Receiving a pre-approved credit card offer can feel almost like a gift — a gift of credit, that is.

But what exactly is a pre-approved credit card offer? Are you guaranteed to get the credit card if you apply? And what impact does a pre-approved credit card offer have on your credit score?

The word “pre-approved" can be quite confusing. We're here to help with this guide to everything you need to know about credit card pre-approvals.

Key takeaways:

When you receive a pre-approved credit card offer, it means the credit card issuer has prescreened you based on certain criteria, such as your credit history and financial information. As a result of this prescreening, they've determined that you'd be a good candidate for their credit card.

Depending on the lender, however, you may still need to apply for the credit card. With certain lenders, the application process for a pre-approved credit card is the same as for any credit card. If this is the case, you'd need to fill out the credit card application with the information the lender requires, and then they'll do a credit check pending approval.

While a pre-approved credit card offer speaks to your creditworthiness, it still requires action on your part: You'll need to decide if you want to take the lender up on their offer.

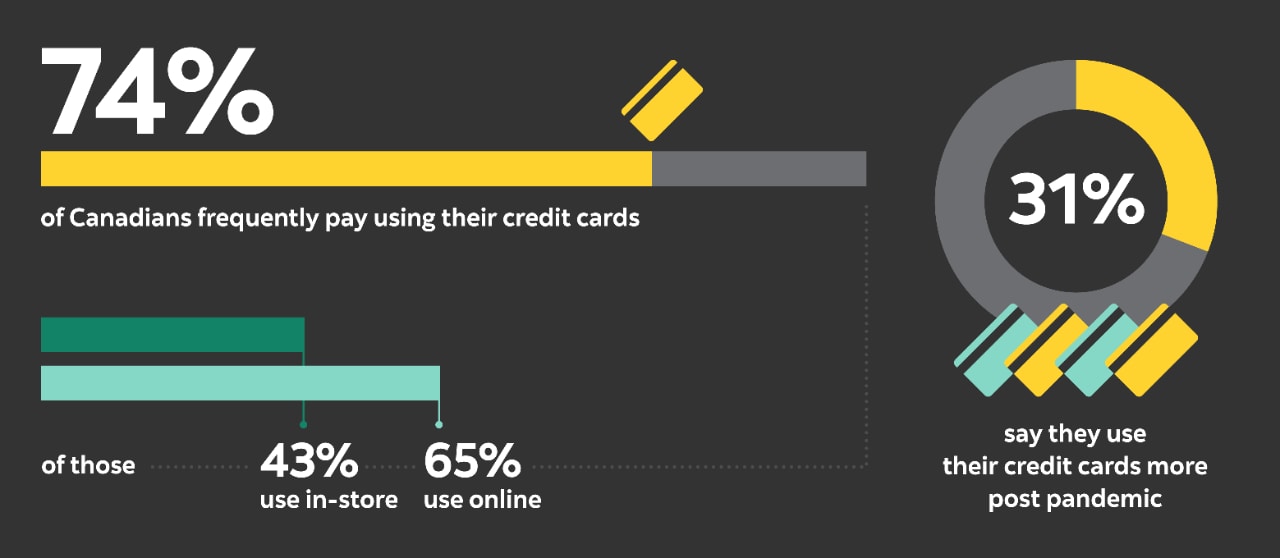

DID YOU KNOW?

More than 70% of Canadians pay their credit card balance in full each month5

Credit card pre-approval doesn't necessarily mean you're guaranteed to be approved. But with some financial institutions it often means you will be approved, unless you've become bankrupt in the interim. Other lenders, on the other hand, might take into consideration any significant changes to your credit history since your pre-approval.

Even if the lender reached out to you first, they can turn around and deny your application. While it might seem like a pre-approved credit card application won't be declined, it all depends on a lender's pre-approval policies. Some lenders, for example, won't decline a pre-approved credit card other than in the event of bankruptcy, but others may have more stringent policies. If they do, you could still be declined after a pre-approval credit card offer.

The following are examples of financial changes that a lender with more stringent policies might consider:

- Updated information. Transunion and Equifax, Canada's two main credit reporting agencies, compile individuals' credit files based on information they collect from various sources, including creditors. If your credit report was updated with new information in the time between the lender's prescreening and your credit card application, you might no longer meet the lender's criteria.

- Recent financial mismanagement. Your financial life doesn't stay static, so you might have made some financial decisions recently that have a negative impact on your credit history. For example, if you've applied for several credit products since you were prescreened, these will now show up as separate credit checks on your credit report. The lender could consider this a red flag.

- Major financial changes. Some credit card issuers may take income or other eligibility requirements into consideration. If they do, big changes in your life that affect your finances could potentially lead to your application being declined despite your pre-approval offer. These might include a change to your employment status or income (for example, if you were laid off).

One worry people often have when they receive a pre-approved credit card offer is the impact on their credit score. After all, the lender had to check your credit information when they pre-screened you. Doesn't this cause your credit score to drop?

Whenever you apply for credit, the lender or financial institution does a credit check, which shows up as a "hard" check or inquiry on your credit report. Hard inquiries have the effect of temporarily lowering your credit score — and if you get too many of them, it's not just your credit score that's affected. Lenders often consider multiple or frequent credit applications to be a sign that a potential borrower may be dealing with financial issues.

But a pre-approval is a "soft" credit check. Soft inquiries are inquiries that are non-credit-related. Unlike a hard inquiry, soft checks are only visible to you, which means lenders and creditors can't see this information.

Examples1 of soft checks include:

- account reviews (pre-approvals fall into this category)

- your own inquiries

- identity verification

- insurance underwriting

A recent study found that 74% of Canadians frequently pay using their credit cards — 43% in-store and 65% online.2 The pandemic has had an impact, too: 31% say they now use their credit cards more.3

Using credit cards more frequently can be either positive or negative though — for example, as we explore below, if you're not paying off your balance in full each month, using your credit cards more often can have a detrimental impact on your financial health.

Receiving a pre-approved credit card offer indicates the credit card company considers you creditworthy. But should you accept the offer?

There are several benefits of saying yes to that pre-approved offer, including:

Building credit

If you've never had credit before, credit cards can be a good way to build your credit rating. In fact, obtaining and responsibly using any credit product will help your credit score. But just accepting a pre-approved credit card offer won't help you build credit.

You'll also need to show a consistent history of good credit practices. This includes making payments on your credit products on time and not defaulting on loans.

To use your pre-approved credit card to build a solid credit history, pay at least the minimum monthly payment on time each month. If you can, it's always a good idea to pay off your balance in full each month.

Credit utilization ratio

By accepting the pre-approved credit card, you'll increase your total available credit. This in turn will decrease your credit utilization ratio, which has a positive effect on your credit score and will help you build credit. So accepting a pre-approved credit card can be a significant pro, if you intend to keep the card and consistently pay it down each month to keep your credit utilization rate low. Your credit utilization ratio, also known as the credit usage rate, is a percentage that shows how you're using your credit. It's calculated by dividing your total debt by your total credit limit and multiplying the result by 100.

For example, let's say you have a $10,000 line of credit and a $2,000 credit limit on your credit card, giving you a total credit limit of $12,000. You owe $3,000 on your line of credit and $500 on your credit card, for total debt of $3,500. Your credit utilization ratio would be 30% (3500/12000 x 100).

According to the Financial Consumer Agency of Canada, it's wise to use less than 30% of your available credit.4 Having a credit utilization ratio of 30%, such as in our example, would be considered a good credit utilization ratio.

Diverse credit mix

When calculating credit scores, credit bureaus also consider a mix of credit products to be a positive factor. For example, if you have a mix of loans, credit cards and lines of credit in your credit file, it's better for your credit score than if you only had a personal loan or a line of credit.

If adding a credit card would give you a wider mix of credit products, saying yes to a pre-approved card offer can help improve your credit score, especially if your mix of credit products includes few or no credit cards.

Intro specials, rewards and perks

Pre-approved credit card offers often come with intro specials and rewards. For example, a card might offer a special reduced interest rate for the first six months, low-interest balance transfers, waiver of the first year's annual fee or increased limited-time travel or cash-back rewards.

These rewards are another reason many Canadians say they like to use credit cards.5 Depending on the credit card, rewards might include points that can be put toward travel or shopping, or a cash back percentage. Some credit cards come with certain perks, too, such as travel insurance benefits or online travel booking.

If your pre-approved credit card offer comes with perks or rewards that interest you and you have good financial payment habits, it might be a good card to add to your credit mix.

Despite the benefits, there are reasons why it might be good to say no to your pre-approved offer. These reasons include:

Effect on your credit score

Some lenders may conduct a hard inquiry when you accept their pre-approved credit card offer. This could impact your credit score, especially if you've also applied for other credit products recently.

If you don't really need the additional credit the pre-approved card provides, it might make more sense not to accept the offer.

For example, let's say you're planning to apply for a loan to purchase a car in the near future. You might decide it's better not to risk any potential negative impact on your credit score until after you've been approved for the car loan.

Potential increase to debt load

When it comes to financial management, the practice of self-awareness is key. In 2021, more than 70% of Canadians paid their credit card balance in full each month6, meaning they used their credit cards for zero interest. But in the current economic climate, it can be more difficult to practice this kind of financial discipline.

Having new available credit can be tempting. If you aren't good at resisting this kind of temptation and don't always pay off your balance in full, you could find yourself with an increased credit card debt load. This would negate all the positive effects on your credit score that saying yes to the new credit card brought you.

Higher interest rates

Although pre-authorized credit cards often come with an intro discounted interest rate that can be very appealing, these rates are typically time-limited. If you plan wisely, you can make use of the period of lower interest without running afoul of the normal, higher, interest rate.

But this can backfire if you end up with an outstanding balance once the regular rate kicks in, as the interest rate for your new card might be much higher than the discounted rate. Unless you make a habit of paying off your credit card balance in full each month, this higher rate could have a significant negative impact on your debt burden.

Takeaways

Getting a pre-approved credit card isn't a guarantee that you'll be approved for the card if you decide to accept the offer. What it does mean is that the lender feels you're a good fit for their card, based on your credit information, and you're likely to get the card, although some lenders may require a credit check to confirm its initial assessment. Whether or not you accept the offer should be based on an understanding your current financial situation and the pros and cons of applying for the pre-approved credit card offer.

This article is provided for information purposes only. It is not to be relied upon as financial, tax or investment advice or guarantees about the future, nor should it be considered a recommendation to buy or sell. Information contained in this article, including information relating to interest rates, market conditions, tax rules, and other investment factors are subject to change without notice and The Bank of Nova Scotia is not responsible to update this information. References to any third-party product or service, opinion or statement, or the use of any trade, firm or corporation name does not constitute endorsement, recommendation, or approval by The Bank of Nova Scotia of any of the products, services or opinions of the third party. All third-party sources are believed to be accurate and reliable as of the date of publication and The Bank of Nova Scotia does not guarantee its accuracy or reliability. Readers should consult their own professional advisor for specific financial, investment and/or tax advice tailored to their needs to ensure that individual circumstances are considered properly and action is taken based on the latest available information.

Sources:

1https://www.transunion.com/blog/credit-advice/the-difference-between-hard-and-soft-credit-inquiries