You know you may need credit to secure or rent an apartment, purchase a home, qualify for a home or auto loan, or get approved for a credit card or other credit product, for example a line of credit, or a personal loan. But when it comes to building credit and what factors raise your credit score, you probably have a lot of questions.

We're here to help.

What is credit and how is it impacted by borrowing?

Having “credit” allows you to pay for a good or service using “borrowed” money – a credit card, loan, or line of credit for example, with the promise to pay it back later. Sometimes how you manage your borrowed funds (whether you pay on time or how much you borrow) is referred to as your “credit history.”

A credit score is a number that represents your financial health and credit worthiness at a specific moment in time and helps lenders decide whether you're likely to repay your debts on time and whether they should extend “credit” to you.

Many banks require you to have a credit score (which is based on factors including your credit history) and a good credit score before you can be approved for a credit product, which can put younger borrowers and newcomers to Canada at a disadvantage.

Building your credit history when you're just starting out can feel challenging, but Scotiabank offers several options that can help. For example:

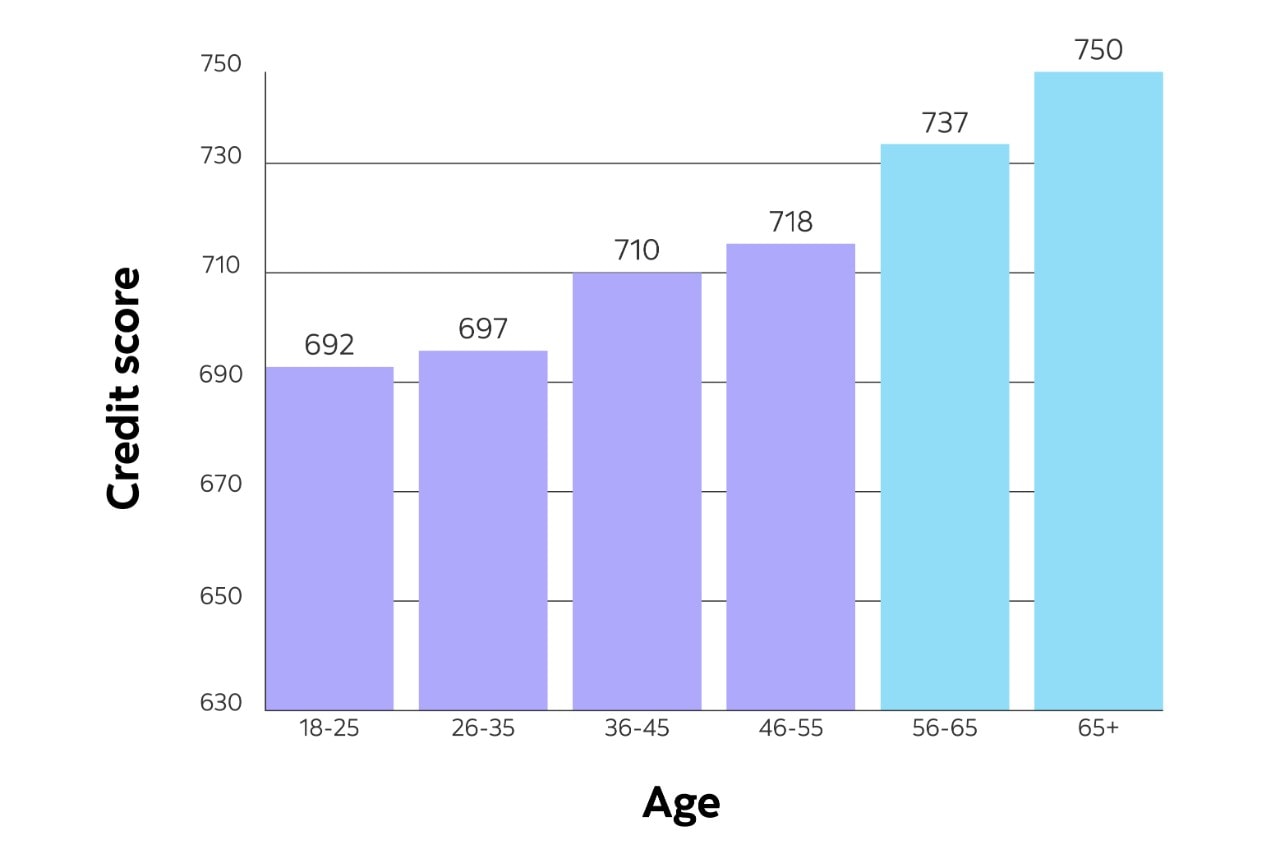

Canadians over age 65 are the most likely to have credit scores above 750 while the highest percentage of Canadians with credit scores below 520 tend to be 25 or younger.

1. Student credit cards

There are a variety of student credit cards currently available that can help you build your credit history (while collecting rewards in some cases on your purchases), and they have no annual fee.1

2. Scotiabank’s StartRight® Program

For newcomers to Canada, you need time to build a credit score in Canada or you may not even have one. This program can help you start banking in Canada with access to credit, savings, no-fee international money transfers and help from Financial Advisors.†

How does a credit score work?

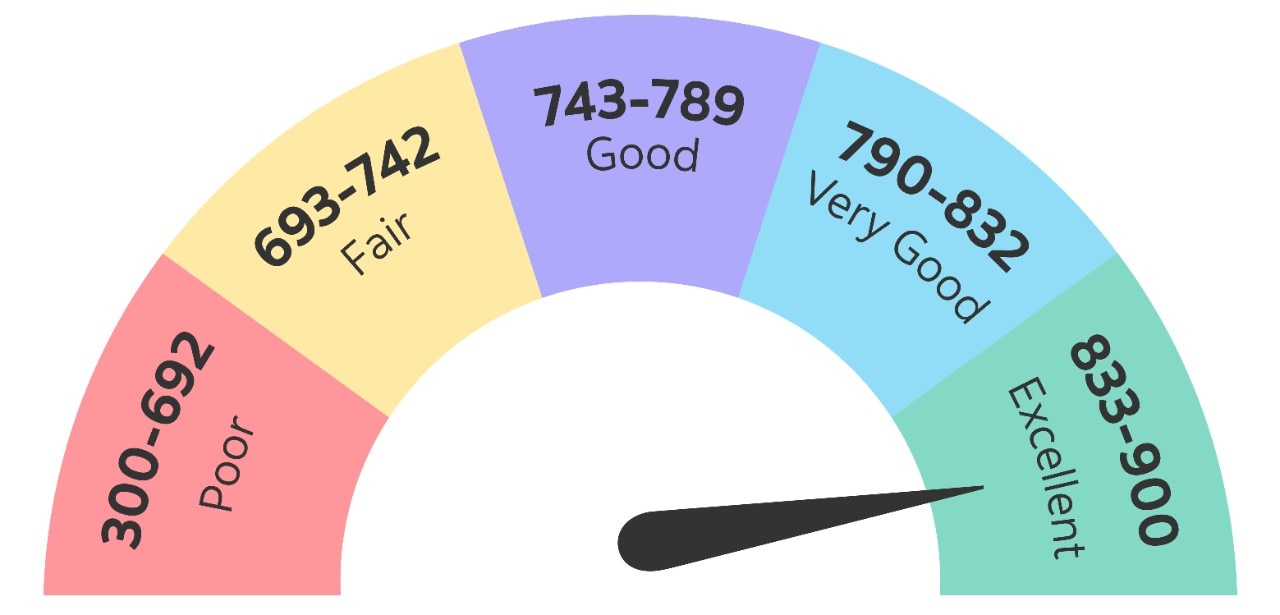

Your credit score is a number. In Canada, credit scores range from 300 to 900. Lenders look at your credit score as part of their criteria to determine factors such as if they're willing to lend to you, how much they are willing to lend to you, and what interest rates they'll offer. The higher the score, the better the chances that lenders will see you as creditworthy and want to lend to you credit at good interest rates.

Credit score ranges

Curious about what is the average credit score in Canada? Data shows that the average Canadian has a credit score of 667.2

You may be asking, “What is a good credit score for my age?" Age may also play a role in credit scores.

In general Canadians over age 65 are the most likely to have credit scores above 750 while the highest percentage of Canadians with credit scores below 520 tend to be 25 or younger.3 The reason: good financial habits and your credit history take time to develop, but you can speed up the process by following some of the tips that help you raise your credit score.

Credit scores by age range

Source: Equifax Generational Study 2018

What factors may raise your credit score?

There are a few things you can do to help ensure you're setting yourself up for success when it comes to increasing your credit score. You'll need to know your credit score before you can raise it, which is why Scotiabank has made it easy for customers to get their free credit repot4 on the Scotia mobile app.

If you check your credit report and your score is low, follow these tips for how to help increase credit scores.

Payment history

Do you pay your bills in full and on time? A strong payment history is an important part of your credit score; it will help improve your score and helps lenders see you as a responsible borrower and a good credit risk. Be sure to pay at least your minimum payment by the due date.

Account activity

Limit the number of credit bureau inquiries, (these occur if you are applying for multiple credit accounts from various lenders in a short period of time), which may give lenders the impression that you're a credit seeker who's having financial issues and needs credit urgently. Try to apply for credit only when you need it, for example, when you arrive in Canada.

Length of credit history

Up to 15% of your total credit score is based on the length of your credit history.5 In general, the longer you use your credit products and ensure you make payments on time, the better it should be for your score.

Now that you know what can affect your credit score, you can focus on building credit or improving your score.

Strategies to build credit

If you've just arrived in Canada or reached the age of majority, it's important to start building your credit history.

Applying for a new credit card like the Scotiabank Value® Visa* Card for newcomers to Canada or the Scotiabank® Scene+™ Visa* Card can allow you to begin building your credit history. Use your credit card to make small purchases and pay the balance each month on time or secure a mortgage, car loan or other personal loans and in each case, pay what you owe on time; doing so – building a history of responsible credit use that includes on time payments – will help you build a good credit history.

Strategies to raise your credit score

Is your credit score lower than you'd like? You're not alone. “How to quickly raise my credit score?" and “How can I raise my credit score in 30 days?" are common online searches. Follow these tips to help build a good credit score:

Pay your bills on time.

Aim to pay your bills in full and work to pay down your debt as quickly as possible.

Get a credit card, line of credit, or other loan to help build your credit history but never borrow more than you can afford to repay.

Don't spend more than your credit card (or other credit) allows and maintain a balance of less than 30%6

Don't borrow more than you can afford to pay on time.

Read your monthly checking account and credit card statements and check your credit reports to ensure they're correct. Report any errors as soon as possible to your bank or lender (statements) or credit bureau (credit reports).

Responsible credit use pays off

To build credit history or raise your credit score, ensure that you're using credit responsibly, making on-time payments, minimizing or eliminating debt, monitoring your credit report, and reporting any errors you find on your credit report. Remember, good credit is the key to accessing loans, securing the best interest rates, and setting the tone for a solid financial future.