Key takeaways:

Doing your tax return may feel like a chore, but if you end up getting a tax refund, it can become a reason to celebrate. While it might be tempting to jump in with some frivolous impulse shopping, you might want to do yourself a favour and plan something practical first.

Whether you’re saving for something big like a down payment or your retirement, or that well-deserved trip to a sunny destination, here are some ways to make that windfall work for your overall financial picture.

Creating a year-end tax plan in advance is wise as deadlines approach. Salaried Canadian taxpayers automatically pay a certain amount of tax every pay period. When you prepare your tax return, you include all the taxes you’ve paid and calculate any tax credits and deductions for the year. If the amount you’ve already submitted is more than you owe (for example, if you have overpaid or changed tax brackets), you get the overpayments back as an income tax refund.

Students in Canada earning taxable income must also pay taxes (snooze). However, students can claim special tax breaks, which could mean a sizable refund (yay), so there will be plenty of spare cash for books next semester.

The process is a bit different for small business owners or the self-employed because tax is not automatically deducted—they must handle that themselves and report during tax filing. However, the same rules apply. If they overpay, for example, in advance instalments, they're eligible for an income tax refund.

ALSO READ: Learn more about filing taxes in Canada

Some years, you might have to pay money to the Canada Revenue Agency (CRA) during tax season, and others, you may get a tax refund. But how can you know which way it will go? And how can you calculate your refund amount in advance?

The easiest way to calculate your tax refund is to file your tax return. Although the CRA might make some adjustments, your tax return is generally a good indicator of whether you’ll receive a refund.

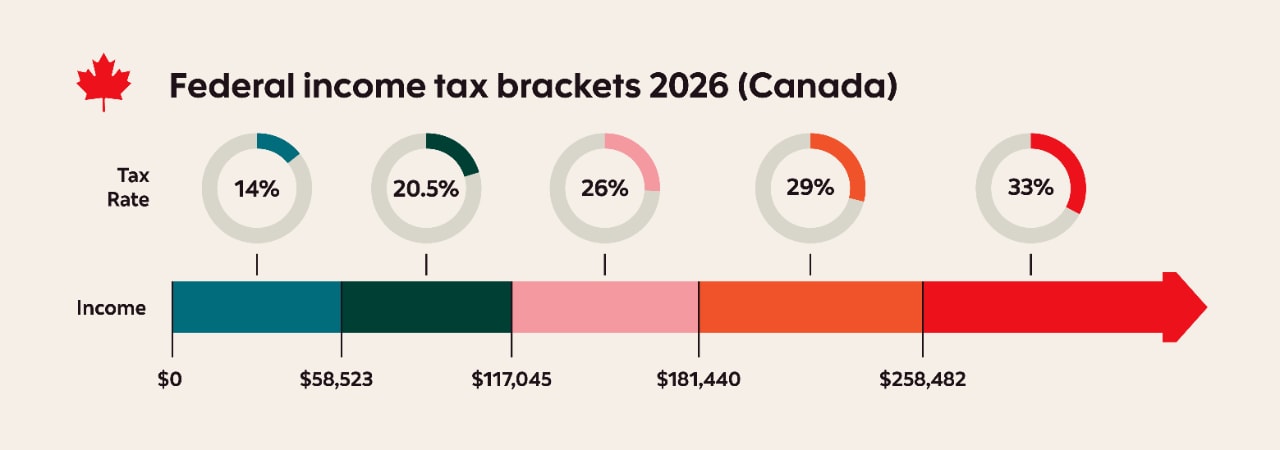

Federal income tax brackets 2026 (Canada)1

Income level |

Federal tax rate |

$58,523 or less |

14% |

$58,523 to $117,045 |

20.5% |

$117,045 to $181,440 |

26% |

$181,440 to $258,482 |

29% |

Over $258,482 |

33% |

To read the tax table, each tax rate applies only to the income within that bracket, not your entire income. You need to deduct the 2026 Basic Personal Amount (BPA) of $16,4521 from your total income to determine your taxable income.

You can view a detailed breakdown of personal income tax brackets by province on the Government of Canada website. If you want to estimate your refund before filling out your tax return, you can use a tax calculator such as the Payroll Deductions Online Calculator (PDOC) offered by the Government of Canada. It could estimate your federal, territorial, and provincial payroll deductions (with the exception of Quebec, which uses its own program). Keep in mind, however, that this is only an estimation.

How you file your income tax return with the CRA affects when you can expect to receive your refund, along with your notice of assessment. According to CRA guidelines, here are some timelines:

Online tax return: If you file online, you can expect a refund within two weeks. This is one benefit of using e-file or netfile during tax season.

Mail-in tax return: If you file with a paper return, it can take eight weeks or even longer—up to 16 weeks—if you file a non-resident return. You can speed up the process by setting up a CRA direct deposit.

Now that you have an idea of how much money you’re set to receive, it’s time to make a plan for what you’ll do with it.

1. Set-up an emergency fund

Building up an emergency fund is one of the most important choices you can make to ensure your financial stability. Think of your emergency fund as a cushion to fall back on in case of unexpected setbacks like car trouble or if your hours are cut at work. Aim to hold between three to six months' worth of expenses in your fund, and you’ll have peace of mind knowing you can weather whatever comes your way.

2. Pay off debt

Insert heading text

with an optional subtitleMany Canadians carry some form of debt, whether it’s a mortgage, car loan or credit card balance. Debt comes with interest, so it’s important to prioritize paying it down as soon as possible. Paying off a large amount at once is a great way to reduce the interest you’re paying, and it’s a big confidence booster, too.

If you decide to use your income tax refund to pay down your debt, be strategic. There are many debt repayment strategies, but you can start with the snowball and avalanche methods.

When you use the snowball approach, you use your money to pay off your smallest debt first. This strategy is helpful for those who need some early wins to gain momentum.

If you’re already committed to paying off your debt, consider the avalanche method. This method has you pay off the debt with the highest interest rate first, reducing the overall amount of interest you pay. Whichever method you choose, putting your tax refund toward your debt may not be the most exciting option, but it does make a lot of financial sense.

3. Put it in savings

While you might keep your emergency fund in some sort of savings account, it’s a good idea to have a separate account to keep your funds for short and long-term savings. If you’re already working towards something—like a home renovation or new car—you might consider using your tax refund to bring yourself a little closer to the finish line.

In addition to regular savings accounts, you might also consider using other types of bank accounts. A tax-free savings account (TFSA) is a registered account that lets you grow your money tax-free. Or, if you’re saving up for your first home, look into a first home savings account (FHSA).

4. Fund your retirement

Planning for your retirement is an important financial goal. Whether you're 21 or 51, you should make the effort to contribute to your retirement fund regularly. That’s because of compound interest, which is the interest on both the principal amount of your savings and the interest paid on it.

The longer your money is invested in a retirement vehicle like a registered retirement savings plan (RRSP), the more compound growth you will see. Plus, with an RRSP, you’ll receive a tax deduction for your contribution, which could result in a tax refund the following year as well.

5. Seed a post-secondary fund

If you have kids, a registered educational savings plan (RESP) is another smart way to invest your tax refund. When you contribute to these funds, the government provides matching contributions up to $2,500, meaning you get a lot of bang for your buck.

If you’ve handled all your other financial commitments, you could use some of your tax refund money to reward yourself. Maybe that's a little weekend getaway, an extravagant meal, or some cash towards a new hobby. Personal finance is all about balance, which is why it’s important to budget for indulgences as well as more responsible expenses.

When planning how to spend your tax refund, the right path can vary from year to year. It may depend on how much money you're getting back and what your financial priorities are. Now that you have some practical ideas on how to make your refund work for you. Don't forget to thank yourself for your efforts with that ice cream sundae.

This article is provided for information purposes only. It is not to be relied upon as investment advice or guarantees about the future, nor should it be considered a recommendation to buy or sell. Information contained in this article, including information relating to interest rates, market conditions, tax rules, and other investment factors are subject to change without notice and The Bank of Nova Scotia is not responsible to update this information. All third party sources are believed to be accurate and reliable as of the date of publication and The Bank of Nova Scotia does not guarantee its accuracy or reliability. Readers should consult their own professional advisor for specific investment and/or tax advice tailored to their needs to ensure that individual circumstances are considered properly and action is taken based on the latest available information.

Sources: