Key takeaways:

Filing taxes in Canada may not be the most thrilling task, but it’s an unavoidable part of adulting — kind of like doing laundry, but for your wallet. Completing your tax return can seem like deciphering a secret code, but it’s really just about reporting your income and figuring out what you owe or what’s owed to you — hello, refund! With a bit of guidance, tackling taxes can feel less like a chore and more like checking off an important life task. Read on to understand the basics that can help make tax season simpler.

Most people living and working in Canada are required to pay taxes. Every year, you will file a tax return where you report your income from the previous year to the Canada Revenue Agency (CRA). You must list all forms of income, including any self-employment earnings, tips or business income, and then check your eligibility for tax deductions or credits.

Even if you haven't earned any money in a given year, filing a tax return still allows you to access benefits like the goods and services tax/harmonized sales tax (GST/HST) credit, among others. The CRA may assess your return and determine that you’re squared up and don’t need to pay any tax, that you are owed money back with a refund cheque or that you still have outstanding taxes to pay.

Filing taxes is mandatory for Canadian residents and newcomers, including immigrants, international students and temporary foreign workers.

You must file Canadian taxes if:

- You received Canadian-sourced income

- You owe the government money

- You want to claim a refund or benefit, such as Canada Child Benefit (CCB)

Did you know?

Filing together with your spouse helps you maximize credits and benefits like the GST/HST credit and spousal amounts.

The Canadian government has established a basic personal amount (BPA), which is the income threshold you can earn before needing to pay any federal income tax. The BPA aims to allow individuals with taxable income below the BPA amount, which has increased to $16,4521 for 2026, to benefit from a complete exemption from federal income tax.

In simpler terms, if your annual income is $16,452 or less in 2026, you’re not required to pay federal taxes. The BPA also offers a partial tax reduction for taxpayers whose taxable income exceeds that amount. You can review the federal tax brackets below and find more information on the CRA website.

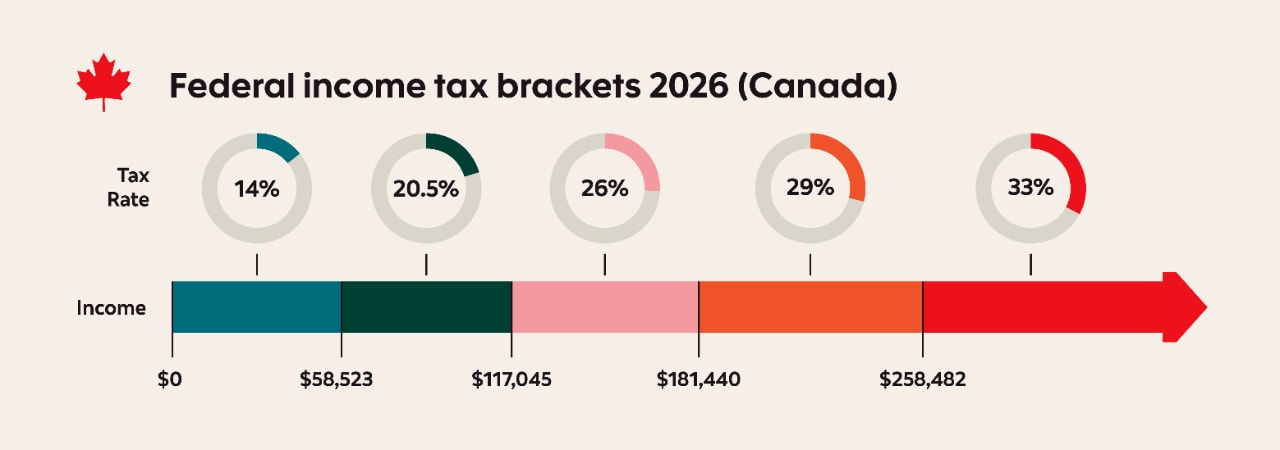

Canada uses a graduated personal tax system, meaning different tax rates apply to different portions of income (up to a certain income level).

If you want to understand which tax rates will apply to your income, you can review the updated Canadian federal tax brackets below in addition to the tax brackets at the provincial and territorial levels. Those may have also changed for 2026 — for a complete list of provincial and territorial tax brackets, visit the CRA website.

Income level |

Federal tax rate |

$58,523 or less |

14% |

$58,523 to $117,045 |

20.5% |

$117,045 to $181,440 |

26% |

$181,440 to $258,482 |

29% |

Over $258,482 |

33% |

Tax deadlines in 2026

Date |

Income Situation |

Details |

April 30 |

Salaried employee |

If April 30 falls on a Saturday, Sunday or holiday that year, returns will be considered filed on time if the Canada Revenue Agency (CRA) receives them or they are postmarked on the first business day following April 30. If you owe taxes, the payment is also due at that time. |

June 15 |

Self-employed |

If you are self-employed or have a self-employed spouse or common-law partner, the filing deadline is June 15. The payment of taxes owed is due on April 30, 2026. |

Tax penalties

If you file late, you’ll face interest on any taxes you owe, plus a late filing penalty. If you can’t afford to pay right away, still file by April 30 and then contact the CRA to discuss your payment options. Don’t worry — they’re there to help.

In addition to your financial reporting, you are required to provide basic information, such as your name and address and your Social Insurance Number (SIN). All newcomers to Canada need a SIN. If you have requested an SIN and are still waiting for your documentation, still file your taxes to avoid penalty charges or benefit delays.

Filing a paper tax return

If you are filing a paper return, you should include one copy of all relevant documents, including:

T4 slips: If you’re employed in Canada, you’ll receive a T4 slip from your employer. It outlines your total remuneration and source deductions for the year (such as Employment Insurance, Canada Pension Plan and income tax withheld).

Business receipts: If you’re self-employed, you need to keep business receipts and invoices to accurately report your income and claim deductions. You may also need them in case the CRA has follow-up questions.

Dependant details: This includes basic information about your spouse, children and/or elderly parents. You may be eligible for certain tax credits.

Receipts for deductions/credits: Examples include medical expenses, childcare costs, charitable donations and tuition payments (T2202 slip).

RRSP contributions: Your Registered Retirement Savings Plan (RRSP) deduction limit and receipts for contributions made during the year.

Tax slips for investments: Capital gains or losses, dividends or interest earnings.

Proof of residency: For claiming certain provincial or territorial credits.

Direct deposit info: To get your refund even faster.

Filing taxes through the CRA’s My Account

If you file electronically through the CRA’s My Account, you’ll need the same information listed above. You’ll still need to keep copies of all of your documents and supporting paperwork in case the CRA needs to see them.

Most newcomers will be able to file electronically through NETFILE, although there are some NETFILE exclusions for certain individuals and non-residents. If you’re unable to use NETFILE, file a paper return.

Additional earnings and tax credits

Don’t forget that in addition to reporting all of the income you earn in Canada, other financial earnings and tax credits need to make their way onto your forms, too. For example:

Foreign income: If you have income from a different country, it must be reported in Canadian dollars on your Canadian tax return. If you’ve already paid taxes on the income you received outside of Canada, you might qualify for a federal foreign tax credit.

Moving expenses: Generally, you can’t deduct expenses incurred to move to Canada. You may be able to claim moving expenses if you moved to work or to run a business at a new location or to study courses as a full-time student enrolled in a post-secondary program at a university, a college or another education institution. If this is the case, your new home must be at least 40 km closer to your new work location or school.

Support payments: Even if your former spouse or common-law partner does not live in Canada, you may be able to deduct support payments made.

Most newcomers will be able to file electronically through E-FILE or mail, though there are some E-FILE exclusions for certain individuals and non-residents.

Congrats — you’ve filed your taxes! If you’re expecting a tax refund, it might be tempting to treat yourself, but also consider putting some of that cash toward your financial goals. It’s an excellent opportunity to tackle money-smart plans, like paying down debt or building a Forget You fund. Either way, you’ve made a smart move toward financial wellness — nice work.

Legal Disclaimer: This article is provided for information purposes only. It is not to be relied upon as investment advice or guarantees about the future, nor should it be considered a recommendation to buy or sell. Information contained in this article, including information relating to interest rates, market conditions, tax rules, and other investment factors are subject to change without notice and The Bank of Nova Scotia is not responsible to update this information. All third party sources are believed to be accurate and reliable as of the date of publication and The Bank of Nova Scotia does not guarantee its accuracy or reliability. Readers should consult their own professional advisor for specific investment and/or tax advice tailored to their needs to ensure that individual circumstances are considered properly and action is taken based on the latest available information.

Sources: