HIGHLIGHTS

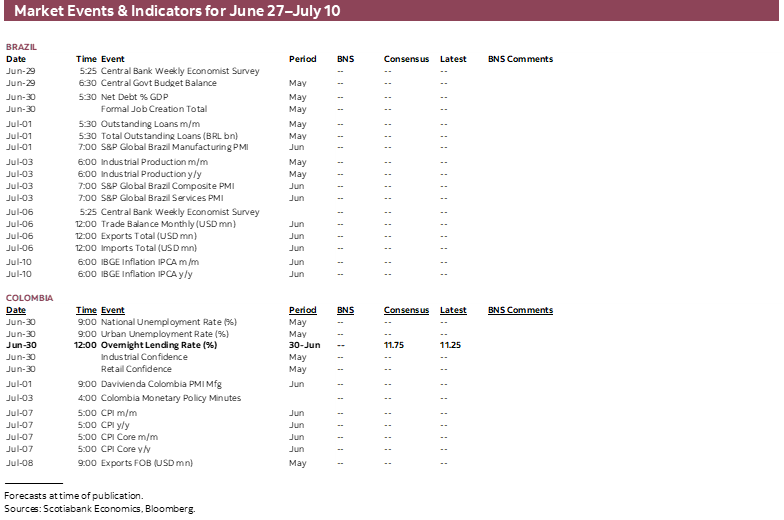

- Next week brings key data releases from around the globe with shortened trading in several key economies due to holidays. Chilean and Peruvian markets are closed on Monday, Canada is out on Wednesday, and the U.S. is off on Friday.

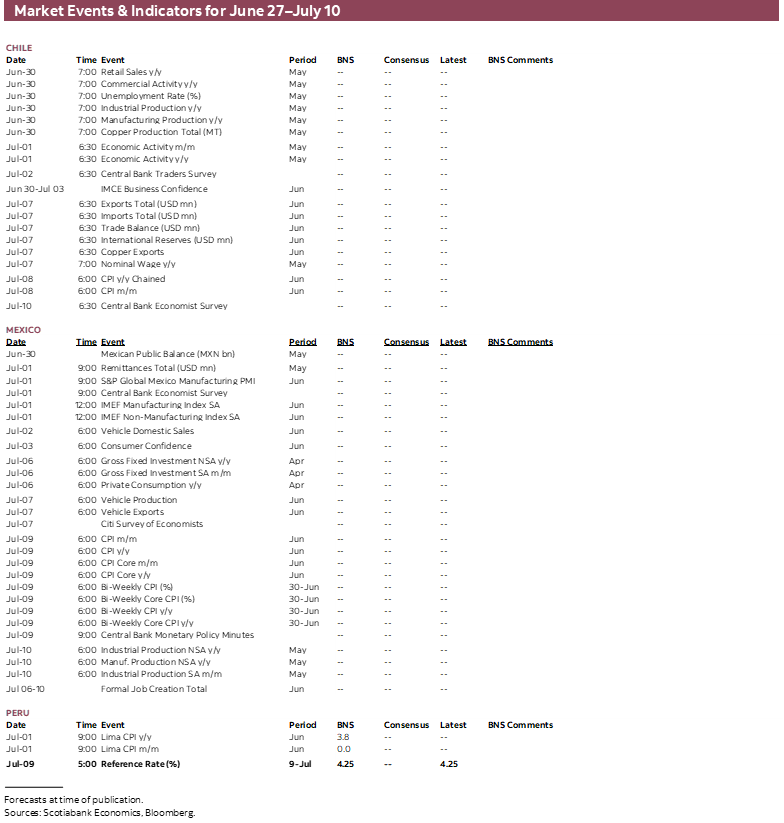

- Chile’s calendar is the busiest of all in Latam, with a flood of macro data on Tuesday and Wednesday, Peru is first out with full-month June CPI on Wednesday, and BanRep is set to announce another rate hike on Tuesday. Mexico and Brazil have second-tier data on tap.

- In today’s report, the team in Peru goes over their expectations for a slight deceleration in headline inflation as lower energy prices clash with higher fish prices due to El Niño. In Mexico, the team covers the latest inflation and Banxico developments.

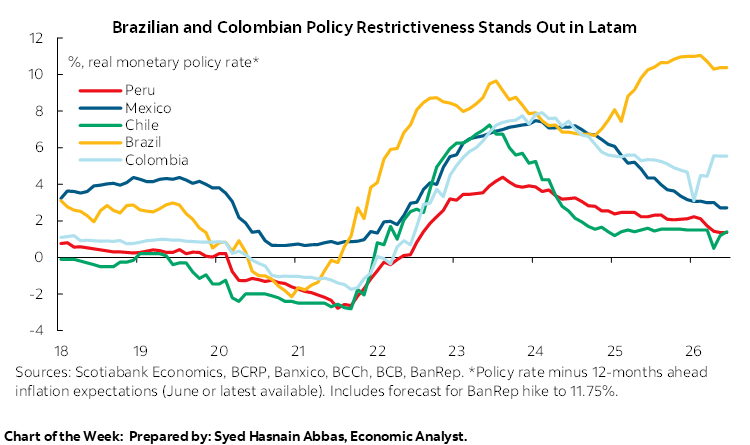

Chart of the Week

CHILE MACRO, PERU CPI, BANREP HIKE

Juan Manuel Herrera, Director

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Next week brings key data releases from around the globe with shortened trading in several key economies due to holidays. Chilean and Peruvian markets are closed on Monday, Canada is out on Wednesday, and the U.S. is off on Friday.

- Chile’s calendar is the busiest of all in Latam, with a flood of macro data on Tuesday and Wednesday, Peru is first out with full-month June CPI on Wednesday, and BanRep is set to announce another rate hike on Tuesday. Mexico and Brazil have second-tier data on tap.

- In today’s report, the team in Peru goes over their expectations for a slight deceleration in headline inflation as lower energy prices clash with higher fish prices due to El Niño. In Mexico, the team covers the latest inflation and Banxico developments.

July kicks off with key data releases from around the globe with shortened trading in several key economies next week due to holidays that could increase market volatility amid thinner liquidity (though coinciding with possible quarter-end adjustments). Equity sentiment looks a bit touchy as AI-driven gains are checked by concerns over the magnitude and speed of capital expenditures, OpenAI’s reported IPO postponement, and rocky trading in SpaceX shares and debt. The tech headwinds as well as Fed hike fears following last week’s policy announcement have dampened the positive sentiment boost from the U.S.-Iran peace treaty, with energy exports and transit through the Strait of Hormuz quickly ramping up to depress crude oil prices to around pre-conflict levels.

Chile’s calendar is the busiest of all in Latam, with a flood of macro data on Tuesday and Wednesday that includes May economic activity, while its regional peers have relatively light schedules where the highlights are Peruvian June CPI on Wednesday and BanRep’s rate announcement on Tuesday. Mexico and Brazil have only second-tier data on tap—international remittances out on Wednesday for the former and industrial production on Friday for the latter, both for May. In Brazil, a recent spat between Flavio Bolsonaro (Lula’s main opposition for the October elections) and Michelle Bolsonaro, his stepmother, has added to the Flavio’s struggle to lift his odds of victory. No major polls have been released since Michelle released a video accusing Flavio of disrespecting her, but Polymarket shows him at a 23% chance of winning, roughly half its peak prior to the Banco Master scandal, compared to Lula at 57%.

Outside of Latam, the U.S. is out with June nonfarm payrolls on Thursday, preceded by June ADP employment and May JOLTS among other releases, Canada publishes April GDP on Tuesday, and Eurozone countries and the bloc as a whole release June inflation data on Tuesday and Wednesday. Official Chinese PMIs come out on Tuesday, with indicators for the country continuing to show muted growth. Chilean and Peruvian markets are closed on Monday, Canada is out for business on Wednesday, and the U.S. is out on Friday.

Economic indicators have trended weakly in Chile in recent months, but economists expect some moderation in this weakness in May data due next week. While declines in mining and agricultural output, due to structural and weather effects, have been an important drag on activity so far in 2026, growth in other industries has also cooled, likely reflecting softness in labour markets. On Tuesday, May retail sales, industrial production, and unemployment rate data are on tap. Retail sales are carrying a strong tailwind from previous months’ strength which means that even with no growth m/m they would grow by 3.1% y/y, but it remains to be seen how the sector performs month-over-month following a 0.5% m/m seasonally adjusted decline. Wednesday’s May economic activity reading will likely show a rebound from a 1.2% y/y contraction in April when mining activity fell by 11.8% y/y but non-mining output also had a soft month with growth of only 0.4% y/y; seasonal factors also played an outsized role in April weakness that may flip in the other direction in May.

As always, Peru is first out with full-month CPI data for May due on the 1st that is the focus of our local economics team in today’s report. Domestic gasoline prices have been steadily trending lower since early-June, but fish prices have headed in the opposite direction as increased sea temperatures in relation to El Niño reduce catch rates. These offsetting factors as well other price dynamics should result in only a tick lower in headline inflation to 3.8% from 3.9% y/y. Transitory El Niño and energy supply shocks in prices mean the BCRP will stand pat over the medium term. On that note, the team outlines the key takeaways from last week’s BCRP inflation report, in which the bank’s staff estimates that El Niño will have a 0.8ppts negative impact on GDP growth in each of 2026 and 2027. Despite this large shock, Peru should still grow by more than 3% this year and next.

Economists are split in their expectations for Tuesday’s BanRep policy announcement, with the bank expected to increase its overnight rate to its highest level since mid-2025. The median among the fifteen economists polled by Bloomberg believes that Colombia’s central bank will hike by 50bps to 11.75% but a third think that a larger 75 or 100bp hike awaits, and only two think a 25bp or a rate hold are in store. In any case, BanRep is in a very uncomfortable position of tightening policy amid accelerating inflation that mainly has large minimum wage hikes and indexation practices to blame. Government-set wage increases at the start of the calendar year will likely be smaller under president-elect de la Espriella, which could help dampen inflation expectations, but the damage is done for this year. On Friday, BanRep publishes the minutes to its policy meeting which should help gauge the size of the next possible rate hike.

Mexican international remittances data for May out on Wednesday may show an extension of its recent improving trend. After contracting year-over-year in every month from April to November 2025, remittances have since been in positive growth territory (except a small dip in January) that may reflect improved labour conditions or greater comfort with wiring funds among Mexicans living in the U.S. The dollar amount still remains depressed versus the highs seen in 1Q-25 (on a 12m rolling basis) but it has stopped declining and is showing early signs of reaccelerating. An increase in remittances would be highly welcome for a domestic economy that remains lethargic amid weak investment and formal employment. In today’s note, our colleagues in Mexico cover the latest developments in the country, which included an undershoot in H1-June CPI, Banxico’s rate hold with signs pointing to rate stability, and the bank’s recent operational amendment that authorizes it to conduct purchase auctions in secondary markets aimed at strengthening its liquidity management framework.

COUNTRY UPDATES

Mexico—Inflation and Banxico Took Centre Stage This Week

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

This week featured two key events for the outlook of monetary policy and the path of short-term interest rates in Mexico: the release of inflation for the first half of June and Banco de México’s fourth monetary policy decision of the year.

First, headline inflation surprised favourably INEGI’s CPI report, standing at 3.55% y/y in the first half of June, down from 3.77% in the second half of May and below the Bloomberg consensus expectation of 3.72%. This deceleration was mainly driven by the non-core component, whose annual variation declined from 2.48% to 1.61%, supported by a -6.15% annual drop in livestock product prices and a moderation in the pace of growth of fruit and vegetable prices. In this context, it is worth noting that the impact of geopolitical tensions in the Middle East on energy prices has so far been limited, as energy inflation stood at 1.43% annually, even below Banco de México’s inflation target.

However, underlying inflationary pressures continue to show persistence. Although goods inflation moderated, moving from 3.74% annually in the second half of May to 3.65% in the first half of June, this reduction was mainly explained by non-food goods, whose rate fell from 2.58% to 2.38% annually. By contrast, processed food prices remain elevated, growing at 5.13% annually. Likewise, services inflation remains stuck at around 4.5%, a level significantly above the inflation target, reflecting still-notable increases in categories such as education and other services, whose annual variations stand at 5.94% and 5.31%, respectively, despite weak domestic growth.

Therefore, although headline inflation has continued to decline and the more volatile components have contributed favourably to the downside in the recent print, it would be highly premature to conclude that the disinflation process is fully consolidated. Factors such as adverse weather events, a prolongation or escalation of the conflict in the Middle East, the growing fragmentation of international trade, or the emergence of new sources of geopolitical tension could trigger a resurgence of inflationary pressures in the coming months.

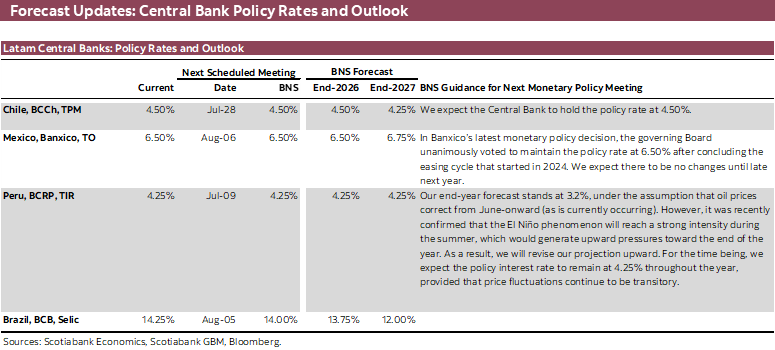

Against this backdrop, Banco de México unanimously kept the reference interest rate unchanged at 6.50%, in line with market expectations and after previously signaling the end of its easing cycle, which accumulated 475bps in reductions since March 2024. The Governing Board left its headline inflation forecasts unchanged and reiterated its expectation that inflation will converge to the 3.0% target during the second quarter of 2027, although it marginally revised upward its projections for core inflation. It also noted that economic activity could show a recovery during the second quarter of 2026, after the previously observed contraction, although downside risks to growth and upside risks to inflation persist, associated with factors such as geopolitical conflicts, trade policies, cost pressures, and potential episodes of currency depreciation.

Under this scenario, we believe that Banco de México currently maintains a monetary policy stance close to neutrality. Consequently, we maintain our expectation that the reference rate will end 2026 at 6.50%, although this forecast will continue to depend on the evolution of inflation, exchange rate dynamics, economic growth, and the stance adopted by the Federal Reserve. This is particularly relevant in an international environment where some central banks have begun to show signs of greater caution and even a potentially more restrictive bias, amid the risk that recent geopolitical tensions generate renewed pressures on global prices with second-round effects on core components of the prices basket.

Finally, another topic that generated broad discussion during the week was the publication of Banco de México’s Circular 8/2026, through which the provisions contained in Circular 6/2012 were amended to strengthen the operational framework for liquidity management through auctions of Monetary Regulation Bonds (BREMS) and government securities. The most relevant change is that the central bank formally incorporates the authority to conduct purchase auctions of government securities and BREMS in the secondary market, in addition to the sale operations already contemplated in its operational framework. With this, Banxico expands the set of instruments available for the implementation of monetary policy and modernizes several procedures related to financial market infrastructure.

It is worth noting that this modification does not imply a change in the monetary policy stance, nor does it anticipate financial stability problems. Rather, it provides the central bank with greater operational flexibility to manage episodes in which its creditor position vis-à-vis the financial system could generate tensions or dysfunctions in the funding market, particularly in the event of a potential scarcity of eligible collateral assets. Through purchases in the secondary market, Banxico can temporarily reduce its creditor position and inject liquidity more efficiently, while through sales it can absorb liquidity when necessary. In this sense, the measure strengthens the functioning of open market operations and contributes to a more orderly formation of the funding interest rate, reinforcing the central bank’s capacity to implement monetary policy under different market scenarios

Peru—Economic Activity Remains Solid, While Inflation Should Ease in June

Ricardo Avila, Senior Analyst

ricardo.avila@scotiabank.com.pe

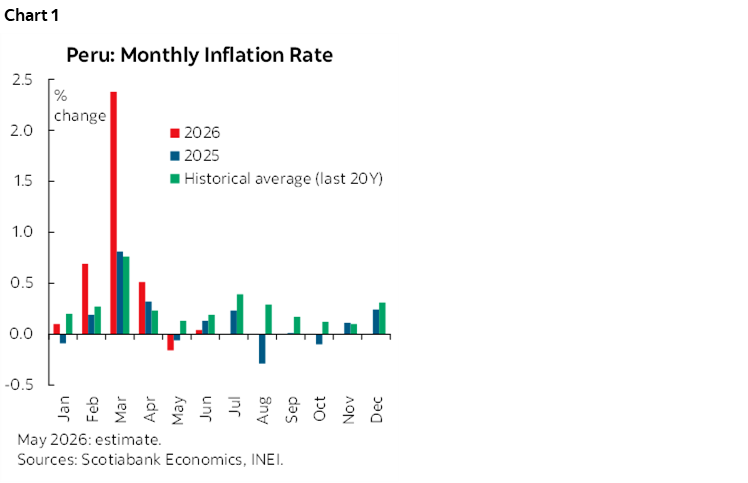

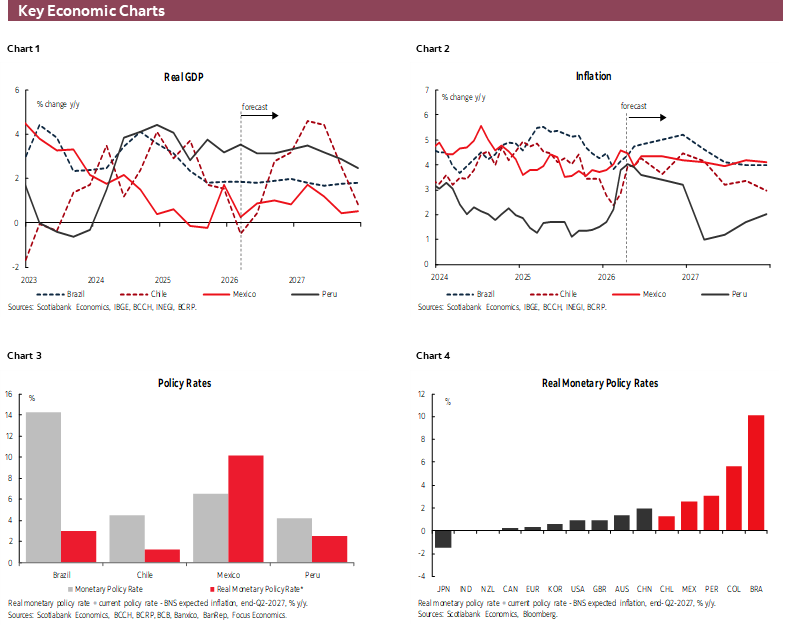

June inflation data will be released on Wednesday, July 1st. We expect annual headline inflation to correct once again (chart 1). During the month, downward pressure would mainly come from the transportation component as fuel prices have been declining since the beginning of June. This effect would be partially offset by food prices. Were it not for the El Niño Phenomenon (FEN), food prices would likely have continued to decline, as chicken prices have remained on a downtrend. However, prices of some fish species that are relevant in the basic consumption basket have started to increase, due to higher sea temperatures which cause these species to move to deeper waters, reducing catch rates. Against this backdrop, we expect monthly inflation to remain around 0.0%, while annual inflation would ease from 3.9% to 3.8%.

Regarding the policy rate, we expect the Central Bank to keep it unchanged at 4.25% in July and over the coming months of 2026 and through 2027. We consider the oil price shock to be transitory. Local fuel prices have already declined since early June and would continue to do so following the drop in international oil prices to levels close to US$70 per barrel. The El Niño Phenomenon would also generate inflationary pressures, although these would also be transitory supply shocks.

We estimate that inflation would return to the target range of 2%–3% in March 2027. In addition, 12-month inflation expectations, currently at 2.9%, would remain anchored within the target range as headline inflationary pressures gradually ease. However, if inflationary pressures prove to be persistent and push 12-month inflation expectations above the target range, there would be a risk of one or two 25 bp increases in the policy rate.

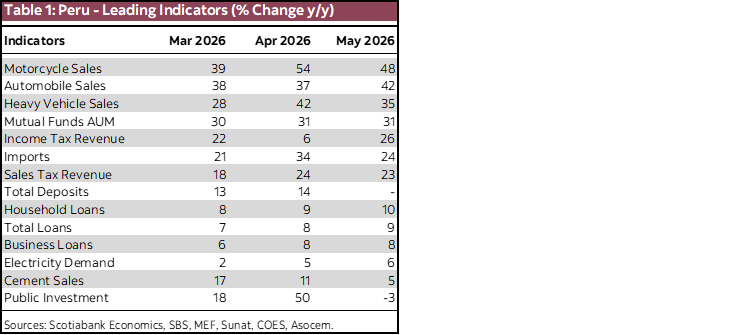

Regarding economic activity, despite the political and electoral uncertainty observed in April and May, we continue to see leading indicators showing solid momentum (table 1). The domestic demand indicators we monitor, particularly those related to private investment and private consumption, continue to post strong growth, pointing to a favourable performance of the economy in Q2-26. In terms of private investment, we note that cement demand, heavy vehicle sales, electricity demand, and business loans continue to accelerate. As for private consumption, investment fund assets, light vehicle sales, and household loans continue to expand. Finally, tax revenues, both from companies and individuals, recorded renewed growth. As a result, we expect the economy to grow by more than 3.0% in Q2-26.

Separately, the Central Reserve Bank of Peru (BCRP) presented its Inflation Report on June 19th. Among the key messages highlighted by Julio Velarde, President of the BCRP, were the following:

- Short-term leading indicators show a fairly strong dynamic, in some cases even growing at double-digit rates, which is associated with robust private investment.

- Looking ahead, one of the main risks is El Niño. The projections already incorporate a “strong” FEN scenario, which would reduce GDP growth by around 0.8 p.p. this year and by another 0.8 p.p in 2027. Even so, the BCRP maintains a growth forecast of 3.4% for 2026, similar to 2025, supported by the momentum of non-primary sectors.

- On inflation, Velarde noted that June monthly inflation will be low and that, in the coming months, the BCRP expects negative monthly inflation if fuel prices continue to decline.

- The BCRP expects the FEN to affect food prices between the end of this year and the beginning of next year. However, inflation would converge to the target range early next year due to base effects.

- For this year, the BCRP revised its inflation forecast upward from 2.4% to 3.8%, while keeping its forecast for next year unchanged at 2.0%.

- Regarding possible policy rate increases, Velarde stated that they are unlikely for now, although he did not rule them out in the future.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.