Key takeaways:

Canadians are living longer than ever before. But instead of celebrating, many people are worrying about having to fund a longer retirement than they’d planned.

Read on to see what you can do to ease your worries about an extended retirement, so you can enjoy living it.

Longevity risk refers to the possibility that you may outlive your retirement savings. In other words, you may not have sufficient savings to last all the years you live.

Thanks to advancements in medicine and health technology, the average life expectancy for Canadians has risen to 81.6 years.1 That makes longevity risk real for people who:

- Underestimated how much money they’d need in retirement

- Had investments and other savings that didn’t grow as much as expected

- Are healthy and may live longer than anticipated

The average amount Canadians expect they’ll need for their ideal retirement is $807,000.2 But since everyone’s ideal retirement looks different, your number might be less — or more. How much you need to save for retirement will depend on your spending habits, expenses and lifestyle.

Did you know?2

- 45% of Canadians said that they invest regularly each month.

- Median amount invested monthly was $375, with that amount increasing with age.

Your retirement planning should take three items into consideration:

- Your anticipated income sources in retirement, such as the Canada Pension Plan (CPP)/Quebec Pension Plan (QPP), Old Age Security (OAS), workplace pension plans and registered and non-registered accounts.

- Your current expenses and estimated future expenses, to help estimate how much you may spend in retirement, while also identifying debt or expenses that can be reduced or eliminated before you retire.

- An estimate of your future health care costs, factoring in any government or employer benefits you’ll still have access to once you’re no longer working.

A Scotiabank advisor can provide you with retirement planning advice that will set you on the path to building the retirement you’ve envisioned. It all starts with a simple conversation.

READ MORE: The retirement hub has timely financial articles, tips and tools, like the retirement savings calculator.

When people think about risk, they tend to focus more on day-to-day market fluctuations and recent gains or losses. But focusing more on short-term ups and downs rather than long-term trends leads to what behavioural finance experts call “recency bias.”

There are downsides to letting short-term concerns impact long-term planning, including retirement planning. Being overly conservative when it comes to retirement investing can limit your long-term growth potential. This could increase your risk of falling short of your retirement savings goal or running out of money when you’re retired, especially after factoring in inflation.

Keep in mind that higher return potential likely comes with added risk. But you can manage risk, including longevity risk by:

- Having a retirement income plan

- Making sure your investments are aligned with your investment time horizon, objective and risk profile

- Investing in a professionally-managed and thoughtfully diversified portfolio, like Scotia Portfolio Solutions, to help minimize risk while aiming for long-term growth

A retirement income plan is a financial roadmap designed to give you an accurate picture of your cash flow throughout your retirement years.

Your retirement income plan and withdrawal rate should take all your retirement sources into account, including government pension programs, workplace pension plans and your personal savings, including registered investments.

Withdrawing your savings too quickly could derail your long-term plans. That said, many people look at retirement as three stages:

- Early retirement: For the first five to ten years, spending tends to be higher. You have more free time to travel, try new hobbies and cross items off your bucket list. Many Canadians also choose to work part time during this stage. If you haven’t had any estate planning conversations prior to retirement, this is an ideal time to sit down with a lawyer to review your financial assets and outline your plans for the next 10 to 20 years. Early estate planning provides greater control and flexibility, helps optimize taxes, and ensures your wishes are documented while you’re healthy and able to make decisions.

- Mid retirement: Ten to 20 years into retirement, spending time with family and friends is often a priority. At this point, you’ll start thinking about how you’ll adjust your plans as you get older — especially where you’ll choose to live, possibly a senior living community.

- Late retirement: In this later stage, the focus is typically on health care, reviewing and updating estate planning and leaving a legacy — ensuring your loved ones and cherished causes are taken care of. An estate plan can help to transfer assets with minimal tax burden, so there’s a smooth transition to the next generation.

The following are some steps you can consider taking now if you think you may encounter a gap between your retirement savings and your desired retirement lifestyle.

Increase your current rate of savings

Time is your biggest ally when it comes to saving, especially for retirement. The earlier you start, the better off you’ll be, thanks to the power of compound growth.

Compound growth is the exponential increase in your investment’s value over time. Earnings grow on the principal, on the growth and then on the growth from that growth. This continues for as long as you’re invested.

If you’ve set up pre-authorized contributions (PACs) to grow your retirement savings, consider increasing your contribution amount, or increasing how often you automatically transfer money to savings or investments. For example, you could switch from monthly to biweekly contributions.

If you don’t have a PAC in place, consider setting one up — it’s a great way to build your savings easily and automatically. To see how quickly your savings can grow, try out our interactive PAC video.

Catch up on RRSP contributions

While maxing out your yearly RRSP contributions is ideal, it’s not always possible. But you can make catch-up contributions if you have unused contribution room. You can find your exact unused contribution room, as well as your contribution limit, in your CRA My Account or on your latest notice of assessment.

If you started saving for retirement later, you may have a large amount of unused contribution room, meaning you should be able to save more on a tax-deferred basis. A Scotia RSP Catch-Up® Line of Credit can help you to maximize your RRSP contributions without using available funds on hand.

The Scotia RSP Catch-Up® Line of Credit also allows you to defer up to three monthly payments at the time of your RRSP contribution while you wait for your tax refund3. If you choose to defer payments, interest at the rate that applies to your Scotia RSP Catch-Up Line of Credit will continue to accrue during any deferral periods from the date you advance funds on it3 ; however, this could give you the option to use your tax return once received toward repayment of the funds advanced from your Scotia RSP Catch-Up® Line of Credit.

Before applying for a Scotia RSP Catch-Up® Line of Credit, make sure this option is right for you, it fits into your budget and you can manage the debt. Talk to your financial or tax advisor if you think this is something that could work for you and your retirement savings and investment needs.

Pay off or reduce your debt

If possible, paying off debt before retirement is recommended, as every dollar you owe reduces flexibility on how your retirement income is used — repaying debt instead of funding your lifestyle.

Even if being mortgage-free by the time you retire isn't a realistic option, reducing your mortgage can make a big difference once you're retired. And if you currently have other debt, such as credit card debt or small loans, your Scotiabank advisor can walk you through options to pay off or reduce debt before you retire.

Prioritizing debt management will also improve your current financial wellbeing. There’s no one right way to tackle debt, so choose a strategy that motivates you to make consistent payments.

READ MORE: Three debt repayment strategies every Canadian should know. Which one is right for you?

Plan for inflation

While the impact of inflation on your investments isn’t usually felt in the short term, its impact can slowly erode the purchasing power of your long-term savings. As the price of goods and services increases over time, a higher amount of savings is required to maintain the same level of purchasing power in the future (for example, during retirement). In other words, when prices rise, your money buys less.

Inflation affects everyone. But having a sound investment strategy can help you maintain your purchasing power and standard of living in retirement.

Scotiabank offers a wide range of portfolio solutions that are actively managed and continuously adjusted to help control risk, including inflation risk, and support your long-term investment objectives.

Retire later

Continuing to work for a few more years than originally planned may provide you with the funds needed to help you achieve and/or extend the retirement lifestyle you want.

Retiring later also gives you a longer investment time horizon — meaning how long you have before accessing saved funds — to maximize compound growth.

If you’re considering retiring later than you originally planned, you can continue to make RRSP contributions until you're 71. Be sure to speak with your financial advisor to see how a later retirement date will impact the value of your RRSP.

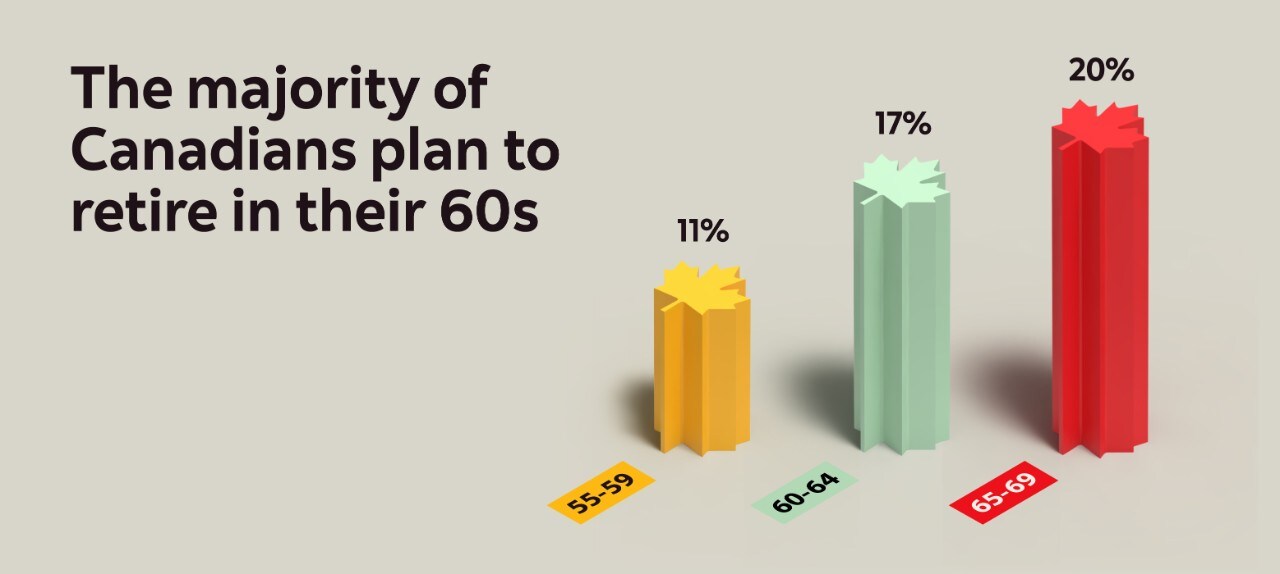

You can also delay your government pension plan payments. Your monthly payments from the Canada Pension Plan/Quebec Pension Plan (CPP) and Old Age Security (OAS) will increase every month you delay drawing them, but only until age 70.

You could also look into other government programs that might be available to you, such as the Guaranteed Income Supplement (GIS).

Did you know?2

Revisit your lifestyle assumptions

If you’re worried about outliving your savings, you might consider making changes to what you’ve planned for retirement. This could entail revisiting your retirement lifestyle and spending expectations to find flexible areas. You might also consider reviewing if downsizing to a smaller house can help reduce your household expenses, like your utilities, property taxes and insurance.

Decide if downsizing is right for you

Downsizing won’t always boost your nest egg as much as you expect. Even if the real estate market is booming, you’ll still have to pay costs like real estate commissions, legal fees and applicable taxes.

You’ll also need a new place to live. Keep in mind that smaller houses don’t always provide a significant decrease in expenses. You’ll still have expenses like utilities, property taxes, insurance and maintenance fees. Although condos may have reduced property taxes and other costs, you’ll have condo fees to pay monthly.

Explore part-time work options in retirement

Another way to extend your retirement savings is to take on part-time work. Any income you earn when you’re retired may allow you to make smaller withdrawals from your retirement savings and extend how long they’ll last.

You may even be able to work part-time or consult in the same field you semi-retired from.

Consider leveraging your home’s value

If your home’s value has increased significantly over the years, you could look into a borrowing plan tied to the equity in your home. To learn more about this option and to see if it’s the right strategy for your situation, you can speak with a Scotiabank advisor.

You could also rent out your finished basement to supplement your income, or your entire home during the winter months while you escape to a warmer climate. This also could help you as it lets you avoid leaving your house empty for an extended period of time.

Whether you’re years away from retirement or counting down to your last day of work, you can reduce the possibility of outliving your retirement savings by having a comprehensive retirement income plan that will allow you to identify possible funding gaps now, when you still have time to close them. Whether that requires delaying retirement for a couple of years, reducing debt or saving a little more now, your future self will thank you.

A Scotiabank advisor can provide you with retirement planning advice and work with you to help you achieve the retirement you want. Find out more about working with a financial advisor.

This article is provided for information purposes only. It is not to be relied upon as financial, tax or investment advice or guarantees about the future, nor should it be considered a recommendation to buy or sell. Information contained in this article, including information relating to interest rates, market conditions, tax rules, and other investment factors are subject to change without notice and The Bank of Nova Scotia is not responsible to update this information. References to any third party product or service, opinion or statement, or the use of any trade, firm or corporation name does not constitute endorsement, recommendation, or approval by The Bank of Nova Scotia of any of the products, services or opinions of the third party. All third party sources are believed to be accurate and reliable as of the date of publication and The Bank of Nova Scotia does not guarantee its accuracy or reliability. Readers should consult their own professional advisor for specific financial, investment and/or tax advice tailored to their needs to ensure that individual circumstances are considered properly and action is taken based on the latest available information.

1 World Health Organization. (2024.) Health data overview for Canada. (Accessed November 2025.)

2 Scotiabank. (August 2024.) Consumer Sentiment Towards Retirement, 2024 Investment Poll.

3 Deferrals currently must be requested in branch and are only available if the account is in good standing. Other conditions apply. Speak to your Scotiabank advisor for more details. Interest will continue to accrue during any deferral period(s) on each advance from the transaction date of each advance until that amount is paid in full and will be applied to the balance monthly.