The start of the new year gives us the chance to reflect on 2021, acknowledging and celebrating our accomplishments and learning from things that didn’t go exactly as planned.

Among the many priorities we typically think about as we move into a new year is our financial well-being. As we all know, when our finances are in order, we feel more confident about the future and our ability to handle life’s unexpected challenges.

To provide you with some helpful advice heading into 2022, we’ve chosen six tips that you can consider as you map out the coming year and your longer-term goals.

1. Take control of your future with a financial plan

Think of a financial plan as your personal roadmap, outlining your financial goals and strategies to help you achieve them. It not only includes longer-term goals, such as saving for your children’s education and retirement planning, but also includes shorter-term goals, such paying down debt or saving for a car or a home.

While everyone’s plan will be unique to their goals, a financial plan is designed to help answer three fundamental questions:

- Where are you now financially?

- What would you like to achieve – both short and long term?

- And how will you get there?

A comprehensive financial plan should include an assessment of net worth (assets vs. liabilities), cashflow (i.e., income and spending), taxes, retirement planning, estate analysis and insurance planning.

4 key benefits of having a financial plan

Helps you set goals and plan for your future

A financial plan will help you set realistic financial goals and outline a strategy and timeline for achieving them.

Identifies opportunities

Whether it’s growing your savings, reducing debt or selecting tax-efficient investments to help you keep more of your money, a financial plan can help you get better financial outcomes.

Helps you navigate your finances with greater confidence

During trying times or periods of market volatility, having a financial plan in place will help you to avoid reacting hastily and making emotional decisions. If you are working with a financial advisor, you will have the opportunity to increase your financial knowledge and learn about better savings approaches, which in turn will make you more confident in the choices you make.

Prepare for unexpected events and risks

A financial plan will look at your current financial situation, identify certain risks and plan accordingly. For example, do you have a will, or enough insurance to maintain your family’s standard of living to handle unexpected life events (e.g., disability or illness, job interruption, loss of life). Do you have an emergency fund established to cover job loss or major home repairs? A financial plan can help analyze your current situation in order to put in place appropriate safeguards.

2. Establish a budget

As we start to feel the effects of inflation at the cash register – from the grocery store to the gas station – many of us are looking for ways to make sure our money goes as far as possible these days.

Quick stats

81%

of Canadians are worried about the increased cost of living and how that will impact their finances1

77%

of Canadians are concerned prices for everyday purchases are going up2

By creating a budget to track your expenses, you’ll have greater control of your finances and a solid understanding of where all your money is going. Here are two steps to help you establish a budget:

Step 1

Calculate the total income you’ll receive from all sources: for example, employment income, rental or investment income, support payments, pension etc.

Step 2

List all your expenses and divide them into two categories:

- Non-discretionary, or mandatory costs such as mortgage payments, rent, hydro, etc.

- Discretionary, or non-essential costs such as entertainment, subscriptions, memberships, etc.

If funds are remaining after you’ve accounted for all your non-discretionary costs, prioritize your discretionary costs based on what is most important to you.

Your budget can be as basic or detailed as you like – whichever works best for you. The important thing is to set up a budget and reassess it often (for example, at least semi-annually) to ensure it’s working to meet both your short- and long-term financial goals, or whenever you have a significant change in your income or expenses.

Visit scotiabank.com/moneyfindercalculator and try the Scotiabank Money Finder calculator. It will help you determine if you have additional funds available to put towards your financial goals by comparing your income to your expenses.

3. Pay down debt

Some Canadians may find themselves feeling the stress of new debt they’ve taken on or repayment of older debt. Creating a plan that lists each of your debts and how you will manage repayment is an important first step. Knowing what options are available to help you pay down your debt more quickly is also key to establishing a sense of control over your finances.

Here are two methods to consider to help you pay down your debt (pick the one you feel will be faster and more effective for you).

- Debt avalanche method

This method focuses on paying off the debt with the highest interest rate first (i.e., debt that is costing you the most per dollar). After that’s paid, you shift to the debt with the next highest interest rate, and so on.

- Debt snowball method

The goal is to start by paying off your smallest debt first. This can create a sense of accomplishment, so you can use that momentum to move on to the next debt. Many people find this method easier to stick to. Keep in mind, however, that you may end up paying more in interest depending on the amount of time it takes to pay off your larger debts with potentially higher interest rates.

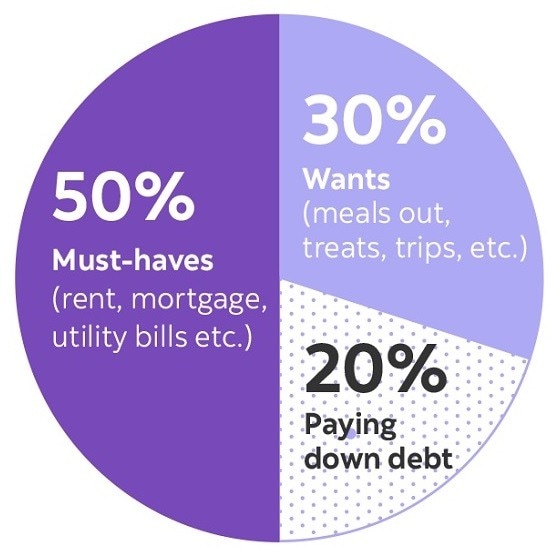

How much of your pay should go towards your debt payments?

This can vary, but a good place to start is to follow the 50/30/20 rule.

If you are feeling overwhelmed with your debt, or want to learn more about options to pay off debt more effectively or quicker, schedule a meeting with a Scotiabank advisor to review your situation and help you find a solution that works best for you.

4. Start saving – it’s never too early

Time is your biggest ally when it comes to saving. Once you start working and can set aside even a small amount each month, you can be well on your way to building savings for your short- and long-term financial goals. When it comes to saving for retirement, the earlier you start the better because your money will have more time to benefit from compound growth.

Let’s look at the impact of delaying saving for retirement

- Susan and Mark would both like to retire at age 65.

- Susan starts saving $100 biweekly when she’s 30.

- Mark decides to put off saving until he’s 45 but will contribute twice as much – $200 biweekly – to help catch up.

At age 65, Susan will have contributed $91,000 in 35 years, while Mark will have contributed $104,000 in 20 years. However, Susan will actually retire with $64,510 more than Mark – even though she contributed $13,000 less. Why? With more time on her side to grow her savings (15 years more) and the benefit of compound growth, Susan’s $91,000 contribution grew to $240,882, while Mark’s $104,000 contribution grew to $176,372 ($64,510 less than Susan).

| Mark | Susan | |

|---|---|---|

| Total Savings at 65 | $176,372 | $240,882 |

| Investment growth | $72,372 | $149,882 |

| Contribution | $104,000 | $91,000 |

For illustrative purposes only and not intended to reflect an actual rate of return of the future value of an actual mutual fund or any other investment. The calculation assumes reinvestment of all income and no transaction costs or taxes. Illustration assumes a hypothetical rate of return of 5%, compounded annually. Amounts are rounded to the nearest dollar.

To see how quickly your savings can grow, visit scotiabank.com/PAC and try out our interactive PAC video. Check out How the “PAC” mentality can help your long-term investment goals to learn more about the benefits of setting up Pre-Authorized Contributions (PACs) – an easy and convenient way to build up your savings.

5. Keep calm and invest on

Market volatility can be unsettling for even the most knowledgeable investor and could lead to impulsive investment decisions that may not align with your long-term financial goals.

During recent market volatility ...3

70%

of Canadian investors say it’s hard to know what to do about investing in volatile times like these

55%

of Canadian investors are relying on the advice of an advisor to help weather the ups and downs of the market

It’s easy to let your emotions get the better of you during stressful times – investing is no different. Sitting on the sidelines or selling for the temporary relief of cash might cost you more in the long run.

Here are some fundamental principles to help you get through periods of increased market fluctuations.

Focus on the big picture

Although it’s practically impossible to forecast market swings, having a well-thought-out investment plan can help provide a sense of confidence that you can get through market volatility. Keeping an eye on your long-term strategy will ultimately help you ride out the short-term volatility and ensure that you don’t derail your long-term investment success.

Stay diversified

Often equated with not putting all your eggs in one basket, diversification is a technique that combines different types of investments – stocks, bonds, cash, for instance – in a portfolio to help reduce risk. Diversification is essential during periods of market stress. While by no means immune to market downturns, a well-diversified, professionally managed portfolio may experience less volatility in turbulent markets.

Manage risk, don’t avoid it

Taking on investment risk doesn’t need to be an all-or-nothing approach. Consider finding a middle ground with an investment solution that offers a balanced approach to risk and return. Not surprisingly, reducing your exposure to riskier investments will help to lower the overall risk of your portfolio, but taken too far, you could increase your exposure to other risks, such as longevity risk – the risk that you’ll outlive your retirement savings. The key to long-term investment success is finding a balanced mix of investments that will let you remain at ease.

Invest automatically and take advantage of market ups and downs

Instead of fearing market corrections, consider them buying opportunities. By contributing on a regular basis through a Pre-Authorized Contribution (PAC) plan, you take advantage of the market dips by purchasing more fund units when your dollar goes farther, and in turn, lowering your average cost. Investing a set amount on a regular basis through a PAC plan not only helps to eliminate the guesswork of when to buy, it’s a convenient and simple way to save without even thinking about it.

6. Seek out professional advice to help increase your wealth

While there’s certainly no shortage of financial advice in today’s digital age, making sense of all the information and determining what applies to you can be overwhelming.

For many Canadians, COVID-19 heightened the need for financial advice – with many facing concerns ranging from market volatility and how/when to invest their money to worries over their personal financial situation.4

49%

Agree getting advice from an advisor is even more important to them now than it was before the pandemic.

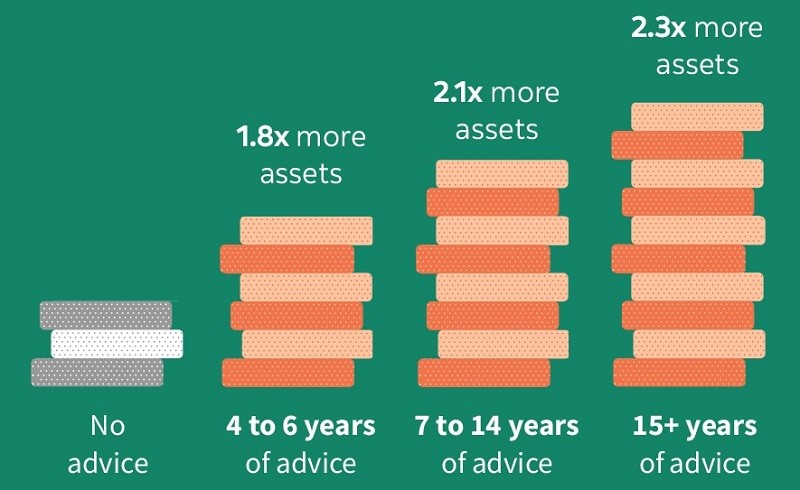

Research has shown that households working with a financial advisor accumulate more assets than those that don’t – and the longer they work with an advisor, the more their savings will grow.

Let’s take a closer look at this research5:

Versus non-advised households, the average household with a financial advisor accumulated:

- 1.8 times more financial assets over 4 to 6 years

- 2.1 times more assets over 7 to 14 years

- 2.3 times more assets over periods greater than 15 years

The best advice starts with a conversation

Scotiabank advisors are highly qualified with experience in financial planning to work with you to create a financial plan that’s right for you and evolves with you – answering your questions, providing advice and updating your financial plan along the way to help you achieve your goals. You’ll also have access to additional resources and advice as Scotiabank advisors work with a range of specialists across the bank.

Schedule an appointment with a Scotiabank advisor or visit scotiabank.com/GetAdvice to meet some of our advisors and to learn about the wide range of topics you can discuss with them – from savings and investments to budgeting and planning for retirement.