Key takeaways:

Over time, owning a home can offer more than a place to live. As you make mortgage payments and reduce what you owe, you may build equity, which is the difference between your home’s market value and your remaining mortgage balance.

For many Canadians, equity provides financial flexibility at different stages of life. Home equity can help pay for major planned costs — such as home improvements or education expenses — as well as help cover unexpected needs, like a broken appliance or car repair.

Two common ways to access your home’s equity are through a home equity loan or a home equity line of credit (HELOC). Understanding how they work — and when one makes more sense than the other — can help you choose the best option for your needs.

A home equity loan lets you borrow money using the equity you’ve built in your home. Because your home is used as security, the loan is registered as a mortgage on your property. This is why home equity loans often have lower interest rates than unsecured options, such as personal loans or credit cards.

You receive the money you borrow as a one-time lump sum and repay it over a set term with regular payments. Like mortgages, interest rates on home equity loans can be variable or fixed.

How much of your home's equity can you borrow?

How much you can borrow depends on how much equity you have and how your lender assesses your application. In most cases, the total amount borrowed — including your mortgage — can be up to 80% of your home’s appraised value. For example, if your home is appraised at $500,000, the total amount borrowed could be up to $400,000, minus what you still owe on your mortgage.

Home equity loans are often used for larger, planned expenses, such as major home renovations, buying a new car or consolidating higher-interest debt like credit cards or personal loans. Because payments are more predictable, home equity loans can be a good fit when you know the amount you need and want a clear repayment timeline.

At the end of the term, the loan must be repaid or renewed, based on your lender's approval, including a review of your credit score, income and home equity.

A home equity line of credit (HELOC) gives you ongoing access to your home’s equity instead of a one-time lump sum. You’re approved for a credit limit and can draw from it as needed, up to that limit.

HELOCs are similar to revolving credit, such as credit cards, in that:

- As you repay what you’ve used, the credit becomes available again.

- You only pay interest on the amount you use, not your full credit limit.

- You can carry a balance, but you must make a minimum payment each month.

HELOCs usually have variable interest rates tied to the lender’s prime rate. So, your rate — and payments — can change over time.

In Canada, the maximum credit limit for a HELOC with a federally regulated financial institution is generally up to 65% of your home’s lending value. That’s the value your lender uses to calculate how much you can borrow. This number may differ from what you believe your home would sell for, also known as the market value.

For example, if your home is valued at $500,000, the maximum HELOC limit could be up to $325,000, minus any outstanding mortgage balance. The amount you can access depends on your available equity and your lender’s requirements.

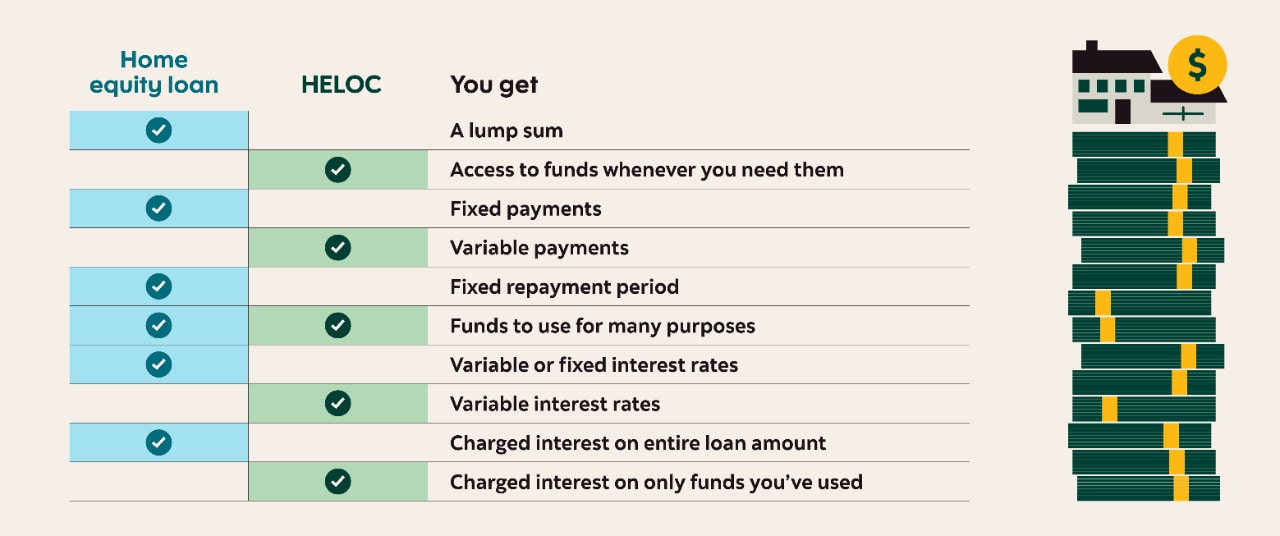

Home equity loan |

Home equity line of credit (HELOC) | |

How you get the money |

One-time lump sum |

Borrow what you need, when you need it |

| Type of credit | Term loan (regular payments over a set period) |

Revolving credit (payments vary based on usage) |

Application process |

New application is needed once the term ends |

One application gives ongoing access to a credit limit |

How repayment works |

Regular payments over a set term |

Payments vary based on usage |

Interest rate |

Fixed or variable |

Usually variable |

Interest charged on |

Full loan amount |

Only the amount used |

Maximum borrowing |

Up to 80% of your home’s appraised value (including your mortgage)* |

Up to 65% of your home’s lending value* |

Designed for |

Large, planned expenses |

Ongoing or unexpected expenses |

Examples of use |

Major renovations, debt consolidation, car purchase |

Repairs, renovations over time, ongoing education costs, flexible spending |

*With a federally regulated financial institution. |

Most lenders offer home equity loans or HELOCs. But with Scotiabank, you don’t have to choose just one option — or refinance every time your needs change.

Scotiabank offers the Scotia Total Equity® Plan (STEP), a flexible borrowing plan tied to the equity in your home. STEP lets you mix and match different Scotiabank credit products — like mortgages and lines of credit — based on your needs. It’s designed to give you more flexibility than if you were to rely primarily on credit cards, loans or lines of credit at the same time.

How STEP works

- Set it up once: STEP is established as part of your mortgage, so you don’t need to reapply each time you access your home’s equity.

- Use what fits your life: Once STEP is in place, choose and adjust your mix of borrowing options as your priorities change.

- Achieve more flexibility over time: As you build equity, additional options may become available — without refinancing or starting from scratch.

- Benefit from an automatic limit increase (if selected): As you pay down your mortgage principal, the credit limit on your designated ScotiaLine Personal Line of Credit can automatically increase, giving you access to more available credit without refinancing or reapplying.

Whether you’re planning ahead or dealing with immediate financial needs, STEP is built to suit you. To see how it could work for your situation, try the STEP calculator or consult with a home financing advisor.

Unlock your home equity with the Scotia Total Equity Plan (STEP)

What makes STEP different is how everything works together. With STEP, you can divide your mortgage into up to three separate mortgage solutions, each with its own term and interest rate. For example, you might choose a fixed rate for one portion of your mortgage, while selecting a variable rate for another.

In addition to your mortgage components, you can also add line of credit solutions — all secured under a single first-priority mortgage on your home. With one application, STEP allows you to combine different Scotiabank credit products to suit your needs.

Calculating your home equity is simple. Here’s the quick way: Home equity = what your home is worth − what you still owe on it

So, if your home is worth $500,000 and your mortgage balance is $350,000, you’ve built $150,000 in equity.

What is LTV — your loan-to-value ratio?

You can also estimate your loan-to-value (LTV) ratio, which compares how much you owe on your home to how much it’s worth. Lenders use this number to help decide how much you may be able to borrow against your home.

To calculate your LTV ratio, divide the total amount you owe on your mortgage and any other loans secured against your home by your home’s value. For example, if you owe $350,000 on a home valued at $500,000, your LTV is 70%.

Why does this matter? A lower LTV generally means you’ve built more equity, which can help improve the borrowing options available to you.

When you apply for a home equity loan or HELOC, lenders also review factors like your credit score, income and overall debt levels to make sure the borrowing fits your situation.

If you’d rather skip the number crunching, the STEP calculator can help estimate your equity and explore options in just a few clicks.

Home equity loans and HELOCs both have benefits and trade-offs to consider.

|

Benefits |

Considerations |

Home equity loan |

|

|

Home equity line of credit (HELOC) |

|

|

Both options let you borrow against your home’s equity. The right choice depends on how you plan to use the money and whether you value payment predictability or flexibility.

When a home equity loan makes sense

Consider a home equity loan if:

- You know exactly how much you need and what it’s for.

- You’re covering a large, one-time expense.

- You want predictable payments and a clear repayment timeline.

- You prefer the structure of a fixed term to help with budgeting.

When a HELOC makes sense

Consider a HELOC if:

- Your expenses are spread out or unpredictable.

- You want ongoing access to funds rather than a lump sum.

- You're comfortable with variable interest rates and changing payments.

- You want the flexibility to borrow, repay and borrow again as needed.

For many homeowners, the right solution isn’t choosing between a home equity loan or a HELOC — it’s choosing the right mix at the right time. One option may suit planned expenses, while another can help cover unexpected costs. Options like the Scotia Total Equity® Plan let you combine the benefits of both options into a single, flexible plan.