ECONOMIC OVERVIEW

- Banxico, BCCh and BanRep rate decisions are next week’s highlight in Latam alongside economic activity readings out of Peru, Colombia, and Brazil—all of which will contend with ECB, BoE, and BoJ decisions, U.S. employment, and global PMIs for their markets’ attention.

- For each of the Latam central banks, guidance will be key, with Banxico and BanRep being challenged by markets expecting rate hikes next year, while the BCCh presents updated views in its Monetary Policy Report—with the BCB also publishing its quarterly update.

- Chile will start the week to a likely victory by Kast in Sunday’s second-round presidential vote, with the attention now turning to the balance of power in Congress. In Brazil, developments around Bolsonaro’s amnesty push are also shaping expectations for next year’s possible candidates for the presidency.

- In today’s report, the team in Mexico goes over the influence of this week’s inflation overshoot and the Fed’s decision on Banxico’s expected policy path, while our economists in Peru analyse economic indicators for October pointing to another month of solid economic growth—which, alongside economic confidence and the PEN, seems unfazed by electoral uncertainty.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch in Mexico and Peru.

MARKET EVENTS & INDICATORS

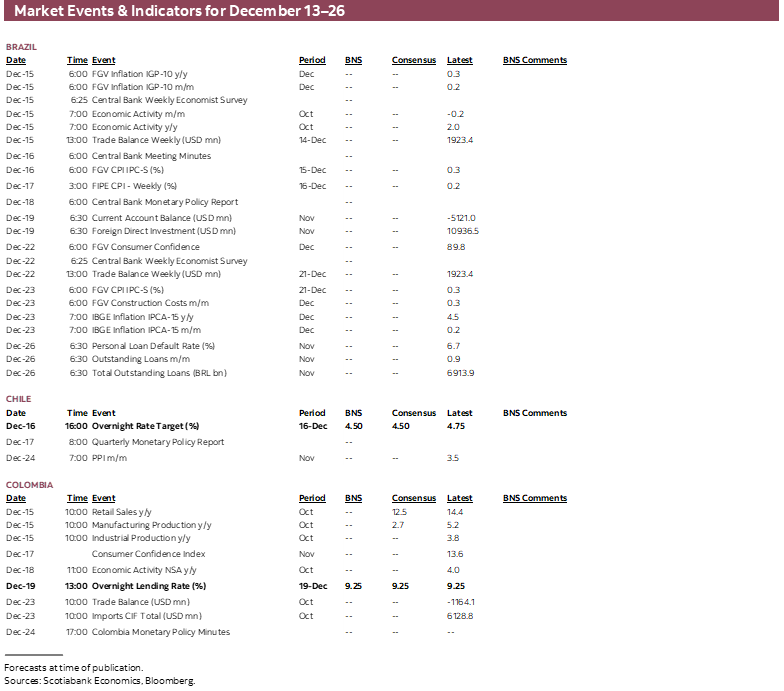

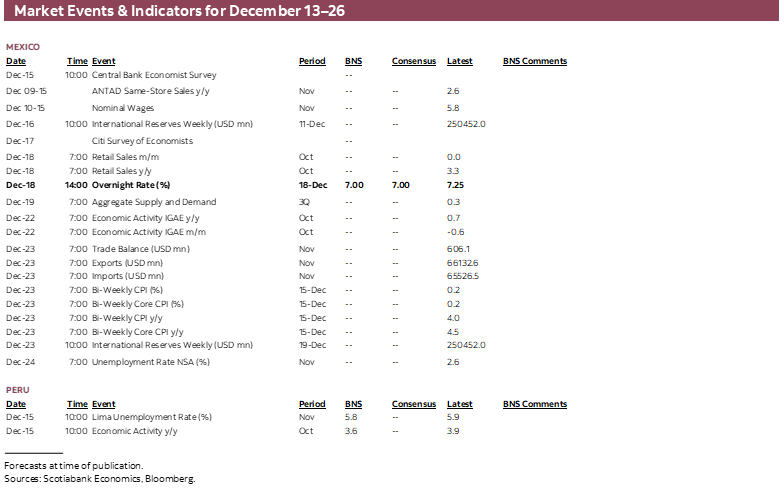

- A comprehensive risk calendar with selected highlights for the period December 13–26 across the Pacific Alliance countries and Brazil.

Chart of the Week

ECONOMIC OVERVIEW: FINAL PUSH OF DECISIONS AND KEY DATA

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Banxico, BCCh and BanRep rate decisions are next week’s highlight in Latam alongside economic activity readings out of Peru, Colombia, and Brazil—all of which will contend with ECB, BoE, and BoJ decisions, U.S. employment, and global PMIs for their markets’ attention.

- For each of the Latam central banks, guidance will be key, with Banxico and BanRep being challenged by markets expecting rate hikes next year, while the BCCh presents updated views in its Monetary Policy Report—with the BCB also publishing its quarterly update.

- Chile will start the week to a likely victory by Kast in Sunday’s second-round presidential vote, with the attention now turning to the balance of power in Congress. In Brazil, developments around Bolsonaro’s amnesty push are also shaping expectations for next year’s possible candidates for the presidency.

- In today’s report, the team in Mexico goes over the influence of this week’s inflation overshoot and the Fed’s decision on Banxico’s expected policy path, while our economists in Peru analyse economic indicators for October pointing to another month of solid economic growth—which, alongside economic confidence and the PEN, seems unfazed by electoral uncertainty.

We have the last big push of the year next week on the monetary policy and data front across Latam and the G10, with about half a dozen central banks on tap around the globe (BCCh, Banxico, BanRep, ECB, BoE, BoJ, etc.) alongside GDP data in Latam, U.S. employment figures, and global PMIs. China will also kick off the week with investment and retail sales data, and markets will keep an eye on Ukraine-Russia peace discussions and the possibility that U.S. President Trump announces his pick to replace Chairman Powell in May. On Monday, Chilean markets will also open to a new President elect, likely one (Kast) that will stand at the opposite end of the incumbent Boric administration. Throughout, markets will be watching AI/tech developments that have been denting hopes for a ‘Santa Rally’ in the final month of 2025.

Starting with Chile, Sunday’s vote is expected to see conservative candidate José Antonio Kast beating out the left’s Jeanette Jara, in a strong shift away from Boric’s reformism to a mandate that Chileans will hope is stronger on crime and deliver improved economic results—with local businesses and markets particularly banking on the latter. As of late-November, polls showed Kast enjoying a double-digit lead over Jara (~10-15ppts) that does not seem at risk of being closed by a massive turnaround by undecideds (15-25% of respondents) that also seem to lean marginally in favour of Kast.

With a Kast victory already priced in by markets, it may not be until the days and months after Kast’s would-be inauguration in March for there to be significant movement in local asset prices regarding politics, or perhaps earlier around noise of Congressional rapprochement. Markets will now gauge the new administration’s pull in Congress given that right wing parties ‘only’ hold half of the seats in the Senate (veto power) and are just shy of a majority in the House. This will likely require working with the People’s Party (~centrist), whose leader Parisi (defeated in the first-round presidential vote) recently said that the would-be victory for Kast would be “bad news” for Chile as it would further polarize political sentiment, and saying his party is not willing to form a coalition with Kast.

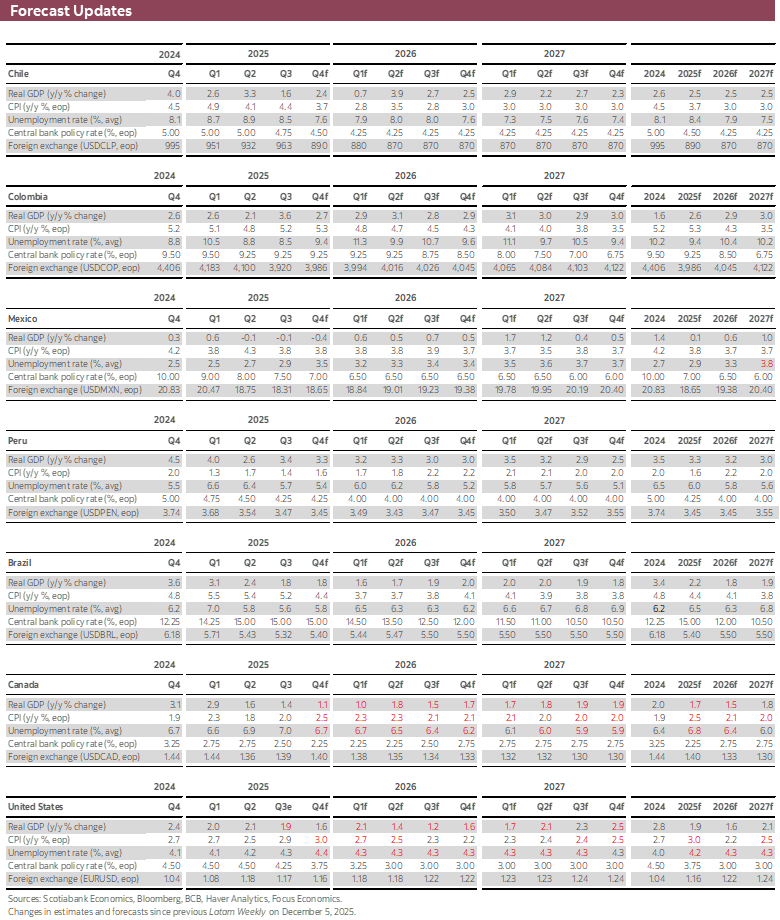

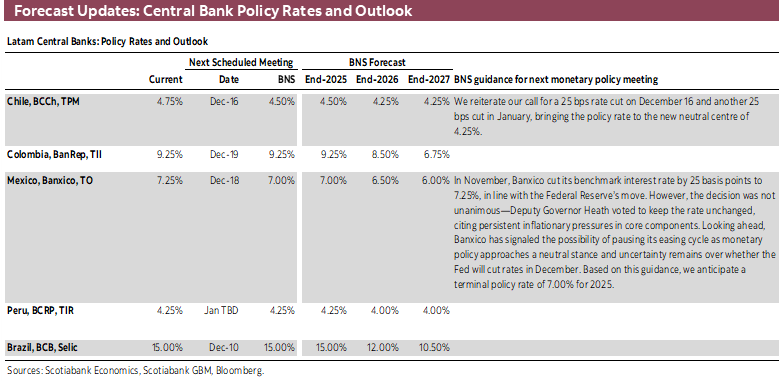

On the monetary policy front, Chile’s central bank is expected to announce a 25bps rate cut at its announcement on Tuesday, to be followed on Wednesday by the Monetary Policy Report where the focus will be on the implied BCCh rate path. As of today’s close, markets were pricing in 21bps in implied cuts for next week’s decision (or about ab 80% chance), while us and all nine economists polled by Bloomberg expect a quarter-point cut; 85% of those polled by the BCCh earlier this week expect a 25bps rate cut, too. As for the path ahead, our team anticipates that the central bank will lower its policy rate by 25bps one final time in 1Q26 to 4.25%, a scenario to which markets are only assigning about toss-up odds of occurring over the course of 2026, but about 90% of economists polled by the BCCh think the bank will cut at least once by year-end (~60% at 4.25% and ~30% at 4.00%). Here, the BCCh’s estimates for the policy rate path as well as its views on inflationary risks and the economy, all found within the MPR, will be key.

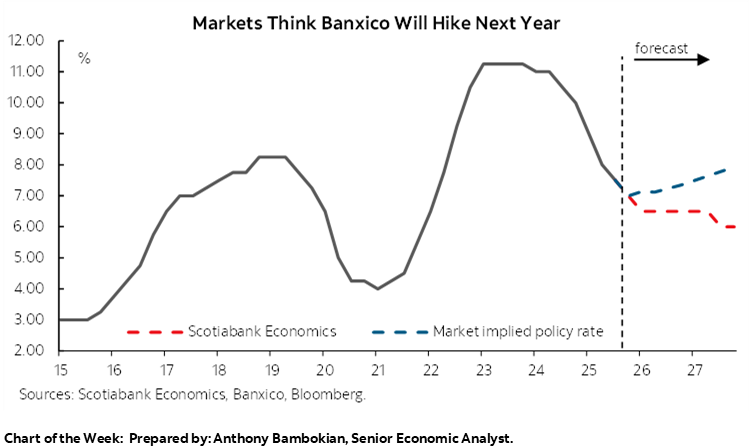

Banxico is also expected to announce a 25bps reduction to its overnight rate at its Thursday announcement, but doubts have grown over whether Mexican officials will announce additional easing next year – and markets are even leaning in favour of rate hikes. As our team outlines in today’s Weekly, recent upside surprises in inflation suggest that Banxico should take a more cautious stance on easing, following months of shrugging off these upside risks as temporary and now due to be compounded by a 13% minimum wage hike, as well as tariff hikes on imports (namely from Asia) and tax increases on soft drinks and tobacco.

Pending Banxico’s rate announcement, we’ve kept our forecast for two more rate cuts to 6.00% in 2026, but this has always been more of a “what we think they will do” rather than “what we think they should do” forecast. Recent developments strongly suggest that Banxico should err in favour of what they should do and more seriously consider a lengthy rate hold or a more data-dependent and cautious stance. Additional rate cuts increase the odds of a policy mistake where the Board is forced to do a u-turn and lift its overnight rate. The latter seems to be the view of markets that think Banxico could hike by about 50bps over 3Q and 4Q26.

We will be looking for changes to the bank’s statement that more clearly tee up a pause in rate cuts after a would-be twelfth consecutive reduction next week. There are also decent odds that the Board is split 3–2 in its decision to cut by 25bps next week, with another voter joining Heath in his preference for no change as he has done so for the last four meetings. On Monday and Wednesday Banxico and Citi surveys, respectively, will show how much the view of economists has changed in recent weeks amid inflation overshoots, with the median economist in both polls eyeing a 6.50% level for the overnight rate at end-2026. Domestic development aside, markets and economists are also taking their cue from Federal Reserve rate expectations, with this week’s Fed decision also seeing Banxico cut bets retreat slightly. In turn, Tuesday’s U.S. nonfarm payrolls and Thursday’s CPI releases could also shape Mexican rates markets.

Brazil, Peru, and Colombia all publish economic activity readings for October next week, due on Monday from the first two and on Thursday from the latter. Brazil’s economy is forecast to have decelerated to around a ~0.5% y/y pace in October, correcting from the 2% expansion it recorded in September which was its strongest month since May; in seasonally-adjusted terms, the economy is estimated to have stagnated in October, though improving from a 0.2% decline in the prior month when the industrial sector dragged on activity.

The data may be of some relevance for the BCB, though the bank’s meeting minutes and MPR on Tuesday and Thursday, respectively, should be of greater importance for markets as these documents could shed some light on the possible timing of the BCB’s return to rate cuts; with about 70–75% odds assigned to a 25bps cut in January. Traders will also keep a closer eye on developments regarding a possible reduction of former President Bolsonaro’s prison sentence—which would influence the odds that his son Flavio bows out of a race against incumbent Lula for the presidency that he is on track to lose.

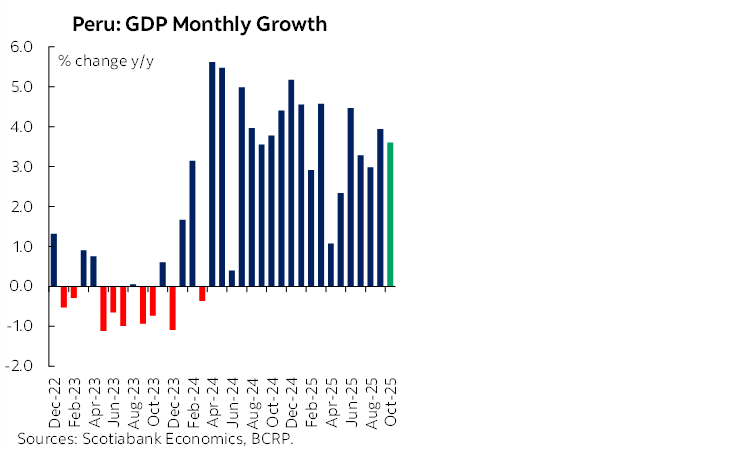

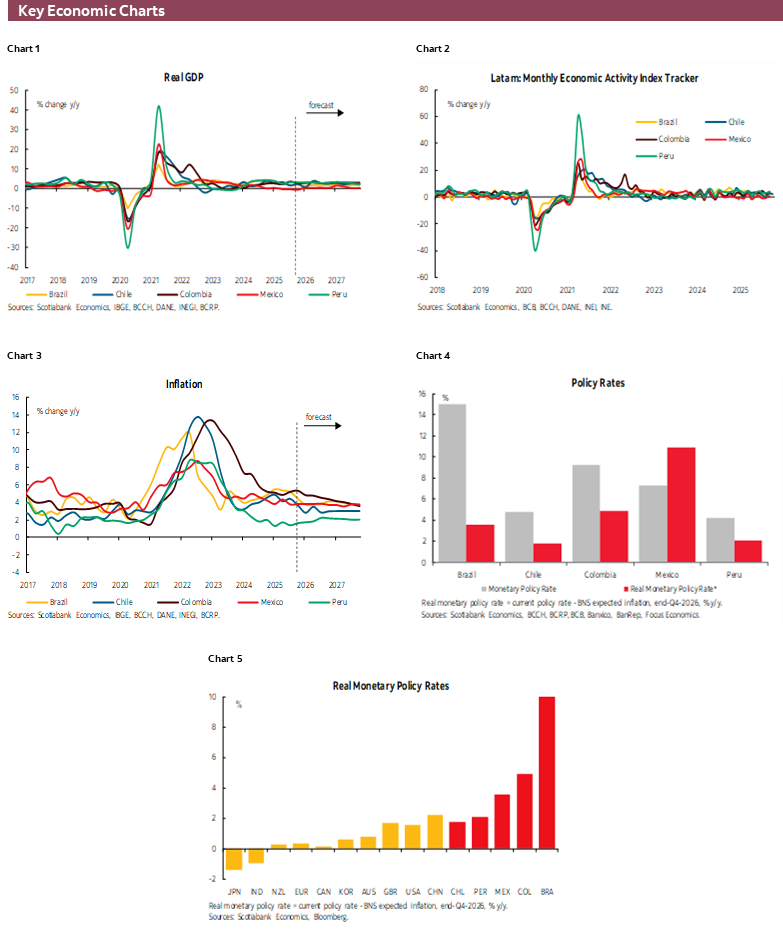

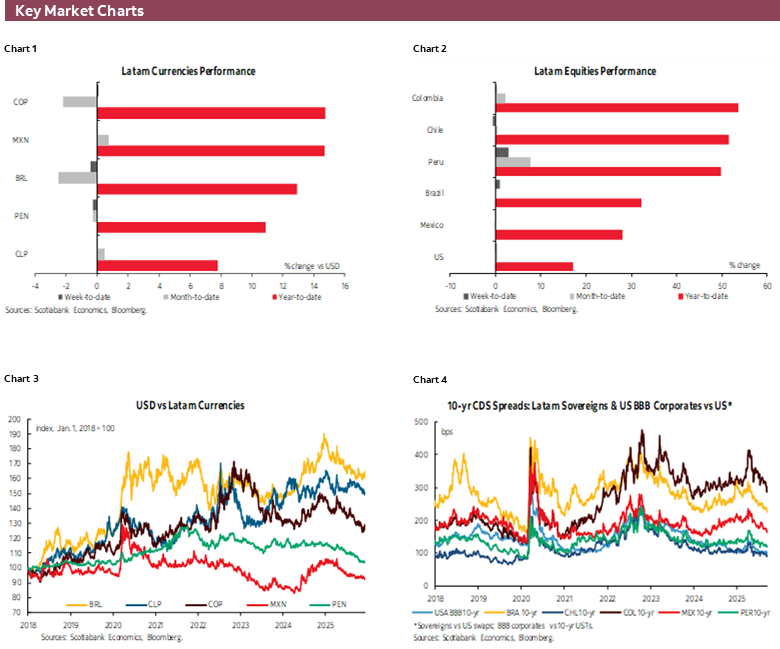

In today’s report, our economists in Lima discuss their expectations for next week’s October GDP, which they project expanded by a strong 3.6% y/y pace, decelerating somewhat from the 3.9% gain in September. Their tracking of key indicators shows that vehicle sales growth strengthened during the month while credit demand, cement sales (construction), and electricity consumption (industrial sector) held to similar rates of expansion as in September, although a contraction in public investment likely dented the overall y/y expansion in GDP in October. The team also highlights the continued improvement in economic expectations as per the BCRP’s surveys, with agents seemingly unfazed by uncertainty regarding the April 2026 elections. The latter has also not been a factor of obvious concern for the Peruvian sol, which is tracking a 10%+ gain for the year, prompting the direct intervention of the BCRP that may be seeking to establish a floor for the currency.

Finally, Colombia starts out the week with retail sales and industrial/manufacturing production data that will help economists refine their estimates for Thursday’s economic activity print for October. Overall, Colombia’s economy has had a solid year, with GDP forecast to have grown by around 3% in October, down from 4% in September, with retail spending and industrial activity expected to have cooled in y/y terms in October from the previous month’s strong showing. While headline economic figures are in a good spot, political and fiscal developments are not, with the failure of the government’s tax bill earlier this week and personnel moves at the financial regulator amid pressure from the government to repatriate pension investments overseas into Colombian assets.

On Friday, BanRep is expected to keep its overnight rate at 9.25% in a now classic divided vote where government appointees will likely vote for rate cuts against the majority preferring a hold. The biggest thing to watch will be the tone of the statement and Governor Villar’s comments in regard to the possibility of rate hikes. This discussion may be heavily influenced by a decision on 2026’s minimum wage hike that could come early next week, where an increase closer to 15% than 10% would certainly increase the possibility that BanRep considers hikes.

PACIFIC ALLIANCE COUNTRY UPDATES

Mexico—Banxico’s Curtain Call: One More Move

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

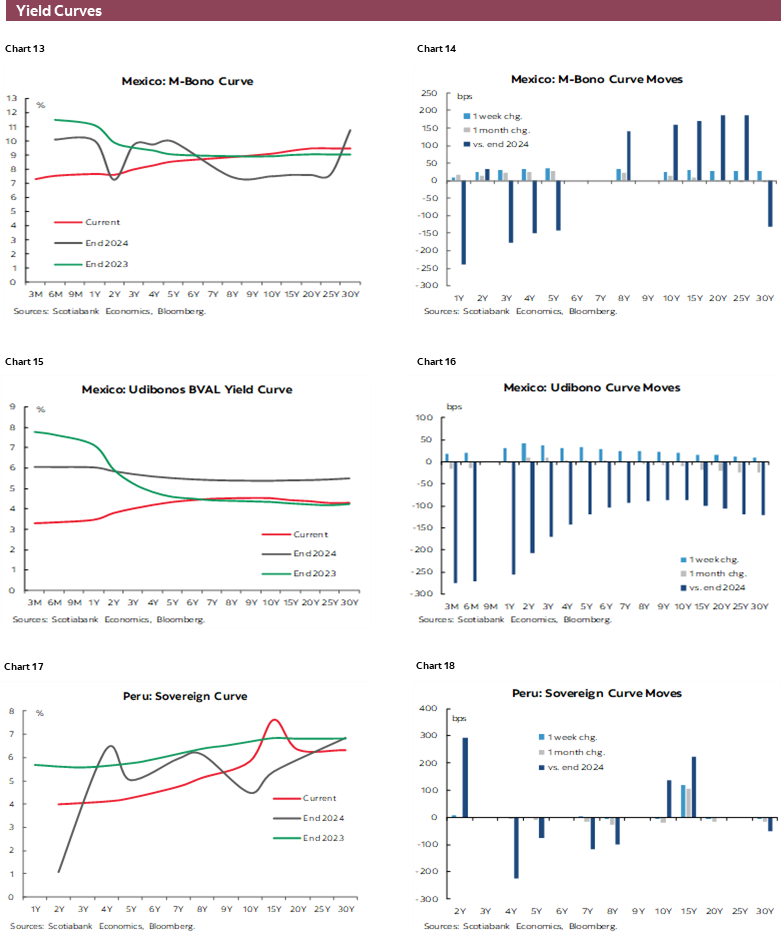

This week, the focus was on two key events that could shape Banxico’s final monetary policy decision of the year and signal its likely path in 2026.

The first was Mexico’s November inflation report; the second, the Federal Reserve’s policy decision. While neither development is expected to alter Banxico’s decision next week, they could strengthen the case for ending the easing cycle in the first quarter of next year.

November inflation surprised to the upside: headline inflation reached 3.80% year-on-year and core inflation 4.43%, both above October’s figures (3.57% and 4.28%) and analysts’ forecasts (3.70% and 4.33%). The increase was driven mainly by goods and services, which have persistently exceeded the 3% ±1% target range. The non-core component also rose, though it remains below 2.0%. Despite these pressures, Banxico is still expected to cut its policy rate next week. However, the inflation data could weigh on expectations, limiting the scope for further easing.

The second event was the Fed’s decision. With a 25 basis point cut in the federal funds target range, Banxico is likely to follow suit to preserve relative monetary positioning and take advantage of the recent peso appreciation, which provides room for additional cuts. However, projections released alongside the decision suggest the Fed expects only one more 25 basis point cut in 2026 and another in 2027. This outlook could constrain Banxico’s ability to lower rates without further narrowing the interest rate differential, which is already near historic lows.

In sum, this week’s developments raise questions about the sustainability of Mexico’s rate-cutting cycle in 2026, particularly as inflation expectations remain anchored at the upper end of the tolerance range and the monetary stance is already considered neutral.

Peru—Economic Momentum Persists: Solid Growth and Optimistic Expectations Ahead of Elections

Ricardo Avila, Senior Analyst

ricardo.avila@scotiabank.com.pe

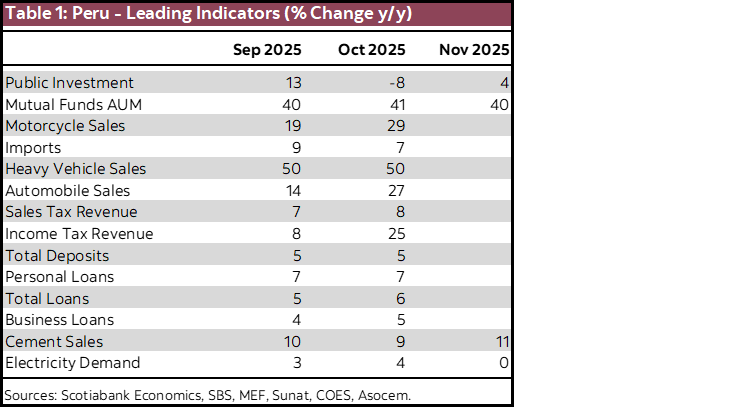

The economy continues to advance at a solid pace. Our key indicators for October are very similar to those of September (table 1), showing strong growth in vehicle sales and savings through mutual funds, sustained recovery in the financial system (loans and deposits), and moderate growth in indicators more closely correlated with economic activity, such as electricity consumption and cement sales, with the exception of public investment, which tends to exhibit significant volatility. For November, some data have already begun to be published, and we can once again anticipate an improvement in economic activity.

This fortnight, the economic activity data for October will be released. We estimate growth will be around 3.6% (chart 1), in line with the 3.3% we expect for Q4 2025. By economic sector, some official figures have already been published, such as the agricultural sector, which grew 1.9% year-on-year; the fishing sector, which posted strong growth of 25.7%; and hydrocarbons, which recorded growth of 4.2%.

An important topic is the General Elections scheduled for April 12th of next year. Despite the latest presidential voting intention survey conducted by IPSOS showing that around 48% of the population has yet to decide whom to vote for, at the moment we do not see any concern among economic agents.

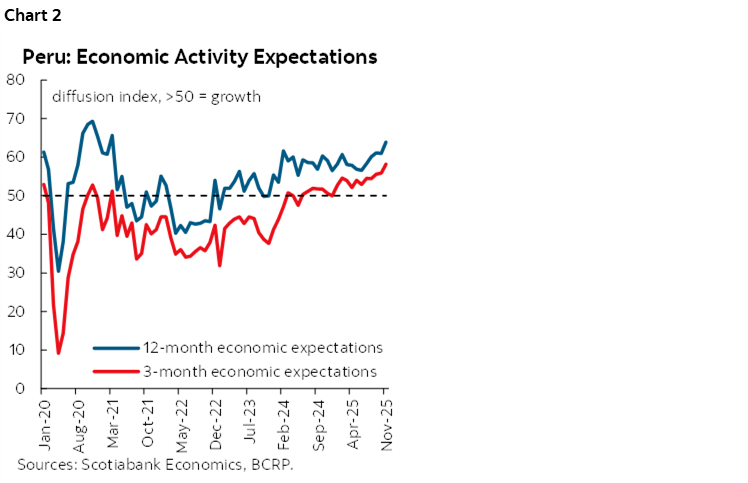

On one hand, on December 4th, the Central Reserve Bank published the results of its Macroeconomic Expectations Survey, reaffirming economic agents’ perception of a solid economy (chart 2). Economic expectations have remained in the optimistic range and have continued to improve, with 12-month expectations reaching their highest level in four and a half years (since April 2021) and 3-month expectations at their highest level in six and a half years (since March 2019).

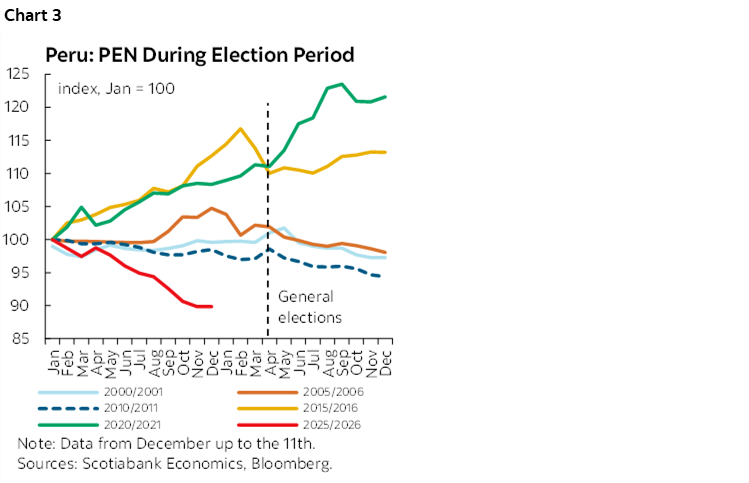

On the other hand, the strength of the sol (chart 3), which has appreciated by around 12% during the year, has shown no signs that the market is concerned about the development of the General Elections. Metal prices have a greater influence on the exchange rate, prompting the Central Bank to intervene in the spot market with purchases of USD 855 million in one month (from November 5th to December 4th), establishing a possible floor at 3.36 soles per dollar. As shown in the chart, the sol is exhibiting a very different dynamic compared to other electoral periods.

From our perspective, we had already anticipated a relatively calm electoral process. Our baseline scenario assumes the new government will maintain an investment-friendly stance and continue responsible macroeconomic policies.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.