You got a raise this year, which is great! What's not so great is that despite the salary bump, your money doesn't seem to go as far. Everything is more expensive these days – from your favourite ice cream to the gas you'll use to drive to the store to pick up that ice cream. What's going on?

Welcome to a period of high inflation! You might have gotten a raise but you're actually making less than you were last year because of the effects of inflation.

We break down what a real wage is and how to calculate yours to help you understand why your money seems to be disappearing from your account more quickly than usual.

Inflation is what happens when a dollar can no longer buy the same things as it used to because of price increases. This gets calculated via the consumer price index (CPI), which uses a basket of representative goods to determine how much prices have gone up over the short-term or long-term. It tracks prices for common items people buy, like housing, gas, apparel, transportation, education and communication, food and beverages, and medical care.

So, why do we have such a high inflation rate right now? Some contributing factors include supply chain issues and labour shortages as a result of the pandemic. But economists will tell you some price inflation is normal (and even encouraged) from a macroeconomic perspective.

Remember a time when an older family member talked about buying their first home in their early twenties? Maybe you sighed and tried to explain that things were different now.

What's different is your real wage. You might be making more in dollars than your family member was when they paid their down payment on that velvet wallpapered mid-century modern ranch, but you're likely making less in relative purchasing power.

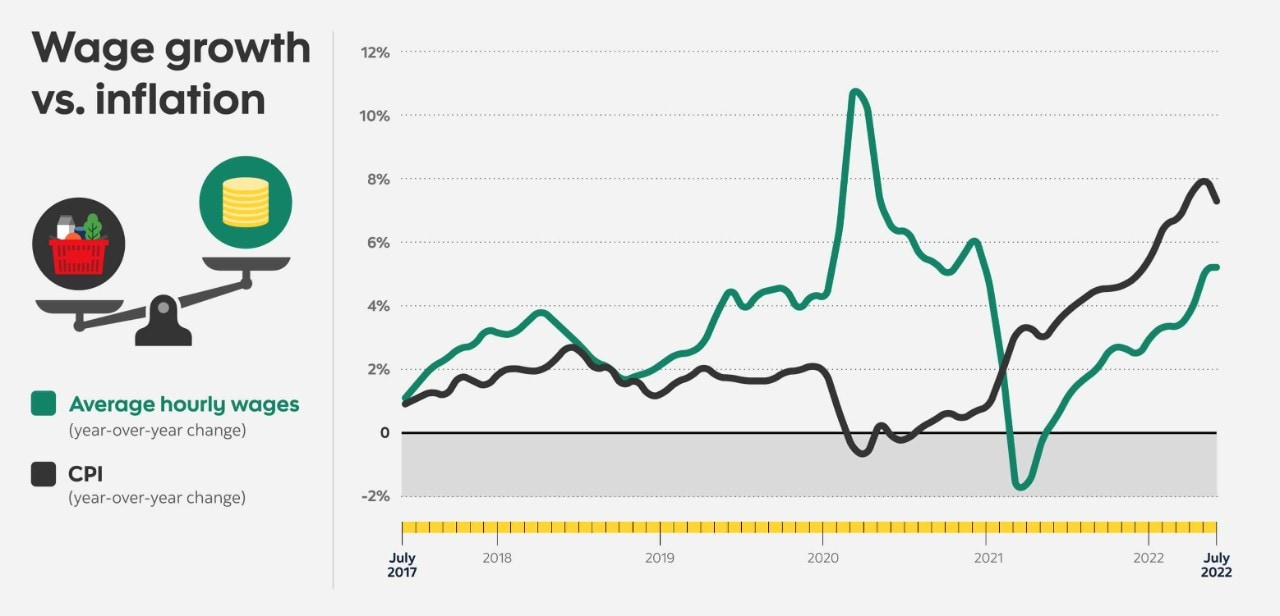

$1 in 1975 was worth $4.98 in 2021. If real wage growth had grown with inflation, then average incomes should be $99,165

Real wages allow you to compare wages in a way that accounts for the increased price of goods and services due to inflation. For example, the average yearly salary in Canada in 2021 was $65,773. In 1976, that number was just $19,932. If you looked at just your nominal wage, or the amount you make measured in dollars, you might see that as a win for wage growth.1

But with inflation, the value of $1 in 1975 was worth $4.98 in 2021. If real wage growth had grown with inflation, then average incomes should be $99,165. But they're not. They're $33,392 less. In 1975 dollars, that equals an income of $13,220.2

You might be wondering what your real wage is and if it's higher or lower than your nominal wage. As of September 2022, the inflation rate is 7.1%. If your wage increase is not equivalent to this unfortunately, you're making less.

Here's how to see just how much less:

- Take how much you made in 2021. Let's say your nominal wage was $65,773

- Add any raises you might have gotten in 2022 to that total. Let's say you got a $2,000 raise

- Divide how much you are making now by 1.076. That gives you $62,986.06

That's right, in the example above, you'd be making about $2,786.94 less this year than you made last year. That works out to $232.25 less per month. If you didn't get a raise in 2022, you'd be making even less in real wages.

Now that you know you're making less money than you were last year, what can you do about it?

1. Talk to your employer

Have a conversation with your employer and tell them that your real wage has gone down. Ask if they're planning to provide an increase to adjust for inflation or whether they can support you in other ways, such as by offering other benefits. Perhaps they can increase your eyecare benefit or allow you to work from home to save on transportation costs, for example.

If they're not able to do that, consider freelancing to make some additional cash or if you really can no longer afford the cost of living with your current job, it may be time to start searching for new or supplemental income.

2. Economize

You've likely read personal finance 101 articles that tell you the path to financial freedom is bringing your lunch to work and making your own coffee. Cutting back on your spending isn't something anyone gets excited about, but it's effective.

The first rule to doing it well is to focus on the big impactful things and not on how many plies of toilet paper you use. Call your service providers, like your cellphone and internet companies, and see if they can get you a better deal. Bonus points if you bring up an ad of one of their competitors offering a lower rate.

After you deal with the big stuff, focus on things that will save money and be fun. For example, create a lunch swap with a few coworkers, where you take turns making each other homemade food. You'll save money overeating out every day of the week and you'll get something new to eat every other day. Like lattes? Buy an inexpensive milk frother for home and experiment with flavour-infused lattes, like lavender ones. Who says spending less has to be boring?

3. Rewards points

What if we told you that you could spend the same amount you do now, buying things you were going to buy anyway, and in the future, get a cool bonus?

By using your credit card for everyday purchases, you can do just that. Even better — if you open a new credit card that has an introductory bonus or a low introductory interest rate, you can even supercharge your savings and rewards.

Some people use their rewards points, like Scotia's Scene+ points, to travel or go to the movies but you can also use them to buy things you need, pay for gift cards at places you shop every day and do countless other fun things. Rewards points can help your money do more since it's currently doing less.

While making less in real income will have an impact on your purchasing power, the good news is that inflation isn't expected to be this high forever. Eventually, your income will catch up. But by advocating for yourself at work and taking actions to ensure you economize, you can make the most out of this inflationary situation. And you finally have a good excuse to get that milk frother you've been eyeing!