As prices for goods and services soared during and after the COVID-19 pandemic, we heard the term “inflation” often, with the inflation rate eventually hitting a peak at 8.1% in June 2022.1 Since then, the pace of inflation has begun to slow down, providing a bit of relief for weary consumers.

But as the rate of inflation decreases from its recent highs, you may have come across the term “deflation,” which describes a different type of environment. As we examine both these terms, their causes, and the different ways in which they can affect your financial future, we’ll also look at ways of managing both and limiting any negative impacts.

Please note that while there are different variations of inflation and deflation (such as hyperinflation, disinflation and stagflation), this article will focus exclusively on the key concepts of inflation and deflation.

| Inflation | Deflation |

|---|---|

| Prices of goods and services increase | Prices of goods and services decrease |

| Purchasing power decreases (your money buys less) | Purchasing power increases (your money buys more) |

| Can occur when the demand for goods and services exceeds supply | Can occur when the supply of goods and services exceeds demand |

| Government response may be to decrease government spending and/or increase taxes | Government response may be to increase government spending and/or decrease taxes |

| Central banks may increase interest rates. Higher rates make borrowing more expensive, helping to slow demand for goods and services, putting downward pressure on prices. | Central banks may reduce interest rates. This has the opposite effect of interest-rate hikes, stimulating demand for goods and services and consumer spending. |

Put simply, inflation is an increase in the price for goods and services. While a bit of inflation is considered beneficial for the economy, inflation becomes a concern when it exceeds the central bank’s target rate. In Canada, the Bank of Canada (BoC) aims to keep annual inflation around the 2% mark, with a target range of 1 to 3%.2

You’ll often hear inflation described by economists as “too much money chasing too few goods.” It comes back to the law of supply and demand. In this case, excess money supply (often fueled by low interest rates) increases demand for a limited supply of products, driving up prices.

How is inflation measured

The Consumer Price Index (CPI) is one of the most widely known economic indicators in Canada. The CPI compares, over time, the cost of a fixed basket of goods and services purchased by consumers – such as food, housing and clothing – which provides direct insight into consumer price inflation or deflation. Essentially, the percentage change in the price of the basket of goods and services is used as an estimate of the amount of inflation in the economy overall.

- Demand for goods and services exceeds supply

When demand exceeds supply, prices rise because consumers are willing to pay more to obtain goods or services. Think of the pandemic, when lockdowns and gym closures increased demand for home gym and office equipment, sending prices higher.

- Low interest rates

When interest rates are low, people can borrow money much more easily. The excess money in circulation, in turn, can create greater demand for goods and services, and companies may respond by increasing prices.

- Increasing production costs

When the price of raw materials increases (whether it’s gasoline, wheat, minerals or even labour), companies may pass on their increased cost to consumers, resulting in higher prices.

- Decrease in purchasing power

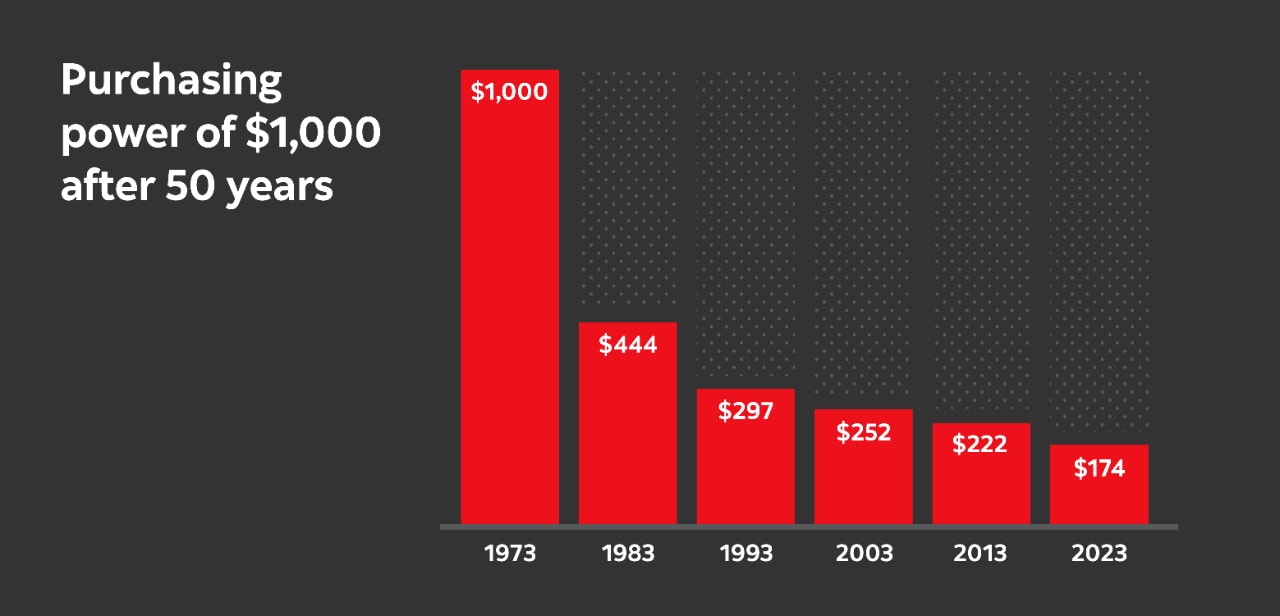

Inflation erodes purchasing power – in other words, when prices rise, your money buys less. See Illustration A, which shows the diminished purchasing power of $1,000 over the last 50 years.

Illustration A

Source: Statistics Canada. For illustrative purposes only.

Core Canadian CPI from December 31, 1973 to December 31, 2023.

- Higher interest rates

The Bank of Canada has a relatively limited toolkit in the fight against inflation. Their “go-to” move is usually to gradually raise interest rates, making it more expensive to borrow money. This can help to cool an overheated economy. For consumers, it makes purchases that require borrowing (such as a home, new car or major appliances) more expensive.

- Slowing down of economic growth

Sometimes central banks “overcorrect”, meaning they raise interest rates too much, or for too long. In some cases, this may cause the economy to grind to a halt and tip into recession, also known as a “hard landing.”

How does inflation impact your long-term savings?

The negative impact that inflation has on your savings over time is an often overlooked risk when investing. Inflation can slowly erode the purchasing power of your long-term savings. As the price of goods and services increases over time, a larger amount of savings is required to maintain the same level of purchasing power in the future, like in retirement.

Keep in mind that the impact of inflation on your investments isn’t usually felt in the short term. Rather, it’s over the long-term that inflation erodes your purchasing power by silently chipping away at the real value of your money.

What can you do to protect your long-term savings from inflation?

Your portfolio’s asset mix is a key determinant of meeting your long-term investment goals and staying ahead of inflation. Generally, a larger allocation to stocks (also known as equities) means greater long-term return potential, but with a corresponding increase in risk. Whereas bonds (also known as fixed income) can provide you with a regular source of income and help soften portfolio losses during equity market downturns.

Scotia Portfolio Solutions invest in a variety of market segments and asset classes (like stocks and bonds) that aim to deliver total returns above and beyond the level of inflation over the long term. Inflation is an important consideration when it comes to all aspects of portfolio construction, from strategically allocating to an appropriate mix of stocks and bonds, actively positioning fixed income to preserve capital in periods of rising rates, to investing in companies that have pricing power for sustainable operating margins, generate positive cash flow, and deliver a high level of return on invested capital.

By investing in different asset classes, regions, and industries, you can benefit from the diversification of how they react to changes in inflation rates, which is important from a risk-management standpoint. By investing in a well-diversified portfolio, you’ll be well positioned to protect the purchasing power of your investment and be well on your way to reaching your long-term goals.

As you may have guessed, deflation occurs when the prices of goods and services fall, which in turn increases purchasing power (in other words, you can buy more with the same amount of money).

While everyone loves falling prices, deflation can become a serious economic problem. A deflationary spiral can occur during periods of economic crisis, like during a recession or depression, which are associated with decreases in overall demand. If people are worried about the economy or unemployment, they may spend less so they can save more. Prolonged bouts of deflation may bring with it reduced productivity, job cuts and financial stress. During the Great Depression in the U.S., deflation was especially sharp, with prices falling nearly 7% each year from 1930 to 1933.

It’s important to note that while the rate of inflation has come down considerably since June 2022, we are not currently in a deflationary environment. Prices are still rising, but at a much slower pace than in 2022.

- Supply for goods and services exceeds demand

When demand fails to keep pace with supply (i.e., consumers are buying less goods or services causing a surplus of inventory in the marketplace), companies may lower their prices to help stimulate demand. Falling prices across a wide range of consumer categories can trigger deflation in an economy.

- Rising interest rates

Rising interest rates increase the cost of borrowing money, which, in turn, reduces the supply of money circulating in the economy. With less access to money, people are less willing to spend, thereby reducing demand.

- Decreasing production costs

A decline in the price of raw materials can decrease production costs. When this happens, businesses may pass on these cost savings to consumers in the form of lower prices.

- Slower economic growth

Falling demand for goods and services and a slowdown of consumer spending may lead to an economic slowdown, and in more extreme cases, a recession.

- Higher unemployment

As demand for goods and services drops in a deflationary environment, companies may be forced to reduce production costs by cutting production, lowering wages and/or laying off workers.

- Lower interest rates

As demand and productivity fall, central banks may be forced to lower interest rates in an effort to spur demand – in some more extreme cases, reducing rates to zero – or even below.

While it’s difficult to fully avoid the effects of inflation or deflation, a sound investment strategy as part of your financial plan can help you maintain your purchasing power and standard of living – now and into the future.

A Scotiabank advisor can help you create a financial plan that’s right for you and then periodically monitor and adapt it as your life and circumstances change. Learn more about financial planning and view some examples of the information you’ll receive in your plan.

To help you build a solid investment strategy, Scotiabank offers a wide range of portfolio solutions that are built to navigate a variety of market conditions, including periods of rising inflation, and align with your risk tolerance and goals.

Commissions, trailing commissions, management fees and expenses may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed or insured by the Canada Deposit Insurance Corporation or any other government deposit insurer, their values change frequently and past performance may not be repeated.

1 Source for Inflation rate in Canada: Statistics Canada

2 Source: Bank of Canada: https://www.bankofcanada.ca/core-functions/monetary-policy/inflation/