Key takeaways:

Preparing to send your child to post-secondary is an exciting — and emotional — milestone. As you help them get ready for the next big step, it's only natural to start wondering how to pay for university or college without overwhelming your family’s finances. From tuition fees to living expenses, there’s a lot to consider — and plenty of ways you can help your child secure the student financing they need to succeed.

Here are some answers to help you and your kid feel more informed and comfortable with the student financing process and the higher education journey ahead.

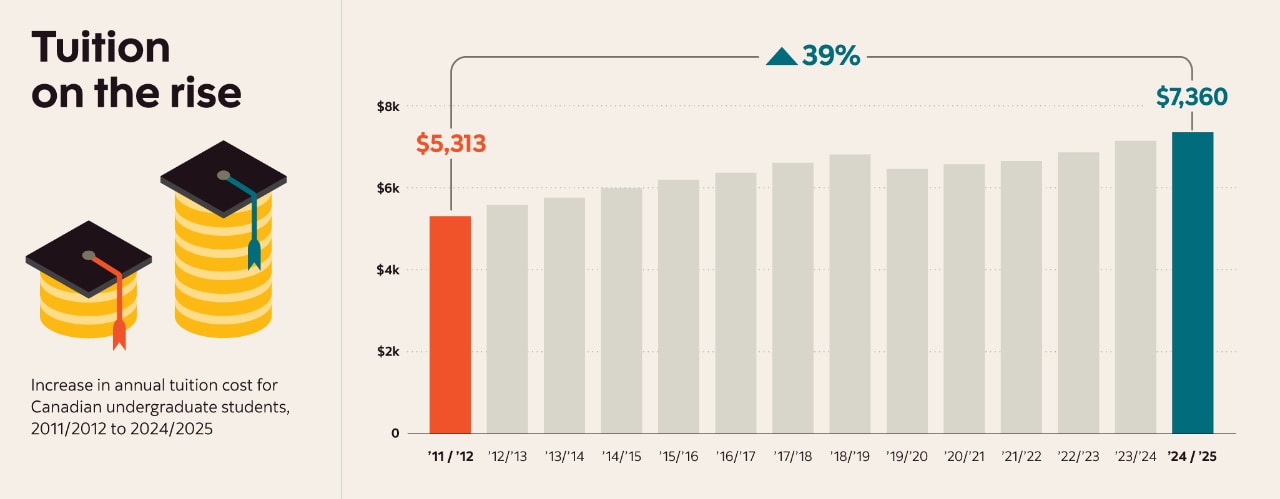

In 2024, the average cost of tuition for an undergraduate program in Canada was $7,360 per year.1 But this figure can vary widely depending on the province and program. For Canadian citizens and permanent residents, tuition fee payments typically range from about $2,500 to $11,400 per year, depending on the school and the program you choose.2

For example, if your child wants to enroll in a professional undergraduate program like dentistry or law, expect the costs to be substantially higher.

For international students, tuition is even steeper — averaging around $36,100 per year for undergraduate studies.3 Exchange rates may also affect the final cost for international payments.

On top of tuition fees, you should also budget for the cost of books and other course materials. At some post-secondary institutions, students can expect to spend between $1,000 and $3,000 per academic year.4

However, annual costs can vary depending on the post-secondary institution and the program — science, engineering, business and technology courses may require more expensive textbooks or specialized supplies. And this doesn’t include residence fees! Check with the office of student services for a breakdown of what you can expect to pay.

Cost of living can vary greatly depending on many factors, including whether your child plans to live at home, in residence or off-campus. If the goal is to save money, having your child live at home while they attend post-secondary can make a big difference.

However, if they plan to go to school out of province, they’ll need to budget for extra expenses, including residence fees. Following are some living costs to consider.

Accommodation

There are pros and cons to living on and off-campus. On-campus living is often more convenient and can help to reduce travel costs, but it comes with residence fees. In an off-campus rental, your child can reduce their costs by living with multiple roommates and splitting rent and utilities.

Where your child goes to school will also have a huge impact on the cost of their accommodation. An off-campus rental in Toronto or Vancouver is likely to be much more expensive than a rental in a small town in Nova Scotia or Saskatchewan.

Food

Some schools have a mandatory meal plan for first-year university students who live in their residences. A meal program can cost anywhere from a few hundred dollars to a few thousand dollars per semester. Those living off campus will have to budget for groceries and be ready to do their shopping and food preparation.

Transportation

A transit pass is often included in the cost of tuition. If your kid uses public transport, this is one way to cut costs. If your kid will drive to school, they must consider the cost of gas and parking in their overall budget. Students who plan to attend school outside of their home province or territory should also consider the cost of travelling home for holidays or summer vacations. Be sure to encourage them to inquire about student discounts whenever they book flights.

Entertainment

Being a student is a lot of work, but it can also be a ton of fun. Don't forget to leave some room in the budget for entertainment costs. This might include a little bit of money each month to pay for streaming services or going out for a bite to eat.

If you're wondering how your kid can finance their post-secondary education, there are a few options.

Registered Education Savings Plan (RESP)

If you invested in a Registered Education Savings Plan (RESP), you can help your kid put this money to good use. Once they enroll in a qualifying post-secondary program, you can use these funds to cover tuition payments, residence fees or other education-related costs.

Also read

Learn more about RESPs and how to make most use of this program.

Government grants and student loans

If you're looking for support beyond a RESP, the Government of Canada offers grants and student loans to eligible part-time and full-time students through the National Student Loans Service Centre (NSLSC). In Canada, students apply for these loans through their province or territory. For example, in Ontario, students apply through the Ontario Student Assistance Program (OSAP), which combines both provincial and federal funding into a single application.

Did you know?

Federal student loans now carry 0% interest after graduation.

If your child applies for financial aid, they’re automatically assessed for government grants, which don’t need to be repaid. However, student loans must be repaid after graduation. Make sure your child knows about repayment deadlines to avoid late fees or late payment penalties. Thanks to recent changes, federal student loans now carry zero percent interest after graduation, making repayment more affordable.

Student grans ad student loans eligibility

Eligibility for government grants and student loans is based on several factors. How much they qualify for will depend on different aspects, including:

- Province or territory of residence

- Family household income (how much you make can impact how much your kid can receive in student financing)

- If the applicant has dependents

- Tuition fees and living expenses

- If the applicant has a disability

Based on these factors, your kid may receive enough money to cover their tuition fees and living expenses. If they don't get enough, there are other options available to fill the gaps, such as private student loans.

In 2024, the average cost of tuition for an undergraduate program in Canada is $7,360.1

Scholarships, bursaries and university financial aid

In addition to government funding, many universities and colleges may offer their own scholarships, bursaries, grants and financial assistance programs. These programs are typically based on merit, financial need or a combination of both, and usually require a separate application through the school's student services or financial aid office.

Encourage your child to research the school's financial aid options early and apply before the deadlines — it’s a great way to reduce costs without taking on extra debt.

Private student financing

Private student loans are typically issued by banks and other financial institutions. A popular type of private student loan is a student line of credit.

A line of credit works similarly to a credit card in that you can borrow money repeatedly up to a certain amount. Like a credit card, your child can use it to borrow money when they need it, pay it back and then borrow again up to their credit limit.

Products like Scotiabank’s ScotiaLine® Personal Line of Credit for Students offer flexible payment plans and interest-only installments during school, with a 12-month grace period for principal payments after graduation (monthly interest payments only).5

Your child can use a line of credit to pay for expenses related to their post-secondary education, including tuition fees, books, residence fees, food or transportation.

There are a few notable differences between a student loan and a student line of credit:

|

Government student loan |

Private student line of credit |

Loan amount |

There are loan limits on the maximum amount of combined federal and provincial student loans that can be received |

You can often borrow more money than you can get with a government student loan |

Co-signer requirement |

No co-signer required |

A co-signer may be required without a strong credit history |

Repayment amount |

Comes as a lump sum amount that must be repaid in full when your child finishes school |

Your child is only responsible for repaying the amount of money they use Some products, like the ScotiaLine® Personal Line of Credit for Students, offer deferred principal payments, with interest-only payments while your kid is still in school and for 12-months post-graduation.5 [NK1] [DS2] As these terms differ from one product to another, it’s good to compare a few options |

Interest payments |

No interest is charged on student loans |

Interest payments begin as soon as they borrow the money |

Access to repayment assistance |

Eligible to apply to the Repayment Assistance Plan (RAP) |

Not eligible for RAP |

If you’re interested in learning more, check out our guide to student loans in Canada.

Beyond the different student financing options available, there are other ways to support your child in their dreams of obtaining a higher education.

Open a student account

Encourage your child (or help them) to set up a student account early. This ensures they have a secure place to store any funds from scholarships, grants, bursaries or student loans.

You can check out Scotiabank's Preferred Package for Students and Youth, which is designed specifically for student life.6 For eligible account holders, this account offers no monthly account fees, unlimited debit and Interac e-Transfer† transactions7 and Scene+™ points earned on everyday purchases.

Set up international students for success with a Canadian bank account

If your child is an international student, opening a Canadian bank account simplifies things like international money transfers and managing day-to-day expenses.

Help set up payment options

Make sure your child understands payment options, including online banking, international payments and payment processing times (which can take a few business days). They should also know how to add the school as a payee using their student number and account number to avoid missing a due date.

Apply for a student credit card

You can assist your kid in signing up for a student credit card and give them advice on responsible credit card use so they can avoid unnecessary debt. Scotiabank offers some no-annual fee credit cards10 you could consider, and on select premium credit cards Scotiabank's Preferred Package for Students and Youth account holders are eligible for an ongoing $40 annual fee rebate (on eligible credit cards)11 It’s a great way for your child to start building a strong credit history while getting rewarded for their everyday spending.

Assist with applications

You can help your child secure the student financing they need by assisting them with applications for student loans, bursaries and grants — or by exploring a private student line of credit if additional funding is required.12

- Always check with your post-secondary institution for specific payment options, accepted methods, deadlines and any extra fees that may apply.

- Most schools allow online payments via online banking.

- Payments can also be made in person at your local bank or using a money order.

- Credit card payment may be accepted, but a convenience fee might apply.

- Make sure you allow time for payment processing to avoid missing fee payment deadlines — some schools need up to three business days.

- Watch out for late fees if payments are delayed.

- Schools will typically issue refunds if there’s an overpayment on the student pay account.

Getting ready to head off to post-secondary is a big deal — not just for your child, but for you, too. It’s an exciting time, but it can also feel overwhelming if you’re unfamiliar with the ins and outs of scholarships, grants and student loans. Start researching different schools and funding options early to give yourselves plenty of time to make informed decisions, build a realistic budget and start saving for their education.

Effective starting on and after June 22, 2026 (the “Effective Date”), clients who have a Preferred Package account (“Account”) will receive an annual fee rebate of $40 (“Annual Fee Rebate”) on one Eligible Card Account where they are the primary cardholder (“Eligible Card”), beginning on the first Anniversary Date after June 22, 2026 (and on each annual Anniversary Date thereafter), provided all of the following conditions are met: (i) there must be at least $15,000 in Qualifying Purchases posted to the Eligible Card Account in the 12 monthly statement periods prior to the month in which the Eligible Card Account’s annual fee is charged to the Eligible Card Account (the “Annual Anniversary Spend Amount"), and (ii) both the Eligible Card Account and the Account must be open and in good standing at the time the Annual Fee Rebate is applied. The Rebate should appear on your Eligible Card statement approximately on, or within the first two statements after the annual fee is charged to the Eligible Card Account.

The first-year annual fee(s) charged on your Eligible Card Account after the Effective Date is not eligible for an Annual Fee Rebate. The Annual Fee Rebate applies, even if you opened an Eligible Card Account prior to the Account Open Date.

Each Account will only receive one Annual Fee Rebate regardless of the number of accountholders on the Account or Eligible Cards held or opened on the Eligible Card Account. If you are the primary cardholder of multiple Eligible Cards, the Annual Fee Rebate will be applied to the annual fee that is charged first on an Eligible Card after the Account Open Date if you meet the Annual Anniversary Spend Amount.

If your Eligible Card Account has an annual fee(s) that is greater than the amount of the Annual Fee Rebate, you are responsible for any difference in annual fee(s) after the Annual Fee Rebate is applied. All other fees and charges applicable to the Eligible Card Account continue to apply.

The Annual Fee Rebate is subject to change and cannot be combined with any other offer including an annual fee rebate or waiver offer. Annual fees, rates and other features for Eligible Cards are subject to change. We may limit or revoke the Annual Fee Rebate(s) without notice if we believe there is suspicious or fraudulent activity, if the offer is being abused, or if you receive an Annual Fee Rebate in error.

“Account Open Date” means the date that the Account is opened.

“Anniversary Date” means the date that is one year after the annual fee is first charged to your Eligible Card Account and every 12 months thereafter.

“Eligible Card Accounts” are currently the Scotiabank Gold American Express®, Scotiabank Passport® Visa Infinite +* and Scotia Momentum® Visa Infinite +* credit cards. Eligible Card Accounts are subject to change.

A “Qualifying Purchase” is a Purchase (as defined in your credit agreement for your Eligible Card Account) that is posted to your Eligible Card Account, less any refunds, returns or other similar credits on your Eligible Card Account. Qualifying Purchases exclude cash advances (including balance transfers and cash-like transactions), interest charges, fees and payments posted to your Eligible Card Account.