FORECAST UPDATES

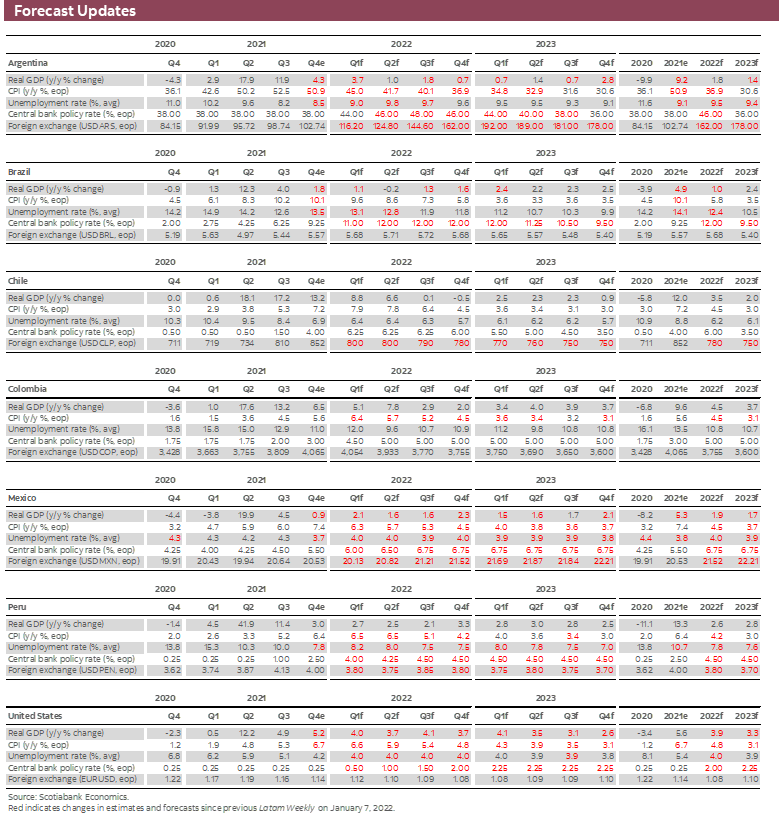

- Scotiabank teams across the Latam region have revised their forecasts. For the most part, where revisions have been made, growth has been marked down. Inflation has generally been revised up. Peru is an exception, given the appreciation now projected, which relieves inflation pressures coming from pass-through effects. See the full range of revisions in the forecast tables.

ECONOMIC OVERVIEW

- As noted in the previous edition of the Latam Weekly, the region faces old challenges in a new year—the pandemic continues to cast uncertainty over short-term economic prospects, while the challenge of raising long-term potential output remains.

- The latest wave of COVID-19 fueled by the omicron variant could be short-lived and its economic impacts limited. Nevertheless, it is possible that more stringent restrictions and increases in worker absences will result in further disruptions to global supply chains that radiate around the globe.

- Such effects could have negative effects on economic activity and stoke price pressures, increasing the likelihood of more aggressive monetary policy responses. That too would have repercussions as global portfolios are rebalanced.

- Measures to bring workers from low productivity activities into the formal sector could provide the sustained growth needed to address the region’s other challenges.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

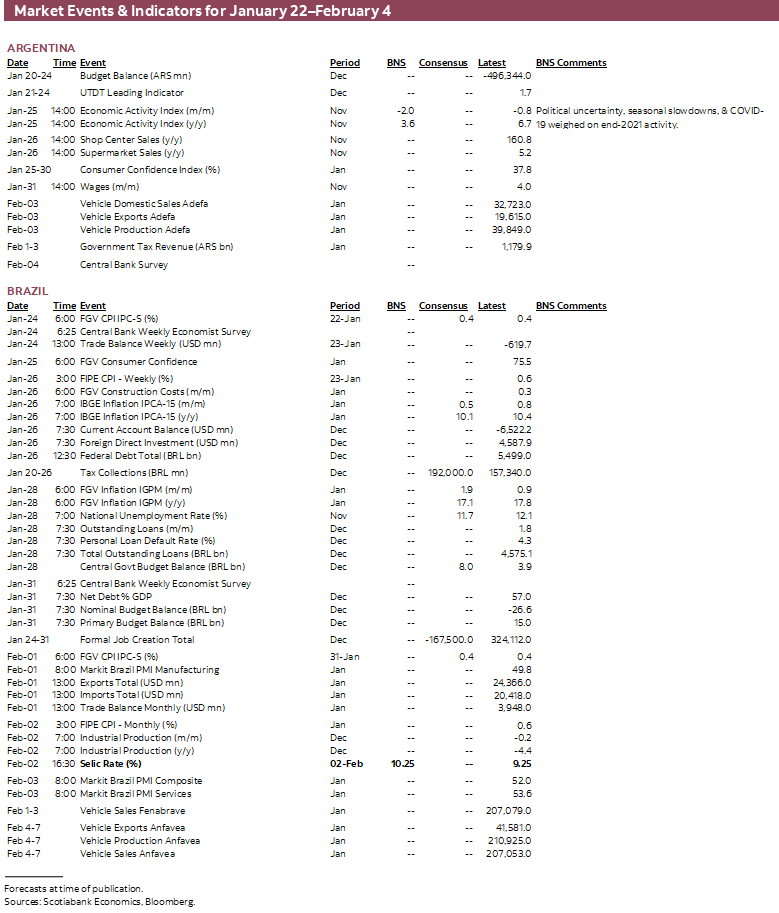

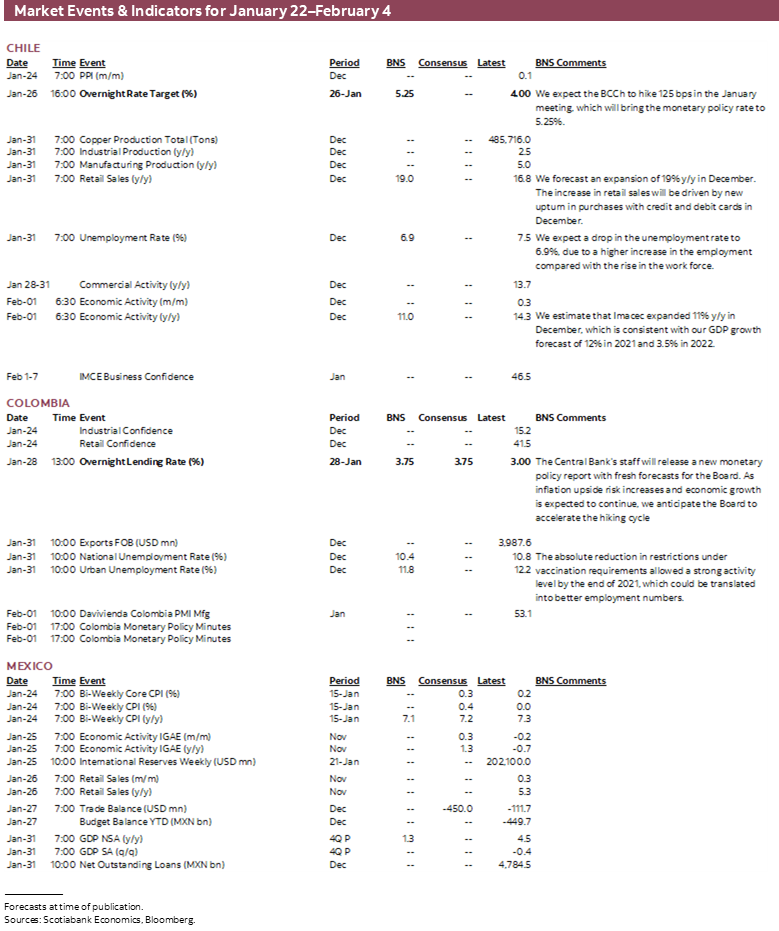

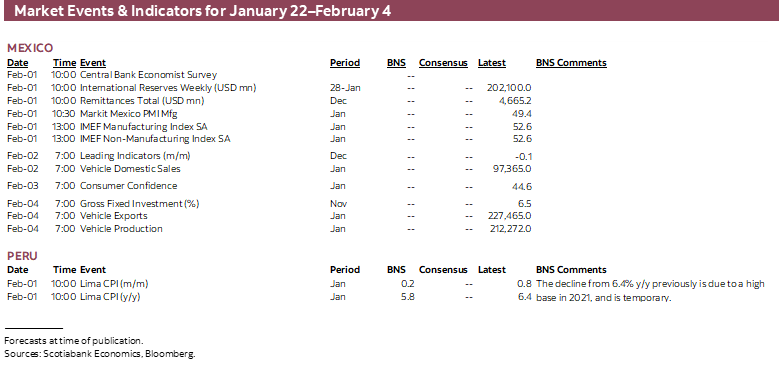

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period January 22–February 4 across the Pacific Alliance countries, plus their regional neighbours Argentina and Brazil.

Economic Overview: No Economy is an Island

James Haley, Special Advisor

416.607.0058

Scotiabank Economics

jim.haley@scotiabank.com

- Scotiabank teams across the Latam region have revised their forecasts in response to new data on inflation, economic activity and the uncertainty resulting from the rapid transmission of the omicron variant and vertiginous increase in new caseloads.

- Increased caseloads could impinge on economic activity and exacerbate price pressures. Both effects would reverberate through the global economy, as central banks respond with more aggressive tightening and disruptions to global supply chains create production bottlenecks.

- These effects reinforce the integrated nature of the international economy in the age of globalization and demonstrate that “no economy is an island.”

- Raising potential output growth—an old challenge in the region—will therefore be critical going forward. And bringing workers from low productivity informal jobs to high productivity jobs in the formal sector may be the key. Policies to facilitate this transition could also help to address underlying social challenges in the region.

NO ECONOMY IS AN ISLAND

The previous edition of the Latam Weekly addressed the challenges the omicron variant poses to the Latam countries and the “old” challenge of raising potential growth in the region. The focus of this week’s Latam Weekly remains on these issues.

Against the background of these challenges, Scotiabank’s teams in the region have revised their forecasts. As discussed more fully below, the impact of recent developments on the pandemic front is unclear. But while the size of probable effects is in doubt, the sign of these effects is not. In broad terms, where revisions have been made, growth has generally been revised down modestly. Inflation has been marked up slightly over the near-term horizon, largely reflecting recent inflation readings. In contrast, Peru is an exception (see the discussion in the country notes below), with our team in Lima now projecting an appreciation of the currency this year, driven by strong fundamentals and a reduction in political uncertainty, which relieves price pressures through pass-through effects.

The short-term outlook is clouded at the current conjuncture, given that the economic impacts of the latest wave of the COVID-19 pandemic are unknown. Despite the heightened transmissibility of the omicron variant, there is reason for cautious optimism. Though it spreads far more quickly than previous strains, based on preliminary and incomplete data, it would also appear to be less virulent than previous outbreaks, particularly the delta variant. Moreover, while the omicron “wave” crests suddenly, it also appears to collapse nearly as quicky. At the same time, economies around the globe have shown resilience to public health protocols as workers, firms, and consumers have “learned to live” with social distancing and other restrictions. Hopefully, these behavioural changes will mitigate the adverse effects on economic activity.

But hope is not a plan, and it would be imprudent not to expect some fallout from the increase in caseloads. In Mexico, for example, there are already early indications that tourist bookings for the peak winter period have fallen as the omicron variant has spread through key tourism markets in the US, Canada, and Europe. With luck, the downturn in tourism traffic will prove temporary and bookings will bounce back once caseloads fall (see the discussion in the Country Notes section below). With signs of new cases stabilizing in areas first affected by the omicron variant, this scenario may in fact come to fruition. In contrast with goods markets, however, the demand for services, such as tourism, can be ephemeral—a winter holiday becomes less attractive to Canadian and other snowbirds once the warmth of the spring sun begins melting the snow. This “best before date” quality of services means that some share of tourism revenues may be irretrievably lost.

Elsewhere in the Latam region, caseloads are soaring, replicating the pattern observed in other countries. And while Chile leads the world in terms of vaccinations administered, progress is uneven across the region, potentially putting populations with lower vaccination rates at risk. In this respect, even with lower mortality and morbidity rates associated with the omicron variant, governments in the region could respond with tighter mobility and isolation requirements to limit the spread of the virus. Those restrictions could lead to lower output. Public health authorities in Chile have already tightened restrictions; officials in other countries are likely to follow.

Such effects are not limited to one country or even one region. There are growing concerns, for instance, that draconian measures introduced by Chinese health authorities under their “zero COVID-19” policy could lead to further disruptions in global supply chains. Traffic congestion resulting from a minor accident may serve as a useful metaphor for understanding the dynamics in such circumstances. Protracted delays can remain long after the vehicles involved in the crash have been cleared away as the initial congestion created by the accident leads to bottlenecks far away. In the same vein, even brief disruptions to critical inputs can have far-reaching and long-lasting effects that ripple through production processes around the globe.

If realized, this scenario could pose a difficult challenge for countries already grappling with protracted price pressures. It also demonstrates that in a highly integrated global economy, no economy is wholly independent. To paraphrase the English poet John Donne, “no economy is an island, entire of itself.” “A supply-side disruption in any one economy affects all, because all are connected through global supply chains.”

The risk that supply-side problems, which according to some reports were slowly being resolved prior to the latest COVID-19 setback, may be exacerbated by the rapid and extensive spread of the omicron variant is, in a word, troubling. Whatever the consequences on the short-term outlook, it is clear the emergence of yet another strain of the virus has once again generated pervasive uncertainty.

By itself, this development could have a material impact on growth prospects. This is because uncertainty acts as a kind of tax on long-term economic decision making, leading firms and consumers to exercise the “option value of waiting.” Firms may curtail investing and households defer purchases until the uncertainty is dispelled. The result of these responses is slower growth. Scotiabank’s team in Bogota note below (see country notes), for example, that increased uncertainty generated by higher inflation and the forthcoming elections could weigh on 2022 growth.

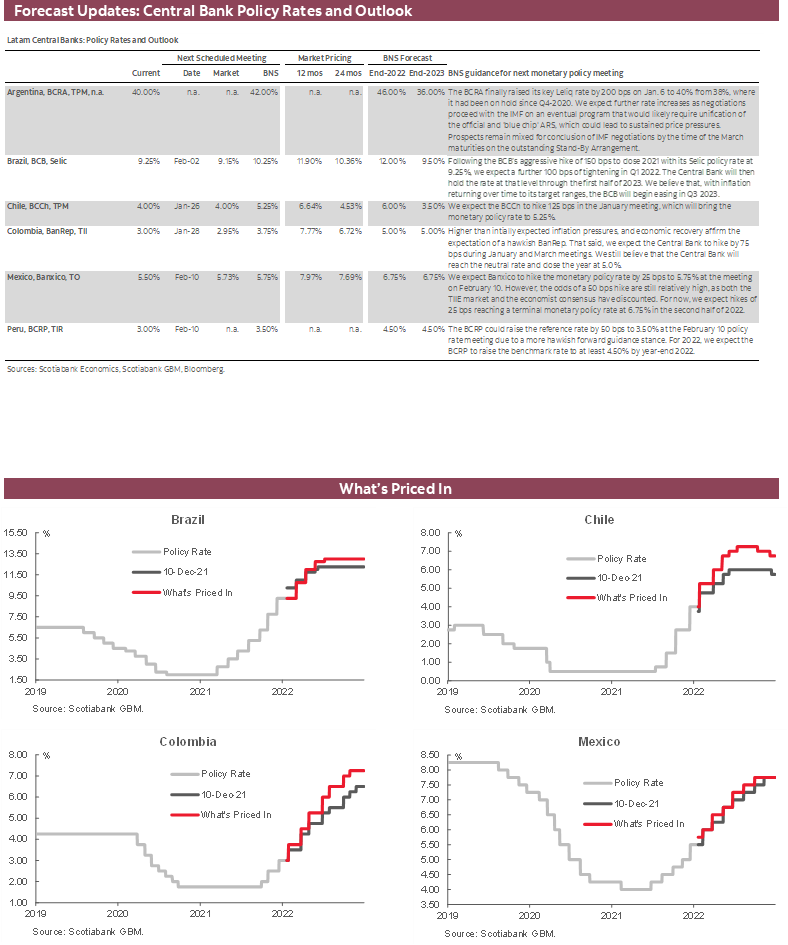

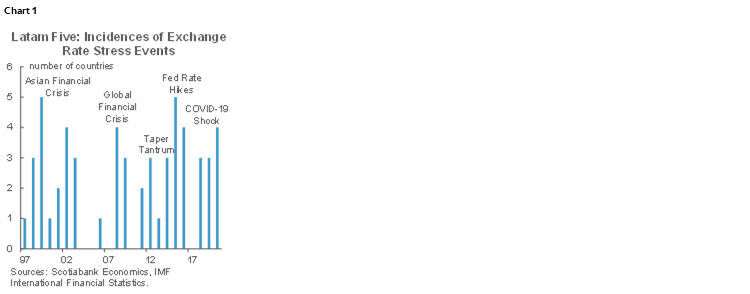

Moreover, this uncertainty comes on top of an increased likelihood that Fed tightening will be more aggressive in the coming months than was thought likely just a few weeks ago. The prospective “one-two punch” of higher policy higher rates combined with a reduction in the Fed’s balance sheet, consistent with the unwinding of quantitative easing, has focused attention on global portfolio allocations. And while Ross Perot’s “giant sucking sound”, albeit with respect to capital and not jobs, is not yet audible, across the Latam region policy makers should be bracing for a possible reversal of capital flows. An accelerated Fed tightening cycle could weigh on regional currencies which, given potential pass-through effects, would further fuel inflationary pressures. This week’s Chart of the Week (chart 1) shows the impact of Fed tightening and other shocks on regional currencies over a longer time horizon.

Past episodes of Fed tightening cycles suggest that rates hikes have fewer negative spillover effects on Latam countries when aggregate demand in the US is strong; the spillover effects can be much more damaging when the Fed tightens in response to price pressures coming from, say, supply-side shocks. In this respect, should the latest COVID-19 wave have serious deleterious effects on US demand, the consequences for the Latam region could more serious. Heightened geopolitical tensions that could trigger a reevaluation of risk appetite and further rebalancing of global portfolios would, clearly, increase the risk of capital outflows.

At the same time, prospective Fed tightening, preceded by earlier aggressive rate hikes by Latam central banks, and the unwinding of extraordinary policy supports erected by fiscal authorities in the region and around the globe puts the spotlight on growth prospects in a world without the stimulus measures introduced in the pandemic. With output back to pre-pandemic levels in most Latam countries, and the need to ensure fiscal sustainability, such rebalancing of macro policies is entirely appropriate. That said, even if growth rates over the medium term broadly return to pre-pandemic levels, as Scotiabank’s teams in the region anticipate, the question remains whether that is sufficient to meet the needs of the region.

As noted previously, the old challenge of raising long-run potential growth continues to haunt the region. The problem is that pre-pandemic growth rates do not establish a particularly high bar given the desultory performance of most countries over that time. In the context of the past four decades, for example, pre-pandemic growth pale in comparison to the increase in output achieved in earlier decades.

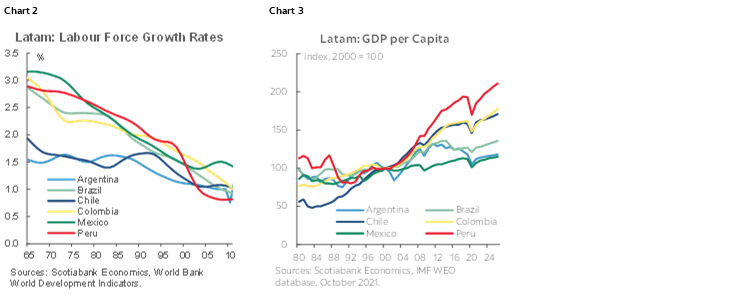

In a long-term growth accounting perspective, however, some reduction in Latam growth rates would be expected given the decline in labour force growth rates (chart 2). This framework decomposes output growth into the growth rates of key inputs, especially capital and labour, and a residual for other intangible (and unmeasured) effects. Thus, as labour force growth slowed from the high rates in the 1960s and 1970s, output growth naturally slowed as well. Increases in productivity—goods and services produced by the average worker—can offset that decline in labour inputs. And for many countries, particularly Pacific Alliance members, economic reforms in the 1990s that liberalized the economy did precisely that, raising GDP per capita (chart 3). Since then, however, progress has slowed.

Going forward, therefore, to sustain growth as pandemic stimulus winds down, Latam countries will have to identify measures to boost potential output. The key to unlocking that old challenge remains elusive. Yet, policies to bring workers from low productivity informal jobs to higher productivity employment is likely part of the answer. Doing so may also address the underlying social issues that animate political dissatisfaction.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—On the Way to Reaching GDP Growth of “at Least” 3.5% in 2022

Jorge Selaive, Head Economist, Chile

+56.2.2619.5435 (Chile)

jorge.selaive@scotiabank.cl

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

Waldo Riveras, Senior Economist

+56.2.2619.5465 (Chile)

waldo.riveras@scotiabank.cl

The daily number of confirmed COVID-19 cases increased sharply in recent days, reaching its highest level since the beginning of the pandemic due to the advance of the new omicron variant. The positivity rate rose to 8.7% in the last week (chart 1). The occupancy of ICU beds is slowly increasing, while the COVID-19-related death rates remain at low levels. Meanwhile, the vaccination campaign reached 92.5% of the eligible population. The rollout of booster (third) doses keeps moving forward—reaching 11.5 million people—and the new booster dose (fourth) is in progress.

Due to the rise in COVID-19 cases driven by the omicron variant, the Ministry of Health toughened mobility restrictions in Santiago’s Metropolitan Region and 45 other municipalities nationwide, starting Wednesday, January 19. The government also reduced the isolation period for people infected with the virus to seven days from 10.

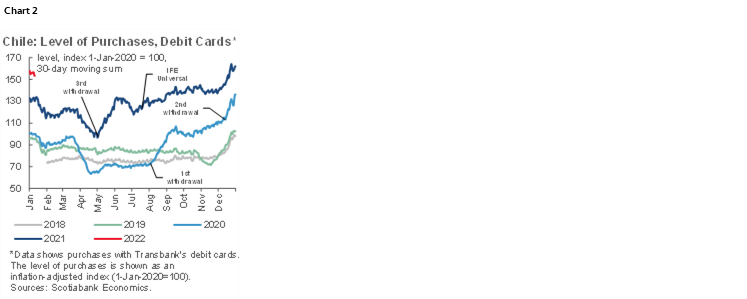

With regard to the economic activity, we forecast a 2022 GDP expansion of 3.5%, well above central bank and market expectations (at 2%). According to our high-frequency indicators of debit card transactions up to the first half of January, the expected deceleration in household consumption has been smooth (chart 2). In addition, savings in chequing and debit accounts remain higher than its historical trend—USD 18 bn above—and should allow a mild deceleration of private consumption. With this, we believe that market expectations for GDP will increase towards the end of Q1-2022—closer to our current forecast of 3.5%—after the release of January’s IMACEC figures (March 1) and supported by a likely upward revision in the GDP growth forecast by the central bank (March 30).

On Tuesday January 18, the Ministry of Finance (MoF) announced its 2022 issuance plan, which anticipates issuing Treasury bonds totaling USD 20 bn in 2022, within the debt limit authorized by the 2022 Budget Law. According to the MoF, local currency issuances are planned in the order of USD 14 bn, and foreign currency issuances are estimated at USD 6 bn. The local currency financing plan considers the issuance of approximately USD 3 bn in short-term notes, with the remaining USD 11 bn in medium- to long-term bonds. Also, the plan considers issuances of peso “social” bonds for a total of USD 4 bn allocated through a book-building process. Finally, the plan considers that USD 2 bn of the total issuances in foreign currency will be transferred to the Economic and Social Stabilization Fund.

In the fortnight ahead, on January 26, the central bank will hold its Monetary Policy Meeting, from which we expect a new hike in the benchmark rate of “at least” 125 bps. However, we do not rule out a more aggressive response by the BCCh, owing to the de-anchoring of longer-term inflation expectations (3.7% in 2y and 3.1% in 3y). For the first half of 2022, we estimate the Monetary Policy Rate would reach 6.0–6.5%.

Colombia—Monetary Policy: Faster But not Higher for Now

Sergio Olarte, Head Economist, Colombia

+57.1.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Economist

+57.1.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

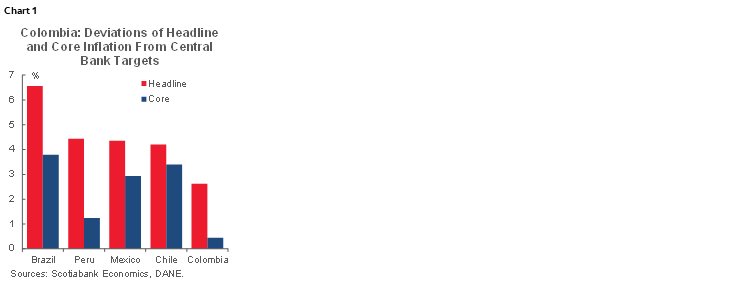

As highlighted in the recent Scotiabank Economics Forecast Tables report, inflation is the main concern globally, with price pressures stronger than previously assessed, triggering a stronger monetary policy response. In Colombia, we think BanRep will speed up its hiking cycle in H1-2022, despite inflation showing a lower deviation from the inflation target as compared to other countries (chart 1). However, we must consider other fundamentals before anticipating a higher terminal rate.

Inflation in 2021 closed at 5.62%, 2.62% above the central bank’s 3% target, with half of this increase attributable to higher foodstuff inflation. High inflation is leading to higher-than-expected indexation effects which, joined by a strong increase in the minimum wage, is transmitting inflation pressures to the core component. Our projections indicate that headline inflation increases in H1-2022 reaching levels around 6.50% before starting to decrease. In fact, we revised our end-2022 inflation forecast to 4.5%, which would imply that Colombia closes the year outside of the inflation target range for the third year in a row; meanwhile, core inflation is expected to increase from the current 3.44% to 4.55%.

On the external side, the trade deficit is pointing to a widening current account deficit, which sits uncomfortably in an environment of tighter financial conditions as the Federal Reserve is expected to act sooner in the hiking cycle.

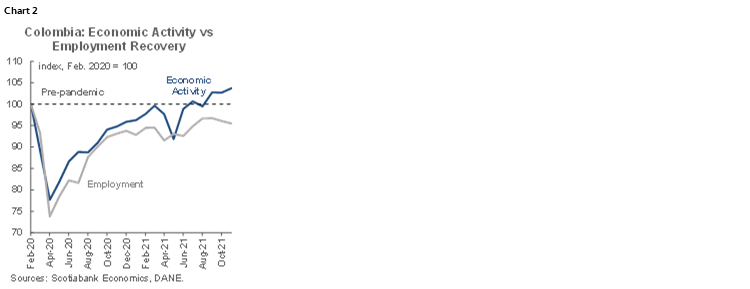

Meanwhile, recent macro indicators show the Colombian economy grew by around 10% in 2021. Looking ahead, we expect economic growth to reach 4.5% in 2022. Yet, according to recent indicators, households are more cautious owing to higher inflation as well as uncertainty regarding the election. These effects could weigh on growth. Similarly, while economic activity has already surpassed pre-COVID-19 levels, employment remains about 5% below pre-pandemic levels (chart 2), which also would diminish prospects for a more robust economic recovery.

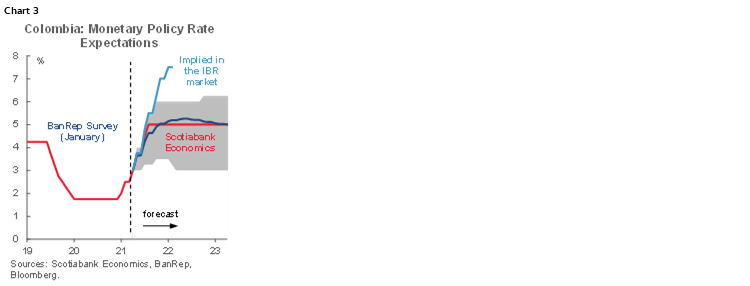

Having said that, despite anticipating BanRep to increase the monetary policy rate more quickly—to 3.75% in January and to 4.25 % in March—we still expect the terminal rate for 2022 at 5%. This projection reflects our expectation that inflation should ease after April and the fact that economic growth is likely to face a challenging H1 due to inflation’s impact on consumption, but also owing to investor uncertainty regarding the elections. However, risks regarding monetary policy are tilted to the upside; new price shocks and the projected reversal of price pressures does not occur, we estimate the hiking cycle to reach 6.25% in a hawkish scenario.

BanRep’s recent economic expectation survey (chart 3) shows that, on average, analysts are not expecting a terminal rate above 5.50%. In fact, rate cuts are expected as early as 2023 on average, which would indicate that current pressures are still perceived as temporary.

To sum up, local and international conditions are triggering a stronger reaction from central banks. In Colombia, however, as inflation is expected to reverse, the anticipated terminal rate is not significantly different from what is considered a neutral rate (nominal 5%, and real at 1.5%—deflated by expected inflation of 4.5%).

Mexico—Updated Forecasts & Outlook for 2022

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

The Mexican economy’s outlook for 2022 has deteriorated over the past couple of months, with both inflation and growth trending in the wrong direction. The end of the year saw a sharper-than-anticipated deceleration in growth leading us to downgrade our annual forecast for 2021. Strikingly, auto output in Mexico looks likely to close the year near 2014 levels, driven in large part by supply chain disruptions, which are expected to improve, though not fully recover, during the second half of 2022. In addition, with the omicron COVID-19 variant wreaking havoc globally, and in some cases leading to renewed travel and mobility restrictions, one of the factors which we anticipated to help the rebound in 2022—tourism—is likely to take a hit, particularly as omicron arrived during the North American winter, an important season for sunny destinations in Mexico. This blow to tourism is hitting an economy that seems likely to have posted two consecutive negative quarters to close out 2021 (measured on a q/q basis). The third quarter of the year is already confirmed to have registered a q/q contraction, while the monthly GDP proxy IGAE posted negative m/m figures in two of the last three months of 2021.

One of the problems caused by the slowdown is the impact it could have on public finances. The government’s 2022 budget is built on a growth assumption of 2.1%, while consensus is edging towards sub-2.0% at the start of the year. In addition, there are two other core assumptions which we believe will be violated:

First, the interest rate assumption, which is anchored on an average 28-day cete rate of 5.0% (while Banxico’s policy rate is kicking off the year at 5.5%, and the TIIE curve is pricing in another 200 bps of hikes for the next 12 months); and

Second, a 1.826 bn barrels of oil production target for Pemex.

Our estimates suggest that missing these assumptions will lead to a miss of the annual fiscal targets of around 0.4–0.6 % of GDP. The past three years saw the fiscal targets be missed, and while the holes were plugged with a combination of asset depletion (using the oil stabilization fund, trusts for natural disaster relief, etc.) and non-recurring revenues, available assets have become scarcer.

On the political front, the election calendar will include gubernatorial elections in the states of Durango, Aguascalientes, Hidalgo, Quintana Roo, Oaxaca, and Tamaulipas. The realignment of political forces after the summer’s elections could once again translate into shifts in the balance of power in Congress (through alliances and the like), affecting the outlook of legislation proposed by the government, which includes the power sector reform, the electoral system, as well as the recently announced telecoms reform.

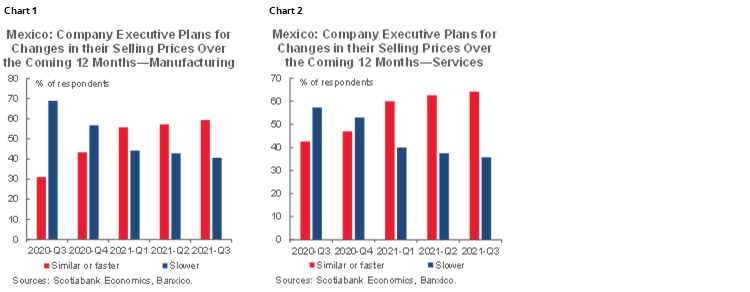

Regarding inflation, although we saw a dip in CPI inflation from 7.37% y/y in November, to 7.36% in December (improving relative to a 7.45% consensus), the composition of inflation was not reassuring. Core inflation continued to accelerate, while services inflation which had served as the main anchoring component also increased. Consistent with the deterioration, observed inflation expectations, measured through both the Banxico and Banamex surveys, also continues its upward trend. Another risk that seems to be emerging on the inflation front is a contamination of the price formation process, as a combination of supply chain disruption, fast-rising producer inflation and the persistence of the inflation shock seem to be leading to rising risk of inflation stickiness. Based on Banxico’s latest survey of company executive plans for prices over the coming 12 months, the majority of companies plan to increase their prices at a similar or faster rate than currently observed (charts 1 and 2).

In this environment of a more complex inflation outlook, and with US monetary policy expectations also showing a more aggressive rate hike outlook, the TIIE curve widened and steepened over the past month. The 2-year node of the curve rose about 20 bps, while the 10yr rate increased 40 bps. For Banxico, the TIIE curve is now pricing in 75 bps for the next 2 meetings, 210 bps of hikes for the next 12 months—which would put the terminal rate at around 7.5%—higher than even our revised terminal rate forecast of 6.75%–7.00%.

Peru—A New Year, a New PEN Market

Guillermo Arbe, Head Economist, Peru

51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

We are markedly changing our view for the USDPEN. Whereas we previously expected the FX rate to depreciate 5.2% in 2022 to end the year at 4.25, we are now forecasting a 4.8% appreciation to 3.80.

The main reasons for the U-turn include the following:

1. Current market dynamics and technical analysis are suggesting a reversal;

2. Strong metal prices and external accounts fundamentals continue to prevail;

3. Fiscal accounts are consistently performing better than expected, with a positive impact on market perceptions;

4. The outflow of domestic short-term capital and assets should be much lower than in 2021;

5. The BCRP is shifting from a highly expansionary monetary policy to a more neutral stance, as we expect it to increase its reference rate by 200 bps to 4.50 in 2022 (chart 1); and,

6. The BCRP currently appears to favour a strong PEN.

There are risks to our view. The main risk is the expectation that the Federal Reserve will be more aggressive in raising its rate. This normally leads to a strengthening of the USD versus emerging markets. The question is whether the reaction in the FX market will be of sufficient magnitude to offset the many factors favouring the PEN. This is not an easy question to answer and poses a real risk to our PEN outlook.

Between its December 6 high of 4.09 and its current (January 19) level of 3.86, the PEN has appreciated 5.6% (chart 2). One of the reasons that the dynamics of the FX market have changed is that the political scenario appears to be more settled. Presidential elections are long past, the profile of the Castillo Government has become clearer—and less radical—over time, the possibility of a Constitutional Assembly has become much less likely, and the fear of a significant break with the past in terms of economic policy and institutions has not materialized. Thus, we do not expect a repeat in 2022 of the uncertainty-fed record out flow of over USD 16 bn in short-term capital that occurred, according to BCRP estimates, in 2021. For something even close to this to recur would require a very dramatic domestic event. What is much more likely is that domestic outflow levels fall back to the more normal highs of the previous decade, which would not be enough to offset the impact of strong metal prices and exports. Having said this, political risk has not disappeared. Political events with the potential to impact the FX market are likely to occur both in Peru and in the region in 2022. This should generate volatility in the FX market, but, hopefully, not enough to generate another bout of safe haven outflows to the USD and offshore assets.

Improved fiscal accounts should also support the PEN. We have reduced our fiscal deficit forecast for 2022 from 3.5% of GDP to 3.0%, based on the strong fiscal trends at the end of 2021, which took the fiscal deficit to 2.6% of GDP for 2021. Furthermore, the Ministry of Finance announced that it intends to rebuild the all-but-depleted Fiscal Stabilization Fund sometime early in 2022, taking it back to its pre-COVID-19 levels of PEN 18 bn. This should also be a positive for market perceptions.

Finally, it would appear that the BCRP favours an appreciation. On January 18 the BCRP sold USD on the FX market, thereby nipping an incipient USD rally in the bud. The BCRP selling USD is not unusual, as it occurred throughout 2021. The novelty was the level at which the BCRP came in to cap the USD upswing—3.87—far below the 4.09 high that the PEN reached in early December. Although it is possible that the intention of the BCRP is for a PEN appreciation to help control inflation, what is more likely is that the BCRP is acting under the belief that the PEN had become misaligned with fundamentals in 2021.

And, of course, all of this is occurring against a backdrop of high metal prices and strong external accounts. We are expecting a record trade surplus of over USD 16 bn. We see upside to this, given that it is based on a conservative scenario of average metal prices this year that are below current levels.

An 11% swing in our USDPEN forecast (from 4.25 to 3.80) will necessarily have some bearing on our inflation expectations. Thus, we are lowering our inflation forecast for 2022 from 4.5% to 4.2% (2023 remains at 3.0%). However, note that the appreciation of the PEN can only go so far in offsetting a global environment of persistently high energy prices, high soft commodity prices (Peru imports most of its wheat, soy and maize—used in staples including bread, edible oils and chicken feed), and high transportation logistics costs.

As a final note, we have maintained our forecast of 2.6% GDP growth for 2022 but have increased our forecast for 2021 from 12.3% to 13.3%. This is simply in recognition of the accumulation of marginally better monthly results in the last half of 2021.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.