HIGHLIGHTS

- May is coming to an end with uncertainties remaining practically as elevated as they were at the start of the month. Middle East peace deal hopes could help markets but commodity supplies remain constrained as the conflict reaches the three-month mark.

- Peru’s second-round presidential vote on June 7th is nearing with polls not providing a clear enough guide into who will come out on top. Scandal-struck Bolsonaro has seen his polling and odds slide for Brazil’s October election. Colombians will cast their votes next Sunday for the presidency, with the contest set to require a second round election on June 21st.

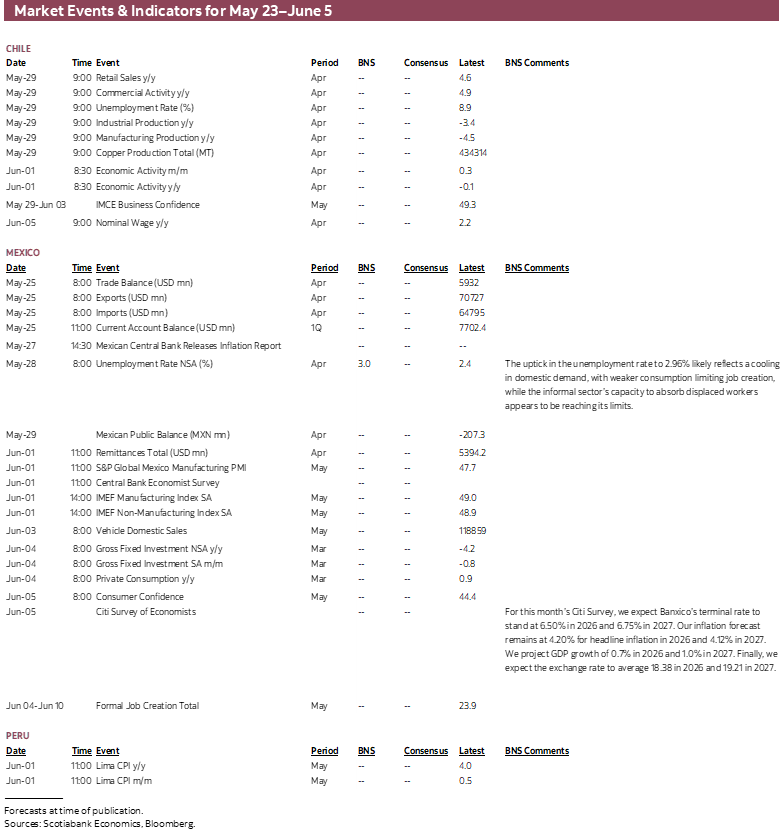

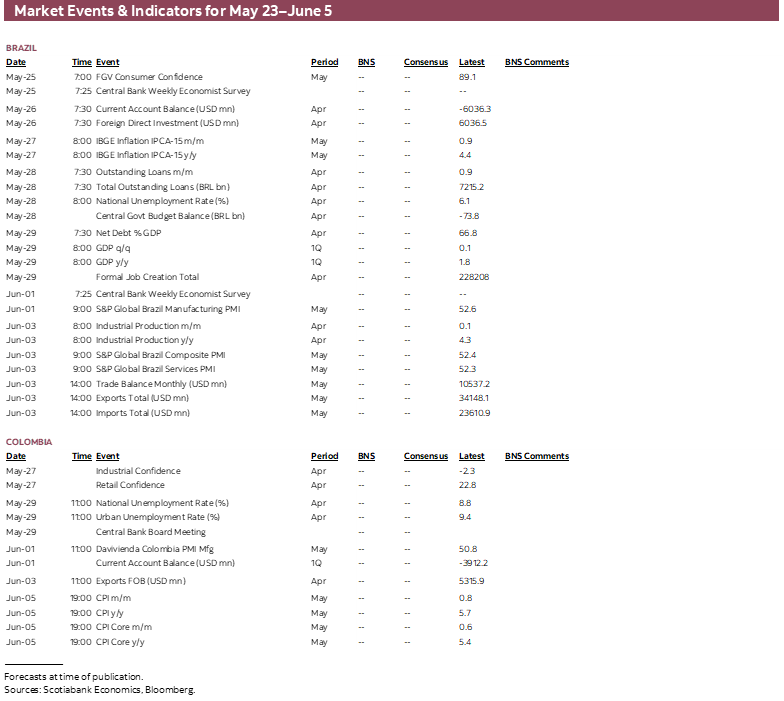

- Aside from geopolitics and Latam elections intrigue, next week’s schedule is somewhat quiet. Chile’s Friday macro flood will give us a first look into the country’s economic performance in the first quarter that is our team’s topic of discussion in today’s Weekly. In Mexico, our economists highlight how the Middle East conflict has had a limited impact on inflation, but it comes at a time of worryingly weak growth and elevated inflation.

Chart of the Week

LATAM ELECTION RISK ABOUNDS, COUPLED WITH MIDDLE EAST UNCERTAINTY

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- May is coming to an end with uncertainties remaining practically as elevated as they were at the start of the month. Middle East peace deal hopes could help markets but commodity supplies remain constrained as the conflict reaches the three-month mark.

- Peru’s second-round presidential vote on June 7th is nearing with polls not providing a clear enough guide into who will come out on top. Scandal-struck Bolsonaro has seen his polling and odds slide for Brazil’s October election. Colombians will cast their votes next Sunday for the presidency, with the contest set to require a second round election on June 21st.

- Aside from geopolitics and Latam elections intrigue, next week’s schedule is somewhat quiet. Chile’s Friday macro flood will give us a first look into the country’s economic performance in the first quarter that is our team’s topic of discussion in today’s Weekly. In Mexico, our economists highlight how the Middle East conflict has had a limited impact on inflation, but it comes at a time of worryingly weak growth and elevated inflation.

May is coming to an end with uncertainties remaining practically as elevated as they were at the start of the month. Next week’s global calendar is relatively quiet as far as scheduled events or data go and the earnings season is winding down, so headlines and news may be of greater importance for market sentiment. The views expressed by central bankers ahead of June rate announcements will also be front and centre, particularly as Fed hike rumblings grow louder (just as Kevin Warsh is sworn in as Fed Chair), while markets broadly shift their uncertainty from “will central banks hike?” to “when will they hike?”

On the geopolitical front, the war in the Middle East will reach the three-month mark—albeit with sharply reduced hostilities in recent weeks thanks to a shaky ceasefire—with representatives from the three main involved parties possibly gathering for peace talks late next week in Pakistan. Lessened military activity notwithstanding, the Strait of Hormuz remains virtually shut, depriving the globe of key resources, and resulting in September Brent crude oil trading in a ~$95–100/bbl all month long. Higher commodity prices and disruptions to fuel supplies become less manageable for second-round inflationary or expectations effects while eroding sentiment and possibly triggering energy shortages and demand destruction.

Domestic politics are a key focus in Latin America. Peru’s electoral authorities finally confirmed last Sunday the two candidates that came on top in the April 12th vote and will now face off on June 7th, Fujimori from Fuerza Popular (right) and Sánchez from Juntos por el Perú, with the presidential hopefuls presenting starkly different paths for the country. Polls are now in the spotlight, where Fujimori leads Sánchez by 3–4ppts according to Ipsos and Datum, but recall that surveys significantly underestimated Sánchez’s odds ahead of the first round vote, failing to capture the strength of left-wing candidates outside of the capital region and urban centres.

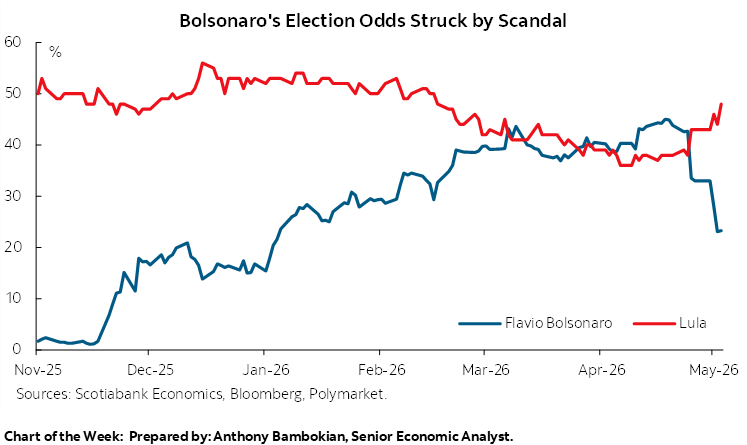

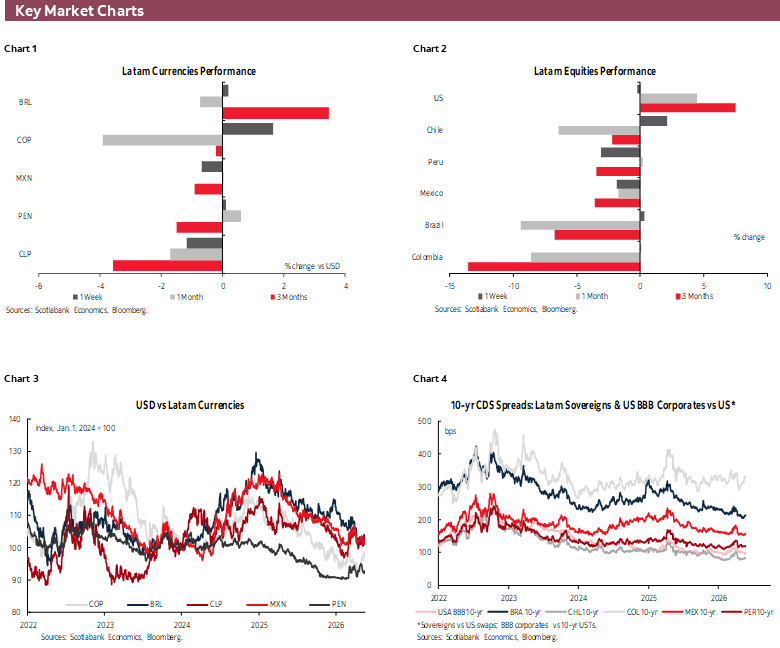

Expectations for Brazil’s October presidential election have sharply shifted in recent days, reverberating negatively on the country’s Ibovespa index that is tracking a 5%+ loss for the month—among the worst performing global equity induces in May alongside Turkey’s and Indonesia’s. The Banco Master/Vorcaro scandal involving Flavio Bolsonaro, President Lula’s main challenger, has sharply dented the conservative candidate’s presidential odds, quickly undoing the progress he had made in polls or prediction markets since his (skeptically-received) candidacy announcement in late-2025. AtlasIntel polling had a Lula-Bolsonaro face-off at 48%–48% in late-April, but the latest survey from mid-May shifted well in Lula’s favour at 49%–42% as a large share of respondents shifted to undecided or null. At the start of the month, Polymarket bettors assigned a ~45% chance to a Bolsonaro win (vs. Lula at ~40%). These odds have now fallen to ~25%, with the incumbent rising to a ~45% chance.

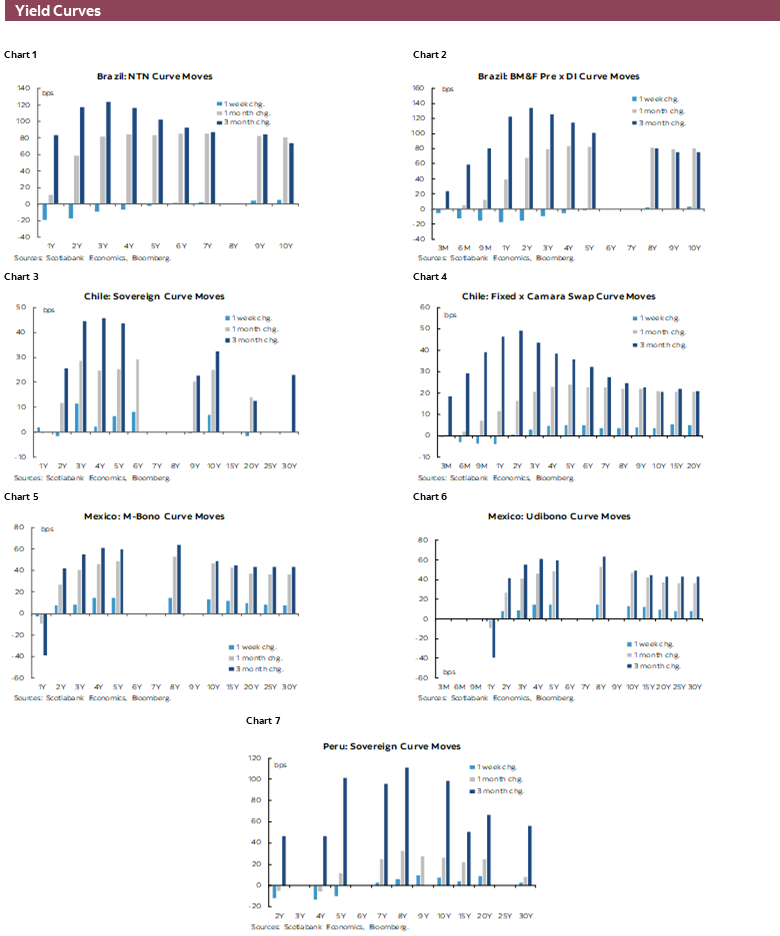

On net, BCB rate cut expectations by end-2026 haven’t really changed since the start of the month, remaining at around 50bps in cumulative easing priced in, but the combination of interest rates set to remain highly restrictive for some time and the less market-constructive electoral backdrop has taken its toll on local equities. Next Wednesday, the IBGE publishes IPCA-15 data for May that is expected to show inflation through the ceiling of the BCB’s 3+/-1.5% tolerance band for the first time this year owing to elevated food prices while retail fuel prices are kept under control, coupled with hot underlying inflation metrics. On Friday, Q1 GDP will likely show an improvement in quarterly growth but with fiscal support measures picking up the slack for muted underlying drivers amid a challenging interest rates environment and political uncertainty.

Banxico’s quarterly report out next Wednesday is the main item to watch in Mexico, coming just after the release of the bank’s May meeting minutes published yesterday which gave a fairly clear impression that officials have reached the end of the easing cycle. The bank’s quarterly report will give us a closer look into their thinking, and markets that are speculating on hikes may pay close attention to the balance of risks to inflation. In today’s note, our local team looks at how Mexico has fared (and how it may fare) under the latest energy prices shock, with fuel prices caps and subsidies helping to limit the pass-through of higher global crude oil prices, but the shock also comes at a time when growth is weak and inflation sits above target.

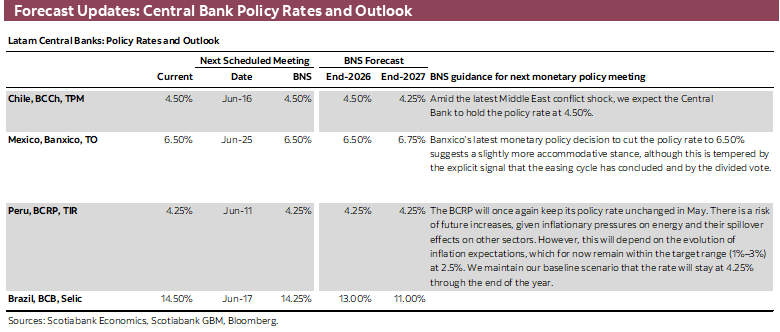

The once-a-month Chilean macro flood takes place next Friday, delivering retail sales, commercial activity, unemployment rate, and industrial/manufacturing/mining production data all at once. Next week’s data will be the first look at how the country’s economy kicked off the second quarter after a weak start to the year—the largest Q1 y/y decline since 2009—that is our colleagues’ topic of discussion in today’s Weekly. With a weak Q1 and lingering headwinds, our economists’ 2% growth forecast for 2026 is biased lower. On a growth-positive note, the Kast administration’s Reconstruction bill gained broad support in its passage through the Lower House, now awaiting a Senate vote that could take place next week.

Elsewhere, Colombia only has unemployment rate data on tap but political noise from the Petro administration and anticipation/positioning ahead of the May 31st vote (with a poll blackout from Monday) will carry markets next week. In the G10, the U.S. is closed on Monday for Memorial Day and has April PCE spending, income, and inflation due on Thursday, Canada releases Q1 GDP data on Friday, with German, French, and Spanish inflation data due that same morning that are unlikely to shift well-entrenched June ECB hike bets (the bank’s May meeting minutes drop on Thursday).

COUNTRY UPDATES

Chile—GDP Contracts in Q1-25, Reinforcing Downside Risks to the Growth Outlook

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

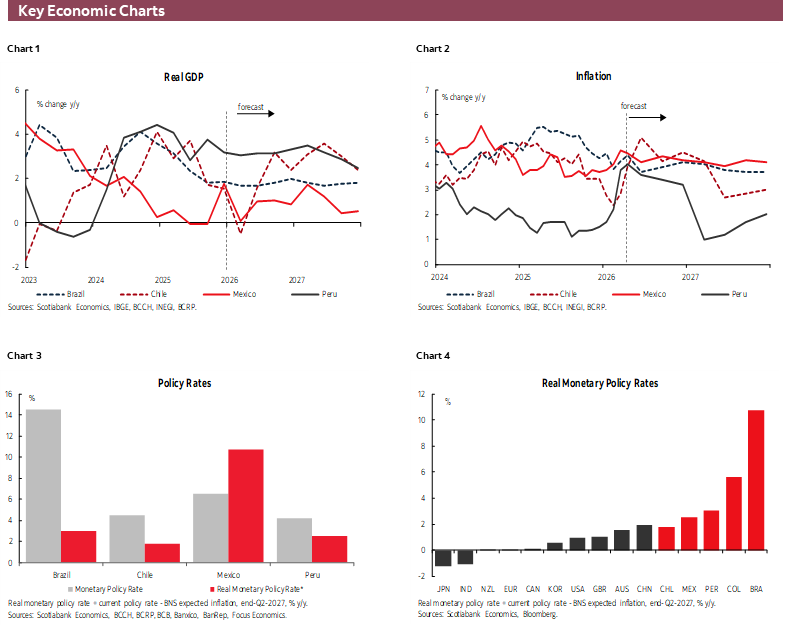

GDP contracted by 0.5% y/y in Q1-25, marking the weakest first-quarter performance since 2009 and introducing a downward bias to our full-year growth outlook. According to national accounts data, the decline was primarily driven by weaker exports, particularly in the agricultural and fishing sectors. In contrast, both private consumption and investment posted positive annual growth, although insufficient to offset the external drag. At the sectoral level, fishing GDP fell 19% y/y and agriculture declined 5.4% y/y, both weighing on manufacturing, which contracted 2% y/y in the quarter.

On a seasonally adjusted basis, GDP declined 0.3% q/q, reflecting softer export performance and a contraction in machinery and equipment investment. By sector, fishing GDP dropped 4.2% q/q SA, while agriculture fell 2.9% q/q SA. The weak performance in fishing has persisted since early this year, largely explained by reduced availability of jack mackerel and sardines off the Biobío coast, amid unstable ocean conditions linked to the transition toward El Niño. High-frequency data through the second week of May suggest that resource availability remains limited, pointing to no meaningful rebound in fishing activity in Q2. A recovery in primary sectors—and export volumes—would likely be delayed until late 2026 or early 2027. Against this backdrop, we reiterate that our 2.0% GDP growth forecast for 2025 is biased to the downside.

Separately, the Chamber of Deputies approved the Reconstruction bill with 90 votes in favour, 59 against, and 1 abstention, signaling broad support built through agreements with segments of the opposition. The initiative includes key measures such as a reduction in the corporate tax rate and stronger incentives to investment, aimed at boosting growth. The bill now moves to the Senate, where a more technical review is expected, particularly on fiscal matters. The government is pushing for a fast-track discussion, with a likely vote by end-May, ideally ahead of the presidential State of the Nation address on June 1st.

Mexico—Global Inflation Shock and Mexico’s Relative Position

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

The escalation of the conflict in the Middle East since March 2026 has generated an exogenous global inflationary shock, mainly through four channels: energy, transport/logistics, fertilizers, and food. The closure of the Strait of Hormuz—through which around 20% of global oil supply transits—has triggered a significant surge in energy prices, with WTI increasing between 65% and 80% relative to end-2025 levels, alongside higher logistics costs and rising pressures on agricultural inputs. This environment has increased uncertainty and reinforced global stagflation risks.

In advanced economies such as the United States and Europe, the impact has been evident in headline inflation—largely driven by energy—while core inflation remains more contained, albeit with early signs of reacceleration. In particular, U.S. inflation has risen from 2.4% to around 3.8%, prompting notable adjustments in monetary policy expectations, with fewer rate cuts priced in (and even priced out) and a longer period of elevated rates anticipated. In Europe, the risk of second-round effects has led to considerations of additional rate hikes. In emerging markets, the pattern is similar: shocks concentrated in non-core components and increased caution from central banks amid the risk of expectations becoming unanchored.

Mexico shares several of these characteristics, but with important differences in terms of transmission and macroeconomic balance. On the one hand, the pass-through from energy shocks has been relatively more contained than in other economies, largely due to domestic mechanisms—such as fuel price policies—that have dampened international prices volatility. In addition, access to U.S. natural gas via pipelines provides a relatively more favourable position compared with economies that are more dependent on spot or maritime LNG markets. This has prevented energy pressures from translating immediately into more severe inflation shocks, unlike in Europe.

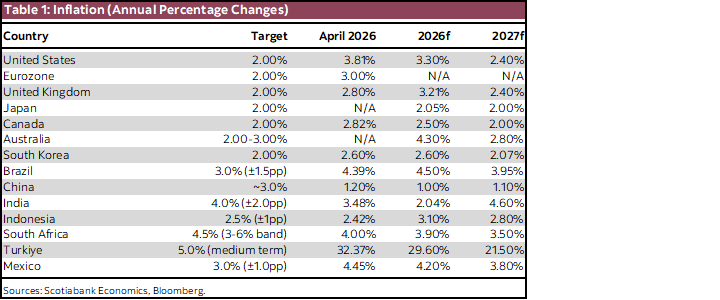

However, Mexico faces a more pronounced constraint on the real side of the economy. While growth in advanced economies remains positive—albeit moderate—Mexico’s activity shows clear stagnation and even recent sequential contraction, reflecting weakness in investment and the industrial sector. Despite this slack, inflation (4.45% in April) remains above Banco de México’s target, mainly driven by non-core components such as agricultural products, while core inflation continues to show persistence. This contrasts with the United States, where core inflation is more clearly converging toward target levels, albeit with upside risks.

In terms of monetary policy, while the Federal Reserve and other central banks have moved toward a pause or are even considering more restrictive stances, Mexico is at a different stage of the cycle. Banco de México has recently completed a rate-cutting cycle, bringing the policy rate to 6.50%, with a stance that is now close to neutral and an increasing likelihood of a pause amid a worsening inflation outlook. This reflects a key difference: Mexico started easing earlier but now faces less room for maneuver in the face of persistent external shocks.

In sum, although Mexico has managed to partially cushion the direct impact of the energy shock compared with other economies, it faces a more challenging environment in terms of growth and an inflation convergence process that remains incomplete. Unlike advanced economies—where the main challenge is to avoid second-round effects—Mexico faces a dual challenge: maintaining inflation expectations anchored amid persistent external shocks, while dealing with a weak economy and limited room for further monetary easing.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.