Over the last decade, Canadians have seen some of the lowest interest rates in history. This has been a huge opportunity for first-time homebuyers since low rates make the cost of borrowing cheaper and buying a home easier in some markets. There's just one issue. With interest rates so low, they can only go up. When that happens, your monthly mortgage payments may go up. This has caused anxiety among buyers since rising interest rates can affect how much they can afford.

In addition, homeowners that have variable rate mortgages may also be worried about how a potential rate hike will affect their mortgage payments. While rising interest rates are something to be aware of, there are ways you can navigate this with your mortgage. Let’s walk you through what you need to be aware of.

First you need to understand how mortgage rates are set. Most people that buy a home need a loan. This is known as a mortgage and it's an agreement between you and the lender that sets out the terms including the interest rate.

When applying for a mortgage, the interest rate you're offered depends on a few factors, such as:

- The overnight rate set by the Bank of Canada (BoC), which is the interest rate banks borrow at and lend from each other in the market overnight

- Your credit rating

- Your decision between a variable or fixed rate mortgage

- The term or length of the mortgage

In most cases, the overnight rate set by the BoC has the biggest effect on variable rate mortgages. When the BoC increases the overnight rate, variable rate mortgages become more expensive. On the other side of things, when the BoC decreases the rate, carrying a variable rate mortgage becomes less expensive.

Your credit rating is another important consideration when banks determine what mortgage rate they can offer to you. If you have an excellent credit score, you'll likely be approved for better rates than if you have a lower credit score.

Your credit score is a number between 300 - 900. If your credit score falls between 700 - 900, it's typically considered good. Once your credit score drops below 700, you may find it difficult to get a good rate or even be approved for a loan.

If you want to improve your credit score, you can take steps including:

- Paying off your debt

- Always making your payments on time

- Making more than the minimum payments on your credit cards

- Keeping your account balances below 35% of your available credit

Prime rate, also called the prime lending rate, is the annual interest rate major banks and financial institutions in Canada use when setting interest rates for mortgages.

It’s influenced by the interest rate set by the Bank of Canada (BoC), which is also referred to as the BoC’s overnight or target rate. The prime rate and the BoC overnight rate are closely related as lenders use the BoC rate to set their prime rate, which generally happens within the few days following the BoC rate change announcement.

Since the Bank of Canada can change interest rates eight times a year, it's best to check their Policy Interest Rate page for the most up to date information on their current rate.

When interest rates are higher, they encourage people to save. Since it is a good time for people to save, less borrowing and spending tends to happen. When this happens, companies may increase their prices at a slower pace or even lower prices to get people to spend again. This reduces inflation since the costs of goods aren’t going up in price as quickly as they would otherwise.

Lower interest rates work in the opposite way. Not only does it cost less to borrow money when interest rates are low, but you also earn less from keeping your money in savings, which means you may end up spending more money. This increase in consumer spending could cause prices to rise as consumers are willing to pay more.

The Bank of Canada actively uses interest rate increases and decreases to control inflation. The BoC tries to keep inflation at 2% a year as most of the population can handle that level of year over year change.

A potential rate hike will affect you in different ways depending on if you're a first-time homebuyer or if you already own.

For first-time homebuyers, any increase in interest rates will reduce how much home you can afford. That's because your carrying costs (a.k.a. your costs for owning a property) will increase.

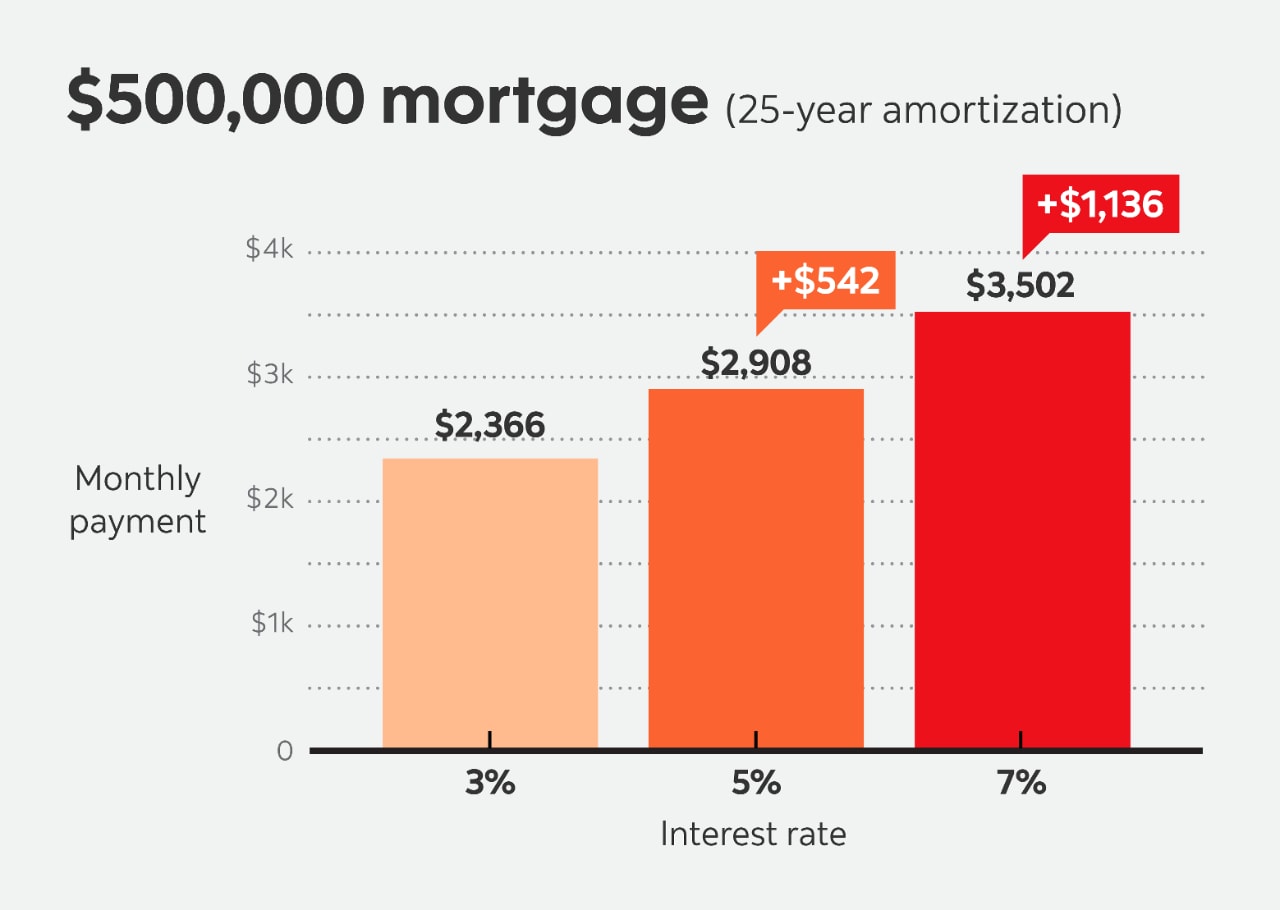

For example, let's say you need a $500,000 mortgage and the interest rate is 3%. Your monthly payment would be $2,366 on a 25-year amortization. However, if the interest rate were 5%, your monthly payment would be $2,908. That would mean you would have to pay an additional $542 each month. Suppose rates went up to 6% or 7%, you'd be looking at monthly payments of $3,199 and $3,502, respectively.

Anyone renewing their mortgage in a rising interest rate environment might be shocked at what their new monthly payments could look like.

Current homeowners that have a variable rate mortgage could also be affected. At Scotiabank, you can either have a variable rate that will increase as BoC rates rise or you could have a variable rate with Cap Rate Protection.

A Cap Rate Protection mortgage has fixed payments for the term of the mortgage that are calculated based on a cap rate rather than the current variable rate; as rates rise more of your payments would go towards interest, and less to the principal (but your monthly payment remains the same). However, if you have an adjustable variable rate, the amount you're paying would increase as interest rates rise.

While having a fixed payment variable rate mortgage can help you with your monthly budget, when your mortgage is up for renewal, you’ll see a steep increase. That's because your lender needs to factor in the increased interest rates and the amount owed to get you back on your original amortization schedule. (The amortization period is the actual number of years it will take to fully repay a mortgage loan.) That means your payments could be much higher, which may catch some homeowners off guard.

If you're a customer who has a variable rate mortgage with Scotiabank, your payments will increase in relation to the bank's prime lending rate. So when your mortgage reaches maturity, you won't have payment shock or need to reset your amortization period.

A fixed rate mortgage customer would see no impact from a BoC rate increase during the term of their mortgage.

When determining what is the right mortgage rate for you, most of the time, you will need to decide between a fixed and a variable rate. Each one has its own pros and cons so it is important to understand how each one works to make the best decision for you.

Variable rate mortgage

Pros

Lower initial interest rate compared to a fixed rate mortgage

Benefit from continued lower interest rate while there are no BoC rate increases

If you have a capped payment plan (see Cap Rate Protection mortgage described above); when interest rates decrease, more of your payments go towards the principal

If you have a adjustable payment plan; as interest rates decrease, your monthly payment will decrease

Can be converted to a fixed rate mortgage of the same term length or greater at any time with no prepayment charge

Cons

If you have a capped payment plan; as interest rates increase, more of your payments go towards interest

If you have an adjustable payment plan; as interest rates increase, your monthly payment will increase

Fixed rate mortgage

Pros

Same payments for the entire term of your mortgage; benefiting from locking in a favourable rate without the risk of being impacted by BoC rate hikes

Easy to understand and manage as payments are fixed and principal paid down by the end of the term is known

Cons

Higher initial rate compared to a variable rate mortgage

There is a prepayment charge to break your mortgage that is usually higher than for a variable rate mortgage

Generally speaking, fixed rate mortgages are ideal for people who want the security of knowing that the payments will remain the same over the term of their mortgage.

Variable rate mortgages will hold appeal to people as the initial interest rate is lower than fixed rate mortgages (depending on the current overnight rate) and offer greater flexibility than locking into a fixed rate. There is the potential to pay less interest over the term of your mortgage with a variable rate mortgage if the BoC has little to modest rate hikes. But as mentioned earlier, if the rate goes up this can mean you end up paying more interest.

Note – if you’re a Scotiabank customer, you can early renew your fixed or variable rate mortgage with no prepayment charge up to 6 months before your maturity date. In a rising rate environment, not having to wait to renew can lead to significant savings for your new mortgage term since you can renew before rates potentially go up further.

Open mortgages have flexible payment options; you can increase your payments by any amount, at any time, with no prepayment charges. Since you can make payments as you please with an open mortgage, the interest rate is usually higher than a closed mortgage.

Choosing an open mortgage is ideal for people that are expecting extra funds shortly that can be used to pay down their mortgage; this could include an inheritance, proceeds from a sale of a home, or a work bonus.

With closed mortgages, there is less flexibility to adjust or make additional payments to your mortgage. Typically, with closed mortgages you have the opportunity to make an additional lump sum payment (up to a capped amount) or increase your payments (up to a capped amount) once a year; any further payments would come with a fee.

At Scotiabank, you have three prepayment options with closed mortgages:

- Increase your payment amount (up to a specific percentage each year)

- Double up payments (on any or all of your payments) – using this option also helps you if you ever need to miss a payment in the future

- Lump sum prepayment privilege (up to a specific percentage of your original mortgage amount) each year. This can be made at any time throughout the year up to the maximum annual amount

If you are interested, you can do any combination of these prepayment options to help become mortgage free faster.

Despite the fact that interest rates can increase or decrease at any time, there are a few ways that you can protect yourself.

Get pre-approved for a mortgage

If you're in the process of looking for a home, you can get pre-approved for a mortgage. By doing this, you'll know exactly how much a lender is willing to extend to you and what your interest rate and terms will be. The rates you get with a pre-approved mortgage are typically locked in for a set period (such as 90 to 120 days). At Scotiabank, once you are pre-approved, you can hold your rate for 120 days. This allows you to shop for a home knowing that an interest rate increase won't affect you as your rate is locked in. With Scotiabank eHOME, this process has been simplified for you so that you can get pre-approved digitally from the comfort of your home within minutes.1

Choose a fixed rate mortgage

If fluctuating mortgage rates give you anxiety, a straightforward solution is to choose a fixed rate mortgage. All of your payments will remain the same for the entire length of your term, so there won't be any need to worry about interest rates for at least a few years.

Convert to a fixed rate mortgage

Most variable rate mortgages will allow you to convert to a fixed rate mortgage. You would have to speak with your lender to see what the steps are and if there are any penalties or fees that you'd have to pay. Scotiabank’s variable rate mortgage lets you convert to a fixed rate mortgage at any point in the term, as long as the new fixed rate term is long enough to complete the original term. For example, if you are three years into a 5-year term, you could convert to a 2-year fixed rate term (or longer). But you can’t choose anything less than 2 years or you may need to pay a prepayment charge.

You don’t have to feel tied down by the decision. With Scotiabank’s Scotia Total Equity® Plan (STEP), you can manage interest rate risks by customizing your mortgage solution to your risk tolerance.2

STEP allows customers to combine up to three different mortgages with either a fixed or variable rate as well as with different terms or lengths for each mortgage. A ScotiaLine® is another option available under STEP that can provide additional flexibility as there is no term or length associated with a line of credit. STEP helps you customize your borrowing so that it meets your changing life needs.

If you have a variable rate mortgage, when the Scotiabank prime interest rate increases, this means that your mortgage payment may be higher, which could impact your cashflow and budget.

Scotia advisors can clearly outline your options and work with you to decide on the best path forward. Contact your advisor to help choose the right mortgage option for you.