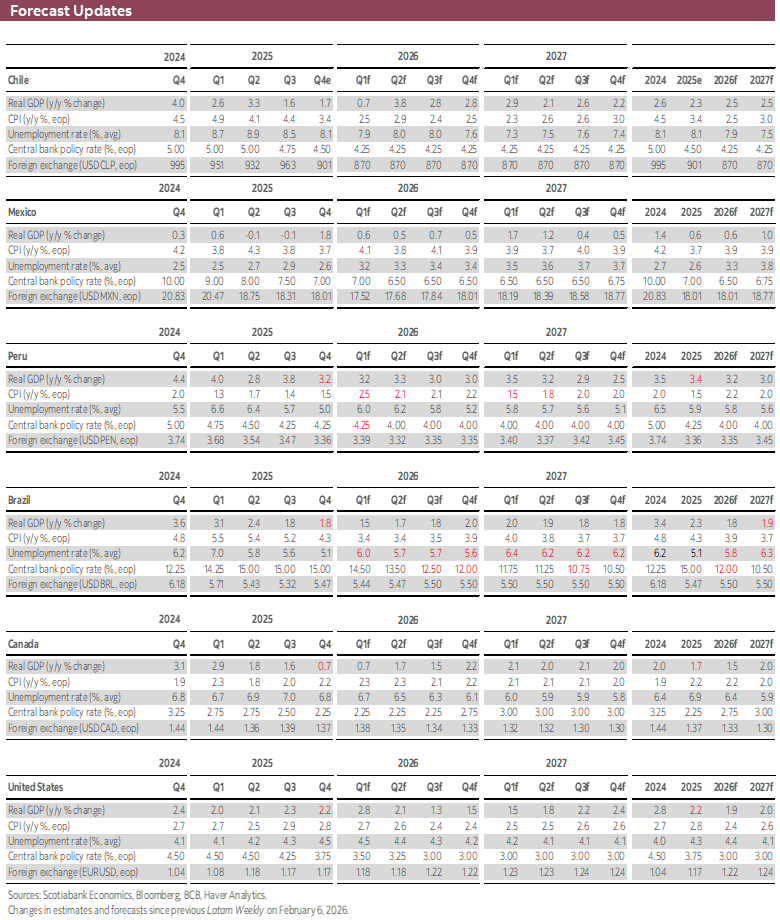

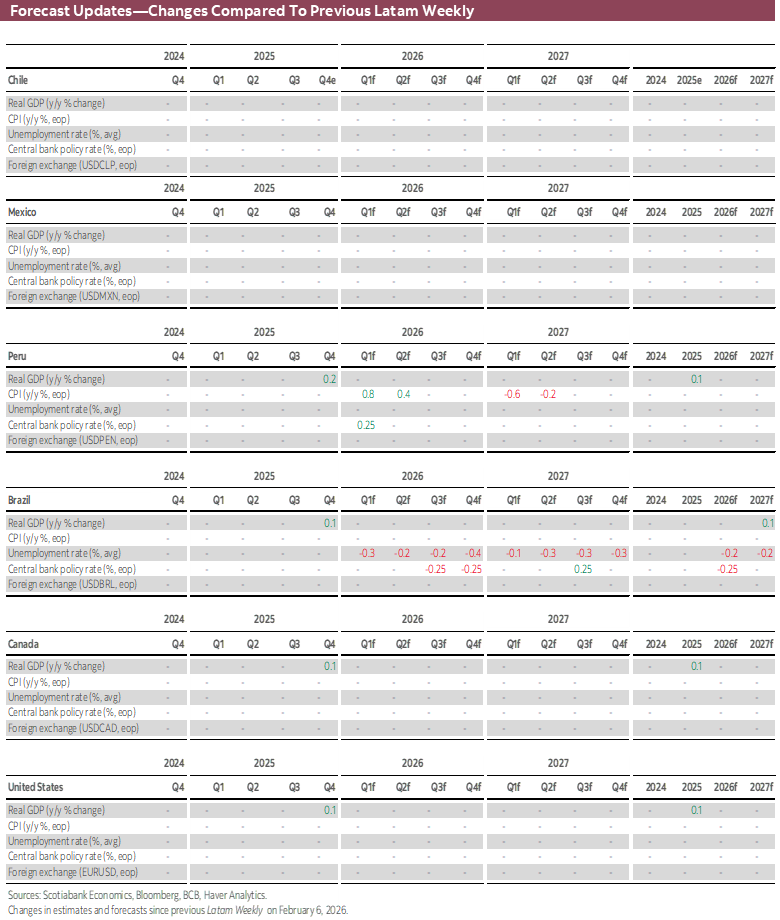

HIGHLIGHTS

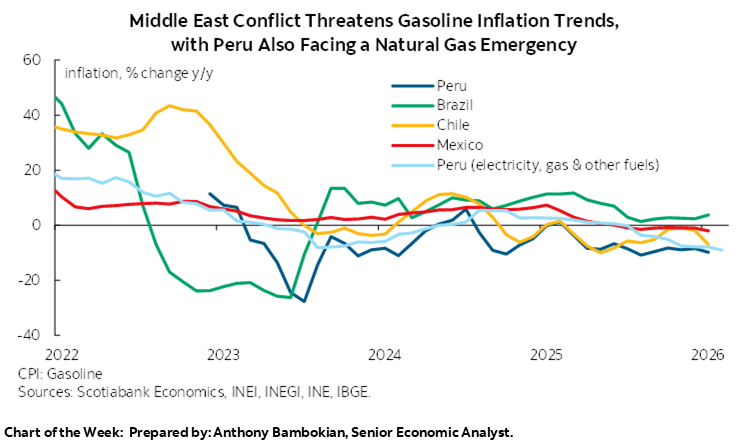

- Inflation readings from a handful of key economies are in the data spotlight next week, but a sharp rise in energy prices over the past week amid the conflict in the Middle East means the data corresponds to a different reality.

- Peru is also dealing with the unfortunate suspension of a key gas pipeline due to leaks, just as concerns grow over a developing El Niño which is our team’s topic of discussion in today’s report. In light of inflation risks, the BCRP will stay put at next week’s rate decision.

- Mexican and Brazilian full-month inflation data should come and go, with local traders trimming rate cut expectations from Banxico and the BCB. As our economists discuss today, Mexico may be a large producer of crude oil but it is highly dependent on international energy supplies, thus leaving domestic inflation at risk of global prices.

- Chile’s latest inflation print and soft economic readings may have backed a March rate cut, but external developments favour a cautious stance. Kast takes over the presidency on Wednesday, with local markets awaiting the rollout of pro-business policies.

Chart of the Week

(STALE) GLOBAL INFLATION

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Inflation readings from a handful of key economies are in the data spotlight next week, but a sharp rise in energy prices over the past week amid the conflict in the Middle East means the data corresponds to a different reality.

- Peru is also dealing with the unfortunate suspension of a key gas pipeline due to leaks, just as concerns grow over a developing El Niño which is our team’s topic of discussion in today’s report. In light of inflation risks, the BCRP will stay put at next week’s rate decision.

- Mexican and Brazilian full-month inflation data should come and go, with local traders trimming rate cut expectations from Banxico and the BCB. As our economists discuss today, Mexico may be a large producer of crude oil but it is highly dependent on international energy supplies, thus leaving domestic inflation at risk of global prices.

- Chile’s latest inflation print and soft economic readings may have backed a March rate cut, but external developments favour a cautious stance. Kast takes over the presidency on Wednesday, with local markets awaiting the rollout of pro-business policies.

Inflation readings from around some of the world’s key economies are in the data spotlight next week, but one may as well pay only limited attention to the figures. Military strikes in the Middle East that began last weekend are showing no signs of letting-up, with tanker transit in the Strait of Hormuz virtually offline—locking in the transportation of about a fifth of global oil and gas flows.

Brent oil prices have risen by a third since last Friday’s close (50%+ in the year-to-date) and European natural gas prices have jumped by two-thirds (80%+ in the year-to-date). The latter is not a massive risk for the American continent thanks to within-continent supplies, or more-diversified sources, while U.S. natural gas prices are up a more modest 10–15% since Friday and flat in the year-to-date.

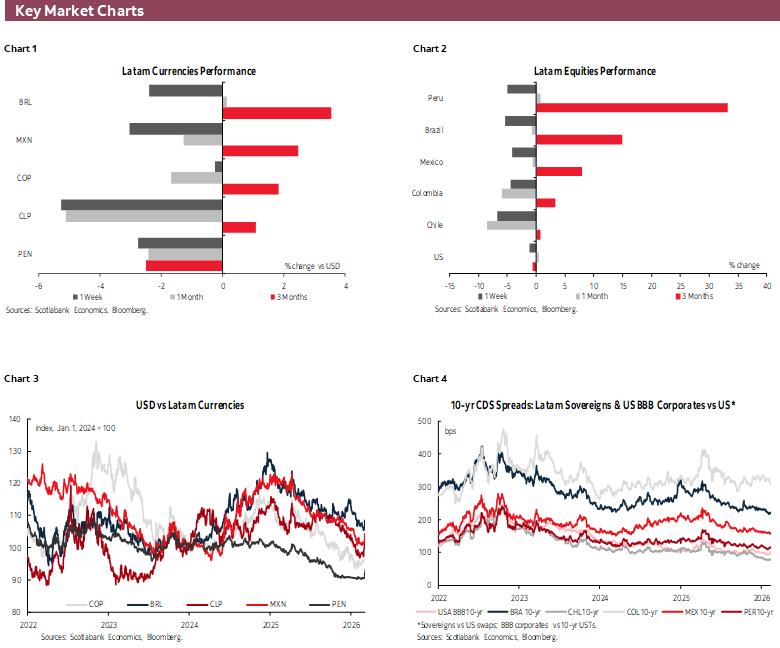

However, the hemisphere will not be able to avoid the knock-on effects of international oil prices on domestic gasoline prices which are lining up to deliver inflationary pressures that will not be captured in next week’s February data. Risk-off sentiment has also acted against Latam currencies, which are down from 0.5% for the COP to ~3–4% for the BRL, MXN, PEN and CLP for the week.

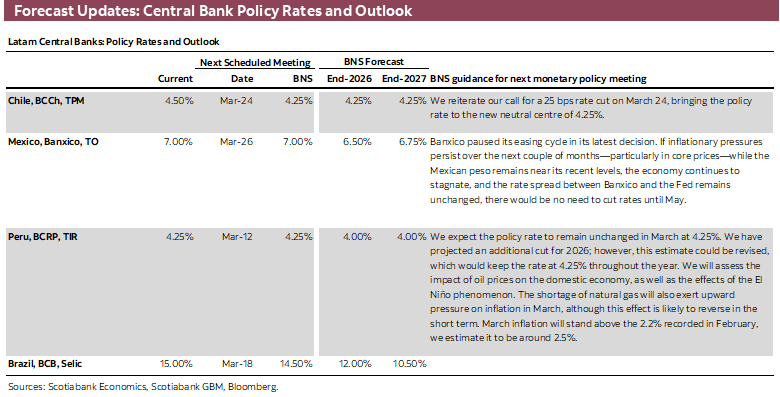

Peru is also dealing with the unfortunate timing of a key gas pipeline leak whose shipments (practically all of Peru’s natural gas supply) have now been suspended, leaving national supply at less than 10% capacity. To boot, the severity of El Niño, which our economists discuss in today’s report, stands as a possible risk for the local economy and inflation. The BCRP’s decision on Thursday should see no shift in policy rates, with the focus squarely on the assessment of risks.

Inflation data from Mexico, Brazil, U.S. (CPI and PCE), China, and Norway due over the coming week will be but a reflection of conditions prior to this large energy shock of to-be-determined duration. Were the conflict to reach a resolution over the next few weeks, February inflation readings could be relied on to gauge the ‘rough’ state of inflationary trends, but it is anyone’s guess how long it will last (seemingly at least a few weeks) and how quickly energy flows will return to normalcy, or whether this energy spike can have lasting second-round effects on prices and inflation expectations.

Under elevated geopolitical and energy prices uncertainty, the response from central banks in Latam and elsewhere will likely one of staying put or scaling back moves until a clearer analysis can be made.

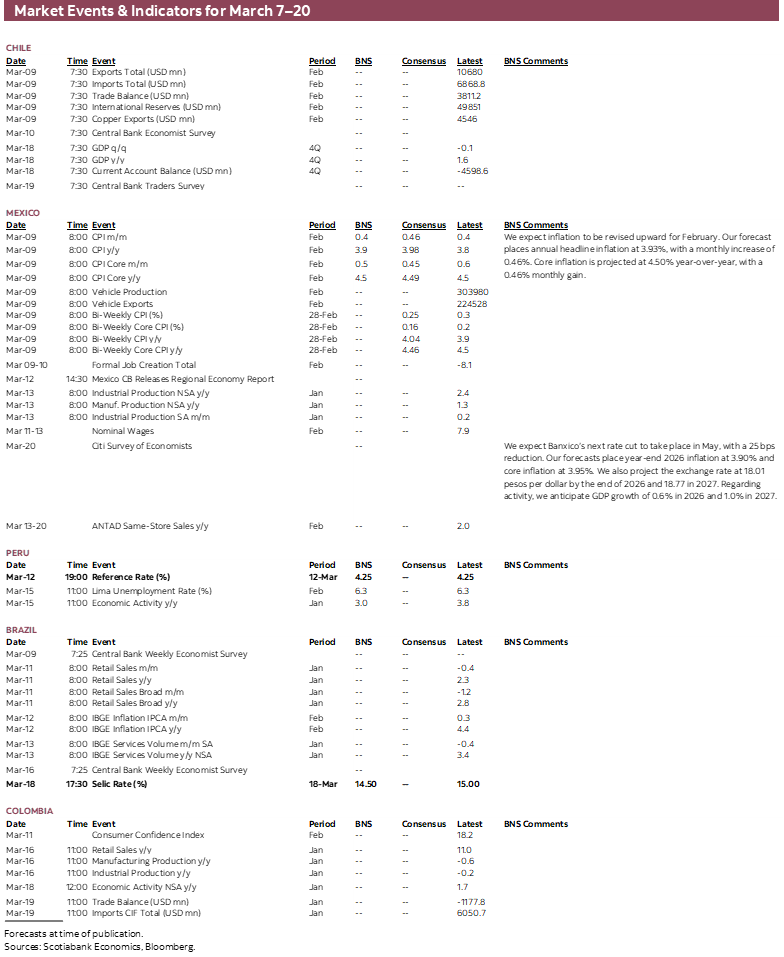

This means that Banxico will probably sit back at its late-March meeting (which was our expectation even prior to the weekend’s events) and possibly a few more meetings beyond depending on how the situation evolves; at writing, markets are assigning ~15% odds of a quarter-point cut on the 26th. Monday’s February CPI, seen at 4% and 4.5% in headline and core terms, respectively, in line with mid-month readings will come and go for markets. Our economists in Mexico go over where the country stands in regard to the latest international developments.

Aside from news from the Middle East, there may also be some focus on the lead-up to the formal start of the USMCA review on March 16th and, on a related note, Banxico’s quarterly report on regional economies out on Thursday may have some colour on how firms are dealing with trade uncertainty.

Most Brazilian traders have also abandoned expectations for a half-point cut by the BCB on the 18th, with 30–35bps priced in compared to 45–50bps last Friday. Like Mexico, the February IPCA release out on Thursday will be of lesser importance for market participants, as will retail sales and services volumes figures out over the week—even if they confirm economic sluggishness in the country. It’s not just near-term expectations that have shifted in just a few days. At end-February, traders saw ~275bps in total BCB cuts by year-end. Today, they see about 75bps less.

In Chile, as our team wrote this morning, recent inflation and economic data would be supportive of a 25bps cut on the 24th, but the external backdrop of higher energy prices and currency weakness have all but zeroed out cut odds, as the BCCh will probably opt for patience and monitoring. We’ll see how economists have adjusted their policy and economic expectations in the results to the BCCh’s survey on Tuesday. José Antonio Kast also takes over the presidency on the 11th, with markets and economists set to keep a close eye on his first few weeks to roll out transformative pro-business policies, and how he may deal with a possible international energy crisis.

Finally, the result of Sunday’s legislative elections in Colombia will be the main topic of discussion at the Monday open, with a strong performance for candidates from the left adding to concerns in markets of rising odds that Cepeda takes the presidency at the end-May vote (with a second round on June 21st). The balance of Congress between the right, independents, and the left following Sunday’s vote could also check the reach of Colombia’s next president once their term begins in August. Data-wise, retail sales and industrial production figures out at the start of the week will be a secondary influence on markets that will focus on election results, geopolitical developments, and this afternoon’s February CPI release.

COUNTRY UPDATES

Mexico—Amid the Middle East Geopolitical Shock: Production, Energy Deficit, and Macroeconomic Implications

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

Mexico maintains a relevant but limited presence in the international oil market. National production reached 1.64 mb/d in November 2025 and 1.40 mb/d in December under the extended OPEC+ framework, equivalent to around 3.2% of the bloc’s supply. This participation contrasts with that of the main producers—Saudi Arabia and Russia, both above 9.5 mb/d, and Iraq, the United Arab Emirates, and Iran, between 3.4 and 4.3 mb/d—highlighting Mexico’s position as a medium-scale producer in the global context. Nevertheless, the country’s energy structure is characterized by a persistent deficit: Mexico imports roughly 1.20 mb/d of crude oil, in addition to large volumes of gasoline, diesel, and natural gas. This structural component of the energy balance increases its vulnerability to external shocks and is already reflected in the trade balance, which posted a deficit of 6.48 billion dollars in January 2026.

The recent conflict involving Iran, the U.S., and Israel has heightened these risks. The Strait of Hormuz—through which roughly one-fifth of global crude oil and liquefied natural gas supply flows—has faced de facto disruptions in ship traffic following attacks on vessels in the region. In response, international prices have surged: Brent has accumulated an increase of about 50% so far this year. For Mexico, a prolonged blockage of Hormuz traffic would imply increases in the cost of crude and refined-product imports, additional pressure on logistics and on the margins of Pemex and private operators, and greater risks of inflation pass-through—especially if not mitigated through fiscal policy.

Additionally, the Mexican peso exhibited the typical behaviour seen in global risk-off environments: on March 3rd it fell 2.3% to 17.70 pesos per dollar, its worst session since April 2025. Since mid-February, the exchange rate has moved from around 17.15 to around 17.80 at writing , accompanied by a rebound in one-month implied volatility. A sustained depreciation tends to amplify the cost of imported energy and puts upward pressure on inflation through fuel prices, road transport, and logistics chains.

Regarding domestic prices, Mexico had faced a relatively benign environment through January. Headline inflation stood at 3.79% year-on-year, and energy inflation—previously a significant source of pressure in 2023—showed a sharp correction, falling from 3.50% in May 2025 to −1.16% in January 2026. However, the recent increase in oil and gasoline prices could reverse this trend, raising the risk of second-round effects in key inputs such as transportation, food, and manufacturing, especially given that gasoline carries a 5.32% weight in the CPI. At this point, fiscal policy plays a central role: Mexico’s excise tax on gasoline (IEPS), determined as the difference between the final price and the producer price, provides room to smooth impacts. Currently, the tax sets rates of 6.70 pesos per litre for lower-octane gasoline, 5.66 pesos for higher-octane gasoline, and 7.36 pesos per litre for diesel. A temporary reduction in these rates could contain inflationary pressures, though at the cost of increased fiscal commitments.

In sum, Mexico combines meaningful oil production with a high dependence on imports of light crude, gasoline, and natural gas—raising its exposure to global disruptions such as the current one. The conflict in the Middle East increases the probability of higher energy inflation, exchange-rate pressure, and a widening external deficit. To mitigate these risks, the economic policy agenda should focus on: (i) countercyclical and prudent use of IEPS; (ii) active management of inventories and supply contracts; (iii) clear communication by Banxico to anchor expectations amid possible temporary price spikes; and (iv) the promotion of infrastructure, logistics, and refining projects that reduce structural import dependence without compromising fiscal sustainability.

Peru—El Niño in Peru: Implications and Impacts

Pablo Nano, Deputy Head Economist

pablo.nano@scotiabank.com.pe

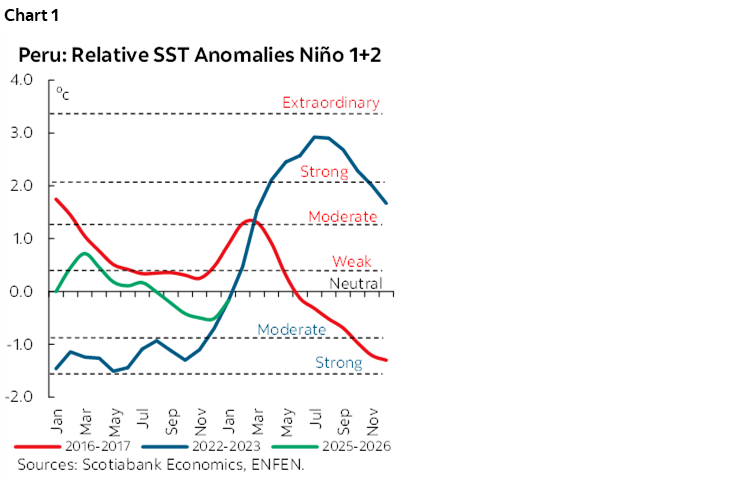

In recent weeks, concerns have increased regarding the development of an El Niño phenomenon (FEN) off the coast of Peru. According to the February 27th, 2026, statement from the multisectoral commission in charge of the National Study of the El Niño Phenomenon (ENFEN), a Coastal El Niño is developing and is expected to last until November (chart 1).

El Niño events are typically characterized by an increase in sea surface temperature (SST), which generates above-average rainfall along the Peruvian coast (Niño 1+2), particularly in the north of the country (Tumbes, Piura, and to a lesser extent, Lambayeque and La Libertad). However, not all El Niño events are the same, and their impacts on infrastructure and economic activity depend on the onset date, the intensity of the sea surface warming, and the duration of the climatic event.

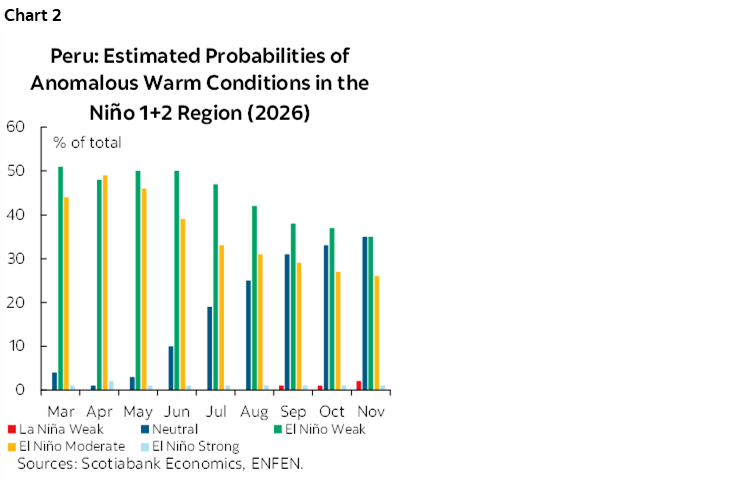

The current El Niño event began in March, unlike the 2017 El Niño, which began in January of that year (chart 2). This distinction is relevant because Peru’s rainy season typically runs between December and March; consequently, the fact that the current El Niño event is starting in March—when the rainy season usually ends—may potentially have a less damaging effect on road infrastructure (highways, bridges, etc.). According to ENFEN, warm environmental conditions of a “weak” magnitude—defined as a sea surface temperature (SST) increase between 0.5°C and 1.3°C—are most likely during most of the event, potentially reaching a “moderate” magnitude—SST increase of between 1.3°C and 2.1°C—before July.

The magnitude of the economic impact will largely depend on the intensity and duration of the weather event. It’s worth noting that a “weak” El Niño event usually doesn’t cause significant damage to road infrastructure, allowing most economic activity to continue normally. By contrast, a “moderate” event could generate infrastructure damage and logistical disruptions, particularly in affected northern regions. Transport constraints could limit the usual flow of goods to and from these areas, with potential negative effects on both GDP and inflation, especially if supply chains are temporarily disrupted.

In the case of the fishing sector, a “weak” El Niño event would not have major effects on anchovy biomass, considering previous events of similar intensity. A “moderate” El Niño, however, could lead anchovy schools to move deeper into the water or southward in search of cooler waters—their natural habitat—making them more difficult to catch. Likewise, the rate of ocean warming will determine whether the potential impact—which would be reflected in a lower catch quota—occurs during the first fishing season (April to July) or the second (November to January). This would be partially offset by the greater availability of warm-water species—such as mahi-mahi, bonito, jack mackerel, and tuna—which would benefit fishing for Direct Human Consumption (DHC). Finally, it is worth noting that anchovy has proven to be a resilient species, recovering quickly after climatic events like El Niño.

Regarding the agricultural sector, a “moderate” El Niño event would have varying impacts across crops and regions. Crops located along the coast—where agricultural exports predominate—would be affected differently depending on the location of the valleys, with greater difficulties expected in the far north (Tumbes and Piura). Currently, the developing El Niño event is coastal, therefore droughts are not necessarily expected in the highlands—where crops for the domestic market predominate—as in past episodes when El Niño was global. In Piura, one of the most important crops is mango, whose harvest season largely concluded between December and February. Meanwhile, avocado harvesting is about to begin, and so far, no major impacts have been reported in Lambayeque and La Libertad. If above-normal temperatures persist, crop yields for products such as blueberries, citrus fruits, and olives could be affected. However, the major agricultural companies have invested in drainage systems to limit the potential damage from heavy rains.

If the El Niño episode is prolonged, it could affect the yields of the 2026/2027 growing season for crops such as blueberries, avocados, grapes, and asparagus, among others. However, lower production and, consequently, lower export volumes would not necessarily mean lower income for agricultural exporters, as they could benefit from higher prices, as occurred in 2023. On the other hand, above-average rainfall would allow for greater than normal water storage, which would benefit the 2025/2026 growing season for crops in coastal valleys with regulated irrigation, as well as for areas irrigated by wells due to aquifer recharge.

Other potentially affected sectors include tourism and the textile and apparel industry. In the case of tourism, above-average rainfall in the far north of the country (Tumbes and Piura) could damage hotel infrastructure located in beach areas—such as that seen in Máncora (Piura)—as well as reduce tourist traffic. These regions are popular destinations for domestic tourism during the summer season, both in March and during the Easter holidays (early April). Regarding the textile and apparel industry, a warmer-than-normal autumn and winter would reduce sales of warmer garments, which have a higher unit price compared to lighter garments that are in higher demand during El Niño events. This could lead to an unwanted accumulation of winter clothing inventories, although anticipating the arrival of the weather event could mitigate this risk.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.