Key takeaways:

During your working years, you do your best to set aside savings for retirement. Because once you retire, the tables turn and those savings become your income.

With Canadians spending about two decades in retirement on average (average life expectancy is 81.6 years)1, it’s important to prepare so that you can easily transition into this new chapter and start enjoying the lifestyle you want.

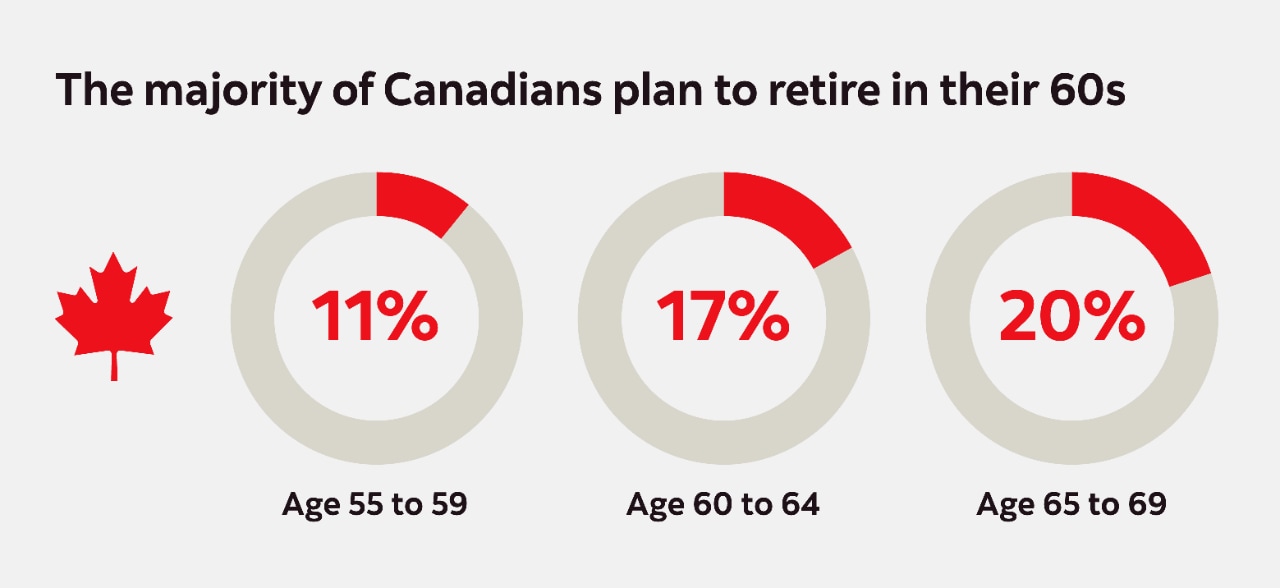

At what age do Canadians plan to retire? 2

According to a 2024 investment poll by Scotiabank, Canadians expect to need about $807,000 to fund their ideal retirement.2 Determining how much you need to save for retirement might be the most important step because once you have a goal, you can create a plan. Although this amount can change over time, your retirement savings goal will depend on when you start saving, the lifestyle you want and your income sources.

- Age: The earlier you start saving, the longer your investment time horizon — meaning the amount of time your money has to grow before you plan to access your retirement funds. And the more time your money has to grow, the more flexibility you’ll have in retirement, allowing you to potentially retire earlier, enjoy a higher retirement income, or leave a legacy for loved ones.

- Lifestyle: Everyone’s ideal retirement looks a little different. Do you dream of travelling or taking up new hobbies? Do you plan to age in place in your current home or at a senior living community?

- Income sources: Do you have income from a workplace pension plan, such as a defined benefit plan, a defined contribution plan or another type of pension or savings plan? How much will you be eligible for through government benefits? Do you have personal savings set aside?

The Retirement savings calculator can help you get started to determine how much you will need to retire.

Whether you’re nearing retirement or still have some time before putting your retirement plan into play, there are many things to consider.

1. Review your retirement income sources

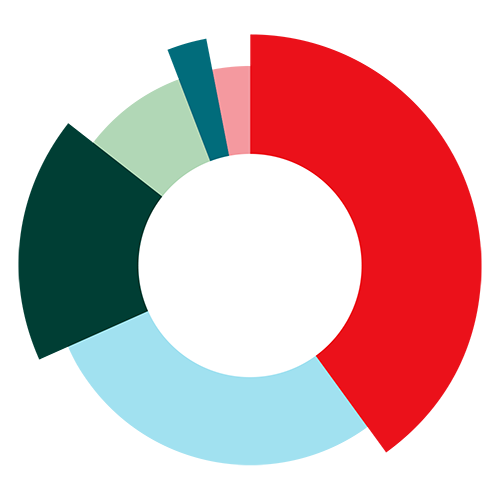

Primary sources of retirement income for Canadians preparing to retire2

26%

Personal employer sponsored pension plans

25%

Government pension programs

16%

Personal savings held in RRSPs/RRIFs

Your first task is to make a list of your anticipated income sources during retirement. This can include government pension programs, workplace pension plans, registered accounts like a Registered Retirement Savings Plan (RRSP), Tax-Free Savings Account (TFSA), and Registered Retirement Income Fund (RRIF), and non-registered accounts.

To make sure your list is complete, ensure you list these details:

- The value of your retirement and savings accounts. If you hold investments at multiple financial institutions, be sure to include all of your accounts.

- Expected income from a workplace pension plan, such as a defined benefit plan or a defined contribution plan.

- The value of your current assets, such as rental income properties, jewelry, artwork and collectibles.

- The amount of your Canada Pension Plan (CPP)/Quebec Pension Plan (QPP), which is funded through contributions from both you and your employer.

- Anticipated monthly payments from the Old Age Security (OAS) pension, which is funded through a percentage of income tax all Canadians pay.

Did you know?

You can find your CPP/QPP or OAS eligibility by checking your My Service Canada Account (MSCA) for CPP and OAS, or by signing up for a clicSÉQUR account for QPP. For a personalized estimate of your benefits, you can obtain your online Statement of Contributions (for CPP) or Statement of Participation (for QPP) through these services, as they provide details on your earnings and potential benefit amounts.

Try out the Canadian Retirement Income Calculator from the Government of Canada website to help estimate how much money you might have when you retire.

2. Optimize your investment portfolio

When reviewing your income sources, it’s important to also review your investment portfolio. Over time, goals can change — you may have decided to work longer than you initially planned or move closer to children and grandchildren.

To optimize your retirement savings strategy, you can work with your financial advisor to:

- Ensure your investment mix is aligned with your risk tolerance and retirement timeline.

- Explore tax-efficient investment strategies, such as maximizing contributions to an RRSP or TFSA.

- Consider investing in ETFs and mutual funds in your portfolio, taking advantage of the strengths of each for different parts of your investment strategy. Scotia Essentials Portfolios™ combine a mix of ScotiaFunds® and cost-effective Exchange-Traded Funds (ETFs) into one convenient solution. They’re also available in Series T options to provide monthly cash flow in retirement.

- If your employer offers a group RRSP or retirement plan, make sure you contribute enough to get the maximum employer matching. This is a great way to boost your retirement savings.

3. Understand what federal government benefits are available

The Canadian government offers three retirement benefits. Keep in mind that you don’t get these benefits automatically — you must apply for them.

Benefit |

How much can you receive? |

When can you apply? |

Depends on your average earnings throughout your working years, your CPP contributions and the age you start your CPP pension |

As early as age 60 or as late as age 70, but monthly payments may be smaller if you start receiving payments before you turn 65 |

|

Depends on your other income and how long you’ve lived in Canada |

Age 65 (or older): If you are living in Canada, you must be a Canadian citizen or legal resident and have resided in Canada for at least 10 years since the age of 18. If you live outside of Canada, you must have been a Canadian citizen or a legal resident of Canada on the day before you left Canada and have resided in Canada for at least 20 years since the age of 18. |

|

Guaranteed Income Supplement (GIS) for OAS pensioners with low income |

Depends on your marital status and your previous year’s income (or in the case of a couple, your combined income) |

Age 65 or older |

Also, even if you receive a public pension, you may be eligible for tax deductions and credits. Consider working with a tax professional to understand your options.

Ages to remember

Age 60 →

Canada Pension Plan (CPP)/Quebec Pension Plan (QPP) may begin

Age 65 →

Old Age Security (OAS) and Guaranteed Income Supplement (GIS) may begin

Age 71 →

You must convert an RRSP into an RRIF or annuity

4. Track or create a budget

According to many retirement professionals, you should expect to spend about 70% to 80% of your pre-retirement budget once you retire. That amount is easy to determine — if you have a budget.

If you’re not in the habit of keeping a budget, Scotia Smart Money can help you create one.3 It makes it easy to track your bills, monitor spending and manage your cash flow from the convenience of the Scotiabank app. Plus, you'll get personally tailored advice on money management.

Tracking your expenses will help you to estimate how much you may spend in retirement, while also identifying debt or expenses that can be reduced or eliminated before you retire.

5. Pay off or reduce your debt

If possible, pay off all debt before you retire. Once you’re no longer working, every dollar you owe will reduce your retirement income and impact your standard of living. Prioritizing debt management now can improve your financial wellbeing later.

There’s no one right way to tackle debt. Check out these three debt repayment strategies to see if one or more is right for you. A Scotiabank advisor can review your financial situation and suggest options to pay off or reduce debt before you retire.

6. Prepare for unexpected costs

Emergencies can happen at any age. When you’re retired unexpected costs can significantly affect your lifestyle and cash flow. If you’re still working, an unforeseen cost could derail your retirement planning — and savings.

If you don’t have an emergency fund, now’s the time to create one. An emergency fund is meant to help you manage any shorter-term unexpected costs so that you don’t have to dip into your retirement savings.

Pre-Authorized Contributions (PACs) are a convenient and flexible way to build your emergency savings. You choose the amount you want to contribute from your chequing account and how often — for example, weekly, biweekly or monthly. And you can adjust the amount and contribution frequency at any point in time. Many experts advise having an emergency fund to cover at least three to six months of total living expenses to get through difficult times, should they arise.4

7. Factor in all three stages of retirement

To determine how much income you’ll need, it’s helpful to think of retirement in three stages:

- Early retirement: For the first five to ten years, spending tends to be higher. You have more free time to travel, try new hobbies and cross items off your bucket list. Many Canadians also choose to work part time during this stage.

- Mid retirement: Ten to 20 years into retirement, spending time with family and friends is often a priority. At this point, you’ll start thinking about how you’ll adjust your plans as you get older — especially where you’ll choose to live, possibly a senior living community.

- Late retirement: In this later stage, the focus is typically on health care, estate planning and leaving a legacy — ensuring your loved ones and cherished causes are taken care of. An estate plan can help to transfer assets with minimal tax burden, so there’s a smooth transition to the next generation.

8. Estimate future health care costs

While no one can foresee the future, it’s more likely that you’ll incur health care costs at some point during retirement than not.

It’s best to think about health care costs now, so you’re not surprised later. To know how much to set aside for health care premiums, research:

- Workplace health and dental coverage: This typically ends at retirement, although some retirees may have ongoing coverage paid by their employer or the option of continuing coverage at their own expense.

- Provincial health care plans: These vary widely and may only cover some of the costs for prescription drugs and long-term care facilities.

- Health insurance: This often supplements items provincial coverage doesn’t cover, such as prescriptions, paramedical services and vision and dental care. However, plans may have limits regarding annual or lifetime coverage and exempt preexisting conditions.

9. Decide if downsizing is right for you

While downsizing may seem like a great idea, the boost to your nest egg may end up being less than you expect after paying real estate commissions, legal fees and other costs.

Plus, where will you live and how much will it cost? Moving to a smaller house doesn’t always bring a significant decrease in expenses. You’ll still have to pay for utilities, property taxes, insurance and maintenance. While condo living has its benefits, there are also condo fees to consider. So while downsizing can provide a windfall, a retirement income strategy is what takes it from lump sum to lasting income.

If you have dreams of retiring early, make sure you’re both financially and emotionally prepared. Many retirees fail to consider life without work and the sense of self and social outlet a job provides.

Retirement is a transition. To ensure it’s a happy one, make a plan for what your new life might look like. If you’re a person who needs structure, dedicate certain hours of the day to accomplishing tasks on a to-do list.

To transition to this new chapter of life in an overall state of well-being, both physically and psychologically, focus on:5

- Reducing stress

- Exercising regularly

- Taking part in social activities

- Eating a balanced diet

You’ve worked hard — and with the right preparation, you can retire with ease and peace of mind. After all, you want to enjoy this next chapter to the fullest.

Speak with a professional, like your Scotiabank advisor, for retirement planning advice and guidance to ensure everything is in place for an easy transition.

This article is provided for information purposes only. It is not to be relied upon as financial, tax or investment advice or guarantees about the future, nor should it be considered a recommendation to buy or sell. Information contained in this article, including information relating to interest rates, market conditions, tax rules, and other investment factors are subject to change without notice and The Bank of Nova Scotia is not responsible to update this information. References to any third party product or service, opinion or statement, or the use of any trade, firm or corporation name does not constitute endorsement, recommendation, or approval by The Bank of Nova Scotia of any of the products, services or opinions of the third party. All third party sources are believed to be accurate and reliable as of the date of publication and The Bank of Nova Scotia does not guarantee its accuracy or reliability. Readers should consult their own professional advisor for specific financial, investment and/or tax advice tailored to their needs to ensure that individual circumstances are considered properly and action is taken based on the latest available information.

Commissions, trailing commissions, management fees and expenses may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed or insured by the Canada Deposit Insurance Corporation or any other government deposit insurer, their values change frequently, and past performance may not be repeated.

1 World Health Organization, 2024. Health data overview for Canada. (Accessed September 2025.)

2 Scotiabank: Consumer Sentiment Towards Retirement, 2024 Investment Poll.

3 To access Scotia Smart Money by Advice+, you must have an active personal banking retail product, have transacted at least once on your account within the preceding 6 months and have logged into the Scotia Mobile Banking App.

4 Government of Canada, (March 2025). Setting up an emergency fund. (Accessed September 2025.)

5 National Initiative for the Care of the Elderly (NICE). Healthy Lifestyle Behaviors for Older Adults. (Accessed September 2025.)