ECONOMIC OVERVIEW

- Central bank decisions around the globe in the past few weeks have all been relatively as expected. No major central bank surprised in their direction for rates, nor in the size of cuts where these were rolled out.

- With strict data-dependent guidance, next week’s economic activity figures from Colombia, Peru, and Brazil are key data to monitor. But, be careful not to read too much into these prints ‘poisoned’ by an Easter timing effect.

- External events, namely the release of US CPI next week and geopolitical developments, also hang over Latam markets.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Colombia and Peru.

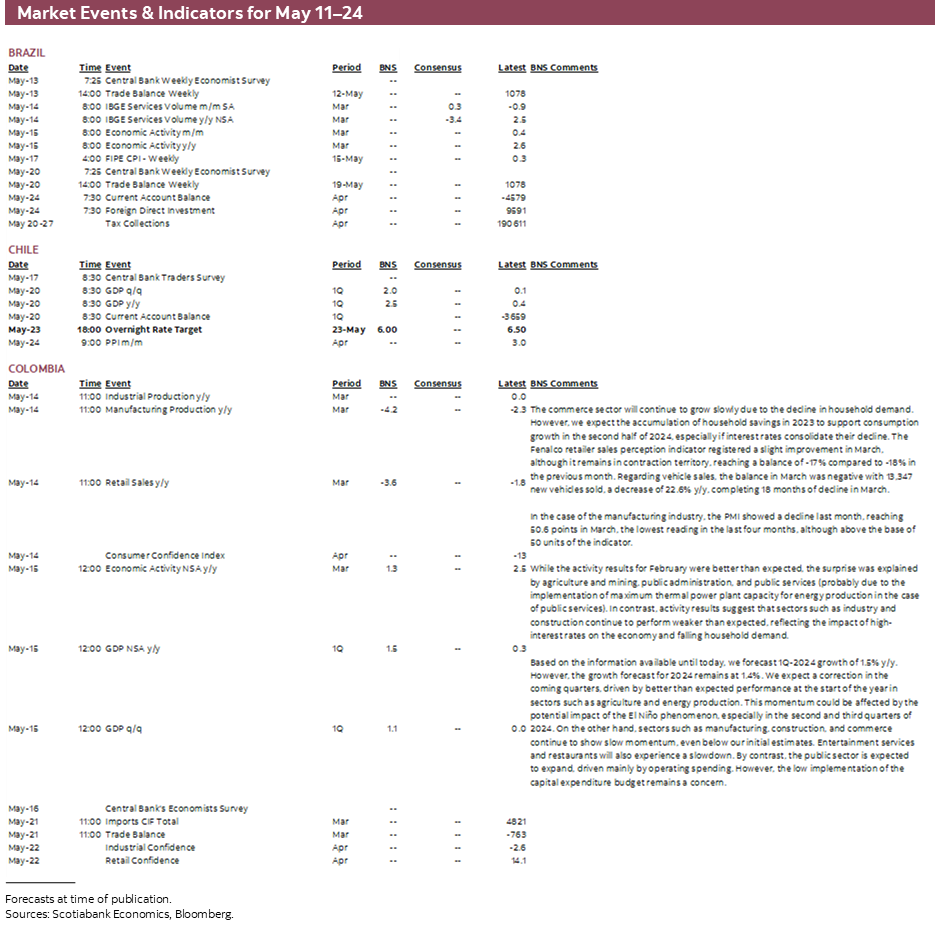

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period May 11th–24th across the Pacific Alliance countries and Brazil.

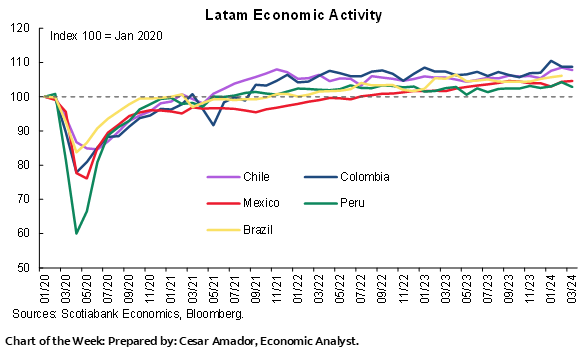

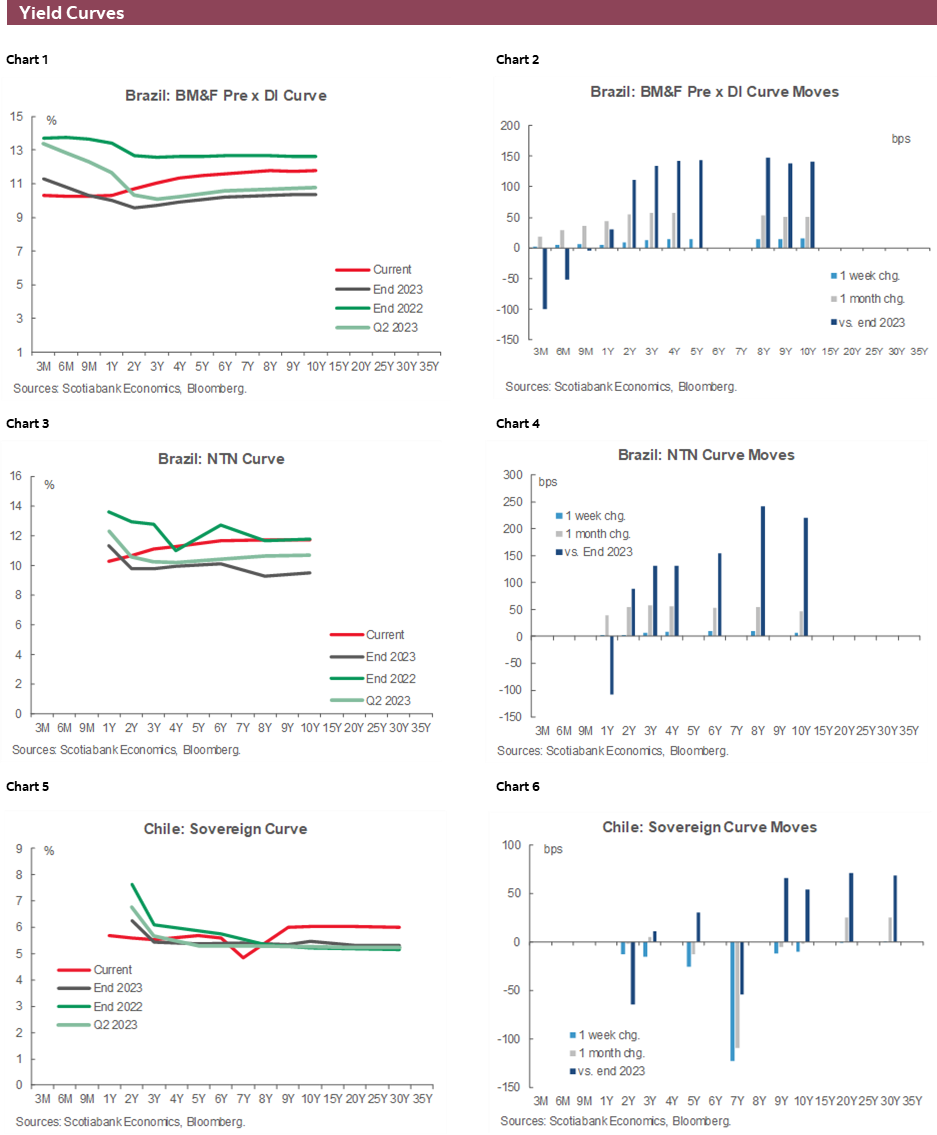

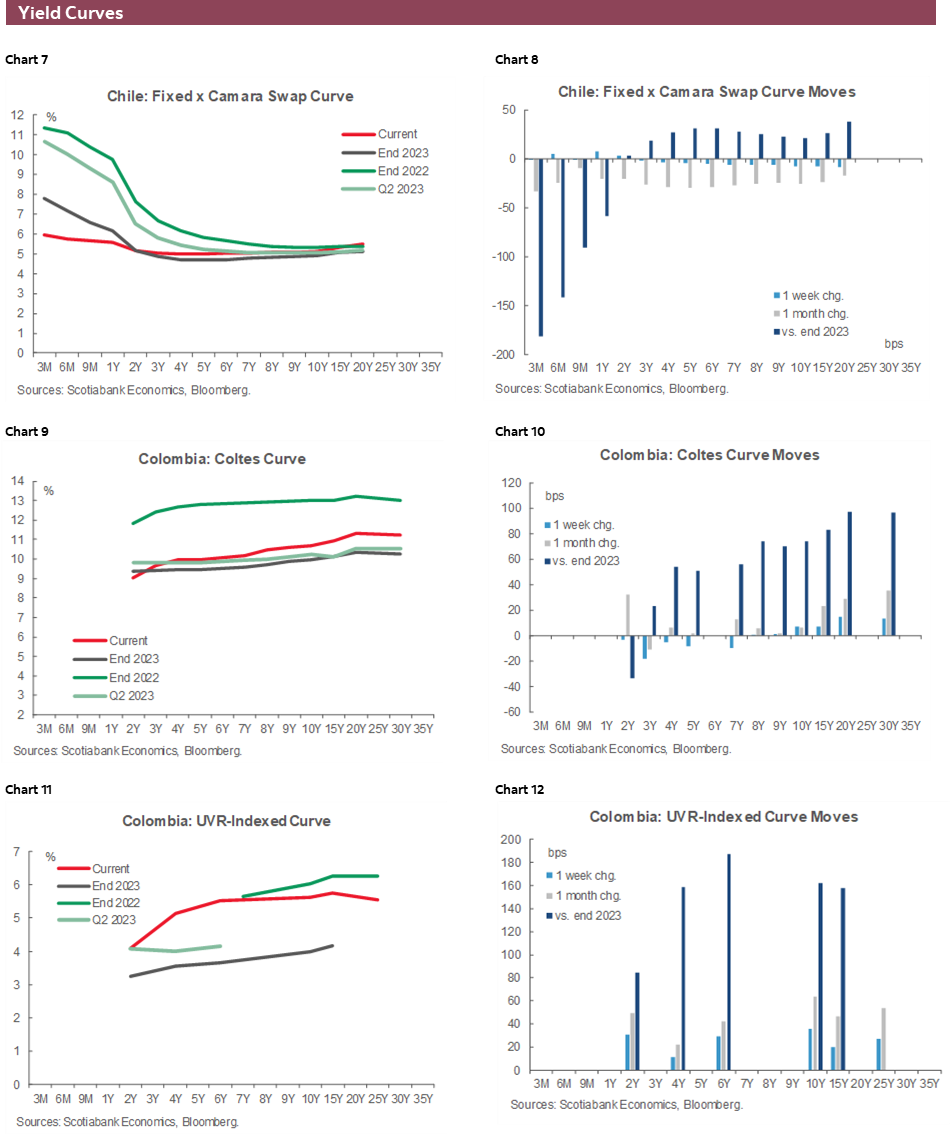

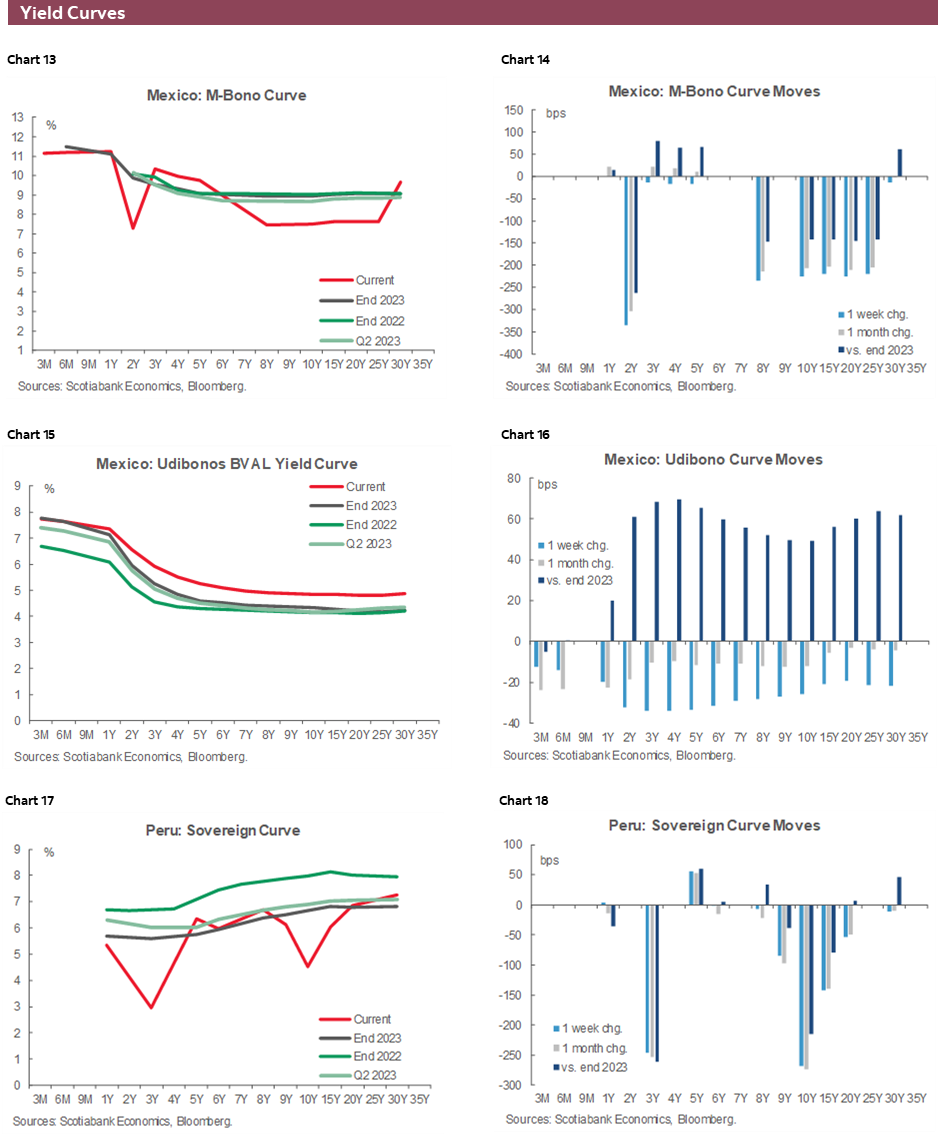

Chart of the Week

ECONOMIC OVERVIEW: POST-DECISIONS TIME OUT (NOT REALLY)

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- Central bank decisions around the globe in the past few weeks have all been relatively as expected. No major central bank surprised in their direction for rates, nor in the size of cuts where these were rolled out.

- With strict data-dependent guidance, next week’s economic activity figures from Colombia, Peru, and Brazil are key data to monitor. But, be careful not to read too much into these prints ‘poisoned’ by an Easter timing effect.

- External events, namely the release of US CPI next week and geopolitical developments, also hang over Latam markets.

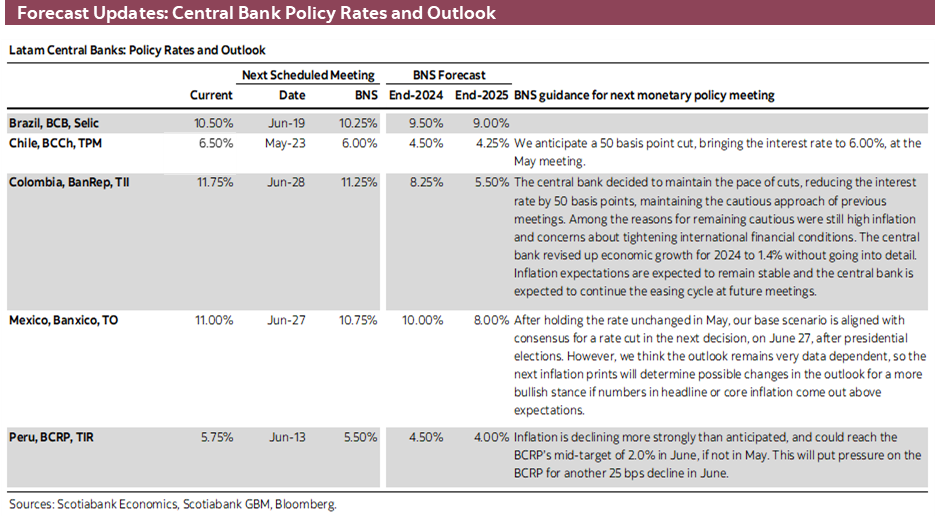

From the Bank of Japan’s rate hold two weeks ago, through the Fed’s benign rate announcement, and to Banxico’s pause and the BCRP’s cut yesterday, monetary policy decisions over the past couple of weeks have all been relatively as expected. Of the major economies that we follow, none of their central banks went off-consensus in terms of direction or in the magnitude of these in the case of cuts.

Guidance was the focus as some banks near the start of their rate cutting cycle (e.g. the BoE) while others shift to a slower pace and mull when halting cuts may be appropriate (e.g. the BCB). But, it truly all comes down to inflation and growth data, and some have to also closely observe how external conditions evolve in terms of commodity prices, global yields, and their domestic exchange rates—as is the case at Latam central banks. Even the weather needs to be monitored as heatwaves and droughts impact economic activity and prices for perishables (see Colombian and Mexican inflation).

Recent prices data in the Latam region were mixed as roughly in line readings in Mexico, Colombia, and Brazil contrasted with a strong beat in Chilean inflation and a solid undershoot in Peru. The latter’s data contributed to a relatively dovish (read: optimistic) decision by the BCRP, supporting our projection of 25bps cuts at the next few meetings. As for Chile’s upside surprise, we don’t think it will pull the BCCh away from a 50bps cut, which is a view shared with the median economist polled by the bank. Traders may be a bit more split in their responses to the BCCh survey (results out next week), but market pricing continues to favour a half-point change on the 23rd.

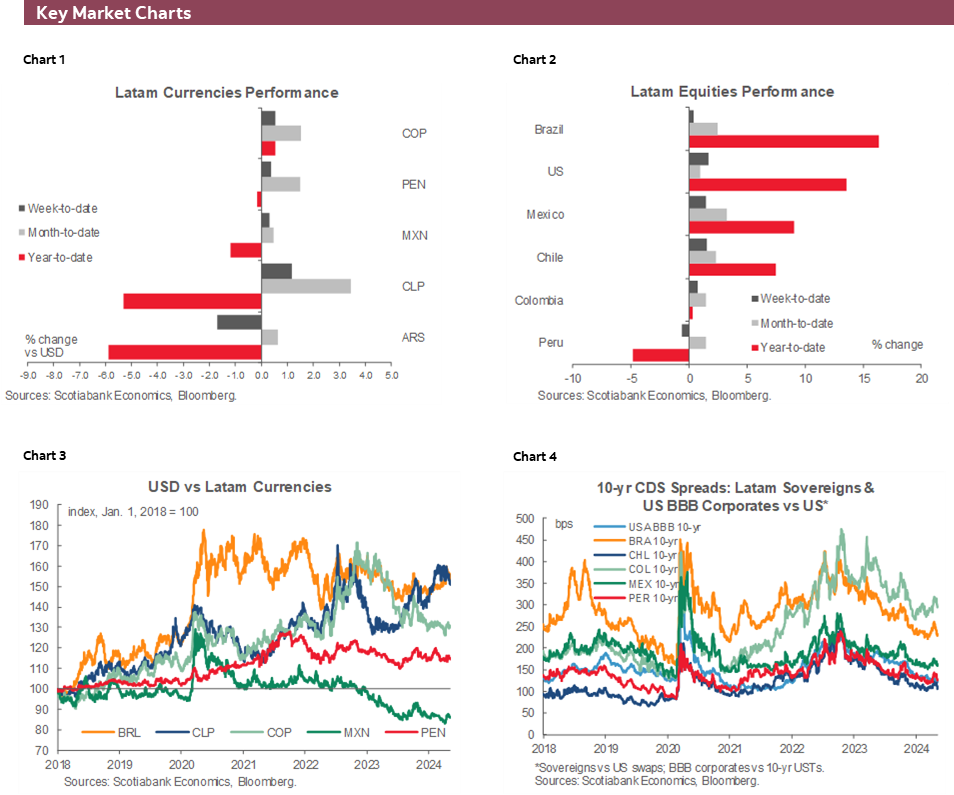

On the external front, the market’s dovish take on Powell’s press conference helped a sharp leg lower in US yields, providing some relief to Latam currencies that were threatened by narrowing rate differentials. For instance, imported inflation via a weaker currency was evidenced in Chile’s CPI data that showed a strong rise in new auto prices. Of course, the 20%+ increase in WTI oil prices in the year to early-April was also preventing a more convincing decline in non-core goods inflation, but the year-to-date rise in prices has now roughly halved to ~10% so some pressure is coming off there as well. There’s no point in sounding the all-clear here, however, as geopolitical risks keep a floor on oil prices and next week’s US CPI release may revert the rates rally post-Fed (to be fair, it could also supercharge it).

Latam economic activity figures have been so-so of late. Mexican Q1 GDP was a bit better in q/q terms but there’s not a lot of confidence in expecting a strong period of growth, less so with power outages and heatwaves impacting the country these days. Maybe increased public spending or support ahead of the June elections in these few weeks could give a hand to growth conditions. There won’t be much to monitor in Mexico (as in the case of Chile) next week with no major data on tap, but we’ll keep a very close eye on possible comments by Banxico officials to gauge the odds of a June cut. Political developments in both countries also stand as key drivers of market sentiment. In Chile, President Boric is pushing for a vote on his modified pension reform proposal soon, while Mexico’s government studies options on a folding in of Pemex debt under the sovereign.

In contrast to bare Mexican and Chilean calendars, Colombia’s is packed with data in a holiday-shortened week with markets closed on Monday. Tuesday’s release of retail sales and industrial/manufacturing production data will be key in refining our projections for Wednesday’s March and Q1 GDP data that should show prevalent economic weakness in the country. BanRep also publishes the results to its survey of economists on Friday and, as always, watch out for unexpected Petro announcements. In today’s report, our team in Colombia analyses the dilemma that BanRep officials face in balancing depressed growth against still very high and sticky inflation; for now, the focus remains on inflation, but when could this change?

Wednesday also presents monthly activity data from Peru and Brazil for March. As our team in Lima outlines in today’s Weekly, the print is going to be a disaster. Year-on-year growth may be null or negative, what a mess. Hold on though, we’ve been here before with Chile. The earlier Easter holidays period in 2024 when compared to 2023, falling in late-March versus early-April, respectively is a big drag so one should wait for the April rebound before making any strong judgments about Peru’s performance based on year-on-year data. And, as often happens with Peruvian data, a huge shift in fishing output—this time a 30%+ y/y drop—will make things look much worse than they really are.

Brazilian economic activity is not looking great and the Easter effect should also result here in a very weak y/y print (negative) for March, with the April print eventually giving back some of this pullback. Unfortunately, floods in the southern part of Brazil are already setting up weak growth in May but we’re keeping an eye on how government support may help reverse some of the hit to activity. Local markets will likely end up taking their cue from the BCB’s meeting minutes on Tuesday that may shed some light on why four members (all Lula appointees) preferred to continue at a 50bps click.

PACIFIC ALLIANCE COUNTRY UPDATES

Colombia—The Role of Economic Activity and Employment in the Monetary Policy Easing Cycle

Jackeline Piraján, Senior Economist

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Santiago Moreno, Economist

+57.601.745.6300 Ext. 1875 (Colombia)

santiago1.moreno@scotiabankcolpatria.com

Daniela Silva, Junior Economist

+57.601.745.6300 (Colombia)

daniela1.silva@scotiabankcolpatria.com

Monetary policy in Colombia is facing a macro dilemma; inflation remains well above target, while economic activity is in a negative output gap, and the labour market is deteriorating in the quantity and quality of jobs. Despite that, BanRep’s board has maintained a cautious approach in the implementation of the easing cycle. This suggests that, at least for now, the main concern is not the weak performance of economic activity, but the achievement of the inflation target for 2025. DANE will release GDP numbers on Wednesday May 15th and we expect to see a robust annual expansion mostly explained by temporary factors which probably will reinforce BanRep’s cautious mode in the short run. Either way monitoring economic activity is a relevant task since underlying economic sectors are under pressure and in some point could motivate the central bank to speed up the easing cycle.

In 2023, the Colombian economy faced a challenging year, with a significant slowdown in economic activity, growing only 0.6%, contrary to expectations. The main obstacle was a sharp decline in investment (including inventories) of 24.8% y/y. There was a sharp contraction in inventories, and investment in residential and non-residential construction, as well as in machinery and equipment. All of this occurred in a context of high inflation and high interest rates. A probable temporary consequence is that manufacturing, construction, and mining sectors became less relevant in overall activity, while entertainment has increased its share of GDP.

At the beginning of 2024, the economy showed an unexpected recovery but unfortunately it was attributed to temporary factors. In the YTD up to February, the economy expanded by 2.2% y/y. The positive surprise came mainly from agriculture and mining, public administration, and utilities sectors. In the case of public administration, the payment of salaries to judicial and defense officials boosted this sector, while in agriculture there was an anticipation of crops to avoid significant impacts from the “El Niño” weather phenomenon. In the case of utilities, the jump is attributed to the electricity generation using thermal power plants. Meanwhile, sectors such as manufacturing and construction remained in negative territory, although there were some signals that the activity in those sectors is bottoming. That said, the annual expansion figure is fueled by temporary factors, but when we dig closer, we find signs of deterioration that prove economic activity remains weak.

The labour market is in fact evidence that economic activity is facing a challenging context of job losses and increase in informality. In March, the employment balance was negative with the destruction of -144 thousand jobs. It is worth noting that the largest job destruction came from the agricultural sector (-207 thousand jobs), which supports the idea that the positive behaviour at the beginning of the year was due to temporary factors and that this behaviour will fade in March. In addition, the unemployment rate rose to 11.3%, which represents an annual increase of 1.3 p.p., also in seasonally adjusted terms. The unemployment rate went from 10.7% in February to 10.9% in March, due to factors related to lower employability in rural areas.

Now, although these facts in macroeconomic matters in the aggregate reveal a bias of weakness in terms of economic activity, for the central bank there is not a significant concern about the economy that obliges the Board to accelerate the easing cycle at the next meetings. This could even be observed in BanRep’s latest monetary policy report, in which the technical team estimates that the annual product gap will be around -0.7% at the end of 2024, which represents a smaller projected excess capacity compared to the -1.2% of the January report. For the technical staff, this upward revision to the gap in 2024 is due to an increase in GDP growth projections for that year, reflecting a temporary increase in potential output because of some supply shocks, which would lead to potential growth of 2.9% in 2024, up from the 2.8% estimated at the beginning of the year. Thus, from the second half of 2025, the excess capacity is expected to be gradually reduced, so that by the end of next year the output gap is expected to close, as economic activity becomes more dynamic, headline inflation continues to converge to the target, and real interest rates decline.

From an analytical point of view, there is a moderate weakness in economic activity and a progressive deterioration in the employment situation. However, these factors do not seem convincing enough to accelerate the rate-cutting cycle. Instead, the BanRep board will likely decide to wait for more macroeconomic evidence before considering accelerating the pace of rate cuts. Nevertheless, we expect a 50bps cut at the June 28th meeting. By then, the central bank board will have a couple of inflation readings that are likely to continue to show a moderate move to lower levels. Ahead of next week’s GDP data for the first quarter of 2024, at Scotiabank Colpatria Economics we expect an expansion of 1.5%. For 2024 the projection is of a 1.4% growth, indicating a gradual recovery, although still growing below its potential pace.

With all this in mind, the discussion will be on the agenda of the next meetings and only a significant deterioration in economic activity that deviates from the expectations and projections of the technical team of the central bank, along with a much greater weakness in the labour market and an unexpected reduction in inflation, could tilt the balance toward a more accelerated pace of cuts in the second half of the year.

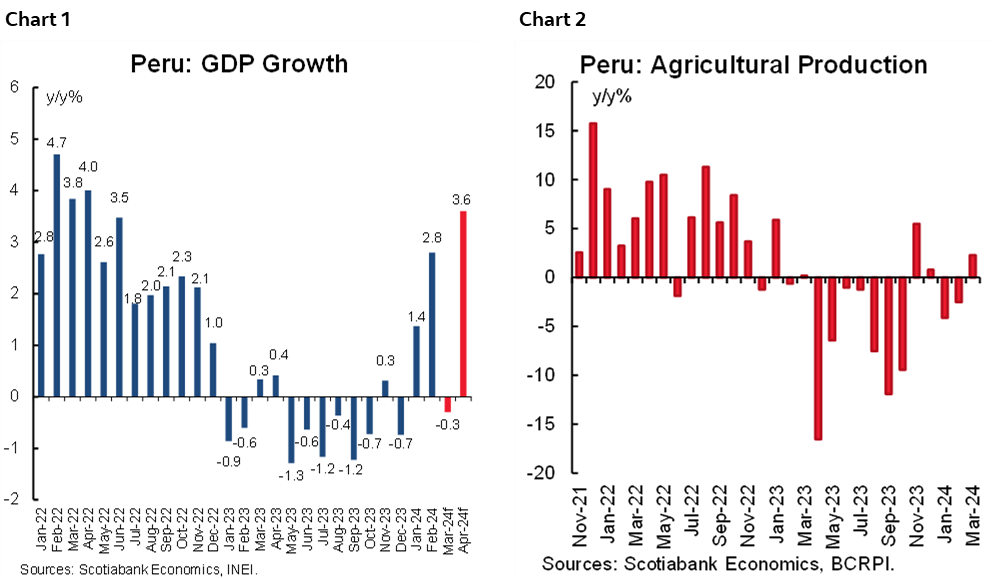

Peru—Forget March, Wait for April

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

Peru’s GDP figure for March will be released on May 15th. Compared to the robust 2.8% YoY growth figure for February, the number for March will not be pretty. The odds are tilted towards the (mildly) negative side of nil, although there is some hope of slightly positive growth if domestic demand linked sectors perform better than we expect.

The main overall reason that GDP growth will be low to negative in March in YoY terms, is that the month had two less working days this year, as Easter occurred in March in 2024, but in April in 2023. Of course, what is lost in March will be made up in April. The contrast is stark. In April, we expect to see GDP growth well over 3.0%, perhaps 3.5%–3.6%.

What a difference an Easter makes. But, it is not the only difference. The varying impact of El Niño on fishing and agriculture is also important. In fact, the main reason why GDP in March may fall into negative territory is the 32% decline in fishing GDP. Now, compare that with April, when the data for fishing points to fishing GDP having risen a whopping 145%! Although fishing has a small weight in GDP, less than 4%, variations such as those in March and April are large enough to make a difference.

Other early figures have been mixed. Mining GDP growth was 4.0%, not bad, but below our trend-based expectations. Oil & gas GDP fell 5.3%, YoY.

Meanwhile, the main, pleasant, surprise was agriculture GDP which grew 2.3%, the first positive figure this year. Does this mean that the lagging impact of last year’s El Niño on agriculture is finally over? Maybe. It’s only one month, and needs to be ratified by output in April. However, the figure for March is a strong sign that the recovery has begun.

Finally, construction. We do not have a construction GDP growth figure, but we do know that cement demand declined 7% in March, suggesting negative construction GDP growth.

In terms of domestic demand, the sector to look at, however, is industrial manufacturing. Once growth in this sector turns decisively positive, we will be able to say with some confidence, that Peru’s economy has turned the corner.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.