ECONOMIC OVERVIEW

- Markets can’t catch a break, as what was supposed to be a quieter global week saw sharp moves in markets amid hawkish central bank speakers and heightened geopolitical risks. Next week will likely be more of the same, but with higher tier G10 data (US PCE, global PMIs) offsetting the calm of the Fed’s pre-meeting communications blackout.

- Latam assets have taken largely their cue from offshore developments, and should continue to do so over coming days. Mexican markets may have more happening at home to differ in their performance, with H1-Apr CPI and February economic activity data on tap. Brazil also publishes prices data, as the BCB hesitates in its cutting cycle. Chile, Colombia, and Peru schedules are practically empty.

- In today’s Latam Weekly our teams in Mexico and Peru outline their outlook for their respective central banks; our economists in Lima now see one less 25bps BCRP cut this year. Our economists in Colombia discuss recent COP price action, and Pension Reform developments and what to watch.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Colombia, Mexico and Peru.

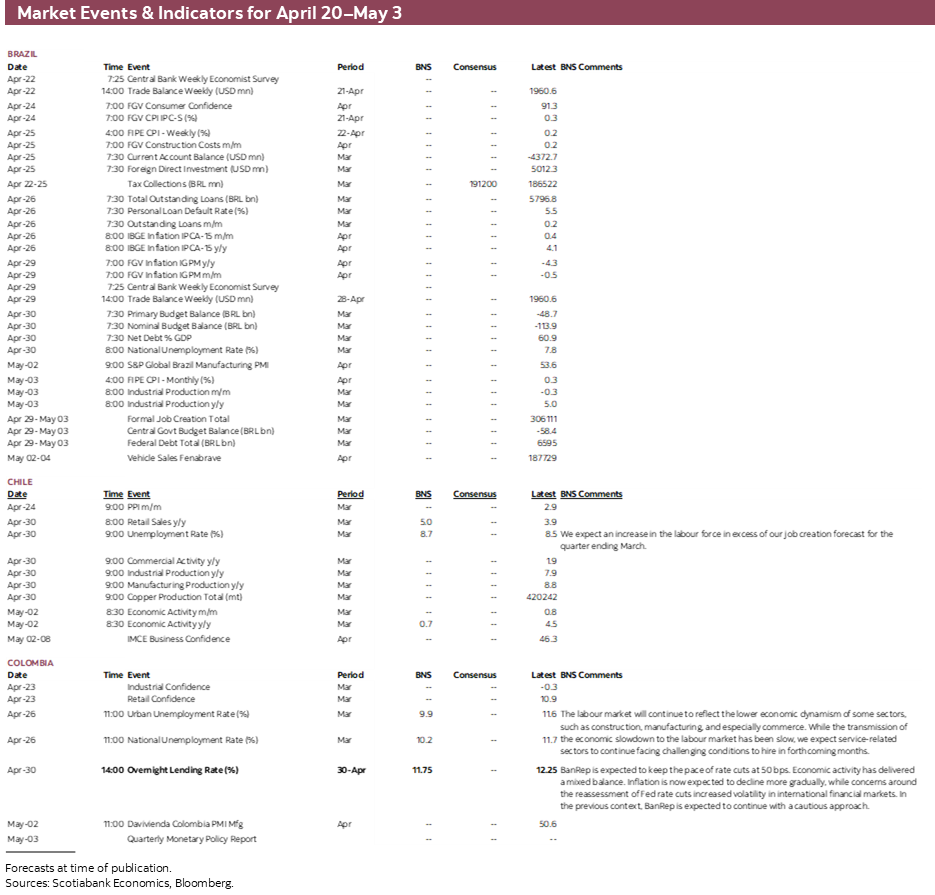

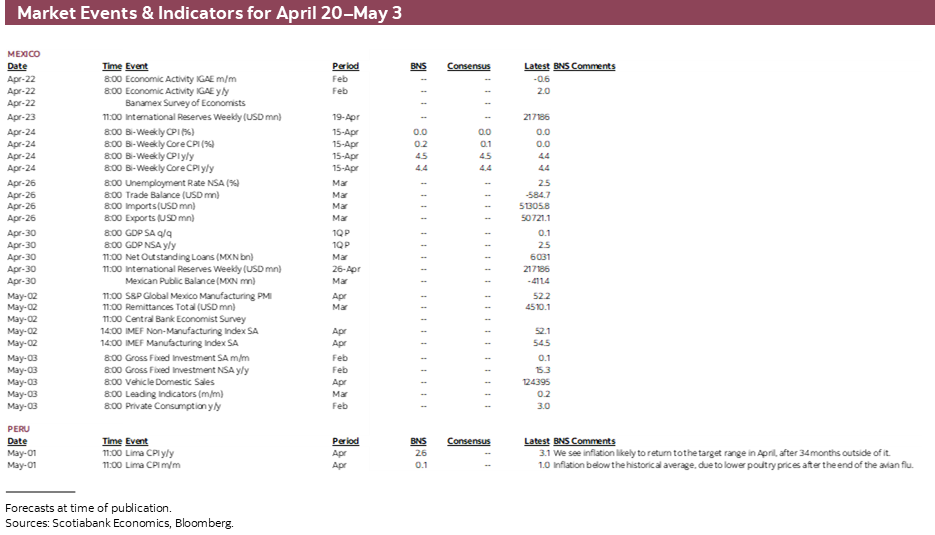

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period April 20–May 3 across the Pacific Alliance countries and Brazil.

Chart of the Week

ECONOMIC OVERVIEW: MEXICO CPI/IGAE, BANXICO AND BCRP VIEWS, COLOMBIA FX AND REFORM ANALYSIS

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- Markets can’t catch a break, as what was supposed to be a quieter global week saw sharp moves in markets amid hawkish central bank speakers and heightened geopolitical risks. Next week will likely be more of the same, but with higher tier G10 data (US PCE, global PMIs) offsetting the calm of the Fed’s pre-meeting communications blackout.

- Latam assets have taken largely their cue from offshore developments, and should continue to do so over coming days. Mexican markets may have more happening at home to differ in their performance, with H1-Apr CPI and February economic activity data on tap. Brazil also publishes prices data, as the BCB hesitates in its cutting cycle. Chile, Colombia, and Peru schedules are practically empty.

- In today’s Latam Weekly our teams in Mexico and Peru outline their outlook for their respective central banks; our economists in Lima now see one less 25bps BCRP cut this year. Our economists in Colombia discuss recent COP price action, and Pension Reform developments and what to watch.

An eventful couple of weeks for global markets, full of geopolitical risk, central bank hawkishness, and data surprises in both directions (e.g. US vs Canada CPI) have seen sharp moves across all assets (and we thought it would be calm). Parallel trading spanning various regional markets has made it difficult to extract the read of local traders to domestic developments, but recent trends in inflation and risks around the Fed’s easing cycle generally point to Latam central bankers taking their foot off the cutting gas.

Before getting into next week’s Latam slate, it’s important to highlight the offshore data and developments that may again dominate regional trading sentiment. The release of global PMIs for April on Tuesday, US Q1 GDP data on Thursday, and the key US PCE inflation release and the BoJ’s (let’s hope uneventful) decision on Friday await; Russia and Turkey also decide on monetary policy. Earnings releases from corporate giants from Microsoft to Exxon Mobil are on tap. Of course, unpredictable military developments in the Middle East and Eastern Europe may see sharp moves in markets.

Mexico’s calendar is the busiest of all in the region next week, with data that will influence policy expectations but that will be insufficient to drive Banxico into choosing to cut rates at its May meeting. The week begins with economic activity data for February and the Citibanamex survey, followed by H1-Apr CPI midweek, and then closing on Friday with unemployment rate and international trade data.

Mexico’s economy surprisingly contracted at the start of the year, printing a 0.6% m/m decline in the January IGAE release. This marked the fourth consecutive month of losses for the worst economic streak since summer 2021, as volatility in agricultural output combines with flatlining secondary and tertiary activity. We already know that industrial production contracted in February as extractive and construction industry activity declined against a rise in manufacturing. On the other hand, retail sales surprised with a 0.4% m/m expansion in data published Friday morning. The INEGI’s timely indicator of economic activity points to a 1.7% y/y expansion, but it has overshot over the past three months.

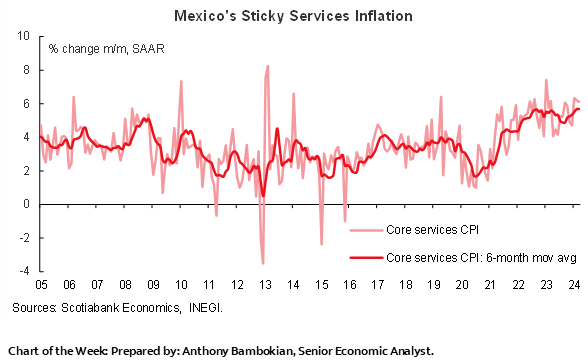

Wednesday’s prices data for the first half of April are expected to show barely any deceleration in core inflation and are even seen ticking a touch higher in headline inflation. Mexican inflation trends remain ultra-sticky, particularly in core services that are running at an average annualised pace of 5.7% over the past six months (seasonally-adjusted) with no suggestion of heading lower soon.

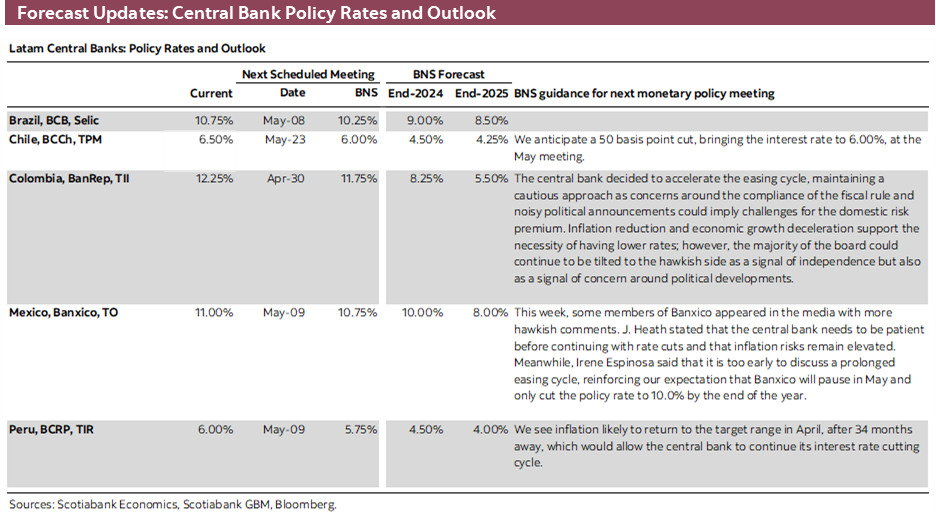

It’s no surprise then that Banxico has seemingly decided to take its time with policy easing, more so if the Fed is now on track to not begin cutting until Q3. A lower than expected inflation reading next week would need to be followed by a few more like it to materially alter our Banxico rate call of 10.00% at year-end. In today’s report, our team in Mexico provide their views on the recent volatility in Mexican interest rates and interpreting Banxico communications.

Elsewhere in the Pacific Alliance, we won’t have a lot to materially move local markets. Peru’s and Chile’s schedules have nothing on the data front that catches our eye. Both countries publish producer price indices data on Wednesday but the figures should come and go. In Peru, we just have the usual political intrigue to monitor, but with limited market implications. Through all the data of the past few months and a change in our (and the market’s) expectations for Fed policy, our economists in Peru have lifted their year-end forecast for the BCRP rate, as explained in today’s publication. Brazil’s central bank is also likely to soon take a break in its rate-cutting cycle, with external (Fed), fiscal, and macro developments increasing policy uncertainty; Friday’s April IPCA-15 print is the local calendar highlight.

Colombia will publish industrial and retail confidence data, as well as unemployment rate figures in the second half of the week. Again, don’t expect markets to read much into the figures, as they will instead be focused on external developments and the possible progress in Pension Reform legislation in Congress. After approving about 60% of the Reform’s articles as of Wednesday night, lawmakers took a break until Monday to discuss the remaining thirty-six articles of the bill. For our economists—as they discuss in today’s report alongside observations on COP moves—the most important component of the Reform is how the public pension fund would operate, but this remains a ways away.

PACIFIC ALLIANCE COUNTRY UPDATES

Colombia—Discussing the Fundamentals Behind the Exchange Rate in Colombia and Pension Reform

Jackeline Piraján, Senior Economist

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Daniela Silva, Junior Economist

+57.601.745.6300 (Colombia)

daniela1.silva@scotiabankcolpatria.com

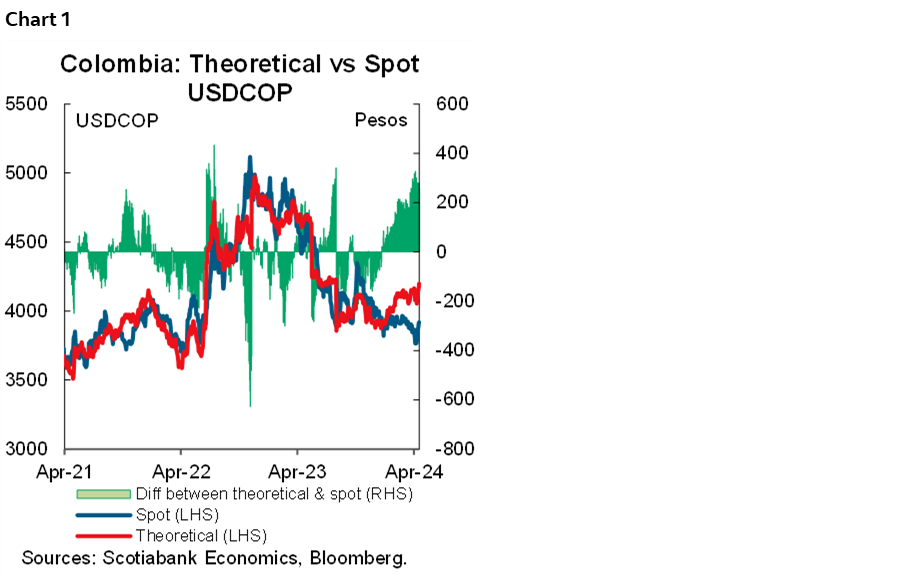

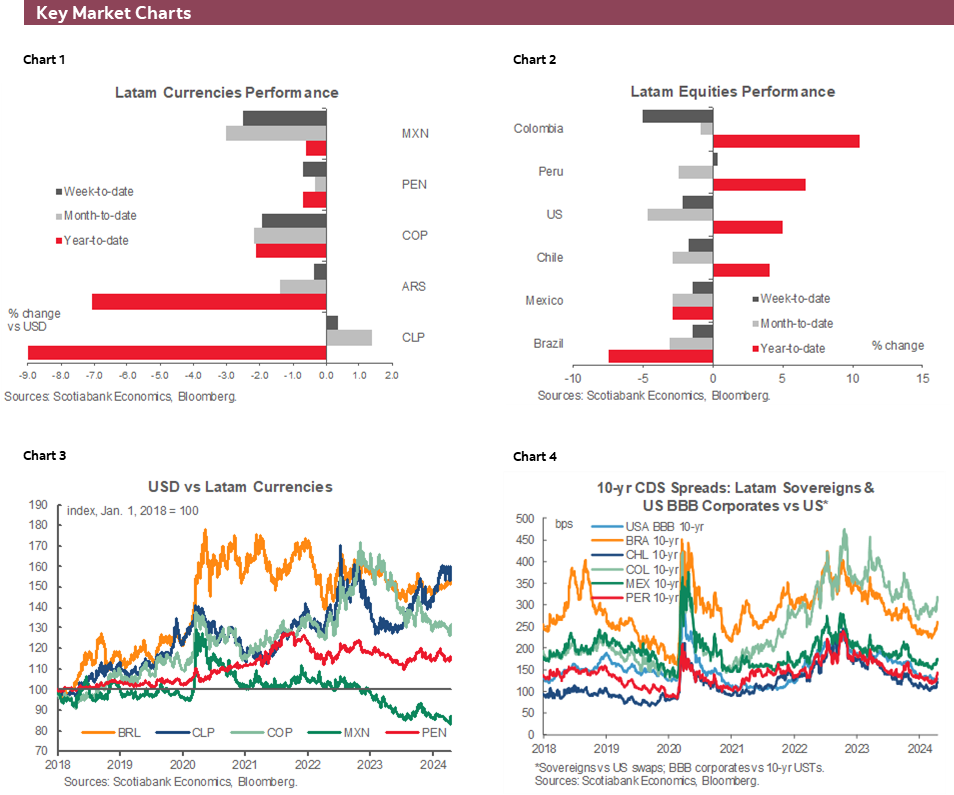

This year, international markets must adjust their expectations about monetary policy; the optimism y about early rate cuts and moderate volatility vanished. In the case of Colombia, USDCOP, over 2023, erased risk premiums that arose during the post-presidential elections period of uncertainty. In that sense, USDCOP operated in a way that was very aligned with traditional macro fundamentals. However, in 2024, the currency decoupled, and COP stayed below the level suggested by conventional macro models (chart 1). In recent days we have seen an upside move but the USDCOP levels are still below fundamental levels.

Many hypotheses surged about why the COP stayed at “relatively” strong levels. From a financial/markets perspective, rate differentials amid a more cautious than anticipated BanRep board kept the COP as one of the most attractive carries across the currencies spectrum. Additionally, the spike in oil prices could also contribute to COP strengthening. On the macro front, economic activity continues to show signs of weakness, which in turn means that the demand for dollars by importers remained low. To the previous point, we have to add that during March and April a couple of events took place: a transaction in the equity market (Nutresa OPA) and the corporate tax payment season, which contributed to better USD inflows. All in all, it was the perfect scenario to see a significant YTD appreciation of more than 9% and atypically low volatility. After reassessing the rate cuts scenario from the Fed and moving past temporary or one-off events, the COP is losing ground but is still below the fundamental medium-term level estimated at 4,100 pesos.

What is being missed in the FX level?

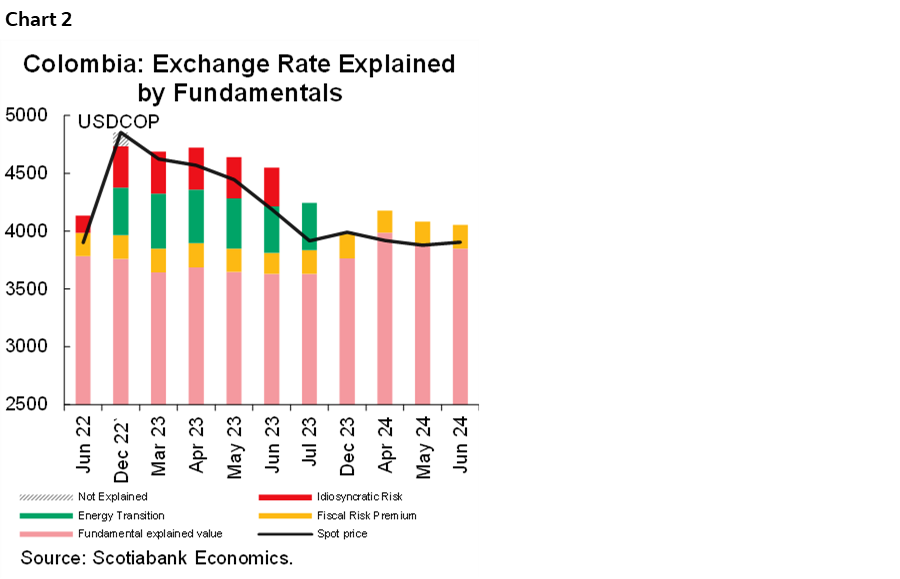

Using our FX fair value model as a starting point, we notice that during 2024, the sensitivity of the USDCOP to higher oil prices and to wider rate differentials vs the US increased. The sensitivity to domestic risk—measured via CDS spreads and regional risk as a principal component indicator of Latam trends—increased when both measures of risk rose. All in all, the sensitivity to positive developments increases. However, what is missed in the equation is that the market euphoria is forgetting about a risk premium associated with the fiscal situation in Colombia and that surge in mid-2021 after the downgrade in the investment status. Recent estimations show that this premium represents 192 pesos (chart 2), which could be part of the misalignment between the spot and macro fundamental levels. We think that over time markets would incorporate this premium again.

It is worth noting that despite markets not pricing the fiscal premium for the moment, we are not expecting a huge depreciation in the short run. This is firstly because economic activity and real demand for dollars are weak, but also because institutions in Colombia proved to be robust, and idiosyncratic risk premiums for political concerns were contained.

What about reforms and their potential impacts?

For now, the USDCOP has responded to the adjustment in expectations around the Fed. However, in Colombia, the reform agenda still remains in focus. This week, Pension Reform partially advanced in the Senate Plenary after the Liberal Party decided to support the debate of the bill. However, the Reform still has a long way to go since it not only has to pass the Senate but also has to pass another two debates before June 20th—the seventh commission and Plenary in the House of Representatives. Time is tight, but we don’t discard it will be approved. In any case, many things are difficult to define, and it is difficult to anticipate an outcome. Even if we have complete approval in the coming weeks, regulations need to be determined before its implementation.

Recall that the current pension system in Colombia is composed of two competing sub-systems, the public (pay-as-you-go/defined benefit) and the private (defined contribution scheme), in which only the private component has investment portfolios; in fact, private pension funds represent 30% of COLTES holders, and their assets under management (AUM) amount to around 30% of GDP. Fears around Reform are about what could happen with pension savings. For now, what is in the proposal is that private pension funds will continue to administrate their current level of AUMs. However, most of the new inflows will go to a public fund, whose administration is still to be determined. Preliminary proposals suggest that the public fund should invest as a regular fund. Still, we must wait for the official regulation if the Pension Reform is completed and approved.

All in all, it is still too early to anticipate an outcome. However, we highlighted that the Reform is not carving out savings from private pension funds, which presents the possibility of forced asset sales (as in the case of Chile or Peru). The critical point is how the new potential public fund will operate, and that is where the spotlight should be.

Mexico—Mexican Rate Volatility and Banxico Communications

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

- Banxico signaled its easing cycle will be cautious, likely intermittent, as well as data dependent. Banxico’s message on this front has been quite consistent. However, the meaning of the cautious easing cycle, and how factors such as US policy, Mexican peso dynamics, and how much the board is willing to relax policy before we get clear signs that sticky core services inflation is abating is not clear.

- Those uncertainties likely explain part of the recent volatility in Mexican rates, which have witnessed moves of 60–100bps in different nodes of the curve over the past month, moving from pricing in 200bps of cuts in a 12-month period to 150bps.

- Although Banxico updated its estimate of the real neutral rate in 2019 (2.6%), we are not aware of any updated estimate of its monetary conditions index, and hence the central bank’s views on how the combination of high real rates and a very strong peso affect the economy are an enigma.

- The transmission channel for interest rate policy into the broad economy in Mexico is narrow, with credit to GDP hovering around 45%, and given low sensibility of interest rates to policy rates (even in mortgages) may be even lower than estimates suggest.

- On the FX side, the openness of the Mexican economy, where trade/GDP consistently sits north of 80% of GDP also means that the currency plays an important role on broad monetary conditions.

- In summary, we argue that part of the recent volatility stems from the lack of guidance on how three elements interact with each other in the board’s decisions: 1) the much looser fiscal stance from the government (especially at a time when the economy is doing fine), 2) broad monetary conditions and the weight of FX and rates settings, and 3) relative monetary policy settings to the US Fed’s.

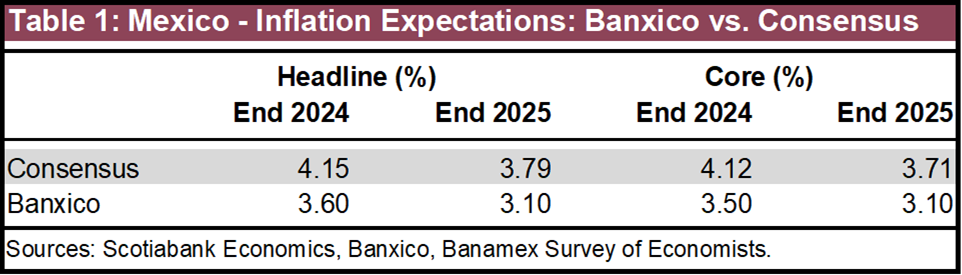

Banxico kicked off its self-described gradual and cautious easing cycle, just before markets began re-pricing expectations for the US. In its March 21st meeting, the board of Banxico delivered a 4:1 decision to cut its overnight rate by 25bps, signaling that future decisions will be data dependent. Banxico’s own projections have inflation converging to within 10bps of its target within the 2 year monetary policy horizon. However, consensus in the latest Banamex survey still anticipates that both core and headline inflation will sit near the top of Banxico’s inflation target tolerance band by the end of 2025. This suggests that private sector expectations are not adequately anchored and raise the risk of Banxico’s inflation objective being seen as asymmetric, and somewhat lacking in commitment (table 1).

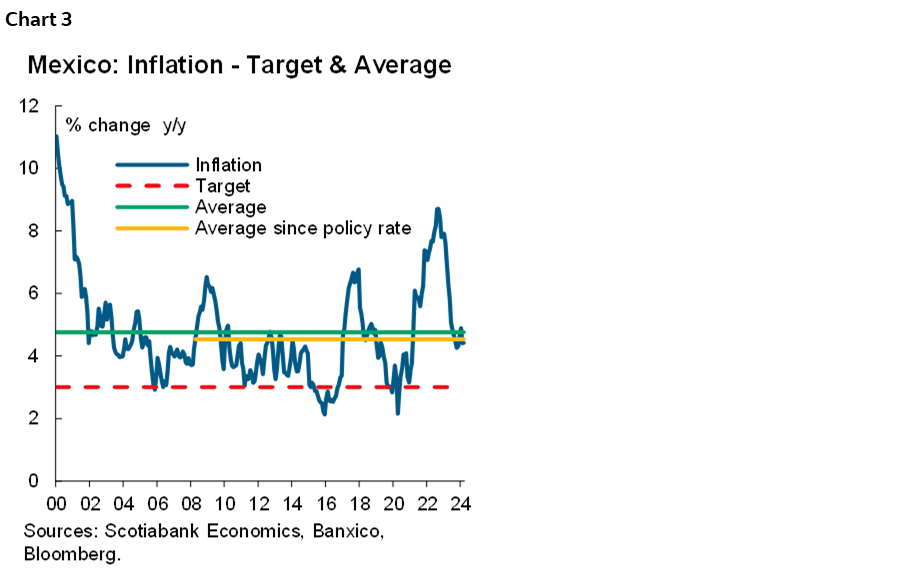

Former President & CEO of the Minneapolis Fed Narayana Kocherlakota argued that recent Fed Chairs have had biases in their inflation targeting, with some being overly hawkish (Bernanke), some too dovish (Yellen), and some having inconsistent biases (Powell). Data suggests that Banxico could have a consistent overly dovish bias, given that inflation has consistently averaged above not only the middle of its target, but above the ceiling of its target range. If we look at the Fed in comparison, inflation overall has been about 70bps above its 2% target over the past 30+ years, but importantly, in the 10 years following the 2007 crisis, inflation averaged below target. Correcting this bias could be part of the reason why Banxico tightened as strongly as it did (it hiked real rates to one of the highest in the world, and delayed the start of its easing cycle to materially later than some other central banks in LATAM). We would argue that Banxico’s hawkishness was prudent (chart 3).

However, at this point in time, it is difficult to sort through Banxico’s communications. Part of the issue is a very uneven amount of communication from its board members, part is due to lack of clarity in how the central bank sees the interaction among different relevant variables (fiscal policy, spread relative to the Fed, FX and different components of inflation), and part could be due to lack of updates in some technical measures such as the Monetary Conditions Index.

Our estimates suggest that Mexico’s neutral rate lies somewhere around 200–300bps in real terms, which is in line with Banxico’s estimate of it sitting somewhere around 260bps in real terms. Given inflation is still materially above the mid-point of Banxico’s target, and services core inflation in particular has been very sticky, tight settings are appropriate. However, Mexico’s real policy rate is currently north of 650bps, which means policy settings are very tight. In addition, if we consider broad monetary conditions, and take not only interest rates, but also the exchange rate into consideration, conditions are arguably even tighter.

Mexico is a complex economy, where the credit channel is narrow (credit to GDP hovers around 45%), and the economy is very open (exports and imports are north of 80% of GDP), meaning that the transmission channel for exchange rate and interest rate settings into the economy are similar in size. We have not seen any updated Broad Monetary Conditions Index from Banxico, which could explain some of the market volatility recently, as there is a debate among financial market players on how strength in the Mexican peso (which had been the case until the last couple of weeks), factors into Banxico’s assessment of adequate monetary policy moves.

We tend to agree with the message that Deputy Governor Heath delivered in Tuxtla Gutierrez in December, when he said Banxico can afford to ease policy somewhat, even without drops in core services inflation and the Fed starting its own cycle. How much is a matter of debate, but we would argue that at this juncture, the spread over the real neutral rate (where there is very ample room) is less relevant than the spread over the Fed. Given the premium that markets are demanding for Mexican debt over USTs, we think it would be prudent for Banxico to not cut its spread relative to the Fed to less than 500bps, as that could un-anchor the peso, triggering a two-sided easing in broad monetary conditions. Hence, we think Banxico can likely cut around 100bps in addition to the previous 25, without meaningful risk.

Peru—BCRP May Be Slower in Reducing Rates, Following the Fed

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

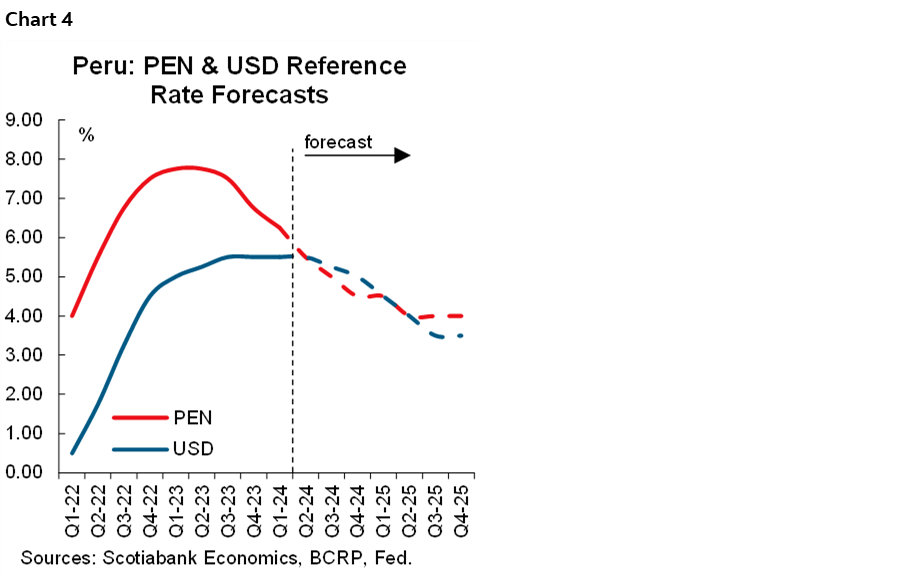

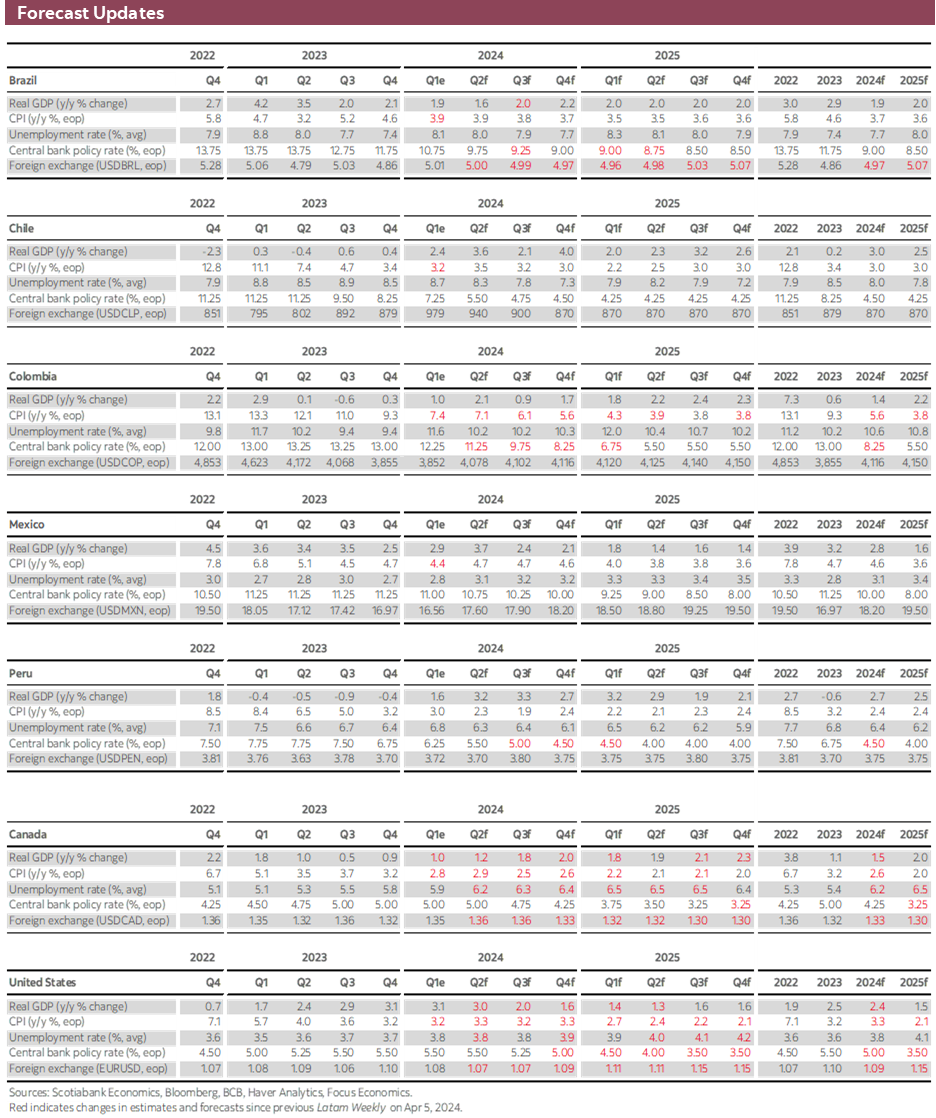

We are adjusting our BCRP reference rate forecasts for 2024 and 2025. We are raising our forecast for year-end 2024 from 4.25% to 4.50%. We are maintaining our terminal rate at 4.00%, to be reached in Q2-25.

We have adjusted the reference rate path slightly, now expecting only two 25bps cuts in Q3-24, to 5.00% (previously three cuts to 4.75%), a 50bps decrease in Q4-24 to 4.50% (previously 4.25%), and then 25bps declines in each of the first two quarters of 2025, to reach the terminal rate at mid-year. Note, then, that our overall view is the same, namely, that the BCRP reference rate will continue declining and reach its terminal rate in mid-2025, only the trajectory of this decline will be mildly slower.

Our new figures largely reflect a change in the outlook for differentials between the BCRP and the Fed reference rates. Scotiabank Economics has increased its Fed reference rate forecasts to 5.00% from 4.50% for year-end 2024, and to 3.50% from 3.00% for year-end 2025. This narrows the rate differentials with respect to the BCRP reference rate and flips them into negative (BCRP rate below Fed rate) earlier and by a greater magnitude. The BCRP has in the past expressed concern over the possibility that Peru’s rate could fall below the Fed rate for any sustained length of time, as this would have repercussions on short-term capital flow and, thereby, on the PEN FX rate. Our new forecasts reflect our expectation that the BCRP would wish to soften this effect.

However, our new forecasts do not eliminate the rate inversion completely. Peru’s inflation and growth dynamics are very different from the US, and we believe it likely that the BCRP will have little choice but to accept some degree of negative rate differentials for a couple of quarters. But, what it can do is soften the impact by being less aggressive in reducing its policy rate. One of the reasons that we believe that the BCRP will have room to accept negative interest differentials is, well, good luck. Metal export prices have risen significantly and, as a result, the impact that negative interest rate differentials could have in weakening the PEN should be at least partially compensated by a greater than expected inflow of USD from high metal exports working in the opposite direction.

Inflation, of course, is another consideration for the BCRP. We have not changed our domestic inflation forecasts, so this would not be, per se, a reason to modify our reference rate expectations. However, Peru CPI does not exist in a void, and the fact that US and, indeed, global, inflation is proving rather sticky does pose a greater risk than otherwise suspected on Peru inflation. This may also be a consideration, albeit probably a minor one, on the BCRP deliberations in favour of greater caution.

Finally, Peru GDP growth is finally showing some life, which is likely to weaken the BCRP’s sense of urgency to lower rates.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.