If you're a permanent resident versus a Canadian citizen, you might wonder how that impacts your life — and your finances — in Canada.

You already know that you can't vote or run for political office with permanent resident status, but what other limitations might you have?

The good news is that, for the most part, permanent residents and citizens are treated similarly in Canada when it comes to things like taxes, investment options and registered savings accounts.

We'll walk you through what you need to know about how both statuses impact how you're eligible to save, invest and plan for your best financial future.

A permanent resident is a newcomer who Canada has extended the ability to live and work in Canada permanently. A Canadian citizen has been confirmed as a Canadian citizen by the federal government like every other naturalized citizen.

The main differences are that permanent residents:

- Can't vote, hold office or have jobs that require certain kinds of security clearance

- Need to live in Canada at least 730 days in a five-year period or they can have their PR status taken away

- Aren't eligible for certain government services if they're sponsored newcomers without reimbursement from the person who sponsored them

- Have different eligibility requirements

- Have different travel documents and travel privileges

You should know: There are very few things that are different for permanent residents in Canada versus citizens.

Unlike many jurisdictions, the Canada Revenue Agency (CRA) bases income tax on residential status in Canada. It doesn't matter if you're a permanent resident, a citizen or here on a temporary work permit, if you're in Canada for a significant portion of the year, you will likely have to file Canadian income taxes. Consult with a tax advisor if you're unsure.

You also have to file income taxes if you have significant residential ties to Canada. The CRA takes into account whether you have a home, a spouse or dependents, personal property, Canadian bank accounts, health insurance in a Canadian province or territory or a Canadian driver's license.

In short, if you're a permanent resident living in Canada, you need to file your income tax return in Canada and report all your worldwide income. Luckily, Canada does allow offshore trusts for new permanent residents that can be used to shelter non-Canadian sourced income and capital gains.

Also, permanent residents can claim any available tax deductions and tax credits.

You should know: Residential status refers to whether you're a deemed resident of Canada, while permanent residency is an immigration status.

Like with income taxes, your eligibility to save money towards your retirement in a Registered Retirement Savings Plan (RRSP) is related to residential status not immigration status. You also need to have a Social Insurance Number (SIN) to open one.

An RRSP allows you to contribute up to 18% of your income in pre-tax funds towards your retirement. That reduces your tax burden and allows those funds to grow tax-exempt until you take them out in retirement.

You can contribute to an RRSP as a permanent resident if you:

- Are under the age of 71; note that while there's no age requirement for how old you need to be before opening an RRSP, many financial institutions will only open accounts when you reach the age of majority of that province or territory

- Earn an income

- Are a resident in Canada according to the CRA

However, since RRSP contribution amounts are based on your previous year's income tax return, you won't be eligible to make a contribution until after you've filed a tax return for your first year in Canada.

You should know: You can use your RRSP to save for a down payment on a home.

Like with RRSPs, you can contribute to a Tax-Free Savings Account (TFSA) as a permanent resident living in Canada and have an eligible Social Insurance Number (SIN). In 2023, every resident and Canadian over the age of 18 can put aside $6,500 in after-tax funds in a TFSA.

Unlike an RRSP, this savings account is available to anyone over age 18 whether they earn an income or not. For this reason, you're eligible to make a TFSA contribution during your first year in Canada, as long you meet the CRA's residency requirements.

You should know: Your contribution room to your TFSA rolls over to future years if you don't use it.

Canada has a few other registered savings accounts you might be eligible for. Here's what you need to know:

Registered Education Savings Plan (RESPs)

Permanent residents living in Canada are eligible to save after-tax money in RESPs for their beneficiaries to use to attend a post-secondary institution. The beneficiary doesn't have to be a resident of Canada to use RESP money, and it can be used for post-secondary education outside Canada.

However, only beneficiaries who are residents of Canada are eligible for top-up grants, like the Canadian Education Savings Grant (CESG) and the Canada Learning Bond, which are government programs designed to help families save more.

Registered Disability Savings Plan (RDSPs)

Permanent residents living in Canada are eligible to save after-tax money in RDSPs for beneficiaries to use to cover disability-related expenses. The beneficiary must be a permanent resident of Canada and will be eligible for government top ups through the Canada Disability Savings Grant program and the Canada Disability Savings Bond program.

Tax-Free First Home Savings Plan

Canada launched a new savings plan in 2023 to help both residents and citizens purchase their first home. It's a tax-advantaged savings account where funds can be used to put money aside to buy a home. These funds then grow tax-exempt until they're taken out to purchase a qualifying first home and can be withdrawn tax-free.

All Canadian residents over the age of 18 can open an account and make contributions up to $8,000 a year or a lifetime maximum of $40,000.

You should know: You can use your registered accounts to invest in a number of different kinds of investments. Learn more here.

Under many permanent residency entry requirements, applicants have to provide proof of funds. This means that you must have a certain amount of money in your account to support living expenses for yourself and your family members if they move to Canada.

Generally, these funds must be readily available and can't be borrowed from another person. They have to be available when the application is put through and when it's accepted. Once you've settled in Canada, you won't need to maintain that level of savings or get letters from financial institutions on an ongoing basis.

You also won't have to show proof of funds when applying for Canadian citizenship if you're already working in Canada and settled here as a permanent resident.

Another financial consideration for permanent residents relates to if a relative in Canada has sponsored them. In this case, your relative is financially responsibility for you for an agreed upon length of time. They'll need to repay any government assistance you require within that period since they're responsible for helping make sure you get a job, find a place to live and have the funds to support yourself.

The time period depends on your age, your relationship to the sponsor and where you live (it can be longer in Quebec).

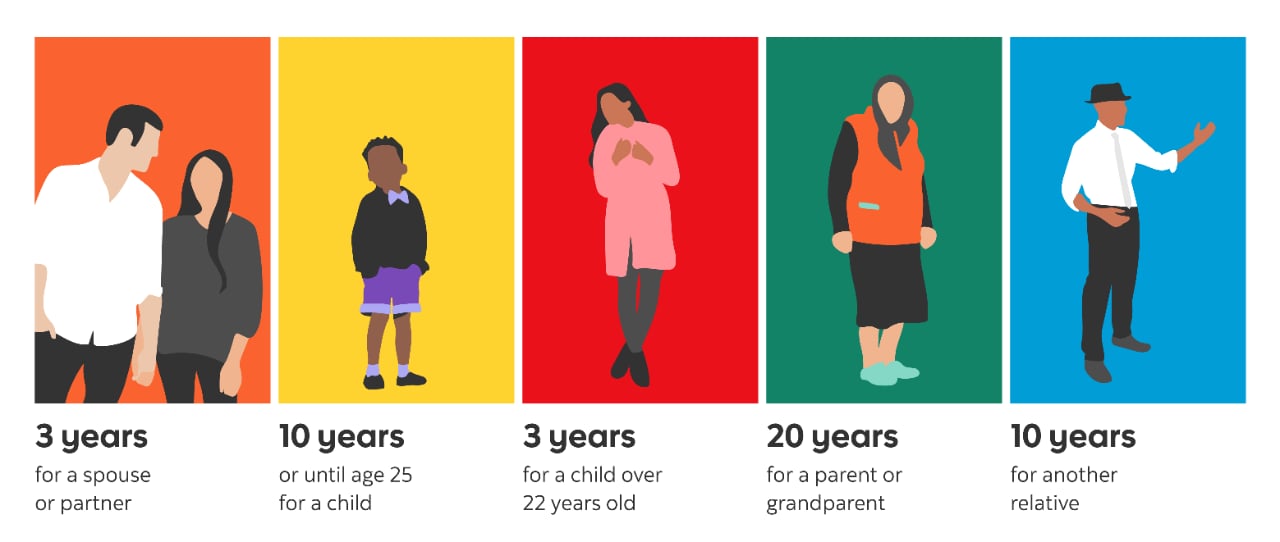

For example, the time period is:

- 3 years for a spouse or partner

- 10 years or until age 25 for a child

- 3 years for a child over 22 years old

- 20 years for a parent or grandparent

- 10 years for another relative

You should know: Your sponsor's obligation to provide you with support doesn't stop if you become a citizen. Regardless of your citizen status, they'll still need to provide for your financial wellbeing for the agreed upon time.

There aren't very many differences between being a permanent resident and a Canadian citizen when it comes to your finances. Most programs are available to all people who reside and pay taxes in Canada.

This is good news! You can take advantage of all these great programs rather than having to wait until you're eligible to apply for Canadian citizenship. This helps newcomers get a good start in Canada — and sets you up for success.