- Colombia: BanRep minutes underscore central bank concerns regarding inflation expectations

- Mexico: Expectations survey revises growth down and inflation up, while remittances hit record high

- Peru: Activity slows but strong growth assured, while inflation takes a breather; politics takes centre stage

COLOMBIA: BANREP MINUTES UNDERSCORE CENTRAL BANK CONCERNS REGARDING INFLATION EXPECTATIONS

On Tuesday, February 1, the central bank released the minutes of its most recent monetary policy meeting held on Friday, January 28, in which five members of the Board voted to increase the benchmark rate by 100 bps to 4.0%, while two members voted for a 75 bps hike. Key highlights of the minutes include:

- The Board agreed that the main challenge for monetary policy is to anchor inflation expectations and avoid stronger indexation effects in a context in which the output gap is closing and a large external trade deficit.

- Board members agreed that less monetary stimulus is required since the output gap is narrowing while inflation expectations continue to increase. However, as in the previous meeting, the discussion was about the pace of the hiking cycle.

- The five members who voted for a 100 bps hike expressed concerns about the possible de-anchoring of inflation expectations and the negative effect that would have on price formation. In addition, the widening current account deficit shows that supply is not keeping pace with the increase in domestic demand, they argued, and that financing of this deficit could become more challenging owing to the tightening of global monetary conditions.

- The two members voting for a 75 bps hike argued that current inflation shocks are transitory and that there is still high uncertainty regarding the economic recovery. They noted that employment has struggled to rebound to pre-pandemic levels and that the SMEs sector, which is the sector most sensitive to rate hikes, remains weak.

Most important, the minutes revealed a strong consensus among the Board that the economy needs less monetary stimulus. That said, there are varying levels of concern about economic growth and inflation expectations.

We expect BanRep to make a new 100 bps rate hike in March’s meeting. And we affirm the upside revision to our expectation of the terminal rate from 5% to 5.75%, which considering the higher inflation, would represent a neutral real rate.

—Sergio Olarte & Jackeline Piraján

MEXICO: EXPECTATIONS SURVEY REVISES GROWTH DOWN AND INFLATION UP, WHILE REMITTANCES HIT RECORD HIGH

I. Banxico’s survey of expectations revises growth downwards and inflation upwards

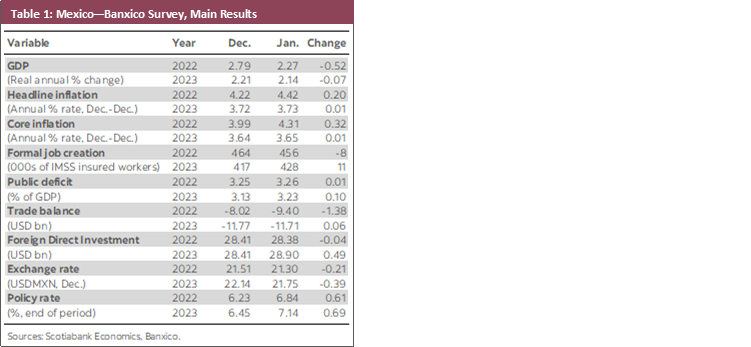

Banxico’s survey of expectations again revised upward inflation expectations, exceeding the central bank’s inflation goal, while lowering growth forecasts for 2022 and 2023 (table 1). Inflation expectations for 2022 rose to 4.42% y/y from 4.22% y/y in the previous estimate. While we expect the effects of tighter monetary policy to become more visible in the second quarter of 2022, we still expect inflation to close the year above target (Scotiabank 4.50% y/y). For 2023, the average response increased marginally, from 3.72% y/y to 3.73% y/y, although responses were in a lower range of variability. Core inflation also increased for 2022 to 4.31% y/y (3.99% y/y previously) and was effectively unchanged for 2023 (3.65% y/y versus 3.64% y/y previously).

The median interest rate expectation for 2022 increased from 6.25% to 6.75%, with the consensus expecting a 50 bps hike between the two decisions in the first quarter. For 2023, the median rose from 6.50% to 7.0%.

The expectation for 2022 growth dropped from 2.79% y/y to 2.27% y/y, reflecting less robust private consumption in the short term, as well as stagnant investment, which still shows no signs of recovery. In this regard, the majority of respondents, 53%, consider that it is a bad time to make investments and a higher proportion of respondents (81% versus 75% of the previous month) believe that the business climate for private sector productive activities will remain the same or worsen in the next six months. According to the report, respondents believe that the main factors that could hinder economic growth in the next six months are related to governance issues (42%) and domestic economic conditions (22%). In particular, the main factors are domestic political uncertainty (15%), inflationary pressures (13%), insecurity problems (12%) and weakness in the domestic market (8%).

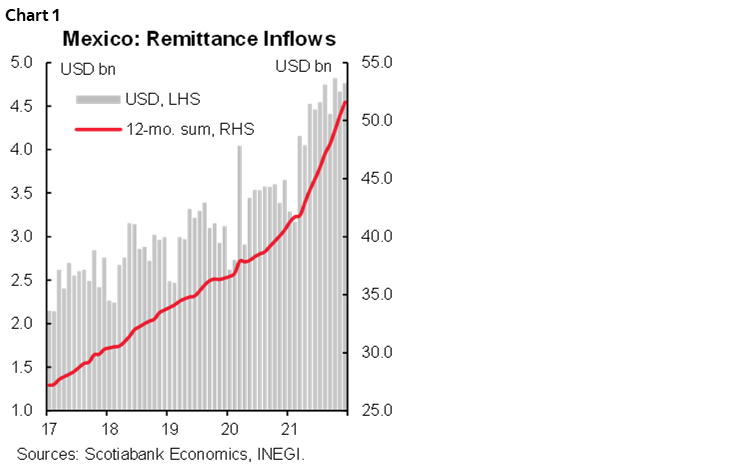

II. Remittances reach an all-time high of USD 51.594 bn

Remittances in December amounted to USD 4.76 bn, 30.4% more than in December 2020 (chart 1). On an annual basis, remittances grew 27.1% and reached an all-time high of USD 51.594 bn, which represents around 4% of GDP. The number of transactions in 2021 rose 14.3% y/y, while the average amount per transaction increased 11.1% y/y. These results can be explained by several factors: the increased difficulties for Mexican nationals abroad to visit Mexico may have caused a substitution effect; the perceived deterioration in the domestic economy; and, fiscal stimulus during most of 2020 and 2021 and the recovery of the US labour market. Going forward, we expect a slowdown in the US economy, which could lead to a moderation in remittances growth. However, remittances will continue to support private consumption.

—Luisa Valle & Miguel Saldaña

PERU: ACTIVITY SLOWS BUT STRONG GROWTH ASSURED, WHILE INFLATION TAKES A BREATHER; POLITICS TAKES CENTRE STAGE

I. GDP continued to slow in December

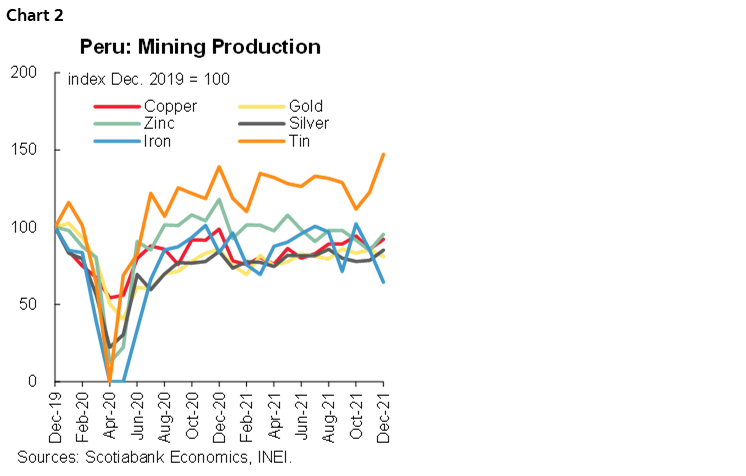

In December, economic activity continued the slowdown shown throughout the fourth quarter of 2021, in line with Scotiabank’s forecast. Based on advance indicators released by the INEI, GDP would have posted a growth of around 2% y/y in December, with an accumulated expansion in 2021 consistent with our forecast of 13.3%. The data show a drop in primary sectors in December, with the mining sector (-7.1%) affected by the drop in the production of iron (chart 2). The fishing sector (-12.6%) was affected by the lower anchovy catch attributable to the reduction of the quota for the second fishing season. Construction activity dropped for the third consecutive month, in line with the projected decline in private investment as a result of the deterioration of business expectations stemming from the high political noise. Economic activity in the commerce and services sectors increased but at a lower rate than that posted in November due to a base effect, since December 2020 was the first post-pandemic month in which GDP grew.

—Pablo Nano

II. Inflation takes a breather in January; INEI updates CPI basket and sets new base year

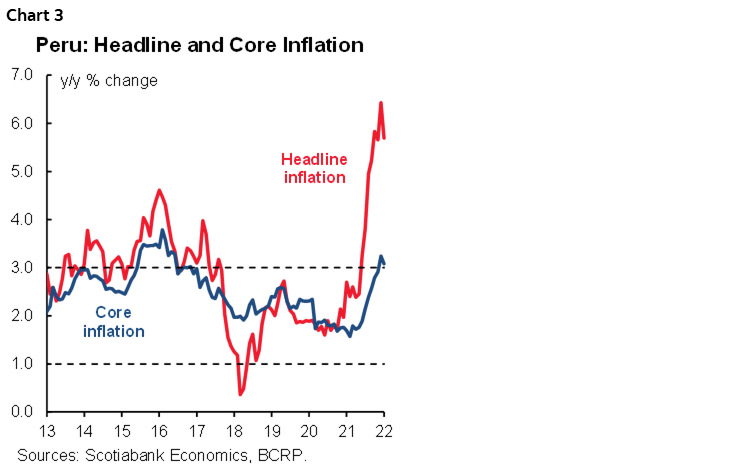

Peru’s inflation was 0.04% m/m in January, the lowest increase in prices since April 2021 (-0.10%) and the lowest rate for the month of January since 2012 (-0.10%). Inflation took a breather on a year-over-year basis, coming in at 5.7%, down from 6.4% in December. This outcome is below the Bloomberg consensus (5.99%), though close to Scotiabank’s forecast (5.8%). This marks the eighth consecutive month that inflation exceeded the upper limit of the central bank’s target range (between 1% and 3%) and with price pressures still far from showing signs of converging towards the target will put pressure on the central bank to continue raising its reference rate in February (chart 3).

The statistical agency (INEI) announced a new base period (December 2021) and updated CPI basket for inflation starting in 2021. There had been no change in the base year since 2009 (12 years—well above the five years suggested by international recommendations). This update has taken three years of review and advice from the IMF and includes an increase in products that make up the basket (+54, to 586 products) as well as greater coverage of points of sale from which price data is collected. Table 2 shows the main changes in the weights between 2009 and 2021. The food and non-alcoholic beverages group, with the greatest weight in the basket, lost 2.16 ppts, which is offset by the increase in the weight in restaurants and hotels and housing, water, electricity and gas. Changes to the rest of the weights are minor.

For February, we expect inflation to once again exceed 6% y/y, driven by a low base effect in February 2021 (-0.13%) and by the increase in local fuel prices. We have updated our inflation forecast from 4.5% to 4.2% for 2022 to reflect our expected appreciation of the PEN, without altering the message that we see inflation above the target range this year as well. The new weighting of the CPI basket gives our forecast a slight upward bias. Our forecast differs from the BCRP, which projects that inflation will return to the target range (2.9%).

Core inflation fell from 3.2% y/y in December to 3.1% y/y in January, above the upper limit of the target range (3%) for the second consecutive month. Wholesale inflation, linked to production costs, fell from 13.6% in December to 12.1% in January, though remains high. Some cost pressures, such as port freight and the FX, have been easing, but other costs, such as the prices of soft-commodities and the price of oil, continue to rise. The PEN depreciation moderated from 10% y/y in December to 5.7% in January, reflecting a shift in momentum after two years of depreciation.

Over the past six months, the central bank raised its benchmark rate by 275 basis points to 3.00% and increased reserve requirements three times, showing by early 2022 a firmer stance on controlling inflation. We believe that further increases in the policy rate will be necessary for inflation expectations (3.7% over 12 months according to the December survey) to return to the target range, so we expect an increase of 50 bps at its meeting on Thursday, February 10.

III. Castillo appoints new Cabinet

President Castillo appointed a new Cabinet chaired by current Congressman Hector Valer, who has been in favour of a Constituent Assembly and is close to the Peru Libre party. The appointment could signal possible friction with Congress, which will have to evaluate whether to grant him a vote of confidence in the coming days.

In the Ministry of Economy, Oscar Graham will replace Pedro Francke. Graham is a former official of the BCRP and the MoF, serving as Director of Financial Markets and Private Pensions, which ensures responsible economic management, and we believe his appointment should be a positive signal for the markets. Other important appointments are Alessandra Herrera in the Ministry of Energy and Mines, who had served as advisor to that ministry, and Hernando Cevallos in Health, who continues in the position.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.