- Chile: February CPI at 0% m/m (2.4% y/y) would have supported another policy rate cut, but external conditions are currently limiting the BCCh’s room

February’s CPI printed at 0% m/m (2.4% y/y), a positive development for consumers and the Central Bank, coming in at the lower end of expectations and slightly below our own forecast (+0.10%). Although core inflation (excluding volatiles) matched our projection, its monthly variation was the lowest for a February in the past five years, largely due to flat core goods inflation following January’s sharp increase. This print clearly surprises the Central Bank’s December Monetary Policy Report (IPoM) scenario to the downside. That said, inflationary risks from the global environment remain significant and could inject volatility throughout the first half of the year—mainly via higher fuel prices.

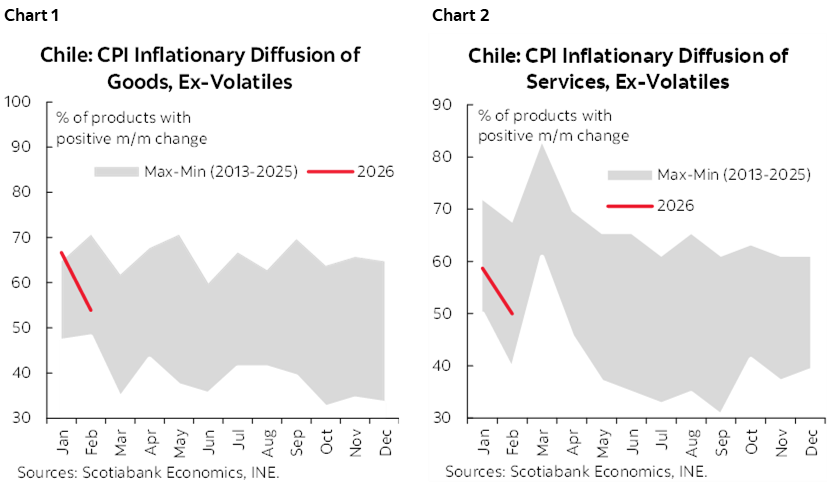

February’s flat inflation was driven by declines in volatile components (electricity tariffs and fuels) combined with historically low core inflation. Relative to our forecast, we saw no surprises in core goods or core services; however, some volatile services posted larger-than-expected declines, such as common expenses, lodging, and insurance. For the latter, we estimate the drop reflects discounts and promotional pricing in auto insurance, likely associated with the lower incidence of violent vehicle theft reported by the Public Prosecutor’s Office in 2025. Diffusion indicators behaved broadly in line with expectations (charts 1 and 2), with a reversal in goods inflation after January’s spike and a normalization in services, which have been hovering around their recent averages for several months.

From a domestic standpoint, the backdrop was set for the Central Bank to deliver a 25 bps rate cut after this CPI print. For this month’s Monetary Policy Meeting, the key inputs were: a labour market showing counter-seasonal weakness, decelerating real wages, a CLP that had experienced significant multilateral appreciation until last week, a February CPI that slightly surprised on the downside with a flat monthly print, and activity data revealing softness in commerce despite improving confidence indicators. However, the global environment has shifted abruptly. The CLP’s appreciation has reversed sharply, and external conditions have turned more complex as higher oil prices and some increases in transportation costs revive concerns about a global supply-side shock. Given that the policy rate is already close to the midpoint of the neutral range (4.25%), we believe that the option of waiting is increasingly becoming the most likely scenario—unless global risks ease meaningfully in the very near term.

—Aníbal Alarcón

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.