With inflation, rising interest rates and uncertainty created by the war in Ukraine, stock and bond markets definitely struggled throughout 2022. While this year’s returns have been uneven so far, it’s important to maintain a long-term perspective on your investing goals.

Five tips to keep in mind as you assess your portfolio performance statements

1. Understand that a loss on paper is not the same as an actual financial loss

You won’t realize an actual loss unless you sell your investments. While rising interest rates and recession concerns suggest volatility may continue for some time, it’s comforting to know that markets have a history of recovering from similar setbacks and have gone on to higher highs.

2. Look at your portfolio objectively

Has the current climate changed your retirement goals or timeline? If retiring is still a long way off and you don’t need access to your savings, staying the course is often the best approach.

3. Focus on your time horizon and not on this moment in time

Retirement typically spans several decades, offering time for the economy, markets and your portfolio to recover. Selling now may limit your ability to participate in future gains and could impact when you can comfortably retire – or how much sustainable cash flow your portfolio can generate during your retirement years.

4. Control what you can and take the uncertainty out of when to invest with pre-authorized contributions (PACs)

Instead of fearing market declines, consider viewing them as a buying opportunity. Investing in regular increments with a PAC plan not only helps to eliminate the guess work of when to buy, it’s a convenient and simple way for you to save without even thinking about it.

5. Regularly review your financial plan to ensure it continues to meet your needs and reflects your personal circumstances

Your financial plan helps to ensure that you’re prepared for the unexpected and focused on the long term, which in turn empowers you to see beyond the ups and downs of market volatility. If you don’t have one, a Scotiabank advisor can help set one up.

Questions or concerns?

Reach out to your Scotiabank advisor

After a difficult year like we saw in 2022, you might be wondering if your investment portfolio is on pace to meet your goals (whether that’s retiring comfortably or buying a home, for example) and how your portfolio has performed after considering market conditions and other factors, such as inflation and taxes.

It may make sense to perform a portfolio checkup once or twice a year – after you’ve had a chance to review your performance statements. You’ll also want to revisit your investment goals as you experience life changes, like the birth of a child, a change in marital status, a new job, or perhaps a move to a new city.

That’s where your Scotiabank advisor comes in. Scheduling a portfolio checkup with your advisor will provide critical insights into your investment performance and help guide your investment decisions. If you discover that your portfolio is on track to meet your goals, that’s great. However, if it’s not, your advisor can help you understand why and recommend adjustments to help keep you on track.

Your portfolio performance review: It all starts with a simple conversation

Whether you need to make adjustments to your investment portfolio or simply want to review certain goals, your Scotiabank advisor can work with you to ensure you’re on track to achieve your financial goals.

DID YOU KNOW?

According to recent Scotiabank research on Canadians working with a Financial Advisor:1

82%

Are confident in the advice they receive from their advisor

77%

Feel optimistic about the future of their finances after speaking with their advisor

65%

Indicate their advisor is proactive in reaching out, not just when they ask for advice

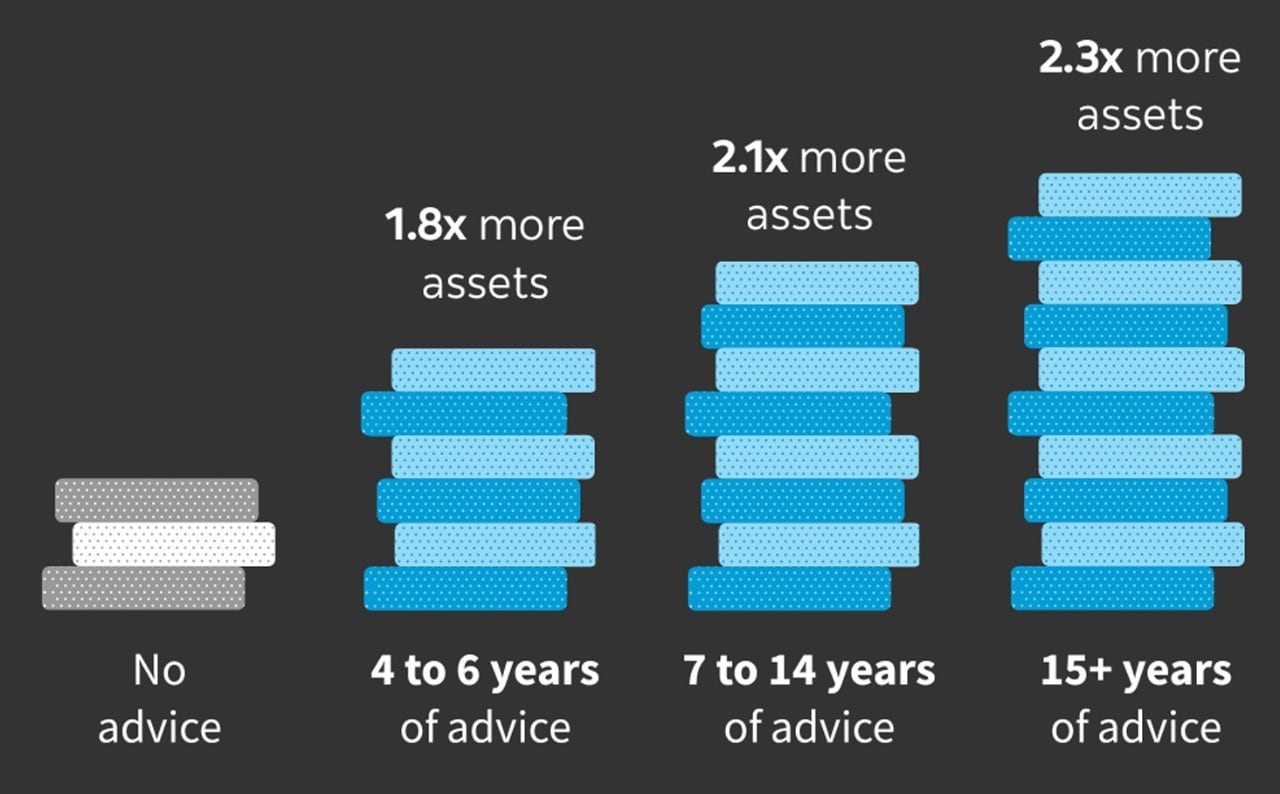

Working with a financial advisor helps you increase your wealth

Research has shown that households working with a financial advisor accumulate more assets than those that don’t – and the longer they work with an advisor, the more their savings will grow.2

Let’s have a closer look: Versus non-advised households, the average household with a financial advisor accumulated:

- 1.8 times more financial assets over 4 to 6 years

- 2.1 times more assets over 7 to 14 years

- 2.3 times more assets over periods greater than 15 years

This article is provided for information purposes only. It is not to be relied upon as financial, tax or investment advice or guarantees about the future, nor should it be considered a recommendation to buy or sell. Information contained in this article, including information relating to interest rates, market conditions, tax rules, and other investment factors are subject to change without notice and The Bank of Nova Scotia is not responsible to update this information. All third party sources are believed to be accurate and reliable as of the date of publication and The Bank of Nova Scotia does not guarantee its accuracy or reliability. Readers should consult their own professional advisor for specific financial, investment and/or tax advice tailored to their needs to ensure that individual circumstances are considered properly and action is taken based on the latest available information.

1 Scotiabank Investment Poll 2022.

2 More on the Value of Financial Advisors, Claude Montmarquette, Alexandre Prud’Homme, CIRANO 2020.