Key takeaways:

Whether your child decides to go to community college, university, trade school or do an apprenticeship, you can invest in their future now by starting a Registered Education Savings Plan (RESP).

Higher education can be expensive. The average annual cost of post-secondary tuition in Canada increased 2.9% for the 2024-2025 academic year to $7,360 — and that doesn't include fees and cost of living expenses1. Putting a little bit of money into your child's RESP every month or depositing a lump sum every year can add up. Whatever your child wants to be when they grow up, they can pursue their dreams without as much worry about the cost of their education or taking out student loans.

Here's what you need to know about RESPs.

A Registered Education Savings Plan is a kind of tax-advantaged account similar to a Tax-Free Savings Account (TFSA). Essentially, the government encourages Canadians to save for their kids' education by providing them with perks.

For instance, by saving in an RESP:

- You have access to several government grants that boost your savings.

- Your money grows tax deferred until it's taken out to pay for qualified education expenses.

With an RESP, parents — along with friends and family members — can contribute up to a lifetime contribution limit maximum of $50,000 per child. The money is invested inside the RESP, allowing it to grow. Because contributions grow inside the RESP tax deferred, the student may end up with more money than was originally invested.

For example, if you put $10,000 into an RESP for an 8-year-old with dreams of being a veterinarian, and that RESP earned 4% per year over the next 10 years, your contributions could be worth $14,802.44 when they're ready to head to their campus of choice. That will pay for a lot of science textbooks.

Since the money you contribute to an RESP has already been taxed — like a TFSA — your savings won’t earn you a tax benefit.

Also, how your money grows in an RESP will depend on how you invest your funds. You can work with a Scotia advisor to decide what will work best with your financial plan.

If you decide an RESP is right for your child, the best time to start contributing to an RESP is as soon as possible. The longer the money can grow in the account, the more it may be worth when your child's ready for post-secondary. Of course, this will also depend on how your money is invested.

RESPs have a lifetime maximum contribution limit of $50,000 per beneficiary. How you contribute is up to you — as long as you don't go over the contribution amount.

There are many ways to contribute to an RESP. You can:

- Put away a certain amount each month, starting when your child is born

- Make annual contributions

- Deposit $50,000 in a lump sum if you have a sudden windfall

One thing to keep in mind: If you contribute too much, you'll have to pay tax on the over contribution and 1% per month until you withdraw it.

Unlike a Registered Retirement Savings Plan (RRSP), RESP contributions aren’t eligible for a tax deduction. But if you want to be eligible for matching government grants in a specific tax year, you need to make your contributions by December 31 of that year.

Once opened, you can make contributions to an RESP for up to 31 years, and it can stay open for a maximum of 35 years.

If you're interested in an RESP, there are two main types to choose from. Each offers a range of investment options:

- Family plan — Let’s you pool contributions for one or more children in the same family

- Individual plan — Let’s you name one beneficiary without age or relationship restrictions (it can even be yourself)

Depositing money into an RESP is simple. You can either deposit a lump sum in a branch or via online banking or mobile banking, or you can have Pre-Authorized Contributions (PACs) taken from your bank account on a regular basis.

Regardless of how you contribute, make sure you're maximizing your RESP.

While an RESP is a strong educational savings vehicle, there are some disadvantages to keep in mind:

- Taxes on RESPs are deferred but not eliminated. Your child will potentially have to pay taxes on the money when it's withdrawn to pay for educational expenses.

- If your child decides not to go to university, college or a trade school and they don't have a sibling who can use the funds, then you'll have to withdraw the funds and close the RESP. This means that you’ll have to return any government grants and pay withholding taxes on the accumulated earnings plus a 20% additional tax on top of that. This also applies if your child goes to university but doesn't spend all of the money in their RESP.

- You can only use RESP funds at qualified educational institutions. Programs must also last a certain number of weeks and be a certain number of hours per week.

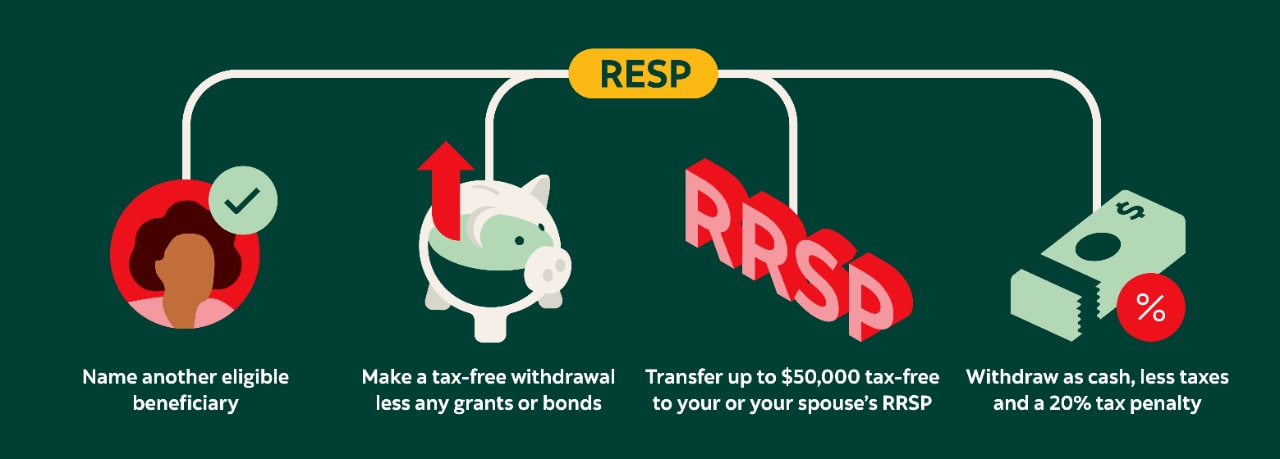

If your child has an RESP but opts against post-secondary, you have several options:

- You can name another beneficiary, such as another child, if they meet the conditions of your plan.

- You can make a tax-free withdrawal of your original contributions, but you must return any grants and bonds you received to the government.

- You can transfer up to $50,000 of the investment income, tax-free, to your RRSP or spousal RRSP if you have enough contribution room available.

- If you’re eligible to withdraw the investment income as cash, you’ll have to pay taxes on it plus a 20% tax penalty, unless it is transferred to an RRSP or RDSP, if there is room for contributions.

The good news is that federal government incentives are available to help boost your RESP savings, such as:

- Canada Education Savings Grant (CESG) — Matches 20% on the first $2,500 of your eligible contributions each year. Receive up to $500 per year per beneficiary under 18 up to a lifetime maximum of $7,200.3 Note: For beneficiaries who are 16 or 17 years old, there are restrictions: there must be a total of at least $2,000 in contributions in the account that haven’t been withdrawn or a minimum annual contribution of $100 made in the previous four years.

- Additional CESG — Depending on your net family income, you could receive an additional CESG of 10% or 20% on the first $500 contributed each year, up to an additional $100 per year per beneficiary under 18 towards the maximum lifetime CESG of $7,200.3

- Canada Learning Bond (CLB) — Depending on the adjusted income of their primary caregiver, children born on or after January 1, 2004, may receive the CLB. It offers a $500 initial deposit, then $100 per year until the eligible beneficiary reaches 15 years of age, to a maximum of $2,000. You don't have to contribute to your RESP to apply for or receive the CLB.

If you're wondering how hard it'll be to withdraw money from your RESP account when you're ready to start taking out contributions, there's more good news. It's easy.

Once your child presents proof of enrolment in a qualified educational institution, they can make withdrawals from their RESP.

The length of time between initiating an RESP withdrawal and seeing the money in your bank account varies by the financial institution. It could take a day to a week — or more — so don’t wait until the last minute.

Once you choose the best plan for your family — Scotiabank offers both individual and family plan RESPs — you simply set up an RESP like you would any other account. Be sure to bring your and your beneficiary's official government identity documents and you're done.

Then, all you have to do is figure out your contribution and investment strategy and help your child decide on their career path. (One of those things might be easier than the other.)