When it comes to your credit score, the day-to-day decisions you make play a role in determining your overall credit score. By taking the time to understand what will and will not affect your credit score, you can take steps to be a more credit-savvy consumer.

In this article

Your credit score is calculated based on the contents of your credit history and is a number between 300 and 900. The higher your number, the more creditworthy you're usually deemed to be by lenders.

A good credit score is 650 or above. This is important if you ever need to apply for credit in the future, such as a credit card, mortgage, or auto loan. That's because lenders look at your credit score as part of one of their criteria to determine if they're willing to lend to you, how much they're willing to lend to you, and what interest rates they'll offer.

If your credit score is lower, you might not get approved or get the best rates.

Generally speaking, the credit bureaus in Canada (TransUnion and Equifax) use five main factors in calculating your credit score. Although there's no specific formula to determine your credit score, here are some tips that can help.

Payment history

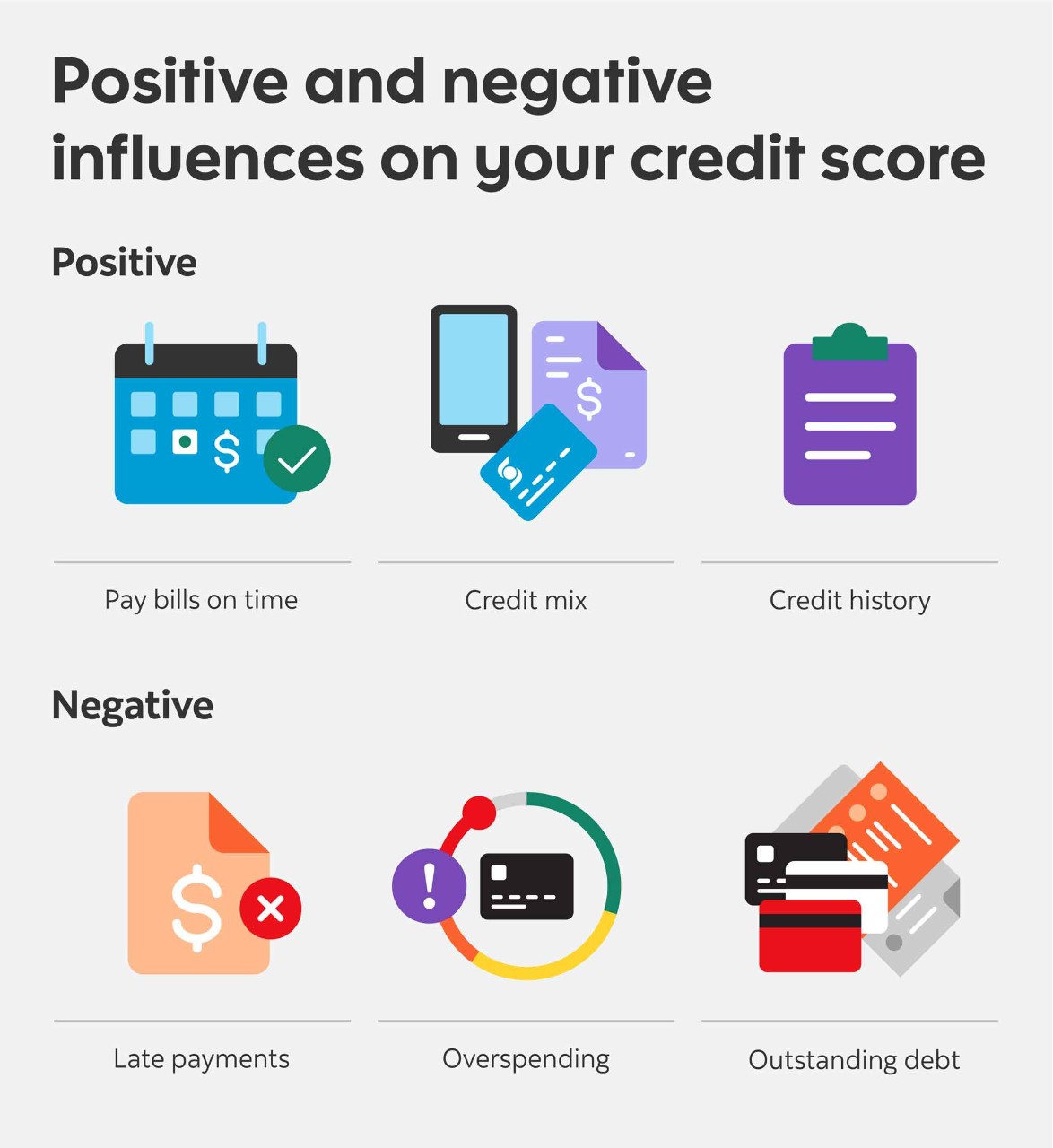

The most important factor that determines your credit score is your payment history. Lenders want to see that you've been paying your bills on time and making at least the minimum payment required. If you've missed payments, had late payments, or paid less than the minimum payment amount, that could negatively impact your score since they'll stay on your credit report.1

Credit utilization

Your credit utilization ratio is how much credit you're currently using of your credit limit relative to how much total credit you have available. For example, suppose you regularly charge $2,500 to all your credit cards and have a total credit limit of $10,000. In that case, your utilization ratio across all your cards is 25% ($10,000 /$2,500) Generally speaking, lenders prefer it when you have a utilization ratio of less than 30% overall.2 As such, your 25% utilization ratio is within that preference.

Types of credit

Having different types of credit available can be beneficial to your credit score since credit bureaus can see how you manage your money. Types of credit include cell phone bills, credit cards, consumer loans, and mortgages.

New loans

Quite often, when you apply for a new form of credit, what is referred to as a “hard check” on your credit bureau is performed by the lender. This type of “hard check” inquiry will likely negatively affect your credit score - regardless of whether you're approved or not - since it's a detailed look at your credit history. The lender might be concerned if you applied for multiple forms of credit from different lenders in a short period. That's because it could look like you're actively trying to seek credit - a sign that you may be having money issues. Note that soft checks, such as checking your credit score for free within the TransUnion CreditView service (available through Scotiabank)3, don't affect your credit score.

Credit history

As soon as you open a credit account, you start building your credit history. When you opened your first credit account, the age (time you’ve had it open) of your most recent account, and the average age of all your credit accounts could play a role in determining your credit score.

Although this may seem like a lot to be aware of, there's no reason to overthink things. Try your best to pay your bills on time and limit the amount of credit you're using.

Understanding the general criteria that affect your credit score is a good idea, but you'll also want to look at how individual decisions can affect things.

What can you do to raise your credit score?

If your credit score is not exactly where you want it to be just yet, there are a few things that could help you get there.

Pay your bills on time

One of the easiest ways to raise or maintain your credit score is to pay your bills in full and make sure those payments are received by your lenders/creditors on time each month. At the very least, you should pay at least the minimum amount required, so you're not picking up debt and if possible more than that minimum payment

Add to your credit mix

Having different types of credit may help also – having phone and utility bills that are paid on time can positively impact your credit score. If you qualify for a line of credit and balances are paid regularly, that can also help increase your score.

Build your credit history

It's a good idea to open a credit account as soon as you can since the length (time your account is open) of your credit matters. Getting a student credit card or putting your wireless phone account under your name are two ways to consider to start building or improving your credit score.

What can hurt your credit score?

In addition to the steps you can take to improve your credit score, there are certain actions that could hurt your score. Being a victim of fraud can also affect your credit score since thieves could use your information to try and open additional credit accounts or apply even if not approved. Every time they make an attempt (apply), it could lower your credit score. In addition, if they're successful at opening fraudulent accounts under your name, they could make expensive purchases. Since they would have no intention of paying the funds back, your credit score could drop quite a bit due to late and missed payments. While it's possible to fix the fraudulent activity on your credit history, it could take some time. Your first line of defence is to be vigilant against fraud by reporting suspicious activity immediately.

Overspending: Maxing out your credit cards, especially on a regular basis, can hurt your credit score since your utilization ratio (100% therefore > 30% recommended) would be high. In addition, you might struggle to make payments on time if you ever run into financial difficulties.

Outstanding debt: If you have any debt that you've been ignoring or has gone to collections, you'll want to address it right away since it can have a negative impact on your credit score.

Checking your credit score doesn't affect it, so it's never a bad idea to do so. You can get your free credit score check online via the Credit View service available through your Scotiabank mobile app. This Credit View feature is powered by TransUnion, so you're getting your credit score directly from one of Canada's credit bureaus.

Not only will checking your credit score keep you up to date about your progress, but you can also see potential signs of fraud. If there are any unexplained dips in your credit score, you could investigate them right away with the credit bureau directly.

By knowing what affects your credit score, it can help you to make smarter credit decisions. Be mindful about how you use your different credit accounts and take the steps to protect your information so you don't become a victim of fraud. Also, don't forget to check your credit score regularly to see how you're doing.