- Mexico: Banxico signals the easing cycle concluded at the May meeting; In Q1 2026, GDP grew 0.2% y/y, with marginal internal movements; In the first half of May, headline inflation stood at 4.11%, with pressures in the core component and moderation in the non-core component; Economic activity increased 1.4%, with declines in industry and growth in agriculture and services in March

MEXICO: BANXICO SIGNALS THE EASING CYCLE CONCLUDED AT THE MAY MEETING

Key takeaways

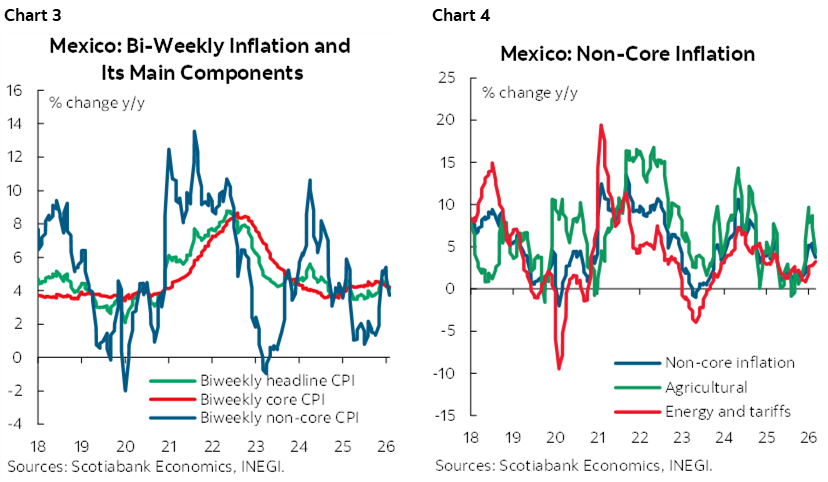

- Banco de México cut the policy rate to 6.50% in a split decision, amid still-elevated inflation, economic weakness, and a restrictive monetary stance.

- On the global front, the Board highlighted persistent uncertainty due to the conflict in the Middle East, which has pushed oil prices higher and weighed on global growth, leading central banks to adopt more cautious stances.

- Domestically, a sharper-than-expected slowdown was noted, with a -0.8% contraction in 1Q2026, alongside declines in consumption and investment and broad-based weakness in economic activity, partially offset by a resilient external sector.

- Regarding inflation, it declined to 4.45% driven by lower core inflation, although pressures persist in both services and the non-core component. The Board also noted no evidence of second-round effects from excise taxes (IEPS) and tariffs, although the balance of risks remains skewed to the downside.

- Looking ahead, a pause in the easing cycle is expected throughout 2026—with a higher probability of rate hikes toward late 2026 or early 2027 due to inflationary pressures—maintaining a terminal rate of 6.50%.

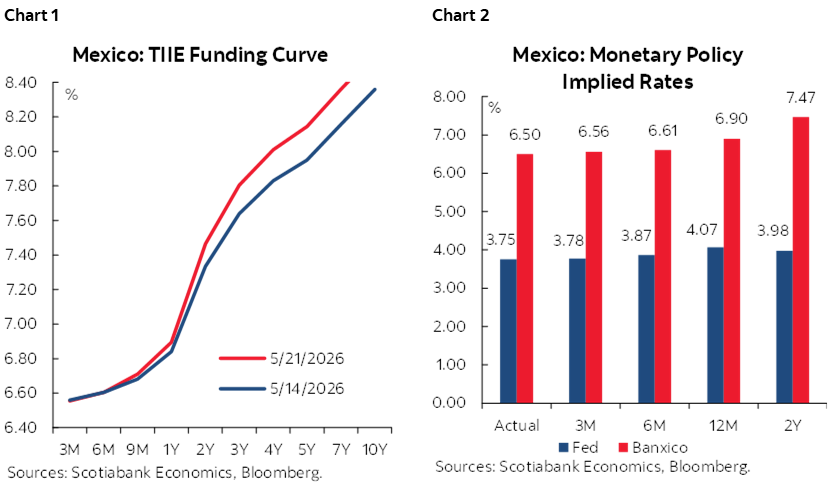

Banco de México released the minutes to the May 6th meeting, in which the Governing Board decided by majority to cut the policy rate by 25 basis points to 6.50%, effectively concluding the easing cycle that began in March 2024. The decision reflects a balance between observed inflation moderation and weak economic activity, as well as the acknowledgment that the monetary stance remains restrictive. Going forward, the Board anticipates keeping the rate at its current level, considering it appropriate to address macroeconomic challenges and ensure inflation converges to target.

According to the minutes, the global economic environment remains highly uncertain, primarily due to geopolitical conflicts in the Middle East. This has deteriorated global growth prospects and generated additional inflationary pressures, particularly through the energy channel. International oil prices have risen significantly—approaching USD 100 per barrel—due to supply disruptions and logistical risks related to the Strait of Hormuz. This shock has led to downward revisions in global growth expectations and upward revisions in inflation forecasts, although second-round effects remain limited in several economies and long-term expectations remain relatively well anchored. In this context, major central banks have adopted a cautious stance, mostly holding rates unchanged and emphasizing data dependency in an environment of high uncertainty.

Domestically, the Board acknowledged that the Mexican economy has shown greater weakness than anticipated. In 1Q26, economic activity recorded a quarterly contraction of around -0.8%, with nearly zero annual growth, reflecting broad stagnation. The decline was driven by contractions across all major sectors, particularly manufacturing, which have experienced several months of contraction, largely linked to weak automotive sector performance. Services interrupted their growth trajectory, and primary activities continued to weaken. Domestic demand has been notably weak, with a contraction in private consumption and a persistent decline in fixed investment, especially in machinery and equipment. In contrast, the external sector has remained resilient and has emerged as the main growth driver, with manufacturing exports—particularly non-automotive—reaching record highs, supported by demand from the U.S. tech industry. The outlook for the remainder of the year points to a moderate recovery, with risks predominantly to the downside, amid increasing economic slack.

Annual headline inflation declined from 4.63% to 4.45% between March and April, mainly due to a decrease in core inflation, although this was partially offset by increases in the non-core component, particularly in fruits and vegetables such as tomatoes, which explained nearly all the accumulated increase so far this year. Core inflation fell to 4.26% from 4.46%, reflecting lower pressures in goods, though it remains above its historical average, particularly in services. Pressures persist in food services—one member noted they could reflect the agricultural shock—as well as in housing and education. Non-core inflation remains volatile and elevated, affected by temporary agricultural shocks and adjustments in energy and administered prices. Most members agreed there is no evidence of second-round effects from fiscal measures (IEPS) and tariffs. Inflation expectations remain above historical averages, with 2026 forecasts revised slightly upward, maintaining an upward risk bias driven by external factors (geopolitical conflict, energy prices, global costs) and persistent services inflation, although mitigated by the restrictive monetary stance, economic slack, and currency appreciation.

Regarding domestic financial markets, they have exhibited relatively favourable performance, consistent with the recent moderation in global volatility. The Mexican peso appreciated against the U.S. dollar, supported by the interest rate differential, solid macroeconomic fundamentals, and global dollar weakness. In the fixed income market, short-term rates have declined, while long-term rates have risen moderately, resulting in a steepening yield curve. There have also been significant capital inflows into government debt instruments, contributing to lower risk premia. Nonetheless, the financial environment remains subject to episodes of volatility driven by external conditions.

Within the Board’s monetary policy discussion, differing views were observed. The majority (3/5) adopted a more flexible stance, noting that recent inflation shocks are temporary and that economic slack, currency appreciation, and the cumulative effects of restrictive monetary policy will help reduce inflation. In contrast, Galia Borja and Jonathan Heath took a more cautious approach, emphasizing persistent core inflation—particularly in services—ongoing supply shocks, and the risk of de-anchoring expectations. They viewed further cuts as premature and favored a pause. The inflation risk balance remains skewed to the upside, with key risks including geopolitical developments, further increases in energy prices, persistent services inflation, and cost pressures from wages and supply chains. Growth risks, on the other hand, are clearly tilted to the downside, reflecting weak domestic demand, potential further deterioration in the global economy, and elevated external uncertainty. Overall, the outlook suggests monetary policy is entering a pause phase with a cautious, data-dependent approach amid external inflationary pressures and a weakened domestic cycle.

Looking ahead, based on Board members’ comments, we expect the policy rate to remain on hold for the rest of the year. However, the probability of rate hikes increases toward late 2026 or early 2027, particularly if the Middle East conflict persists. In such a scenario, pressures on energy and fertilizers would remain persistent and feed into intermediate goods and transportation costs, potentially reinforcing an inflation rebound and affecting expectations. These have already been revised upward for 2026 and could begin rising for 2027 as well. Additionally, factors such as a possible currency depreciation or a narrowing of the monetary policy differential between the U.S. and Mexico could intensify these pressures. In this context, we maintain our expectation of a 6.50% terminal rate for 2026, although we do not rule out a higher level by year-end.

IN THE FIRST HALF OF MAY, HEADLINE INFLATION STOOD AT 4.11%, WITH PRESSURES IN THE CORE COMPONENT AND MODERATION IN THE NON-CORE COMPONENT

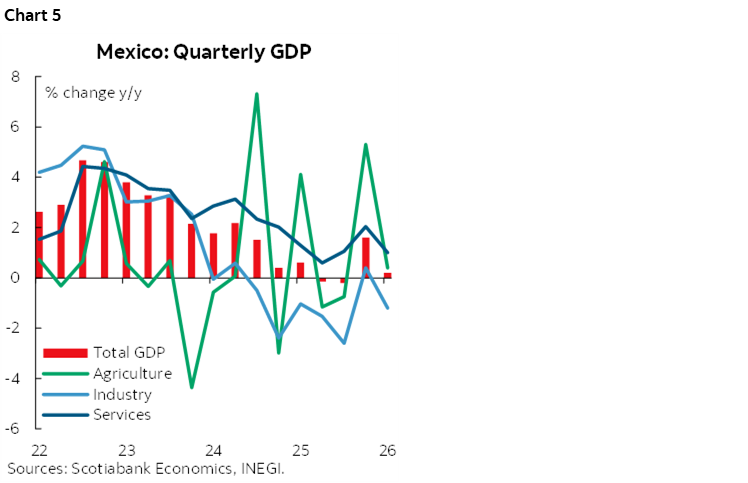

In the first half of May 2026, headline inflation in Mexico stood at 4.11% y/y (charts 3 and 4), with a biweekly change of -0.16%, mainly reflecting declines in the non-core component. Core inflation remained elevated, increasing 4.22% y/y and 0.13% biweekly, driven primarily by services (4.59% y/y) and, to a lesser extent, goods (3.83% y/y). Within goods, processed foods stood out at 5.18% y/y, while other services reached 5.35% y/y.

In contrast, non-core inflation showed a notable moderation, at 3.73% y/y and -1.14% biweekly, explained by declines in energy and regulated tariffs (-1.64% biweekly)—particularly electricity—and in agricultural goods (-0.53%). In terms of contributions, upward pressures were mainly driven by tomatoes, detergents, and LP gas, as well as services such as housing and food items like potatoes and chicken; meanwhile, the largest downward contributions came from electricity, green tomatoes, and eggs, reflecting seasonal effects in electricity tariffs and lower prices for some agricultural products.

IN Q1 2026, GDP GREW 0.2% Y/Y, WITH MARGINAL INTERNAL MOVEMENTS

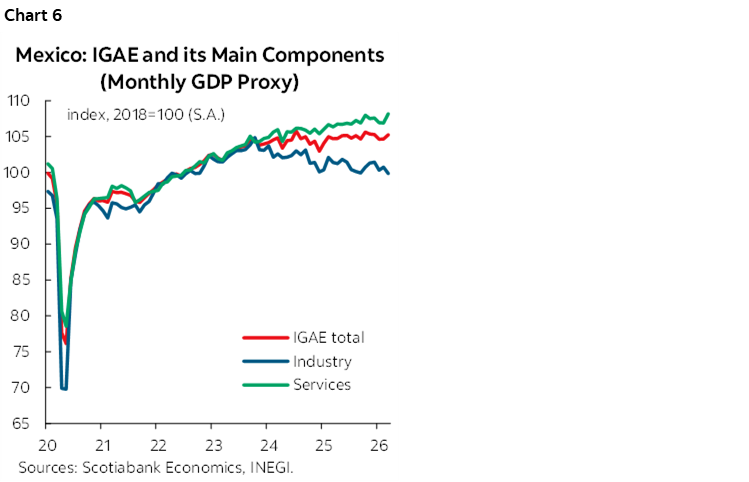

Today, revised GDP figures for Q1 2026 were released (chart 5). According to INEGI, GDP posted an annual growth rate of 0.2% in original terms—slightly above the preliminary 0.1% estimate. Internally, movements were marginal: agricultural activities increased by 0.4%, while services grew by 1.0%, driven by legislative activities (5.3%) and health services (3.3%). Meanwhile, industry contracted by -1.2%, reflecting declines in utilities (-0.2%), construction (-0.7%), and manufacturing (-2.0%), partially offset by a 1.6% increase in mining. On a quarterly basis, GDP declined by -0.6% q/q, with broad-based contractions across sectors: agriculture -1.7%, industry -1.0%, and services -0.4%.

ECONOMIC ACTIVITY INCREASED 1.4%, WITH DECLINES IN INDUSTRY AND GROWTH IN AGRICULTURE AND SERVICES IN MARCH

In March, the Global Indicator of Economic Activity (IGAE, chart 6) showed annual growth of 1.4% (compared with -0.3% in February) in original terms. By sector, primary activities expanded by 2.2%. Industrial activity declined by -1.3%, with construction falling -6.2%, manufacturing -1.0%, while mining rose 6.0% and utilities grew marginally by 0.2%. Services increased by 2.8%, driven by entertainment services (12.3%) and legislative activities (11.3%). On a seasonally adjusted monthly basis, the IGAE rose 0.4% (vs. 0.1% previously), with gains in primary activities (4.5%) and services (0.8%), and a contraction in industry (-0.6%).

—Rodolfo Mitchell, Miguel Saldaña & Martha Cordova

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.