- Mid-month Mexican and Brazilian CPI await next week as the main event in Latam, with markets betting on Banxico to deliver another rate cut at its December announcement and the BCB to unwind highly-restrictive policy rates in early-2026. Banxico’s Quarterly Report may provide some insights into the bank’s thinking on still-sticky core inflation against sluggish economic momentum.

- Chile’s macro flood on Friday should show a continuation of economic resilience in October, while markets keep an eye on messages of support for the December runoff candidates—with implications for the legislative balance—as Kast handsomely leads Jara in polls. Colombia’s calendar has little to offer outside of unemployment rate data, while Peru’s is bare of major releases.

- In the U.S., relatively stale September retail sales and durable goods orders figures will keep markets somewhat busy alongside Fed speeches ahead of the communications blackout that starts on the 29th; local markets are closed on Thursday for Thanksgiving. The Eurozone’s majors release inflation data alongside Tokyo and Australia, Canada publishes 3Q GDP, the RBNZ is seen cutting 25bps, and the U.K. government unveils its Autumn Budget.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch in Mexico.

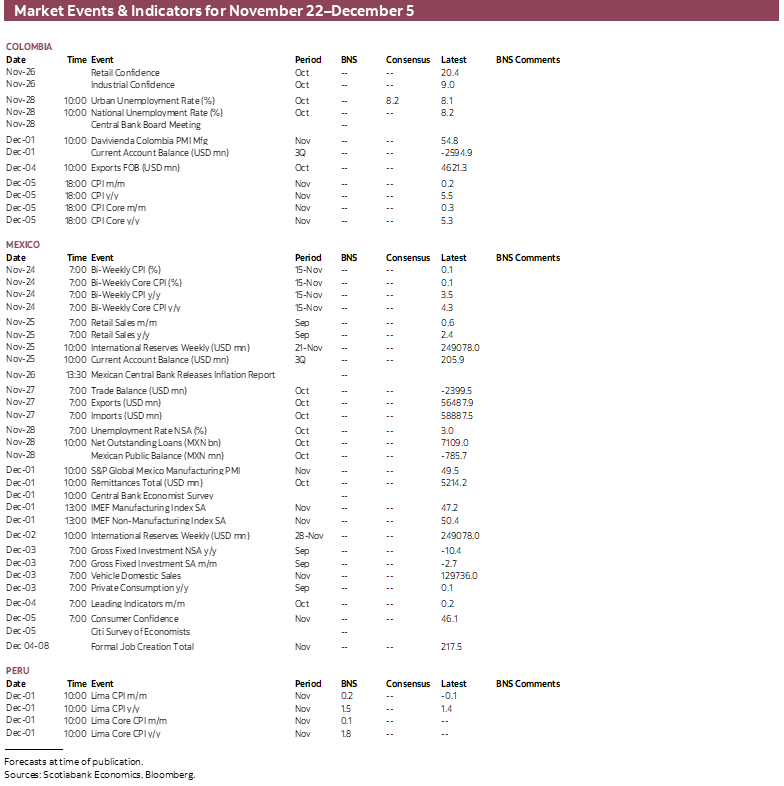

MARKET EVENTS & INDICATORS

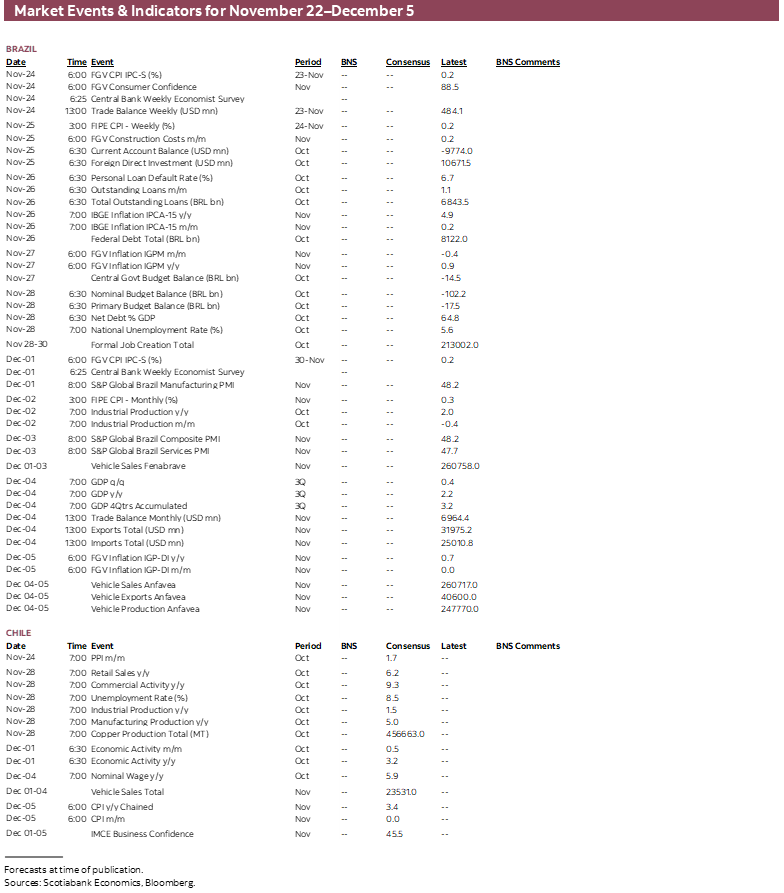

- A comprehensive risk calendar with selected highlights for the period November 22–December 5 across the Pacific Alliance countries and Brazil.

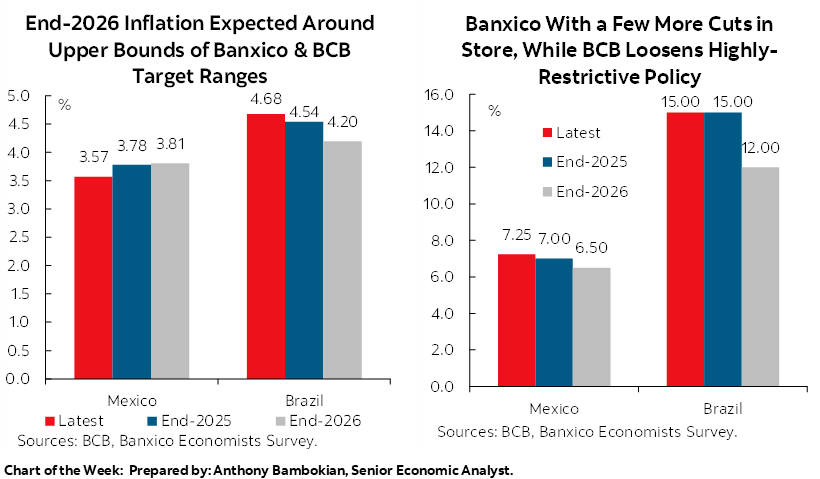

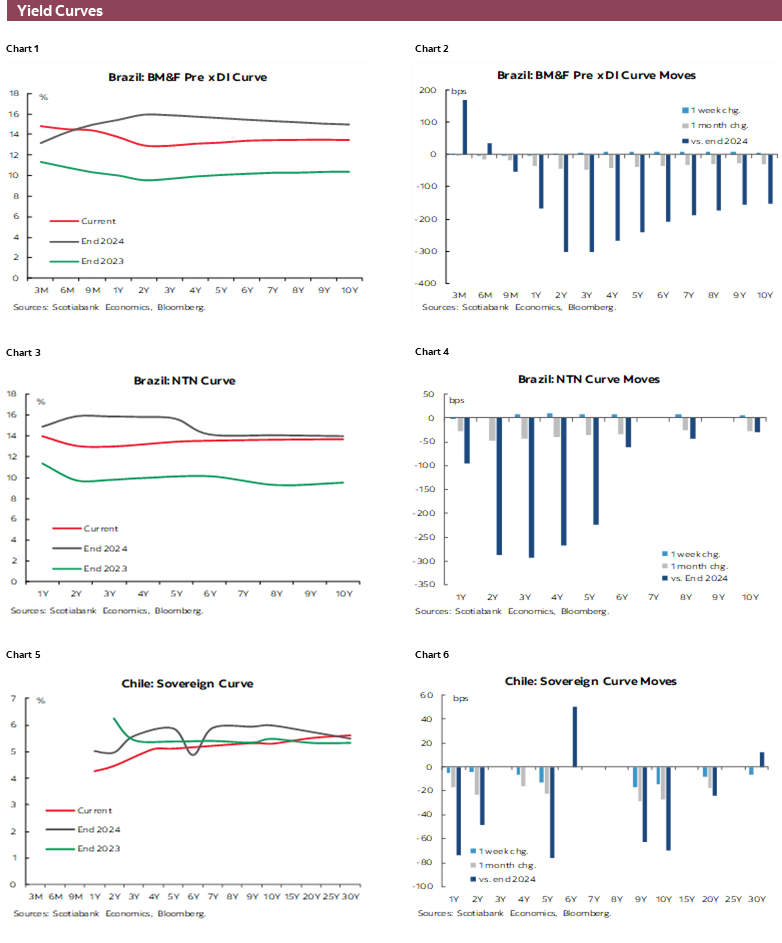

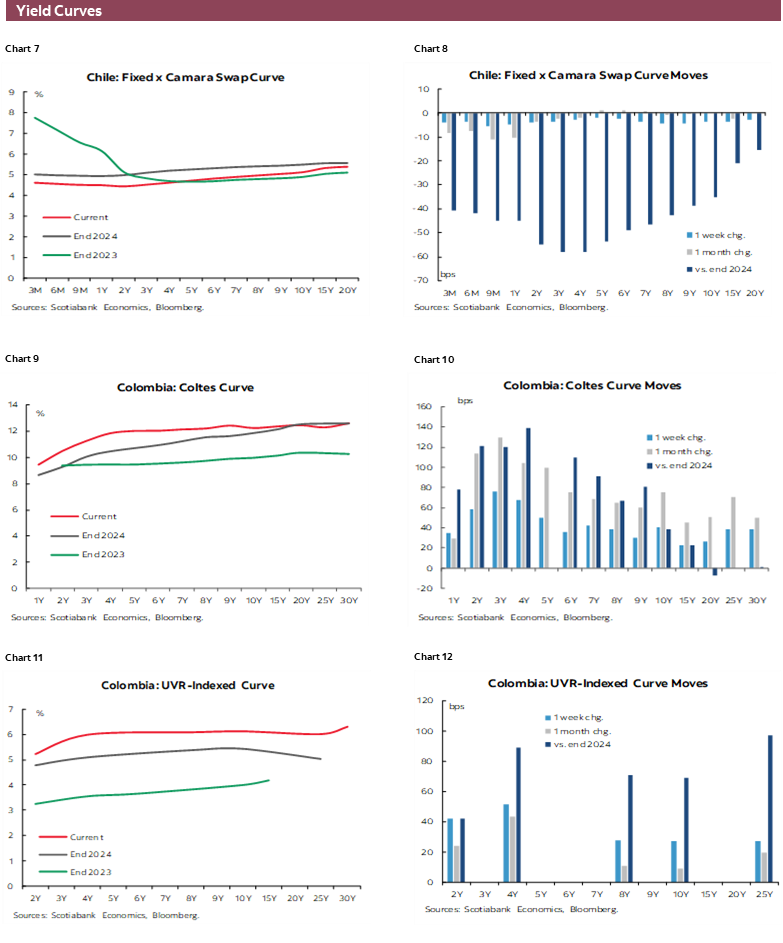

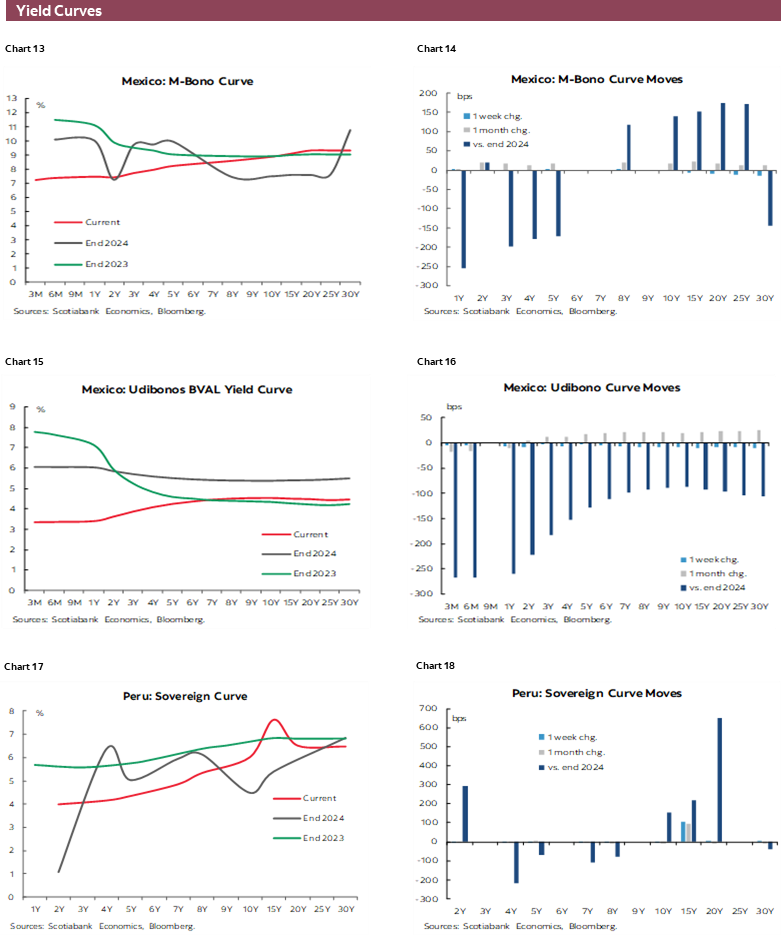

Chart of the Week

ECONOMIC OVERVIEW: REGIONAL AND G10 CPI CLOSE OUT THE MONTH

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Mid-month Mexican and Brazilian CPI await next week as the main event in Latam, with markets betting on Banxico to deliver another rate cut at its December announcement and the BCB to unwind highly-restrictive policy rates in early-2026. Banxico’s Quarterly Report may provide some insights into the bank’s thinking on still-sticky core inflation against sluggish economic momentum.

- Chile’s macro flood on Friday should show a continuation of economic resilience in October, while markets keep an eye on messages of support for the December runoff candidates—with implications for the legislative balance—as Kast handsomely leads Jara in polls. Colombia’s calendar has little to offer outside of unemployment rate data, while Peru’s is bare of major releases.

- In the U.S., relatively stale September retail sales and durable goods orders figures will keep markets somewhat busy alongside Fed speeches ahead of the communications blackout that starts on the 29th; local markets are closed on Thursday for Thanksgiving. The Eurozone’s majors release inflation data alongside Tokyo and Australia, Canada publishes 3Q GDP, the RBNZ is seen cutting 25bps, and the U.K. government unveils its Autumn Budget.

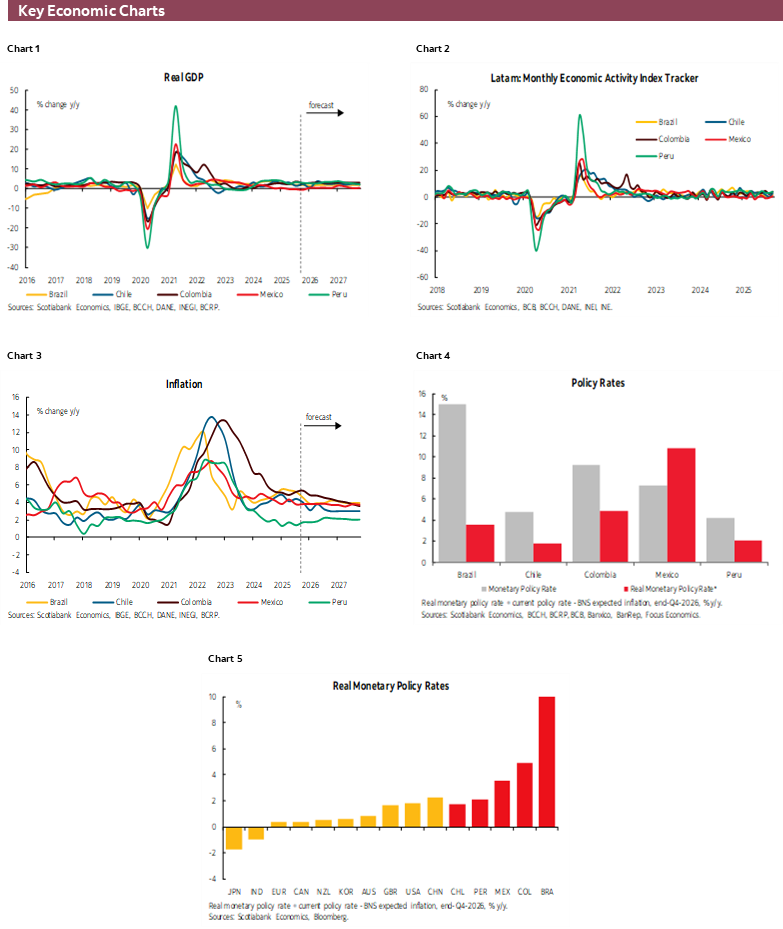

The month is coming to an end with a relatively quieter week across the globe as the U.S. data calendar still looks relatively light (alongside closed markets on Thursday for Thanksgiving) with retail sales in focus while, in Latam, Mexico has a packed schedule in contrast to Peru’s empty slate and Colombia, Chile, and Brazil sit somewhere in between. Both Mexico and Brazil publish mid-month CPI data, and all but Peru (with an empty schedule) release unemployment rate figures, with Chile’s as part of a Friday October macro flood. Mexico’s calendar also includes retail sales and international trade data, and Banxico’s quarterly report.

Elsewhere, Germany, France, Italy, and Spain—three-quarters of the Eurozone basket, coming after the ECB’s meeting minutes—as well as Australia and Tokyo release inflation data, Canada publishes quarterly GDP, the U.K. announces its Autumn Budget, and the RBNZ is expected to roll out a 25bps rate cut. Japan is also closed for business on Monday. Things are also quieter on the earnings front with all the Magnificent 7 names having already reported earnings (neither confirming nor denying AI bubbliness), but we’ll watch for company news on consumer spending strength around U.S. Thanksgiving week sales (September retail sales data out next week are stale). Do keep an eye on comments by Fed speakers in the final days before the pre-communications blackout starting on November 29th ahead of the December 10th decision, with market bets swinging wildly of late to currently sit at about 75% implied odds of a cut.

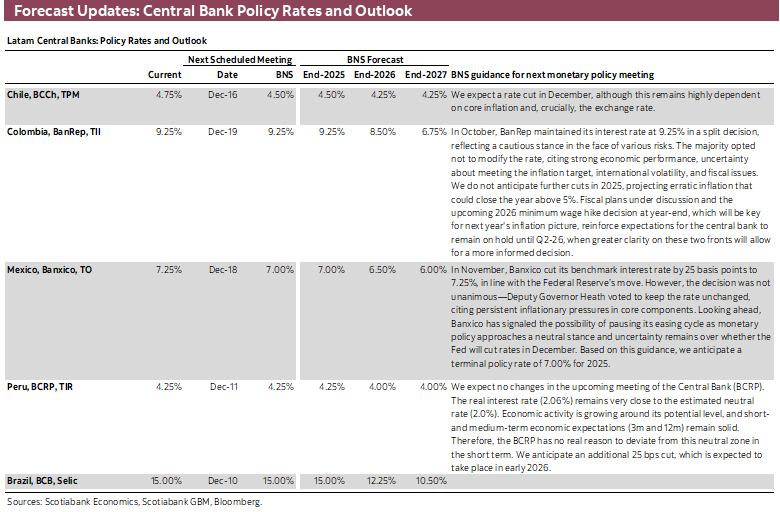

Mexican CPI kicks off the week on Monday, with economists expecting that inflation held practically unchanged from H2-Oct’s readings of 3.5% and 4.3% y/y in headline and core terms, respectively. Core inflation has been stubbornly stuck in a ~4.2–4.3% range since mid-June with all month-over-month price gains in 2026 at or above those recorded twelve months prior due to upward pressures in core merchandise prices. Retail sales out on Tuesday will likely keep to around a 2% pace, nothing extraordinary, while Thursday’s international trade data for October should show a normalisation in the country’s trade deficit which, in September, widened to its biggest since January with Mexico’s deficit with Asia ballooning to $24.7bn from $19.4bn in September 2025; for reference, Mexico’s surplus with the U.S. sat at $25.6bn a couple of months ago, and $21.3bn twelve months prior.

On Wednesday, Banxico releases its Quarterly Report, which will provide some colour on the bank’s views regarding the domestic economy and, in turn, help shape expectations for the December policy decisions. As the team discuss in today’s Weekly, the minutes to Banxico’s meeting in early-November guide that the bank will opt for another rate cut at its final gathering of the year, but it has also slightly opened the door to a rate hold. The Fed’s own minutes showed some division within the FOMC that suggests U.S. policymakers could keep rates steady next month—which may influence Banxico’s rate call the following week. At writing, markets are pricing in about 18–20bps in cuts for the December 18th Banxico announcement (or about the same as is priced in for the Fed).

Turning to Chile, PPI on Monday and Friday’s industrial, manufacturing, and copper output, unemployment rate, and commercial activity releases will bookend a week where markets will also remain focused on expectations for the December presidential runoff elections and expressions of support. The contest will pin the left’s Jara against the right’s Kast, with the latter enjoying a solid lead of roughly 15–20ppts over the former in the handful of polls published since the November 16th vote. Even with around 10% of voters still undecided, a Kast victory seems pretty much guaranteed, but a more convincing win could help strengthen the Chile Grande y Unido coalition’s position in Congress. Last week’s legislative elections left it just shy of a majority in the Lower House with 76 of 155 seats, but a clearer backing of Kast by Chileans would help earn the support of some of the 42 representatives of the Cambio por Chile block.

In Brazil, IPCA-15 inflation is expected to slow from near 5% to the mid-4% area that would mark its lowest reading since late-2024/early-2025, with November discounts guiding the deceleration on top of beneficial base effects. In November 2024, IPCA-15 prices jumped by 0.6% m/m due largely to surging good prices reflecting the impact of droughts. Normalizing conditions point to a softer 0.2% m/m increase this time around that will help bring inflation lower and towards the BCB’s survey year-end median forecast of 4.5%—which sat above 5% as recently as the July poll. That aside, economists expect only a small deceleration to 4.2% at end-2026, at the high-end of the BCB’s 3% +/-1.5ppts target band. The progress made on inflation is nevertheless giving the central bank a chance to cut rates as soon as its January meeting, but the market’s main concern is now how many cuts officials may roll out next year (currently, around 250–275bps are priced in).

PACIFIC ALLIANCE COUNTRY UPDATES

Mexico—Banxico and Fed Minutes Guide December Cut Expectations

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

This week, several key events and economic figures relevant to Mexico’s monetary policy were released. Among them were the minutes from recent decisions by both Banco de México and the Federal Reserve. Additionally, following the reopening of the U.S. government after the partial shutdown, delayed labour market data was published, providing crucial insights for U.S. monetary policy outlook.

The FOMC minutes from the October 28th–29th meeting indicated that many officials consider it appropriate to keep rates unchanged for the remainder of 2025, although some see room for another cut in December if economic conditions evolve as expected. These positions highlight internal divisions over whether inflation or unemployment poses the greater risk. The delay in releasing the October jobs report and uncertainty around other key data, such as CPI, have reduced expectations for a December rate cut.

Meanwhile, September’s nonfarm payrolls surprised to the upside with 119,000 jobs added, compared to the 53,000 expected and the prior month’s decline of 4,000. However, the unemployment rate rose to 4.4%, its highest level in nearly four years, reflecting both increased labour force participation and more layoffs. The report, delayed by the shutdown, showed job gains concentrated in healthcare and leisure, while sectors like manufacturing and transportation shed jobs. This suggests labour market cooling may be more structural—linked to reduced labour supply from immigration policies—than cyclical, lowering the likelihood of further Fed cuts. Additionally, October figures will be released alongside November data on December 16th, without the unemployment rate, adding uncertainty ahead of the December 10th policy decision.

Banco de México also published minutes from its November 6th meeting, where the Board voted by majority to cut the reference rate by 25 basis points to 7.25% and adjusted its language, interpreted as signaling a possible pause in the easing cycle. The minutes reveal that two of five members remain concerned about inflationary pressures, view monetary policy as neutral, and warn that further narrowing of the rate differential with the U.S. could pose medium-term risks to price stability. In this context, we believe the case for the Fed holding rates in December is strengthening, which—combined with higher inflation readings and a weaker peso—could lead Banxico to pause at its final meeting of the year.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.