Key takeaways:

With so much to plan for while you’re in college or university, drafting a student budget may not feel as pressing as deciding where you're going to live or what classes you'll take. But don't skip this big to-do item — it’s one of the best ways to start reaching your financial goals.

A budget gives you a roadmap for purchases and helps you to become more mindful about your spending, so you can stay Zen even during midterms. When you know how much money you have available in your bank account, you can make better financial decisions and make a better call on which purchases are worth making and which are not.

You'll not only be less likely to overspend on things you don't care about, like subscriptions you don't use, but you may also feel happier and more satisfied with the purchases you do make since you'll know you can afford them.

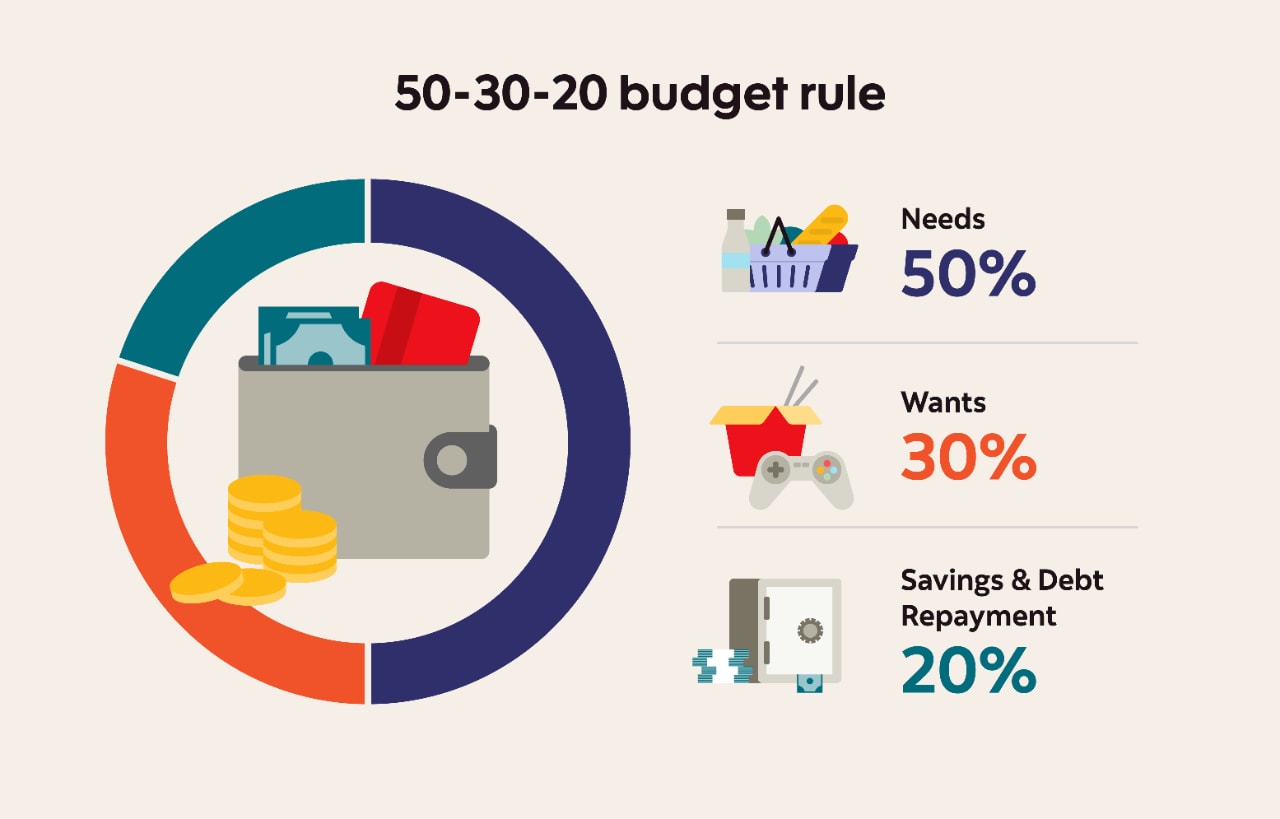

One popular and well-known budgeting technique is the 50-20-30 budget rule, which is simple to memorize and use.

The 50-20-30 budgeting rule is a simple rule-of-thumb for how to allocate your income. When you follow the 50-20-30 rule, you prioritize your budget based on the following categories:

Needs: 50%

At least 50% of your income should be set aside for anything you need to survive, such as food, housing and transportation costs.

Savings: 20%

Before you allocate the rest of your money to things you would like to buy, but don't need to survive, first set aside at least 20% of your income for savings. These savings could be for future short-term needs, such as next semester's books budget or starting an emergency fund, or it could be for long-term needs, such as tuition fees, a new car or paying off your student line of credit.

Wants: 30%

If you can, try to set aside at least 30% of your income for the things you don't need now or in the future, but that you really want. Leaving enough room in your budget for fun you can afford will make it easier to say no to unaffordable purchases.

Before you make a budget, start by estimating how much money you'll have available. That's tough if you haven't set foot on campus yet and aren't sure how much you'll earn. But you can guess.

Tally up how much you expect to have from your sources of income, including any family contributions, part-time work or student loans. Some students may also rely on savings from a Registered Education Savings Plan (RESP) to help offset costs.

If you plan to take on a work-study job, check with your college’s or university's financial aid office to see what wages undergraduate students can expect. Depending on your situation, your expected earnings may also be listed in your student financial aid package, especially if you have demonstrated financial need.

If you decide to work off campus, remember to keep your hours manageable. If you're a full-time student, you'll be highly limited in the number of hours you can work.

The next step is to add up all of your expenses. But since you're new to college or university, you'll first need to figure out what those expenses will look like.

Your overall expenses, including tuition fees and living expenses, will likely vary depending on your situation. For example, a student who lives on campus at a post-secondary institution might spend more on room and board than a student who lives at home or in an off-campus apartment with roommates.

Did you know?

On average, living costs are around $15,000 per year for university students.

Source: University Study

Students who live off-campus also have to account for utilities, transportation, rent and groceries — all of which can add up quickly. Similarly, an international student will likely pay more for tuition and travel.

EduCanada offers a search tool you can use to get an idea of what you might pay, depending on the school, your intended major and your personal circumstances, such as whether you're studying in a big, expensive city.

Ask your college or university about average student expenses

Many universities will also break down estimates for the total cost of attendance by category and give you the most up-to-date information for how much it costs to live in a dorm, enroll in a meal plan or pay tuition and expenses for the academic year.

They'll also include estimates for other common purchases, such as books, technology, transportation, student life activities and extracurricular expenses. Always check your school's website for the latest information.

Do some research

It's also a good idea to research outside costs yourself since your school’s estimate may not be accurate or up to date. For example, if you plan to live off campus, check the average cost of gas or public transit, as well as average rents near campus. Similarly, if you decide to live on campus, check which amenities are within walking distance. Is there a grocery store nearby? What about shops and restaurants?

Drafting a budget isn't hard. But sticking to it can be if you don't have much practice at being in charge of your own money. Luckily, you can take steps to make your life easier. The key is to build in some flexibility and ensure that your spending plan is reasonable.

Here are some more budgeting tips for students:

1. List your total income

Your income could include any of the following and more: how much you expect to earn through a work-study gig or a part-time job, help from family, student grants, scholarships, bursaries, a student line of credit or student loans.

2. Assess your total expenses

- List expenses yourself: Next, list every potential expense for the next school year, including occasional purchases and everyday expenses. Be thorough.

- Look for available useful tools: Also check out the online budget planner by the Financial Consumer Agency of Canada, which lists a wide variety of potential costs, including ones you might easily forget about, such as gifts, laundry, toiletries, haircuts and cellphone bills. It also lists non-essential purchases, such as entertainment, so you don't forget to build in room for fun.

3. Do some math

- Add it all up: Once you've estimated how much you plan to spend in every category and added it all up, subtract the expenses from your income and check how much extra money you have.

- Then cut some out: If there's not much wiggle room between your income and expenses or you're spending more than you're taking in, then it's important to start cutting. Be realistic, but firm. Consider your everyday spending habits and look for opportunities to shift your habits or try something new to save money. You can also trim your expenses by searching for student discounts and limiting how much you're willing to pay for certain purchases.

4. Use budgeting tools to help

If you're feeling overwhelmed, don't worry. There are plenty of tools to help make budgeting and money management relatively effortless. Here are some you could try:

- Scotiabank’s Money Finder Calculator: Makes it quick and simple to compare your expenses to your income and calculate your likely savings.

- Separate student bank accounts: Keep your savings separate from your spending.

- Online and mobile banking apps: To help you pay your bills on the go, quickly check transactions, stay up to date with your finances, and offer useful tools like Scotiabank’s Pay Yourself First and Savings Finder.

You can also explore additional government resources, such as those provided by the Government of Canada, which offers financial literacy tools and budgeting help for students.

Bottom line

Making a budget — and learning how to stick with it — is an important life skill. But don't forget: You're still a student. You'll be busy, and you might make mistakes. Give yourself plenty of flexibility and remember that you're only human. No matter how tight your budget, beware of trimming it so much that you don't leave room for fun.

Try not to overcomplicate your budget — and think about using banking products built for students and youth like the Scotiabank’s Preferred Package for Students and Youth,1 which offers no monthly fees, unlimited debit and Interac e-Transfer† transactions2 and more.

Last but not least, the Scotia App can be a great place to check your spending and make sure you're still on target with your goals and overall financial situation.