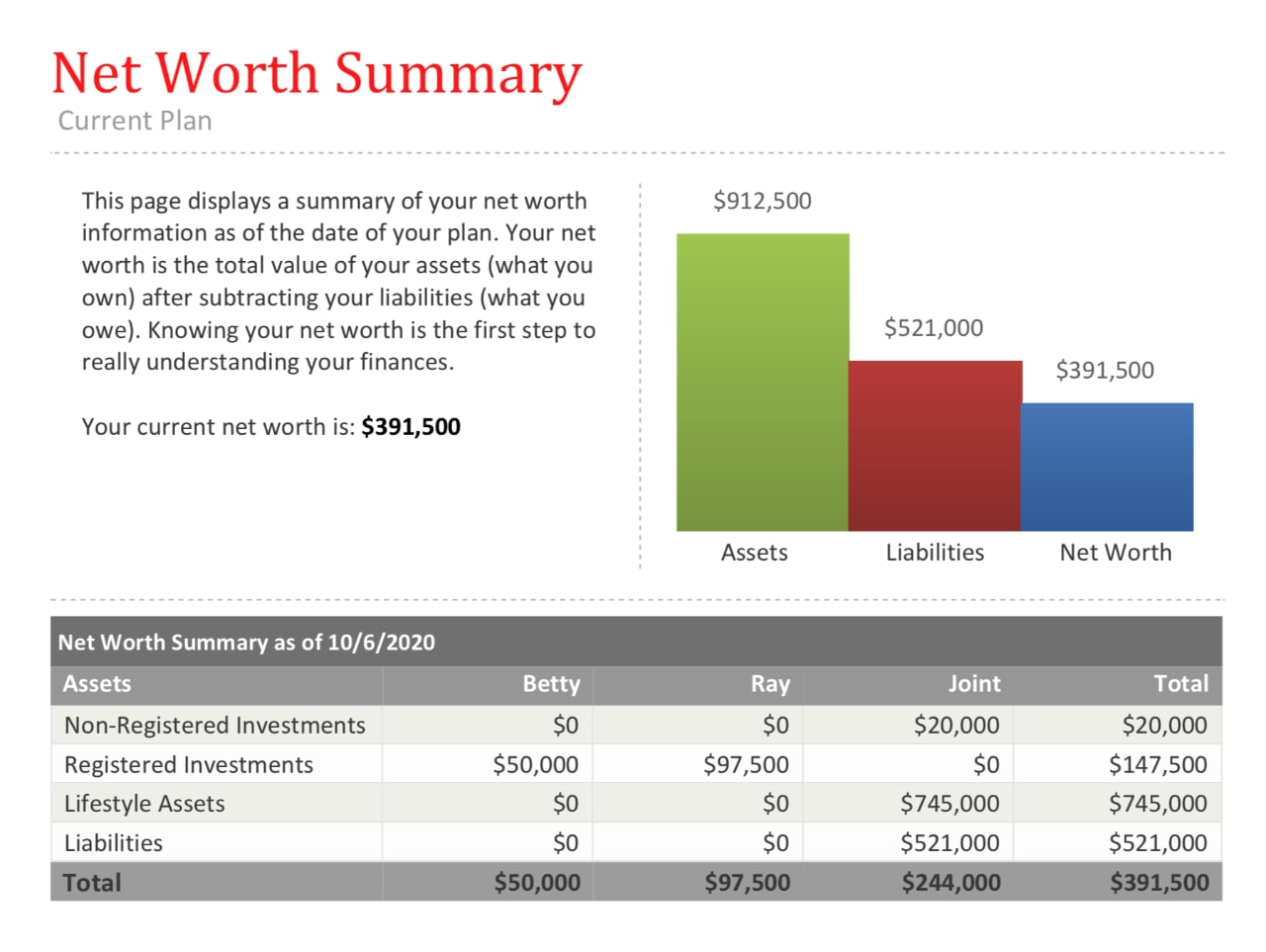

Your Net Worth Summary combines and classifies the financial assets you hold today. Many people have never been able to get a clear picture of their current status, and it’s essential to know your starting point so you can plan effectively for the future.

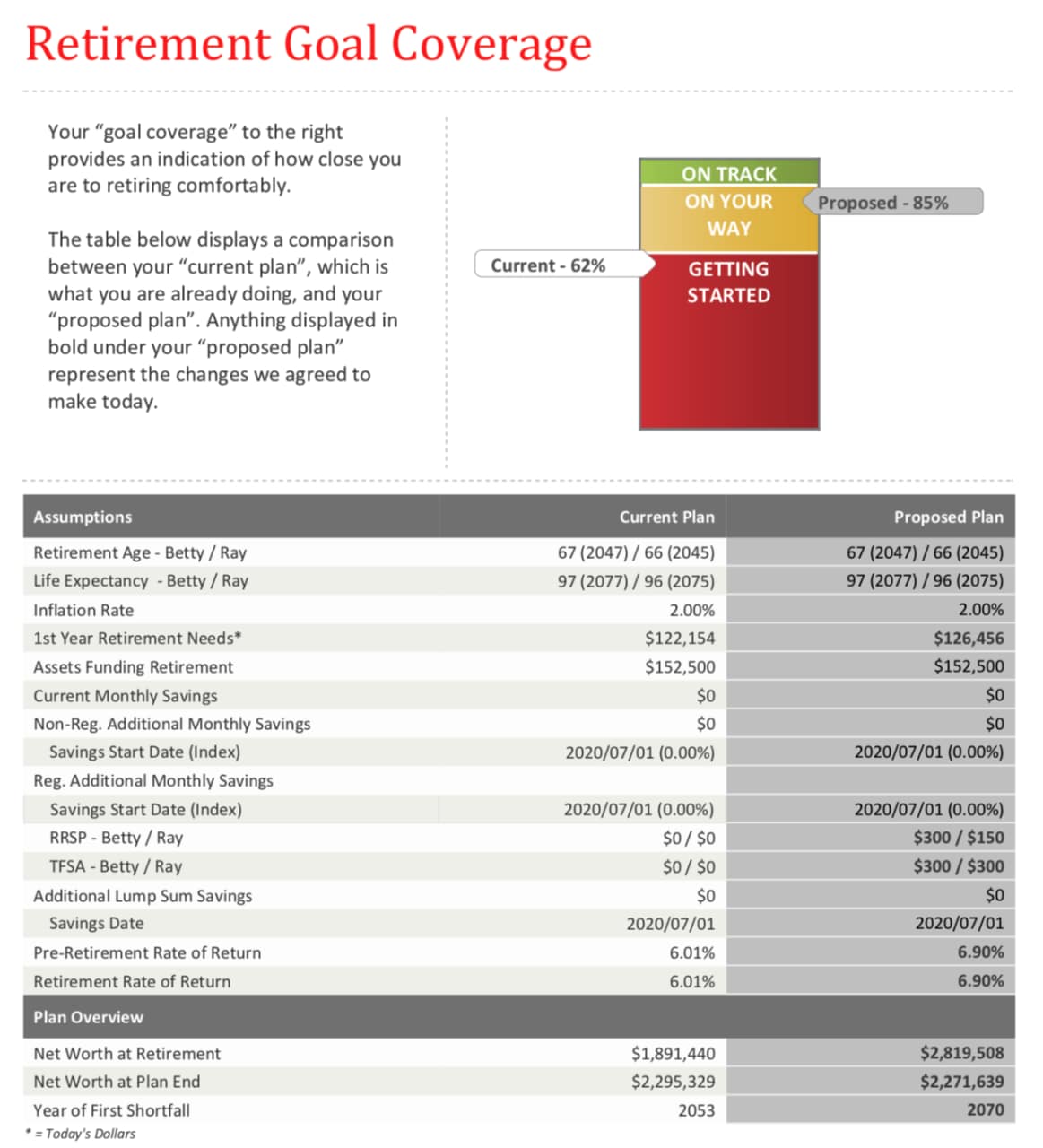

Retirement Goal Coverage ensures you have enough money saved to cover your retirement. After discussing your personal ambitions for your retirement, your advisor will calculate how far you are from achieving your goals. The plan your advisor will create with you aims to close that gap so you can feel confident and excited about your retirement.

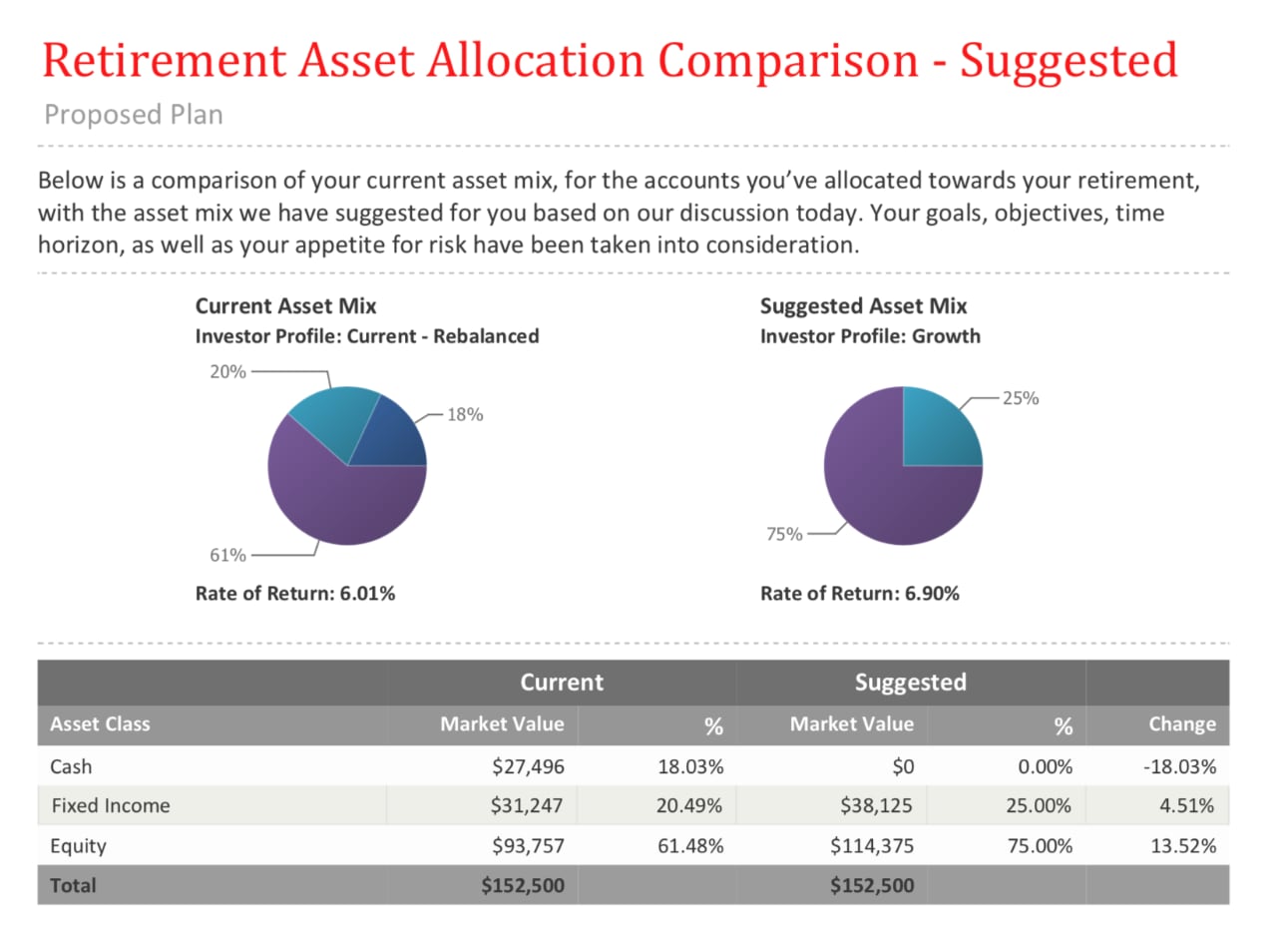

In Retirement Asset Allocation comparisons, your advisor examines where your money sits and looks for potential unused funds to re-allocate so that we can help achieve your financial goals. These suggestions form the basis of an Asset Allocation Comparison, which can show the path to help you reach your goals faster. Other goals, such as saving for education, are also covered.

Planning your financial future can feel overwhelming, but you don’t have to do it alone. A Scotia advisor can help you come up with a plan.

In this guide, we’ll explain the process, so you feel confident enough to ask questions and make informed decisions.

Book an appointment with an advisor and get your finances on track.

Whatever you want to achieve in life, a financial plan helps bring focus to your overall strategies to help you achieve them. These goals can be long-term, like retirement planning, or shorter term, like saving to buy a house.

Whether it’s growing your savings, cutting the interest you have to pay, or reducing debt, a financial plan can help you get better financial outcomes.

By analyzing your current financial position, we can help create a safety net for you and your family and plan for unexpected events in your life.

Working with a financial advisor will help you know your RRSP from your TFSA, and your PAC from your HISA. We’ll talk you through the often-confusing world of finance so you feel confident in the choices you make. And we’ll stick with you over the years so you always have a financial expert on your team through all life’s twists and turns.

A financial plan doesn’t give you only financial benefits. A major study of Canadians found that those of us who have a comprehensive financial plan have significantly higher levels of emotional wellbeing than those who just try to navigate one day at a time.**

A financial plan is a comprehensive approach to your financial future that you design with your Scotia advisor. Based on your personal aims, it gives you peace of mind that your finances are under control and headed in the right direction.

Scotia advisor Farah El-Masri explains the basics of what a financial plan is.

A financial plan is about more than just saving and investing. It’s a plan that helps you navigate your short, medium, and long-term financial goals towards a vision of your future. Understanding all of the elements that go into your plan will help you stay on track.

Review of your financial situation

Your Scotia advisor will take the time to get to know you and get a clear understanding of your needs and goals, which is the first step in helping you build a financial plan. This includes looking at things like your mortgage, debt, dependents, and all other assets and accounts.

Investing

When it comes to investing, a financial advisor can help you determine the right mix of ingredients, or assets, to create your personalized investment portfolio. These assets will be defined based on the conversation you have, and geared entirely towards your financial goals, your timeline, and your attitude towards risk.

Budgeting and cashflow

You can start to budget by taking note of your essential vs. non-essential spending, and create positive cashflow every month. Your essential spending is what you need to spend, while your non-essential spending is what you like to spend. Once you figure out what you need, you can plan for what you would like to have in the future.

Major purchase planning

Your plan can incorporate working towards buying a home, saving for a trip or other big purchases you want for you and your family.

Education planning

Whether you are saving for your kids’ college education, or you want to go back to school as an adult, we can consult on all the available programs to help you get there and maximize all the available government grants.

Retirement planning

How much should you save for retirement? What will your future health costs be? These questions are a good starting point when planning for retirement. Your financial plan can be tailored towards the kind of retirement you want to enjoy.

Managing debt

Managing your debt can help you feel more in control of your finances. The first step is figuring out how much you owe. From there, with the help of your financial advisor, you can come up with a plan to consolidate and reduce your monthly payments, pay off debt sooner, or even get mortgage-free faster.

Risk tolerance

Risk tolerance is the amount of risk you’re willing to accept when investing. At Scotiabank, we categorize risk into five levels: low, low/medium, medium, medium/high, and high. Low risk preserves the money you have, while higher risk can grow your investment in the long term. Finding the right balance will set you up to achieve your financial goals.

Government benefits

Many Canadians are entitled to claim from government programs they are not even aware of. A Scotia advisor will look for opportunities where any of these might apply to you.

Estate planning

Your estate is made up of everything you own. Making a plan for the transfer of your wealth can ensure that you provide for the financial future of your family and loved ones.

Here’s a cheat sheet to help you get comfortable with some more common financial terms.

Registered Retirement Savings Plan (RRSP)

An RRSP is a government-regulated investment account with special tax benefits to help you maximize your retirement savings.

Registered Retirement Income Fund (RRIF)

A RRIF is a plan that allows your savings to continue growing tax deferred while generating a steady stream of income during your retirement years.

Tax-Free Savings Account (TFSA)

A TFSA is a registered account that lets you grow your investments tax free. You don’t even pay tax when you withdraw funds.

Registered Education Savings Plan (RESP)

An RESP is designed to help you save for a child's post-secondary education. Any money deposited into this plan will grow tax deferred.

Guaranteed Investment Certificate (GIC)

A GIC is an investment product that keeps your principal investment safe and may have a guaranteed rate of return.

Mutual Fund

In a mutual fund, your money is pooled with other like-minded investors and is invested on your behalf by qualified investment professionals.

Pre-Authorized Contribution (PAC)

A PAC is a regular automatic payment that is withdrawn from your chequing account and deposited directly into your investment account. PACs are great as they help you to automate your saving without having to remember to do it every month.

Pension Plan

A retirement plan that requires an employer to make contributions to a pool of funds that are set aside for a worker’s future benefits.

Credit Score

A credit score is a number lenders look at to determine the probability that you’ll be able to pay back a loan. It’s based on your credit history.

High-Interest Savings Account (HISA)

This is a type of savings account that earns you more interest than a regular account.

Interest

Interest is the percentage of a loan that you must pay back in addition to the money borrowed. Interest is also earned when you deposit or invest so can add to your income.

Line of Credit

A line of credit is a flexible loan that you can access as needed and repay either immediately or over time.

Your Scotia advisor will be your partner in piloting your finances through every stage of life. They will help you organize your goals, and monitor and adapt them as your life changes, for your best financial future.

Farah El-Masri explains her role as a financial advisor and how the process of creating a financial plan works.

1. Your first conversation

Your advisor will use this time to get to know you, your partner and family, and learn about your financial situation. We will ask you questions about yourself to uncover your financial needs and what you're looking for in the future.

2. Start goal setting

Together with your advisor, you’ll work together to understand what your goals are, for your best financial future.

3. Putting your goals into action

Once you and your advisor have created your specific goals, your advisor will walk you through personalized options in order to achieve them. This may include opening new accounts, making changes to your borrowing accounts, reviewing investment options, and setting up automated savings plans.

4. Evolving your plan as your life changes

You’re building an on-going relationship with your advisor. After your initial meetings, you can agree how frequently you want to stay in touch to make sure your plan stays up to date and matches any changes in your life.

“My financial advisor did an amazing job in patiently explaining and helping me out with my investment and retirement plan options. He is extremely friendly and diligent and made my Scotia banking experience a breeze.”

“Martin was friendly and knowledgeable. He made me feel confident with how to manage and plan for wealth management and retirement.”

Time to start building towards your goals!

Over the course of your meeting(s) together, your advisor will gather your information and, when you’re ready, provide you with personalized recommendations and options to help you navigate your financial goals.

You’ll be asked to provide information on the following:

You can keep track of your goals through tools like Scotia Smart Investor and Scotia Smart Money

Your financial plan can start with a simple conversation. Book an appointment with a Scotia advisor near you.

Now that you know the basics, you’re all set to meet with a Scotia advisor.

For your personalized financial plan, find an advisor and book a meeting at a branch near you.

It can help you make money decisions with greater clarity, but it works best as a starting point, not a substitute for human advice.

Worried about high taxes when you retire? Find out how a spousal RRSP works and why it might be the perfect way to split your income.

Learn about the key features and differences between these popular investment funds and find the right approach to meet your needs.

** Financial Planning Standards Council, The Value of Financial Planning, 2012