HIGHLIGHTS

- Next week’s Latam schedule is fairly light, coming on the heels of regional June CPI releases that mostly surprised higher (Chile and Peru) or lower (Mexico and Brazil).

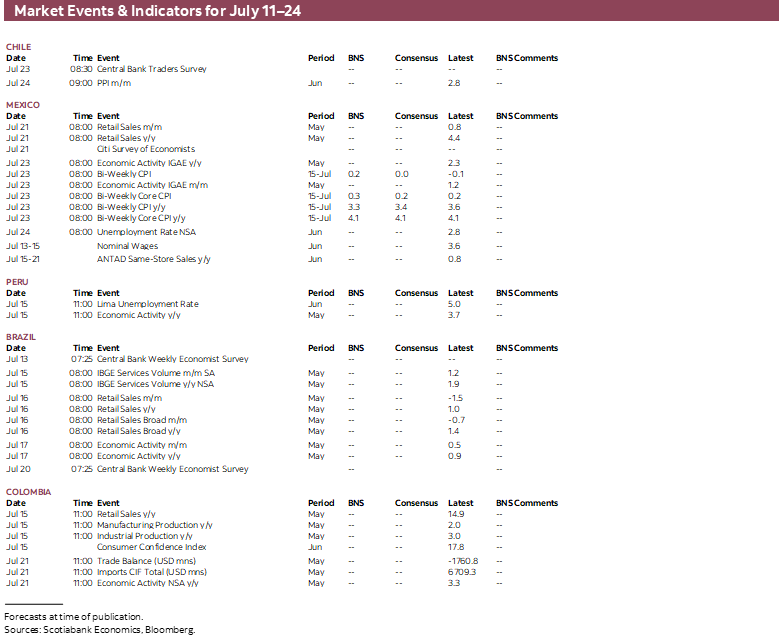

- Brazilian and Peruvian economic activity data for May is the regional highlight, while Mexico’s and Chile’s calendars are bare of notable releases. Global markets will focus on U.S. CPI data and Fed Chair Warsh’s appearance in Congress.

- In today’s report, the team in Mexico looks at the latest inflation undershoot and Banxico’s meeting minutes, with both pointing to an on–hold central bank at least through the remainder of the year.

Chart of the Week

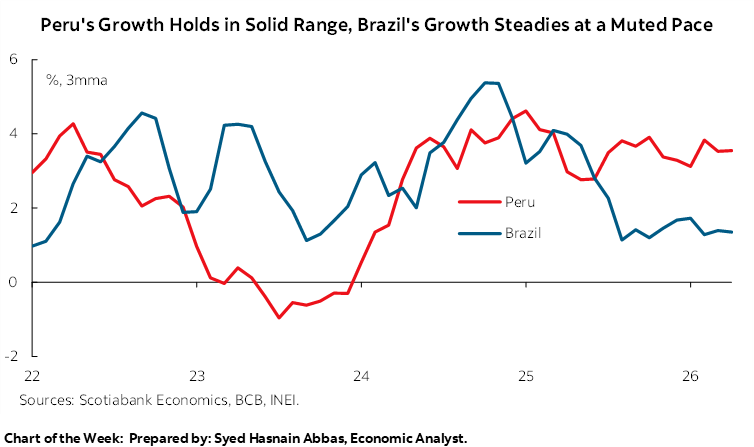

BRAZILIAN AND PERUVIAN ECONOMIC ACTIVITY

Juan Manuel Herrera, Director

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Next week’s Latam schedule is fairly light, coming on the heels of regional June CPI releases that mostly surprised higher (Chile and Peru) or lower (Mexico and Brazil).

- Brazilian and Peruvian economic activity data for May is the regional highlight, while Mexico’s and Chile’s calendars are bare of notable releases. Global markets will focus on U.S. CPI data and Fed Chair Warsh’s appearance in Congress.

- In today’s report, the team in Mexico looks at the latest inflation undershoot and Banxico’s meeting minutes, with both pointing to an on-hold central bank at least through the remainder of the year.

Next week’s Latam schedule is fairly light, coming on the heels of regional June CPI releases that mostly surprised higher (Chile and Peru) or lower (Mexico and Brazil), with implications for monetary policy expectations that have been pulled in all directions in recent weeks—and not just in Latam. The broad market mood remains primarily driven by two things, AI news and Middle East developments, with a side dish of economic data and comments by central bankers.

The market handled the ‘end’ of the U.S.-Iran ceasefire (and military strikes in the region) relatively well, believing that the rise in tensions is mostly noise as the two sides are still engaging in talks toward a longer-lasting peace agreement. All in all, the ~5% rise in crude oil prices this week is relatively small and while Brent oil briefly broke through the $80/bbl level, its current price of ~$75/bbl is still about twenty dollars less than this time last month and only ~$5/bbl higher compared to end-February.

Brazilian and Peruvian economic activity data for May is the regional highlight, while Colombia publishes industrial and retail readings, and Mexico’s and Chile’s calendars are bare of notable releases. Abroad, June U.S. CPI and Fed Chair Warsh’s two-day appearance in Congress are in focus, accompanied by Chinese Q2 GDP and the Bank of Canada’s rate announcement and forecast update. Next week, traders will also have to contend with the start of the Q2 corporate earnings season.

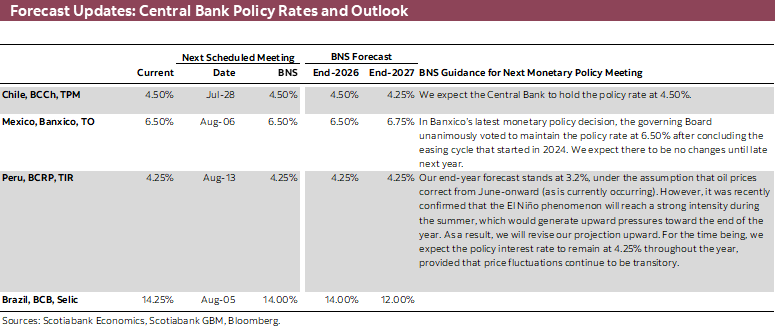

In today’s report, the team in Mexico looks at the latest inflation undershoot and Banxico’s meeting minutes. A few months or weeks back, economists and markets were toying with the idea that Banxico could hike this year, as the bank practically shut the door on additional near-term rate cuts at its May decision and data showed a fast acceleration in inflation. However, recent inflation prints—including yesterday’s 0.1ppts miss in headline and core inflation data for June—have weakened these expectations, as vegetable prices inflation retreats, helping to take inflation to its lowest level since 2021 in June, at 3.4% y/y. This is after printing its highest reading since late-2024 back in March, at 4.6%. Markets are currently pricing in a 7.05%–7.10% Banxico overnight rate twelve months from now, compared to the ~7.6% high around this time last month.

Underlying metrics remain elevated and there’s no evidence that these may soon correct; core services inflation has hung around the 4.5% mark since spring 2024. But Banxico has shown an inclination to look past core inflation consistently sitting above the 2–4% target band, so the current backdrop of ‘under control’ headline inflation gives Banxico room to keep policy rates as they are for the foreseeable future. While inflation has fallen of late, economic activity data have tentatively trended in the opposite direction (though growth remains underwhelming). The Fed’s path ahead remains an unknown that could also influence Banxico’s decisions. So, there’s really no obvious path to take aside from the current one of rate stability.

Peruvian GDP growth will likely correct from the strong 3.7% y/y expansion it recorded in April but should still hold at a very strong expansion of around 3% in May that remains about the best among the major countries in the region. Despite electoral risks and El Niño impacts on the fishing (big drag in May) or agricultural sectors, or the sharp increase in inflation in recent months due to global energy prices (that should now ease), the country’s economy continues to expand at a strong pace supported by healthy household consumption and investment drivers. The recent confirmation of Keiko Fuijimori as the winner of the presidential election—with her term beginning later this month—has also resulted in a recovery in economic expectations that took a hit following the first-round vote. We’ll see whether a pro-business presidency gives an extra push to Peru’s private sector in the months to come, though economic activity could face a transitory hit from a harsh El Niño.

In Brazil, growth remains so-so although decent considering election risks and highly restrictive policy rates. On Friday, economic activity is estimated to have grown in May by about half of April’s 0.9% y/y rise with a flat or slightly negative print on a month-over-month basis. Industrial production growth held around the mid-2s y/y for the month, but it contracted by 0.2% m/m in seasonally adjusted terms. There’s not much else to go on but it’s fair to assume at least a slowdown from the 0.5% m/m expansion registered in April. Ahead of the data, we’ll get figures on services volumes on Wednesday and retail sales on Thursday that will help narrow expectations for the economic output aggregate.

COUNTRY UPDATES

Mexico—Inflation Surprises to the Downside on Lower Agricultural Pressures, Reinforcing Banxico’s Pause

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

The release of Banco de México’s June monetary policy meeting minutes contained few surprises. However, together with the June inflation report—which came in notably below market consensus due to a moderation in the non-core component—it strengthened expectations that the policy rate will remain unchanged for the rest of the year. Nevertheless, the possibility of an additional rate cut later this year cannot be ruled out if inflation remains below 4.0% in the coming months. This stands in contrast to the outlook in advanced economies, where markets anticipate tighter monetary conditions in the second half of the year as a result of rising inflationary pressures linked primarily to the geopolitical conflict in the Middle East and its impact on energy prices.

In June, headline inflation continued to surprise on the downside, reaching its lowest level since December 2020, falling from 3.94% to 3.37% y/y, below the consensus forecast of 3.50%. The result was largely driven by a sharp deceleration in non-core inflation, which declined from 3.10% to 1.11%, reflecting a drop in food prices of -1.72% as meat and poultry prices retreated. Core inflation also eased, falling from 4.19% to 4.03%, below the market expectation of 4.10%. Within the core basket, goods inflation moderated from 3.78% to 3.55%, while services inflation edged down from 4.52% to 4.49%, suggesting that the recent football-related events had only a limited impact on prices. On a monthly basis, headline inflation declined by -0.27%, core inflation increased by 0.24%, and non-core inflation fell by -2.04%.

Against this backdrop, the June meeting minutes reinforced the perception that Banxico has entered a prolonged pause phase. While Board members acknowledged that part of the recent improvement in inflation stemmed from the volatile behavior of the non-core component, they also highlighted the absence of significant demand-side pressures and the persistence of economic slack, factors that continue to support the disinflationary process. Moreover, the prevailing view was that the current monetary stance remains sufficiently restrictive to ensure convergence toward the inflation target. As such, any additional adjustment will depend on more compelling evidence of sustained disinflation and on developments in the external environment.

The signal of policy stability in Mexico contrasts with the expected path of monetary policy in several advanced economies. The IMF’s July World Economic Outlook update indicated that the global disinflation process has stalled and revised upward its inflation forecasts for 2026. The report emphasized that pressures stemming from the conflict in the Middle East continue to pose a significant risk to energy prices and global supply chains. As a result, markets are increasingly pricing in episodes of tighter monetary policy should inflationary pressures persist.

By contrast, we believe Banco de México can maintain its current monetary stance without facing the same inflationary pressures that are affecting some advanced-economy central banks. This is largely due to the government’s efforts to contain increases in gasoline prices. Furthermore, if headline inflation remains below 4.0% over the coming months and core inflation continues to moderate, we believe Banxico could consider an additional rate cut toward year-end. This possibility is already beginning to appear in the latest Citi survey of analysts, where 5 out of 37 respondents now anticipate further easing, with one participant expecting a cut as early as December.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.