- Mexico: Banxico delivers a rate hike

- Peru: BCRP raises rates; new Cabinet sends a message; industrial production up

MEXICO: BANXICO DELIVERS A RATE HIKE

As was expected by both markets (the TIIE curve had the move priced-in) and most economists (19 of 22 in Bloomberg’s latest survey), Banxico delivered a 50 bps hike in its February 10 meeting. The decision was as anticipated as a 50 bps hike can be and led to an almost non-existent reaction by MXN. The peso closed down -0.4% against the greenback, but the depreciation was largely in sync with other moves in global currency markets. Interestingly, there was virtually no discussion of domestic growth in the statement, despite two consecutive q/q contractions in Q3-2021 and Q4-2021. We take this as a signal that the new governor wanted to send the message that Banxico remains a single mandate inflation-targeting central bank. The statement mentioned the contraction in activity, and that slack remains in the economy, but devoted only two sentences of the entire statement to output.

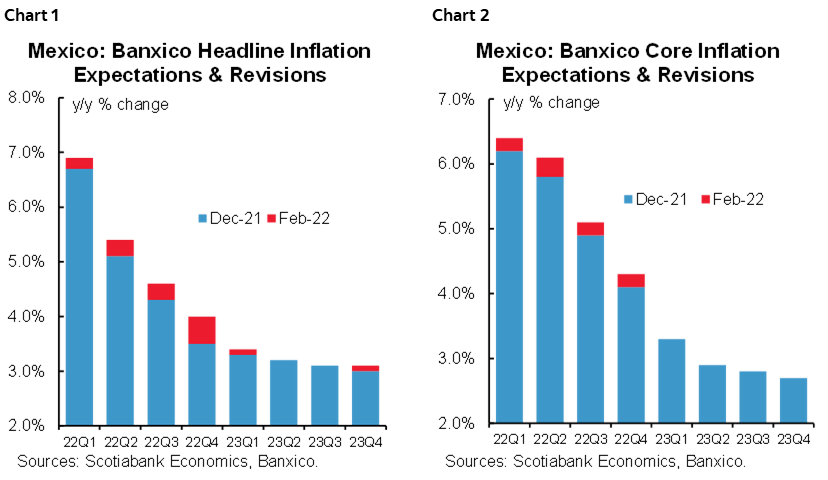

On the domestic price front, the statement highlighted stronger-than-anticipated inflation, with headline printing at 7.01% y/y for the first half of February (chart 1), while core inflation continues to gain momentum, even in services, where slack remains greater (chart 2). The Board also noted that the most recent revisions to private sector inflation expectations remain biased higher, while it also sees the balance of inflation risks tilted to the upside. In our view, the most important part of the statement is the revision to Banxico’s inflation forecast, which acknowledges that inflation is likely to prove stickier than previously anticipated, with both core and headline inflation forecasts seeing upward changes.

A strong majority supported the 50 bps hike. The vote was 4:1, with only Esquivel voting for an increase of 25 bps. However, it is difficult to read Governor Rodriguez and Deputy Governor Borja, as they have been very quiet with respect to their views. In particular, we are not yet sure what factors would lead them to support additional 50 bps moves or support smaller hikes. Overall, we think the statement and the decision sent an almost perfectly balanced message ahead of a highly important FOMC meeting that will not just result in a US rates lift-off, but could lead to a 50 bps increase, which markets and Fed watcher hold out as a possibility given US CPI rising at a 7% pace.

—Eduardo Suárez

PERU: BCRP RAISES RATES; NEW CABINET SENDS A MESSAGE; INDUSTRIAL PRODUCTION UP

I. BCRP hikes rate to 3.50% as market expected

The Board of Peru’s central bank (BCRP) raised its key interest rate by 50 bps to 3.50% on Thursday, February 10, in line with the market consensus (Bloomberg), the interest rate swap market (4.2% with a term of six months), and our own forecast. The decision is consistent with the more aggressive stance the BCRP adopted in January, and continues the normalization of monetary policy that began in August 2021.

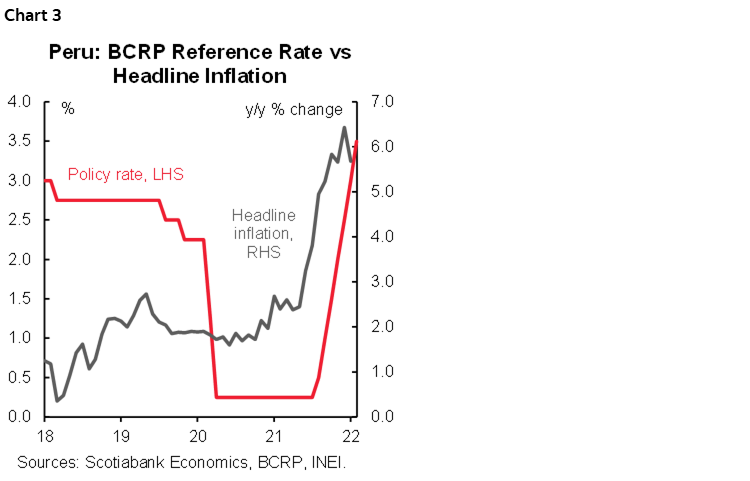

The rate hike comes in the wake of rising inflation. After ending 2021 at 6.4%, inflation took a breather in January at 5.7% y/y (chart 3), due in part to a high comparison base. However, inflation expectations continued to rise (3.7%) and remain above the target range for the seventh consecutive month. These developments put pressure on the BCRP to raise its reference interest rate more frequently, in line with the hawkish tone of its statement. And given the change in BCRP’s forward guidance, our policy rate forecast is 4.50% for 2022 as indicated in our Latam Weekly (January 21, 2022).

Peru’s monetary policy interest rate remains one of the lowest in the region. The real interest rate of monetary policy rose for the fifth consecutive month, but remains in negative territory, at -0.2% after the decision, still in an expansionary orientation.

The BCRP statement retains the expectation that inflation will return to the target range during Q4-2022, as transitory factors on inflation are reversed, such as the FX rate and international fuel and soft-commodities prices. At the same time, the BCRP signalled concerns regarding the transitory nature of these effects, given that a greater persistence in the rise of international energy and food prices has been observed. Our view is less optimistic as we forecast inflation above the target range for this year (4.2%), even after incorporating a 5% PEN appreciation over the year.

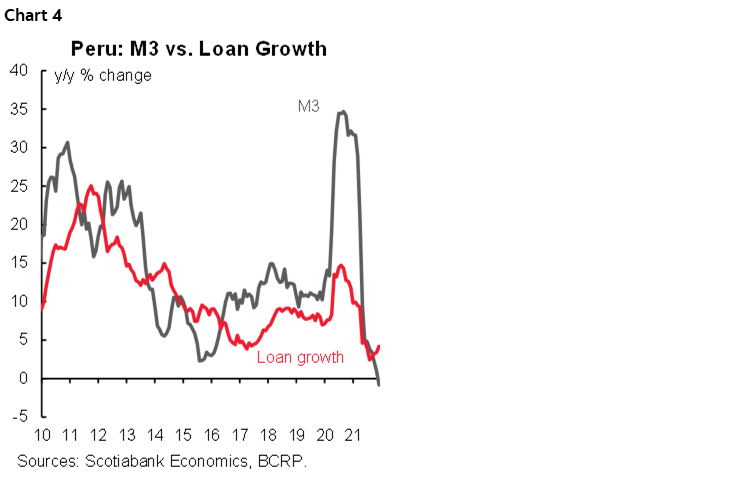

Likewise, the BCRP’s Board also indicated that it will remain attentive to new information regarding inflation expectations and the evolution of economic activity “to consider, if necessary, changes in the monetary policy position that guarantee a return to the target range”. The expansion of the quantity of money (M3) dropped -0.9% y/y in December 2021, falling into negative territory for the first time in 21 years (June 2001), reflecting tighter monetary control. However, loan growth continued to expand at the end of 2021, rising 4.6% y/y (chart 4).

The BCRP also pointed out that expectations with respect to the economic outlook remained were biased downward in January and that economic activity remains below its potential level. The statement expressed concern about the uncertainty associated with the pace of reversal of monetary stimulus in advanced economies.

The BCRP continued to send messages to the FX market, showing itself to be complacent with the PEN appreciation trend (6.3% YTD), as it contributes to reducing inflationary pressures. Between BCRP’s Board meetings, it has made discrete sales in the spot market averaging of USD 32 mn and through derivative instruments (USD 929 mn).

II. New Cabinet’s first measures

In its first announcement, the new Cabinet signalled its intent to pursue market-oriented policies, support free enterprise, and promote a strong government that can prevent monopolies and other concentrations of economic power. This is a good start. The Finance Minister Oscar Graham also announced that the government will reject a bill approved by congress to return around PEN 42 bn (USD 11 bn) or 20% of the public budget to workers who contributed to a defunct housing fund. That bill would generate imbalances in fiscal accounts, so the government will replace it with a new bill by amount estimated at PEN 6.6 bn (USD 1.8 bn), or 3% of the public budget. The Deputy Finance Minister, Gustavo Guerra, linked to the moderate left-wing and appointed by Pedro Francke, resigned. This would allow Minister Graham to reinforce his team with a more technical profile.

III. Industrial output figures

On the economic side, industrial production grew 17.9% in 2021 compared to 2020 and 3% compared to 2019, exceeding the pre-pandemic level, according to official data. Non-primary manufacturing (+24.2%) benefited from the recovery in industrial exports as well as domestic demand, while primary manufacturing (+2.0%) was mainly driven by higher fishmeal production. The official GDP figures for 2021 will be released next Tuesday, February 15.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.