For many Canadians, the phrase financial planning sounds like an overwhelming and exhaustive exercise. If you’ve considered creating a financial plan, you may have put it off for a number of reasons: not knowing how to start, what’s involved or who can help. Another key deterrent may be information overload – or misinformation overload – about the process itself.

What is financial planning?

According to the Financial Planning Standards Council of Canada,1 a financial advisor provides comprehensive planning when considering one’s major life goals and events, or at least three out of the following six planning components: household budgeting, tax, retirement, estate planning, investing, debt or risk management.

In this article, we’ve outlined some of the most common misconceptions about financial planning in order to give you the confidence you need to get started on your plan.

If you want to attain financial success, it’s important that you have a financial plan. Think of a financial plan as your personal roadmap, clearly outlining your financial goals and the steps you need to take to help you achieve them. Your plan will include longer-term goals, such as saving for your children’s education and retirement planning, as well as shorter-term goals, such as saving for a car or a home.

A financial plan gives you better control of your finances and peace of mind, knowing there are strategies in place to help keep you on track during both good and challenging times.

While everyone’s plan will be unique to their specific goals, a financial plan is designed to help answer three fundamental questions:

- Where are you now financially?

- What would you like to achieve – both short and long term?

- How will you get there?

Once you have a plan in place, it’s important to revisit your plan regularly to confirm that you are still on track to meet your goals, or if adjustments should be made.

A common misconception among many is that you need substantial wealth in order to start a financial plan. That’s simply not the case. You start a plan in order to begin building wealth.

This misconception may cause some to put off starting a financial plan, which can affect their long-term savings goals. It’s never too early to start saving for retirement. The earlier you start, the better off you’ll be because your retirement savings will have more time to grow. And it all begins with creating a financial plan. If you earn income and have financial goals, having a financial plan in place will set you on the path to achieving them.

Let’s look at the impact of delaying saving for retirement*

- Susan and Mark would both like to retire at age 65.

- Susan starts saving $100 biweekly when she’s 30.

- Mark decides to put off saving until he’s 45 but will contribute twice as much – $200 biweekly – to help catch up.

• At age 65, Susan will have contributed $91,000 in 35 years, while Mark will have contributed $104,000 in 20 years. However, Susan will actually retire with $64,510 more than Mark – even though she contributed $13,000 less.

• With more time on her side to grow her savings (15 years more) and the benefit of compound growth, Susan’s $91,000 contribution grew to $240,882, while Mark’s $104,000 contribution grew to $176,372 ($64,510 less than Susan).

Because there is duplication between a budget and financial plan, many mix up one for the other.

While a budget contains your income and spending practices, which are major components of your financial plan, a financial plan contains much more.

You create a budget to help track your spending and saving habits in order to gain control of, and become more efficient with, your cash flow.

A financial plan includes all aspects of your financial life – an assessment of your net worth (assets vs. liabilities), cash flow (income and spending), taxes, retirement planning, estate analysis and insurance planning – to help you achieve your short-, medium- and long-term financial goals.

While it’s great that you’ve decided to start a financial plan, you might want to reconsider tackling it on your own.

Although there’s certainly no shortage of financial advice in today’s digital age, making sense of all the information and determining what applies to you can be overwhelming. At some point on your financial journey, you will require the support of financial professionals who can guide you and introduce you to additional tools and resources.

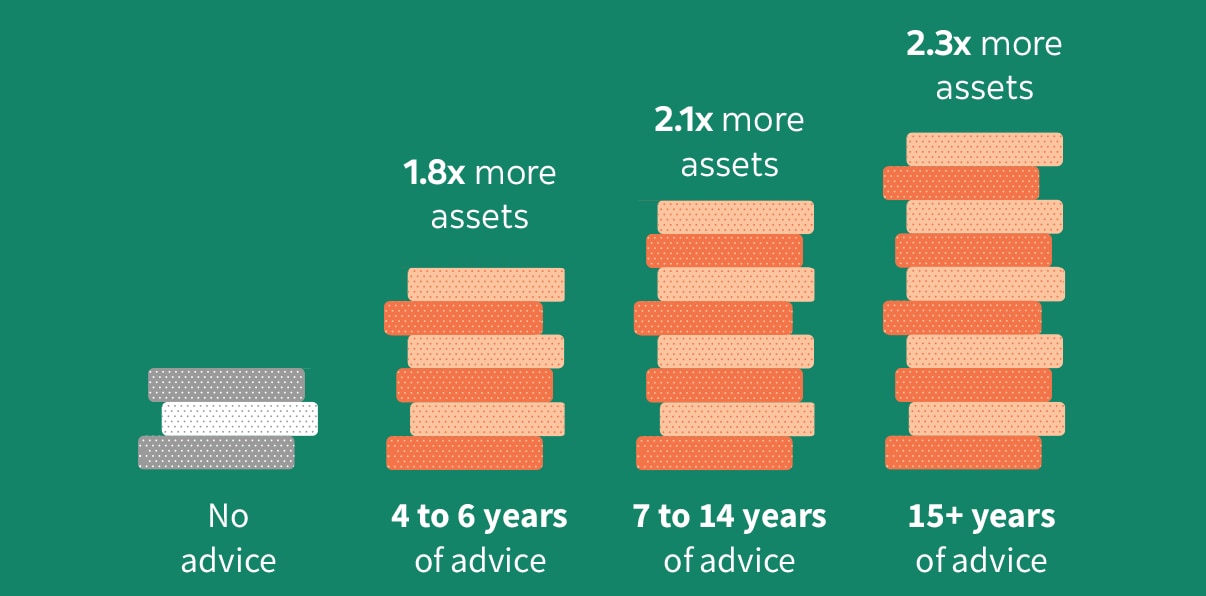

Working with a financial advisor helps you increase your wealth2

Working with a financial advisor to create a financial plan will help you build up your wealth through better savings approaches, while increasing your financial knowledge, so that you can be confident in the choices you make.

Research has shown that households working with a financial advisor accumulate more assets than those that don’t – and the longer they work with an advisor, the more their savings will grow.

Consider the following research:

Versus non-advised households, the average household with a financial advisor accumulated:

- 1.8 times more financial assets over 4 to 6 years

- 2.1 times more assets over 7 to 14 years

- 2.3 times more assets over periods greater than 15 years

While having a financial plan is a great start, it’s important to remember that to provide its maximum benefit, your plan needs to be continually updated to reflect the ongoing changes in your life. That includes everything from marriage and the birth of a child to career changes or a new home purchase, just to name a few.

Keep in mind that financial planning is an ongoing process. That’s why we often refer to a financial plan as a “living document,” something that’s continually amended to reflect the changes in your life. For that reason, it’s a good idea to keep your plan accessible so that you can easily review it as your financial situation changes.

Think of your relationship with your advisor as a partnership, with both of you taking an active role to reach your financial goals.

As the client, get in the habit of staying on top of your investments by keeping a file of your account statements, tax slips and any other related documents. Make sure you read documents that you receive about your investments and take a keen interest in your portfolio – after all it’s your financial future. Taking an active approach will in turn help your financial advisor to deliver timely information and in-depth support to help you reach your financial goals with confidence.

It’s also critical that you keep your advisor informed about changes in your personal or financial circumstances. Major life changes – such as marriage, the birth of a child, divorce or the death of your spouse – can profoundly impact your financial outlook. Your financial advisor can be instrumental in making necessary adjustments to your financial plan to ensure you’re on track to reach your financial goals.

Here’s some good news: Your initial meeting with a Scotiabank advisor would only take about an hour. This will provide them the opportunity to ask questions about your financial situation, go over your goals and identify any specific needs. While it may take a few meetings to put your plan into action, it’s time well spent. With a financial plan in place, you’ll be more confident knowing that you’re in a better position to achieve your financial goals.