HIGHLIGHTS

- Middle East conflict developments will remain the leading driver of market moves next week as involved parties enter into negotiations, the prospect of which has already helped global equities, bonds, and commodity prices retrace some of the moves since the breakout of the conflict in late-February.

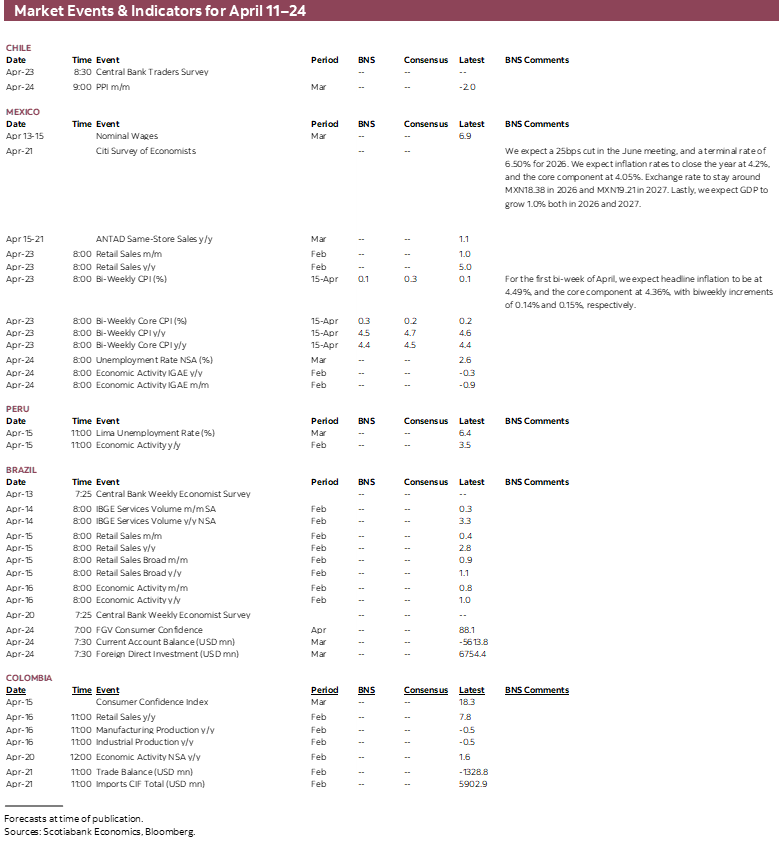

- The data calendar has mostly backward-looking figures, with U.S. PPI and Chinese GDP standing as the highlights outside of Latam, while Peruvian and Brazilian economic activity are the regional (stale) standouts. Mexican and Chilean markets have little on offer.

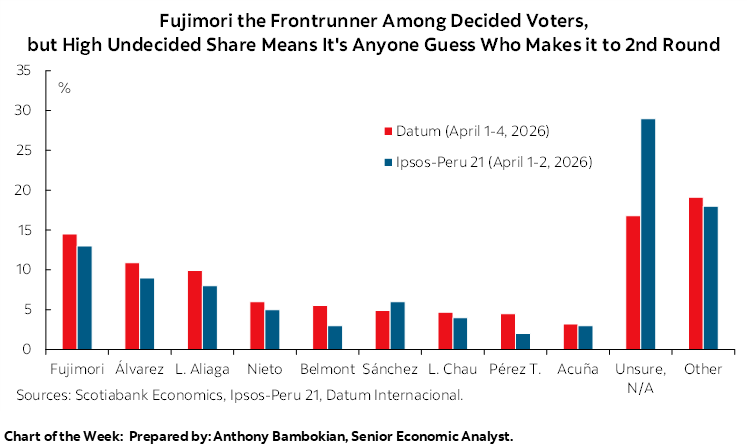

- Peru’s presidential and legislative election on Sunday is the main event in Latam, with polls leaving the race wide open in terms of which two candidates will make it to a near-certain second round vote in June. As per the latest polls, three candidates from the right-wing spectrum enjoy the best odds of making it to the head-to-head contest.

- In today’s Weekly, the team in Mexico goes over recent economic data, with an overall weak read of the economy clashing with the MinFin’s very optimistic view—upon which its latest fiscal estimates are conditioned.

Chart of the Week

PERU’S FIRST ROUND VOTE, ‘QUIET’ WEEK AHEAD

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Middle East conflict developments will remain the leading driver of market moves next week as involved parties enter into negotiations, the prospect of which has already helped global equities, bonds, and commodity prices retrace some of the moves since the breakout of the conflict in late-February.

- The data calendar has mostly backward-looking figures, with U.S. PPI and Chinese GDP standing as the highlights outside of Latam, while Peruvian and Brazilian economic activity are the regional (stale) standouts. Mexican and Chilean markets have little on offer.

- Peru’s presidential and legislative election on Sunday is the main event in Latam, with polls leaving the race wide open in terms of which two candidates will make it to a near-certain second round vote in June. As per the latest polls, three candidates from the right-wing spectrum enjoy the best odds of making it to the head-to-head contest.

- In today’s Weekly, the team in Mexico goes over recent economic data, with an overall weak read of the economy clashing with the MinFin’s very optimistic view—upon which its latest fiscal estimates are conditioned.

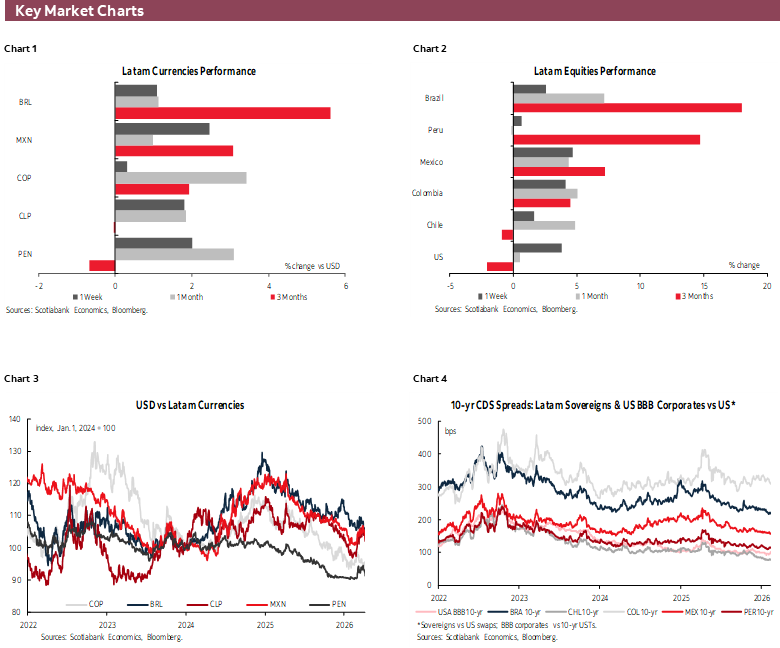

It’ll be more headlines casino for global markets next week that will track developments in Middle East ceasefire negotiations, with the announcement of these helping the S&P 500 to recover to only a ~2% loss from its all-time high on February 27th—coming back from as deep as a 9% peak-to-trough move on March 30th. The cautious optimism has helped Brent oil June futures to fall to around $95/bbl, down from their $110/bbl peak at the Monday close, but still sitting close to $25/bbl higher versus late-February.

While peace talks are a positive for risk sentiment and a negative for energy prices, the two sides are far apart in their demands. A partial reopening of the Strait of Hormuz may also not be sufficient to meet immediate global energy needs as countries and companies draw down reserves or at-sea oil. ‘Spot’ Northwest Europe crude oil continues to trade at $130–135/bbl (down from a ~$145/bbl peak), double its pre-conflict price, reflecting extremely tight immediate delivery supplies that risk fuel shortages in certain parts of the globe.

There won’t be much on the data front in Latam nor in the G10 to keep trading distracted from Middle East developments, especially for data that perceived as backward-looking. In Latam, Mexican and Chilean calendars are bare of data releases, with markets focusing on public policy regarding energy prices and possible comments by central bankers. Brazil has some stale February economic activity, retail sales, and industrial production data on tap that should not move the needle for traders.

Peru has the most exciting week in the region, opening to the results of Sunday’s vote (more below), also releasing February economic activity and March unemployment data on Wednesday, with another mid-3s expansion expected for the former (ahead of natural gas disruptions in March alongside would-be impacts of the Middle East conflict). Colombian retail and industrial production data for February should be but an afterthought for local markets that are keeping a closer eye on risks to BanRep’s April policy meeting. FinMin Avila withdrew from last month’s gathering and it is unclear whether he will join the late-April gathering.

The Latam highlight will be the result of Peru’s first round vote on Sunday, set to determine the two candidates that will make it to a runoff contest on June 7th. As the chart on the front page of this report shows, it’s a wide-open race with a high share of undecided voters that could deliver a surprising set of finalists. As per the latest polls, three right-wing candidates (across its spectrum) make up the podium for first round voting intentions. Don’t take away too much from who comes out on top from Sunday’s vote, however, as the split field leaves the contest open to alliances and ‘anti-votes’ campaigns forming ahead of June’s round. In a single round election, Peruvians will also vote on a new legislature, with a fractured vote breakdown bound to require congressional coalitions.

Outside of Latam, the highlights will be March Producer Prices Index from the U.S. on Wednesday (with a focus not just on direct fuel price shocks but also on how these are spreading to other prices charged), Chinese 1Q GDP on Thursday (though somewhat backward-looking), and U.K. February GDP that same day (even more stale, but could possibly scale back BoE hike bets). On Tuesday, the IMF will publish its quarterly World Economic Outlook, whose forecasts tend to lag those of private-sector economists, but the document may offer some interesting thoughts on the possible impact of the ongoing energy and fertilizers supply shock.

COUNTRY UPDATES

Mexico—Latest Figures Do Not Support the Ministry of Finance’s Most Recent Estimates

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

Economic data released this week reinforce the view that the Mexican economy is undergoing a period of deeper and more persistent weakness than assumed in the central scenario outlined by the Ministry of Finance (SHCP) in the 2027 Economic Policy Pre-Criteria. Taken together, the data on activity, domestic demand, confidence, inflation, and the external sector do not validate the narrative of a gradual acceleration in growth, an orderly convergence of inflation, or a comfortable path toward monetary easing.

On the activity front, the Global Indicator of Economic Activity (IGAE) for January showed a significant contraction, reversing a large part of the gains observed in the final quarter of 2025 and placing the level of activity once again at levels comparable to mid-last year. This reading confirms that the economy entered 2026 with notably weak momentum, inconsistent with a growth trajectory that would quickly converge toward its potential. Along the same lines, gross fixed investment in January posted a broad-based and significant decline, extending its streak to 17 consecutive months of annual contractions. The machinery and equipment component was the most affected, suggesting that capital formation remains one of the main structural drags on growth. Investment not only remains negative, but it also shows no clear signs of a turning point, amid an environment marked by both global and domestic uncertainty, as well as trade tensions and still-elevated financing costs.

Consistent with the above, the performance of private consumption in January also fails to support the implicit optimism in the Pre-Criteria. While consumption had shown resilience in previous quarters, the most recent figures point to a clear moderation, consistent with a cooling labour market and a gradual deterioration in confidence. In this regard, consumer confidence in March recorded a significant decline, reflecting increased pessimism about the current and future economic situation of both the country and households. This deterioration in expectations is particularly relevant, as it has historically preceded further slowdowns in spending, even against a backdrop of real wage increases.

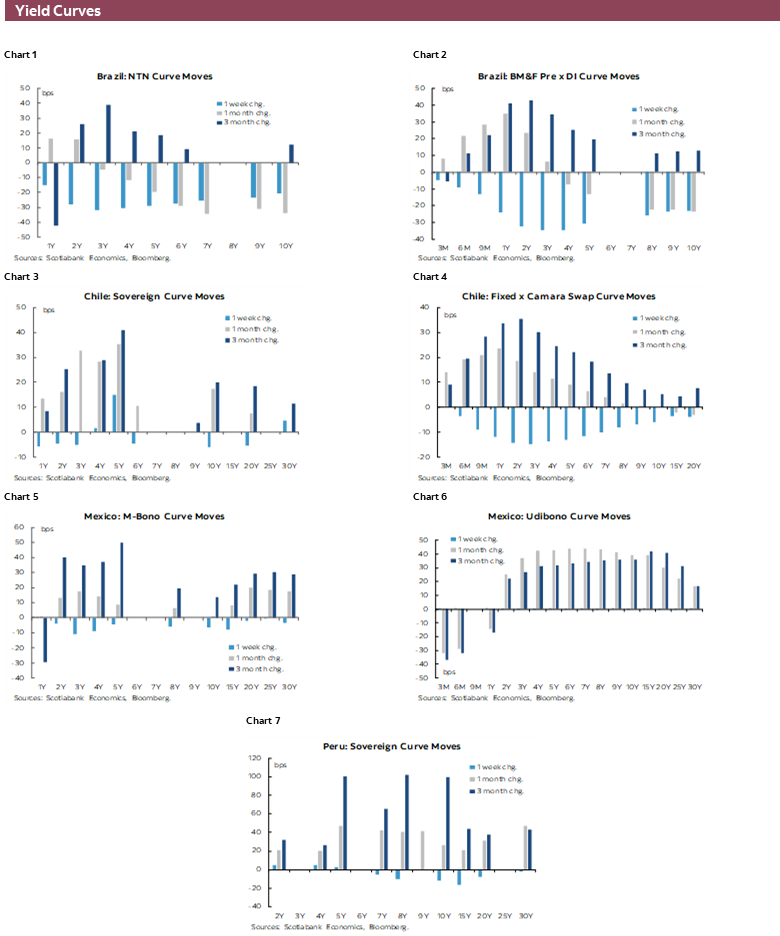

From a prices perspective, March inflation once again surprised to the upside (at 4.6% y/y) and remains above Banco de México’s tolerance range, driven by shocks in the non-core component—particularly food prices—while core inflation continues to display rigidity and persistence, especially in services. This inflationary configuration contrasts with the SHCP’s assumption of relatively rapid disinflation and complicates the monetary policy outlook by increasing the risk that interest rates may need to remain at restrictive levels for longer than anticipated.

Private sector expectations, as reflected in the most recent surveys conducted by Banco de México and Citi, reinforce this more cautious view. Analysts have revised their growth forecasts downward and continue to project inflation and interest rates that are consistently higher than those presented in the Pre-Criteria. This divergence is not trivial, as it suggests that markets are assigning a growing probability to a low-growth scenario with still-uncomfortable inflation, thereby reducing the scope for accelerated monetary easing.

Finally, developments in the automotive sector—one of the pillars of export performance—also send mixed signals. While exports and production of light vehicles remain at relatively high levels, domestic sales show weakness, and recent dynamics point to a deceleration relative to the pace observed in 2025, in line with softer domestic demand and heightened risks for manufacturing activity in the coming months.

In sum, the figures released this week do not support the SHCP’s scenario of robust growth, declining inflation, and sustained interest rate reductions for 2027. On the contrary, they outline a macroeconomic environment marked by fragile growth, weak domestic demand, persistent inflation, and limited room for maneuver in monetary policy, suggesting that the assumptions embedded in the Pre-Criteria may prove overly optimistic given the reality reflected in the latest hard data.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.