Key takeaways:

Your credit score might not cross your mind often — until it suddenly matters. Whether you’re applying for a mortgage, credit card or a personal loan, this three-digit number is one tool that helps lenders gauge how responsible you are with managing credit.

In Canada, a rating of 660 or higher is generally considered an acceptable credit score. The higher your score, the more confident lenders are in your ability to repay debt, and the better your chances of getting approved for credit on favourable terms.

But it’s not always as straightforward as it sounds. Let’s take a closer look at how credit scores are measured — and some tips on how to build a good credit score in Canada.

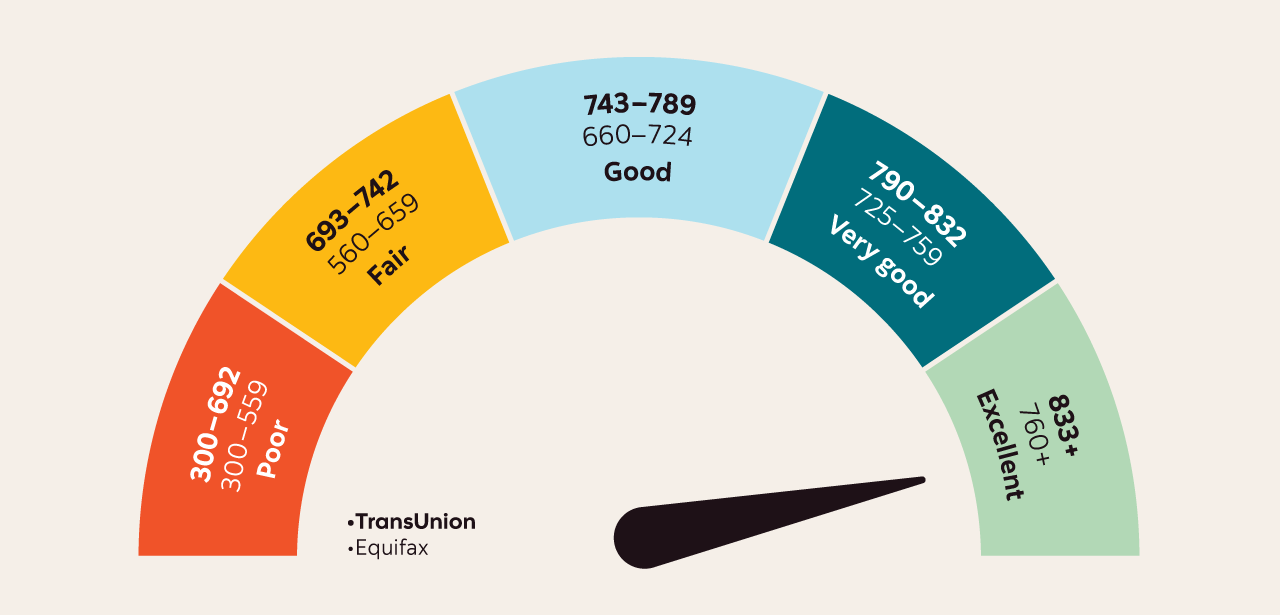

A credit score range is the scale lenders use to assess your creditworthiness. In other words, it signals how risky or reliable you are as a borrower. In Canada, that range runs from 300 to 900, with 900 being the highest possible score. Here’s how most lenders interpret the ranges:1

These ranges are based on Equifax data.

Note: TransUnion credit score ranges may look slightly different. Read on to learn more about how credit score ranges are calculated in Canada.

TransUnion Score Range |

Equifax Score range |

Rating |

What it means |

300-692 |

300–559 |

Poor |

Approval will be tough. Expect high interest rates if approved. |

693-742 |

560–659 |

Fair |

You might qualify for some products, but likely with higher interest rates. |

743 – 789 |

660–724 |

Good |

You’re considered a reliable borrower. |

790-832 |

725–759 |

Very Good |

Higher approval odds and more competitive rates. |

833+ |

760–900 |

Excellent |

The credit elite. You’re likely to qualify for the best interest rates and loan terms. |

Reaching an excellent credit score range is a great goal, but don’t stress about hitting a perfect 900 — it’s relatively rare. In general, anything above 660 puts you in a strong position with most lenders.

Did you know?

Your credit score isn’t just for getting a loan or credit card. When you’re looking to rent a place, landlords may also check your credit score to see how responsible you are with money. It helps them decide if you’re a good fit — along with a few other things.

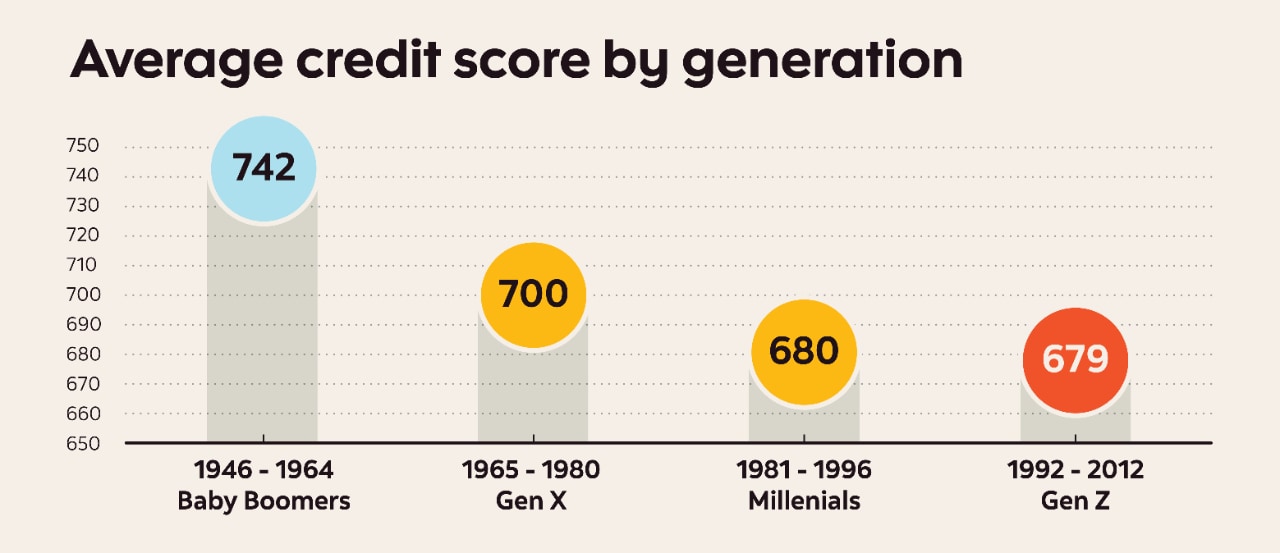

As the chart above illustrates, a credit score of 660 or higher is typically considered good in Canada. Scores between 725 and 759 are very good and anything above 760 is excellent.

That said, what’s considered “good” can vary by lender, product or even credit bureau.2 One lender’s “good” might be another’s “meh.” At the end of the day, a good score is the one that helps you achieve your financial goals.

As of November 2024, the average credit score in Canada was 760,3 according to the Fair Isaac Corporation (FICO®), one of the most widely used credit scoring companies in the world.

That puts most Canadians in the very good range. Don’t panic if your score is lower! There’s plenty you can do to increase your credit score — and anything above 660 is still considered solid.

Why do different websites show different credit scores? It’s because there’s no single, standard formula for calculating a credit rating. Credit reporting agencies and lenders may weigh certain factors differently, depending on the scoring model, industry or purpose.

In Canada, there are two main credit bureaus: Equifax and TransUnion. Each uses their own models and receives updates at different times. Not all lenders report to both bureaus, so your score can vary depending on who’s checking it, when and why.4

Did you know?

90% of top Canadian lenders and credit unions use FICO® Scores, which aren’t available directly to consumers.5 So, the score you see from your financial institution or a free service may not match the one a lender uses when making a credit decision.

Even if you’re not applying for credit tomorrow, your rating still matters. A higher credit score can lead to a few things you might want:6

- Lower interest rates: Qualifying for better rates on loans, variable rate credit cards and mortgages can help save you on interest over time. Cha-ching!

- Higher approval odds: It can boost your chances of getting approved for credit cards, personal loans, rental applications and more.

- Credit card perks may be better: With a higher score, you’re more likely to be approved for premium credit cards. These often offer better perks than standard cards with low or no annual fees. Premium cards may offer cash back, rewards programs (like Scene+™), travel and lifestyle privileges, lower interest rates on variable rate credit cards, higher credit limits and more.

- Stronger standing with landlords: A solid score may help you snag the rental you want, often with fewer conditions or deposits.

- Fewer hassles with utilities and phone plans: A higher score may help you avoid upfront deposits or extra paperwork when setting up services.

- Negotiating power: A good credit rating often gives you leverage to ask for better rates and terms.

Think of a good credit score as a financial VIP pass — it can save you money on interest, open doors and make life easier.

Your digits regularly rise and fall based on how you use and manage credit. Paying bills on time and keeping balances low? That helps. Missed payments or maxed-out cards? Not so much.

Here’s what can help keep your score in good shape.7

Length of credit history matters (the longer the better)

Think of this as your credit résumé. The longer you’ve had accounts open and handled them responsibly, the better it looks on your credit history. A solid track record shows lenders that you’re more apt to handle your finances wisely.

Credit score building tip: If you need to close a credit card, avoid closing the oldest one you have.

On the flip side, having little or no credit history could hold you back. Lenders have less information to assess how reliable you are with credit, which can make approvals harder or interest rates higher.

That’s why it pays to start building credit early, even if you’re a student!

Bill payment history

Potential lenders want proof that you pay your bills on time and in full. Late or missed payments (or paying less than the required minimum payment) can lower your score.

Credit score building tip: It’s a good idea to pay your credit card in full each month — or at least the minimum payment — on time. Setting up pre-authorized payments on the due date for at least the minimum amount due can help you avoid accidentally missing payments.

Credit utilization ratio

Maxing out your credit limit? That can ding your score. Lenders want to see that you’re using credit responsibly and not relying on it too heavily.

Keeping your usage below 30%9 of your total credit limit signals that you’re financially responsible. For example, if you have a $10,000 limit across all your credit cards and carry a $3,000 balance, your utilization is 30%. That’s about as high as you’ll want to go — and lower is recommended.

Credit score building tip: Staying well below your limit can help strengthen your credit score over time.

Types of credit you use

Having a credit mix (like a credit card, a line of credit and a mortgage) shows lenders you can handle different forms of borrowing.

Credit score building tip: Although having variety of credit is good, ensure you only take out credit you need and that’s suitable for your financial situation, not just for optics.

Recent credit applications

Applying for new credit can cause a temporary dip in your score because lenders may perform what’s referred to as a “hard check” on your credit report.

Credit score building tip: Planning to apply for a bigger credit product like a mortgage or line of credit? It’s best to avoid applying for new credit — like a credit card — close to or at the same time, as it could impact your approval chances.

Negative marks on your credit report

Accounts in collections, consumer proposals or bankruptcies can damage your score. Even if you’re accounts are in good standing, you should check your credit report at least once a year to make sure everything is accurate and there are no errors.

Credit score building tip: If you’re struggling to make minimum payments, call your lender and explain your financial situation before you fall behind. They may work with you to find a solution to keep your account in good standing until you’re back on your feet financially.

Read more

Check out this detailed guide to learn more about what affects your credit score

Checking your credit score is easy, usually free and doesn’t hurt your score. Here’s how:

- If you're a Scotiabank customer, you can check your score through the CreditView section in the Scotiabank mobile app or online banking.*

- Equifax Canada and TransUnion Canada can also provide a copy of your credit report, which gives a more detailed view of your credit history.

Since your credit score plays such an important role in your life, it’s a good idea to check it regularly. In fact, it’s one of the easiest ways to stay on top of your financial health.

Once you know your credit score, you can take simple steps to improve or maintain it. These habits don’t take much effort, but they could lead to big wins over time.

Tip

Why it matters

Pay on time, every time

Late payments can damage your credit rating. Make your payments in full and on time – even if if you can only make the minimum payment. This shows solid payment history and also helps avoid accumulating excessive debt.

Keep your credit usage low

Using less than 30% of your total credit limit helps demonstrate control. High balances or maxing out your credit accounts can signal risk to lenders.

Start building credit early

A longer credit history helps your rating. Even a low-limit credit card can help you build it.

Avoid too many credit applications at once

Each hard check can lower your score slightly.

Keep accounts open

Keeping older credit cards or lines of credit open can lengthen your credit history and increase your available credit, both of which support a stronger score.

Check your credit reports regularly

Reviewing your credit report regularly can help catch errors or signs of identity theft early.

Read more

Check out this guide on how to improve your credit score

Still have questions about your credit score? Check out our credit score FAQ section below.

Your credit score is more than a number — it’s a key that unlocks better rates, more borrowing power and greater financial flexibility.

With the right habits (pay on time, use less credit, don’t go wild with loan applications), you can build a score that opens doors — whether it’s to your dream home, a premium credit card or just peace of mind.

No gimmicks, no magic. Just smart choices and a little personal finance know-how. Now that you’ve got that, your credit rating is in good hands — yours.

Your TransUnion Credit Score and other TransUnion Credit Score services are provided by TransUnion Interactive, Inc. ("TransUnion") and are made available to you as a customer of The Bank of Nova Scotia (“Scotiabank”) at no additional charge. Accessing your TransUnion Credit Score will not impact your Credit Score. Scotiabank and its affiliates are not responsible for the TransUnion Credit Score or any of the information provided to you through TransUnion's Credit Score services.

To access your TransUnion Credit Score, Scotiabank will share your personal information such as name, address and date of birth with TransUnion so that TransUnion can identify you and provide your Credit Score. Your information will not be used or disclosed by TransUnion for any other purposes.

The TransUnion Credit Score service is subject to certain terms and conditions that can be viewed here Terms of Use.

Equifax Canada – What is a good credit rating?

Equifax, [https://www.equifax.ca/personal/education/credit-score/articles/-/learn/what-is-a-good-credit-score/]

Equifax Canada – Why Do I Have Different Credit Scores?

Equifax, https://www.equifax.ca/personal/education/credit-score/articles/-/learn/different-credit-scores/

Equifax Canada – Why Do I Have Different Credit Scores?

Equifax, https://www.equifax.ca/personal/education/credit-score/articles/-/learn/different-credit-scores/

Equifax – Seven Benefits of a Good Credit Score, Equifax, https://www.equifax.com/personal/education/credit/score/articles/-/learn/benefits-of-good-credit/

Credit report and score basics, Financial Consumer Agency of Canada, https://www.canada.ca/en/financial-consumer-agency/services/credit-reports-score/credit-report-score-basics.html