- High US inflation increases the odds that the Fed has fallen behind the tightening curve, possibly requiring rate hikes that come faster and are larger than previously expected. That scenario could entail an abrupt slowing of the US economy.

- Higher US rates and lower external demand would weigh heavily on Latam growth prospects. And central banks in the region that are dealing with their own inflation problems will have to find the sweet spot in their monetary tightening, calibrating the pace and size of their response to meet their price stability commitments.

KEY ECONOMIC CHARTS

Fresh inflation data in the US point to heightened external risks to the Latam region. As Scotiabank’s Derek Holt argues, January’s inflation numbers released February 10 increase the odds that the Fed has fallen behind the tightening curve. And with that possibility comes the potential for faster, higher US rate hikes that could lead to an abrupt slowing of the economy.

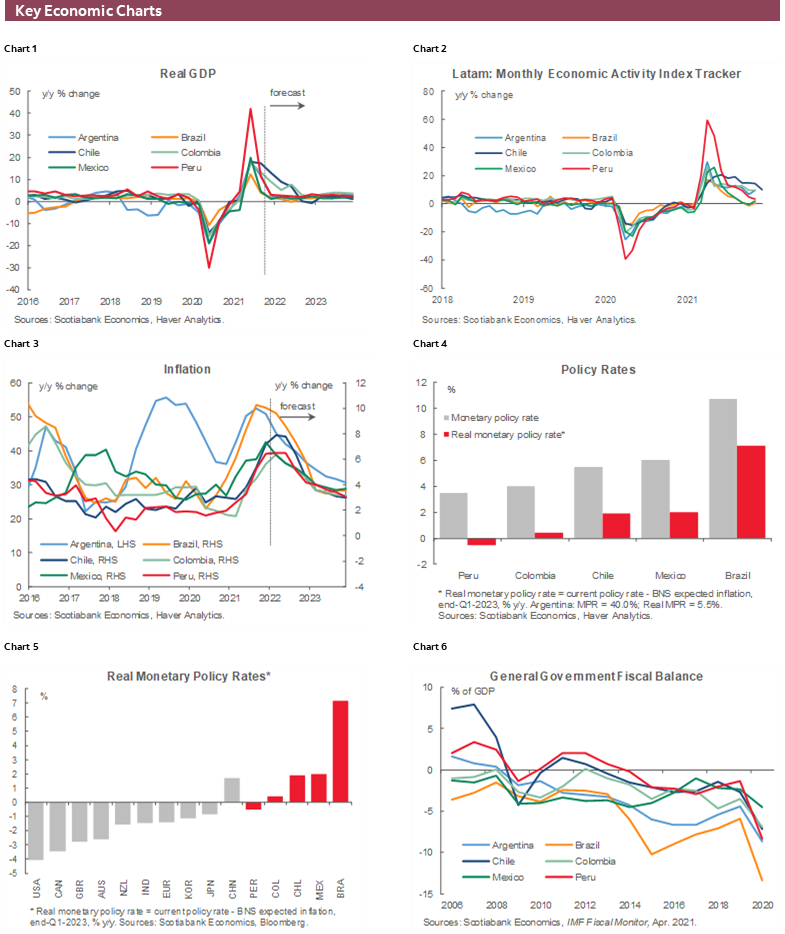

Lower external demand and higher US interest rates would weigh heavily on Latam growth prospects. Central banks in the region have been actively tightening monetary conditions to contain their own inflation problem, attempting to find the “sweet spot” in terms of a glide path for growth, which rebounded strongly in 2021 and is expected to return to pre-pandemic levels (chart 1).

Recent monthly economic activity indicators (chart 2) are broadly consistent with that profile. In Chile, for example, the December Imacec indicator showed a year-over-year increase of 10.1%, but weakness on a month-over-month basis. Meanwhile, the Ministry of Finance in Lima raised its forecast of 2022 growth to 3.5%, up from 2.5%. Similarly, in Peru, while activity slowed in December, strong growth is assured for 2021. The outlook is less certain in Mexico, which is teetering on the edge of a technical recession with two consecutive quarters of negative q/q growth. Recent activity indicators there have sent a mixed message. The situation in Brazil also warrants close monitoring as activity has fallen sharply.

Central banks’ search for the sweet spot has taken on added urgency and importance in recent weeks as additional inflation data has come in. Inflation increased significantly over the course of 2021 (chart 3), and now exceeds central bank targets. Price pressures have proven stubbornly persistent, contrary to the expectation just a few months ago. In Colombia, inflation surged higher in January to 1.67% m/m (6.94% y/y). And even where headline inflation has moderated slightly, as in Mexico, core inflation has pushed higher.

This increase in inflation across the Latam region has occurred despite higher policy rates (chart 4), which have been on an upward trajectory for the past six months or more. In this respect, while Latam central banks have moved earlier than their advanced country counterparts, they are nevertheless grappling with the question of whether they have been sufficiently aggressive in their rate hikes. Banxico in Mexico and the BCRP in Peru both raised their policy rates 50 basis points on February 10; across the region, higher rates are coming, with decisions dependent on new data as it becomes available. For example, our team in Santiago expects that the BCCh will have to raise the policy rate by 100–150 bps in its March meeting given the 1.2% m/m inflation recorded in January.

Because Latam central banks have moved earlier than their advanced country peers, real policy rates (adjusted for inflation) are now positive, with the exception of Peru (where rates remain slightly negative), in contrast to international experience (chart 5). But with US rates headed higher, that gap is likely to narrow. Going forward, therefore, external financial conditions will become more challenging.

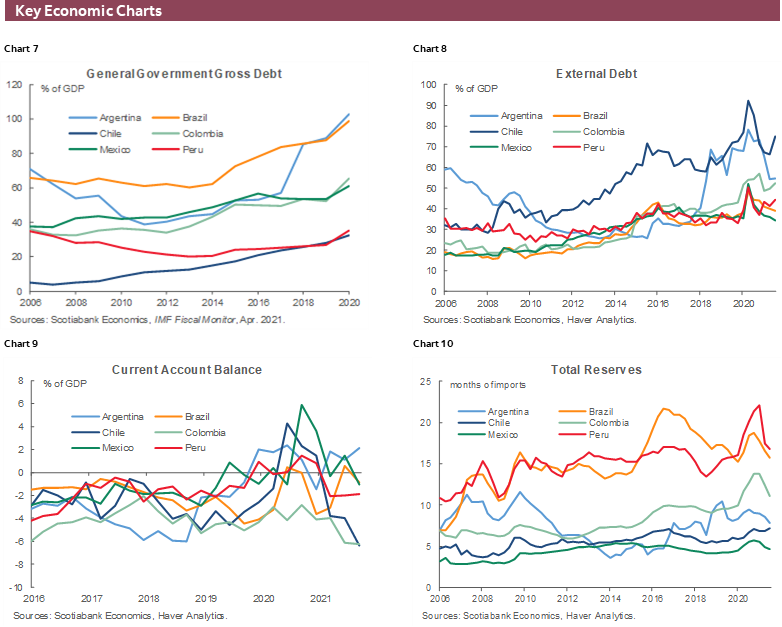

In this environment, global investors will become more attuned to, and capital flows more sensitive to, a wide range of indicators. Fiscal balances, which deteriorated in the pandemic as governments in the region provided extraordinary supports to the economy and vulnerable populations, are one such indicator (chart 6). General government gross debt as a share of GDP (chart 7) is another indicator. Latam governments have been proactive on the fiscal front, reaffirming commitments to medium- term fiscal plans and identifying fiscal reforms to ensure long-term sustainability. Meanwhile, in Colombia strong growth in 2021 has led to better-than-expected fiscal outcomes in 2021 and lower expected borrowing requirements for 2022. Strong growth in 2021 also improved tax collections in Peru, and led to a lower projected structural fiscal deficit in Chile.

Global investors and domestic residents will also be looking at external debt burdens (chart 8), current account balances (chart 9), and international reserves (chart 10). As we have repeatedly observed in recent editions of the Latam Charts Weekly, none of these are signalling immediate concerns. However, the persistent widening of current account deficits in Chile and Colombia may garner more attention in the months ahead, particularly if that trend accelerates.

KEY MARKET CHARTS

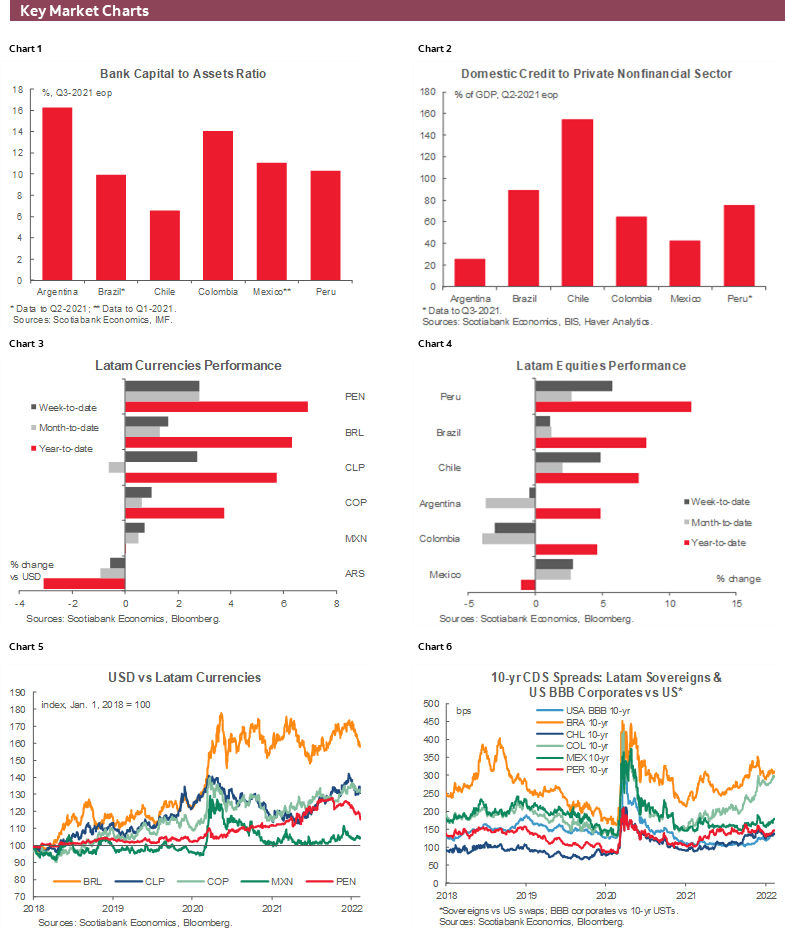

Latam financial markets have generally performed well since the start of 2022. Most regional currencies have appreciated against the US dollar, despite the increasing likelihood of larger Fed rate hikes. In contrast to their regional neighbours, Argentina and Mexico have seen their currencies depreciate.

Similarly, equity markets across the Latam region have seen strong gains over the past six weeks, led by Colombia. Mexico’s market has lost ground, likely in response to the deterioration in the economic outlook and prospects of higher rates needed to contain price pressures. Renewed political uncertainty in Peru, stemming from a revolving door on the Cabinet room, may be reflected in market losses over the past week or so.

Over a longer-term perspective, Latam currencies depreciated against the US dollar over much of 2021 (chart 5). In Peru, the PEN staged an impressive appreciation in the second half of the year, notwithstanding persistent political uncertainty, driven by strong global metals prices. For the most part, 10-year CDS spreads have been broadly stable since the start of 2022, though at levels above pre-pandemic levels in Chile and Peru; the widening spreads on the 10-year sovereigns of Brazil and Colombia in the second half of 2021 (well above pre-pandemic levels) continues to warrant attention.

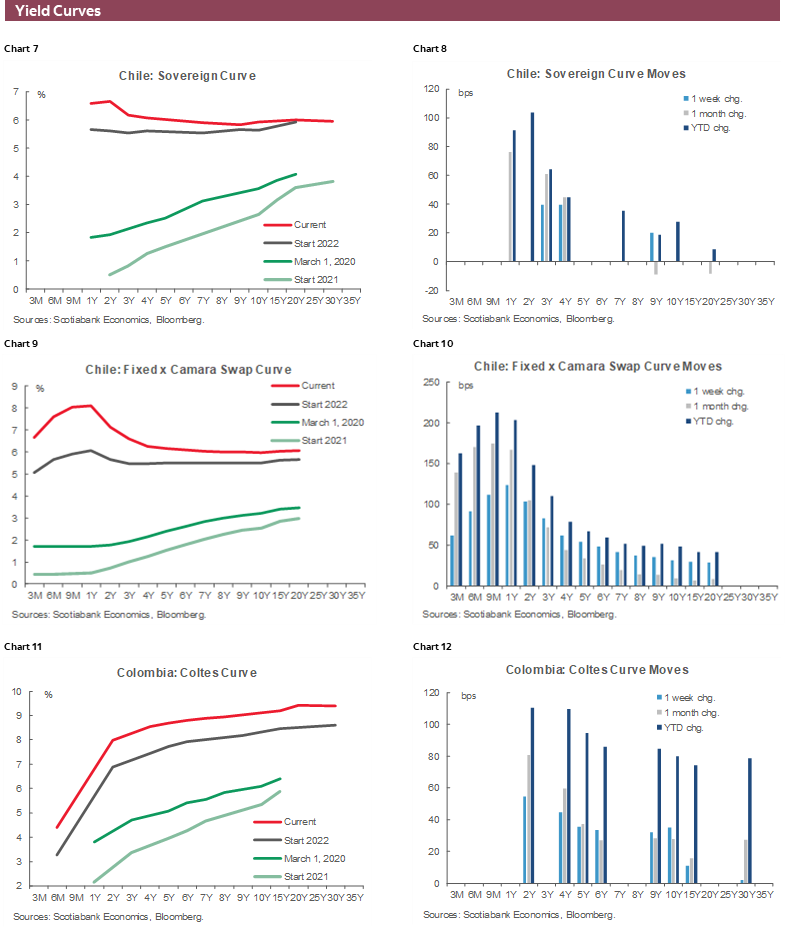

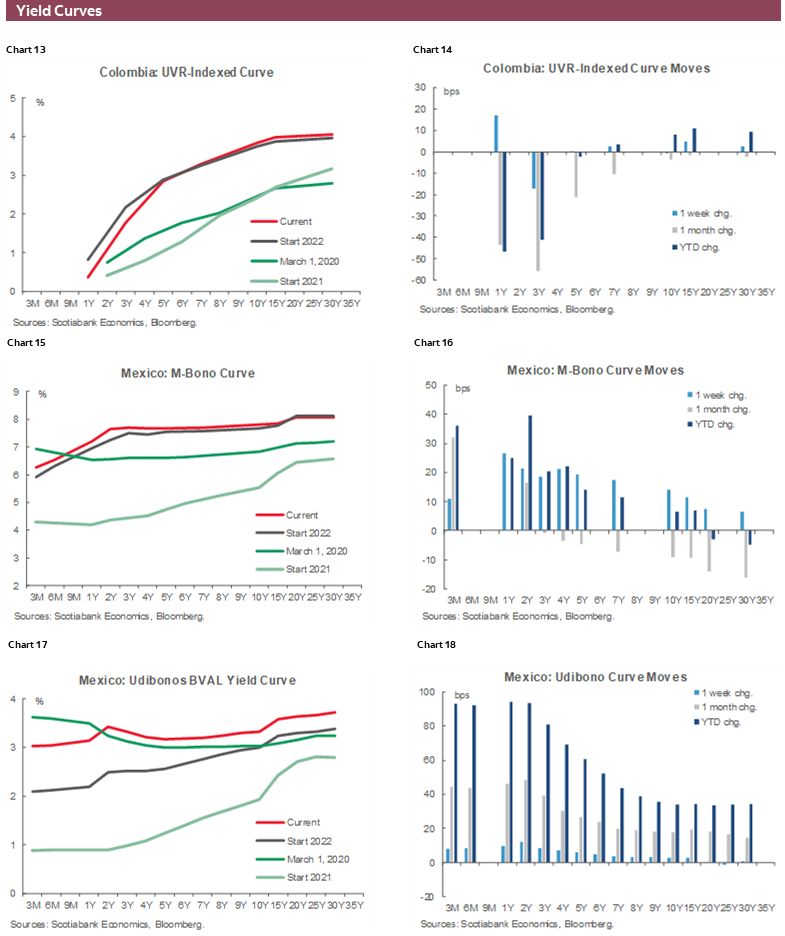

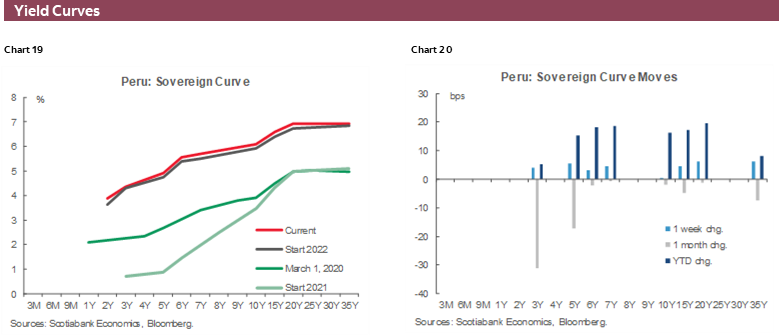

YIELD CURVE CHARTS

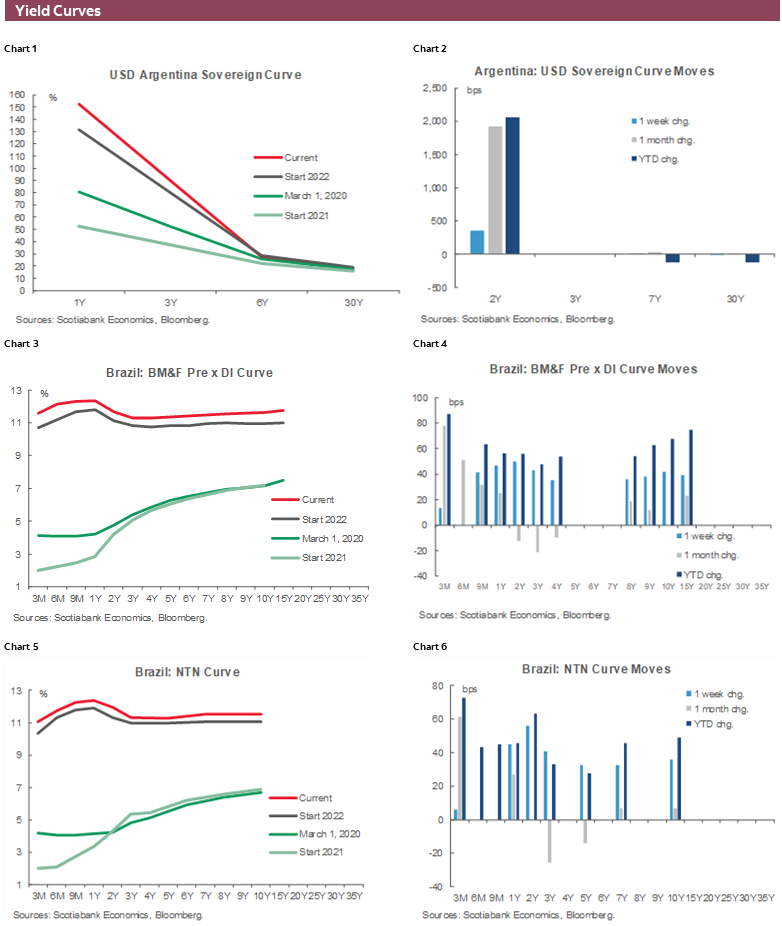

Sovereign yield curves across the Latam region have been remarkably stable since the start of the new year (charts 1–20). Most shifted up more or less uniformly across the maturity spectrum, though there has been a marked flattening in Brazil’s and Chile’s curves relative to a year ago, while Argentina’s yield curve remains highly inverted.

KEY COVID-19 CHARTS

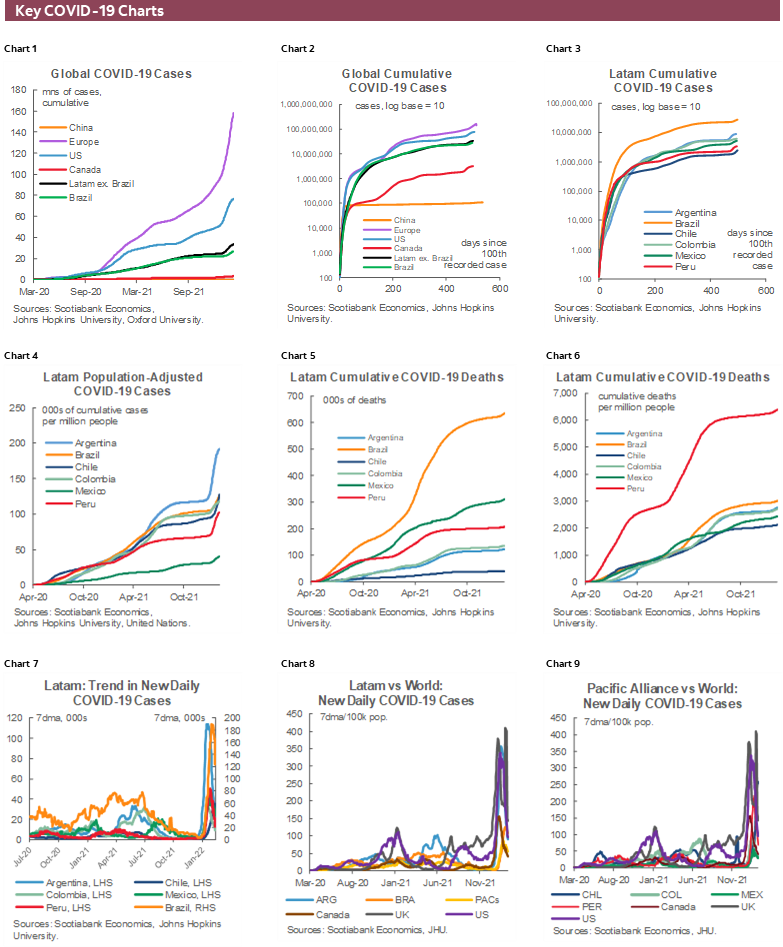

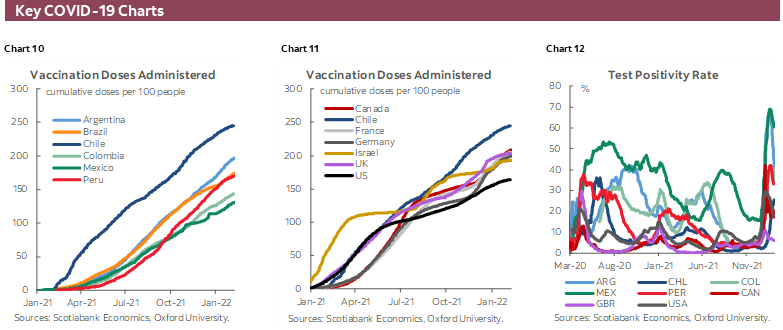

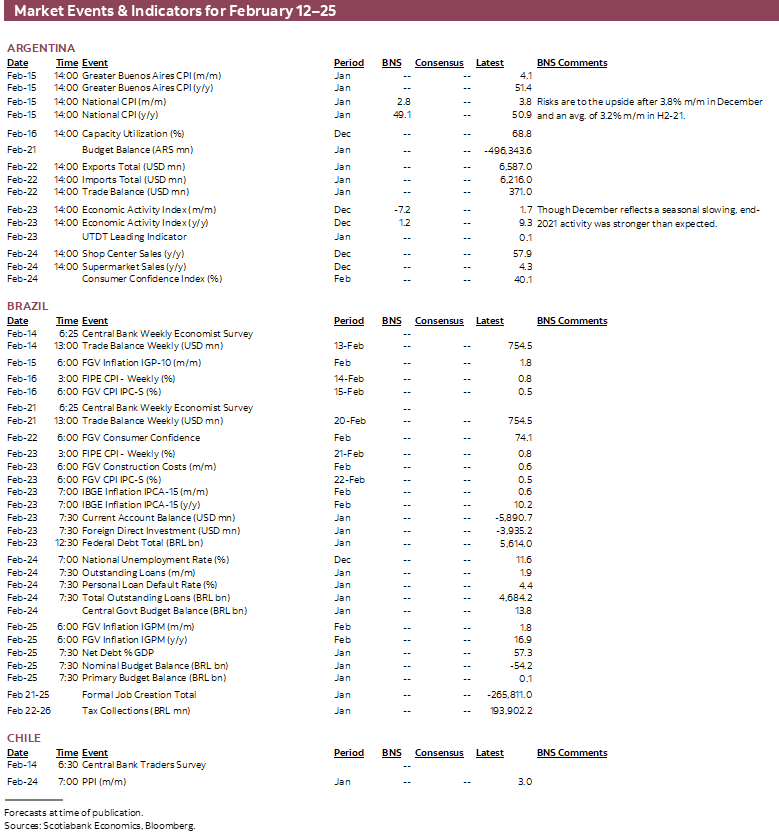

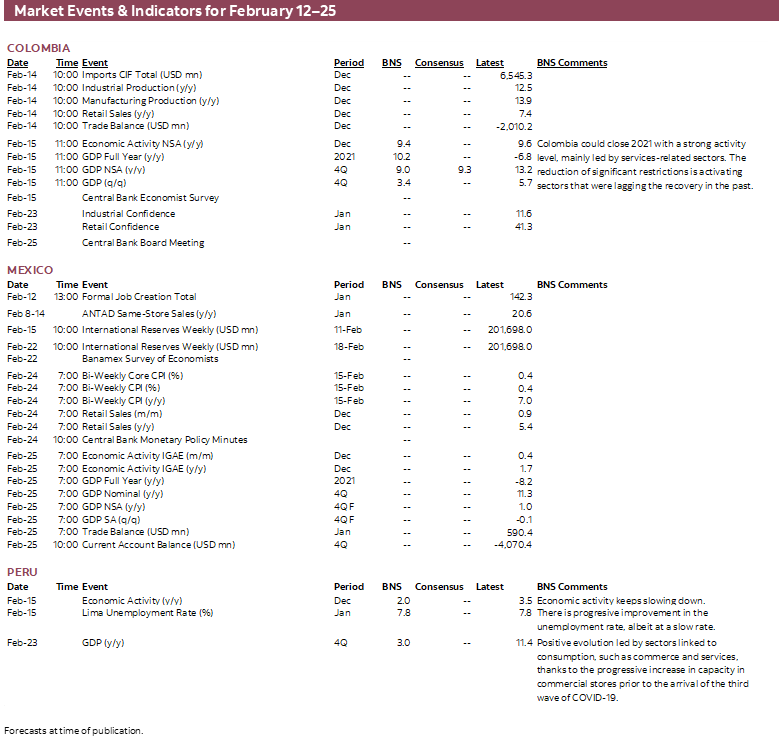

While the Fed’s potential response to sustained US inflation point to heightened risks to Latam growth prospects, the omicron variant poses a more immediate threat. Key COVID-19 monitoring charts (charts 1–12) provide useful guideposts for tracking the latest developments. As has been observed in other countries, cumulative cases (chart 4) and new daily cases (chart 7), and test positivity rates have all shot higher. However, to this point at least, higher caseloads have not been reflected in the data on cumulative mortality rates (chart 6). This effect is explained, in part, by the lag between infection and subsequent severe illness, and in part by the protection provided by vaccination. In this regard, progress has been made in getting populations inoculated with at least one dose (chart 10), with Chile leading the way both in the region and on a global basis (chart 11).

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.