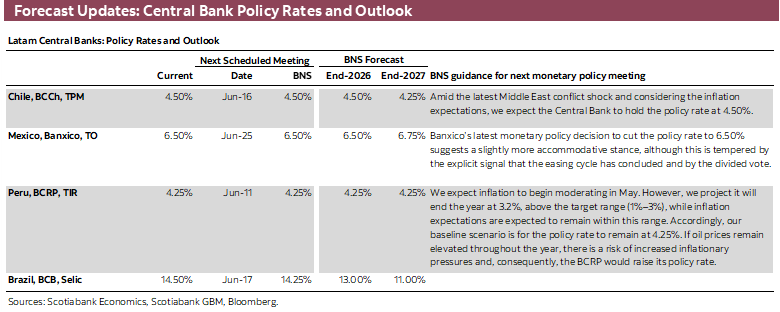

HIGHLIGHTS

- Global markets are heading into the weekend on a heavy dose of optimism backed by a possible U.S.-Iran peace agreement that they hope will be formalized over the coming days.

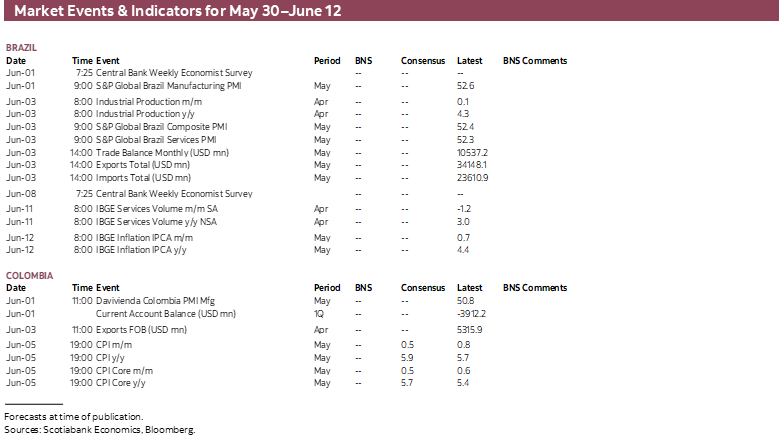

- Markets will also have to digest some key figures out of the U.S. (employment and ISM), CPI data from Peru, Colombia, and the Eurozone, Chilean economic activity, and second-tier Mexican and Brazilian data.

- On Sunday, Colombians head to the polls to determine the two presidential candidates that will face off at a likely second-round vote on June 21st. Peru holds its own second round presidential vote next Sunday, with a large share of the electorate still undecided.

- In today’s report, the team in Peru outlines their expectation for next week’s inflation print for May and go over economic indicators for April demonstrating economic resilience. Our colleagues in Mexico and Chile discuss fiscal developments in their respective countries.

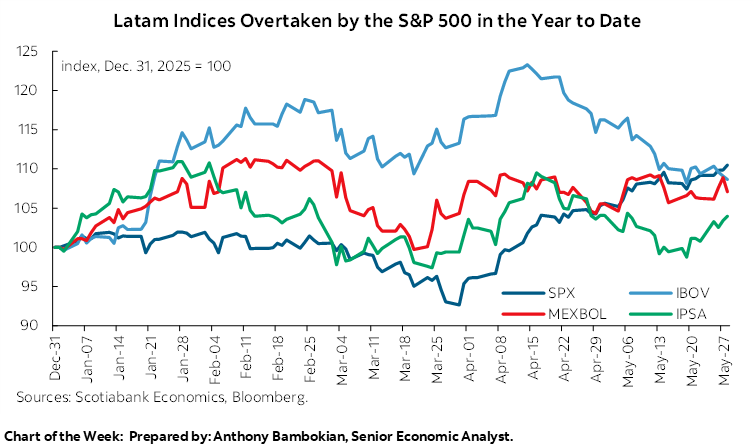

Chart of the Week

PERUVIAN CPI, CHILEAN ACTIVITY, AND COLOMBIA’S FIRST ROUND VOTE

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Global markets are heading into the weekend on a heavy dose of optimism backed by a possible U.S.-Iran peace agreement that they hope will be formalized over the coming days.

- Markets will also have to digest some key figures out of the U.S. (employment and ISM), CPI data from Peru, Colombia, and the Eurozone, Chilean economic activity, and second-tier Mexican and Brazilian data.

- On Sunday, Colombians head to the polls to determine the two presidential candidates that will face off at a likely second-round vote on June 21st. Peru holds its own second round presidential vote next Sunday, with a large share of the electorate still undecided.

- In today’s report, the team in Peru outlines their expectation for next week’s inflation print for May and go over economic indicators for April demonstrating economic resilience. Our colleagues in Mexico and Chile discuss fiscal developments in their respective countries.

Global markets are heading into the weekend on a heavy dose of optimism backed by a possible U.S.-Iran peace agreement that they hope will be formalized over the coming days. While nothing is confirmed and the usual public back and forth of denials, threats, and grandstanding continues, negotiations do seem to be trending in the right direction. But soon so should oil and gas tankers through the Strait of Hormuz or risk a reversal of the recent decline in global energy prices—and, by association, hike bets.

It is likely then that, once again, news regarding the three-month-long conflict will be the main shot-caller for next week’s market performance, but traders will also have to digest some key figures out of the U.S. (employment and ISM), CPI data from Peru, Colombia, and the Eurozone, Chilean economic activity, and second-tier Mexican and Brazilian data. In the case of Colombia, however, inflation data will be of secondary importance to the results of Sunday’s presidential election where no candidate is expected to take 50%+1, so the focus will be on the performance of the likely candidates (Cepeda, from the left, and de la Espriella, from the right) that will head to a second round contest on June 21st.

A week from Sunday, we also have Peru’s second-round presidential vote, pinning Fujimori (right) against Sánchez (left), who took respective 17.2% and 12% shares of ballots in the April 12th round. The latest polls place the former candidate ahead by around 5ppts but there remains a high share of undecided voters or who claim will submit a null/invalid vote (with wide variation in surveys from ~25% to 35%+ combined for these categories). It is anyone’s guess who will come out on top.

Ahead of the vote, we’ll get Peruvian CPI data for May at the start of the week which we expect will show a deceleration in headline inflation from 4.0% to 3.8 % y/y on the back of a 0.3% monthly decline in prices. As covered in today’s report, our team’s tracking of key items in the basket sees sizeable declines in poultry, fruits, and tubers (which have been under significant upward pressure of late) that will more than offset higher electricity bills and a roughly neutral impact of gasoline prices. With recent developments in global energy prices, and if trends were to continue, there may soon be positive news on the side of inflation expectations which at a twelve-month horizon are trending toward 3% (2.8% as of the April survey compared to 2% at the start of the year).

Chilean economic activity for April also opens the week, with the country likely to post another soft month, after a 0.1% y/y loss in March, in light of data published this morning. In April, retail sales slowed to 4.1% from 4.5% y/y, commercial activity decelerated to 3.2% from 5% y/y, and industrial production deepened its decline to 4.7% y/y from 3.3% y/y. The latter’s contraction was its worst y/y showing in around three years, driven by a 9>% decline in mining sector output where copper production fell 14.3%. The latter is, admittedly from a high base of comparison last April, but the ~400k metric tons produced last month was the lowest April total since 2003 amid declining ore grades (concentration) in aging mines and delays in the upgrading of certain sites.

Falling copper output comes at a tricky time for the Kast administration that is aiming to quickly narrow the deficit as part of its key campaign pledges, so they could’ve used increased volumes. Thankfully, higher copper prices saw the Ministry of Finance recently revising higher its projections for mining revenues, which act as a partial offset to weaker non-mining revenues and a higher expected spending bill, as discussed in today’s Weekly by our team in Santiago in their review of the latest fiscal developments in the country.

Remittances, investment, and formal employment data, as well as the results to the latest Banxico and Citi economist surveys are on tap next week in Mexico. The data should continue to show very muted economic momentum in the country while also coming at a time of growing concerns around the fiscal trajectory in response to Moody’s recent rating downgrade of Mexican debt to the lowest investment grade level. In today’s report, the team goes over the government’s optimistic fiscal assumptions that stand in clear defiance of structurally weak growth trends, with fiscal adjustments constrained by immovable social spending. We’ll also keep an eye on reports regarding USMCA negotiations as talks heat up ahead of the July 1st review. Today, the WSJ reported that the U.S.’s starting position is a 50% U.S. content requirement in autos for duty-free treatment under the trade pact (an economically unfeasible ask for Mexican automakers), within a regional content requirement sought to be higher than the current 75%.

COUNTRY UPDATES

Chile—Request for Additional Sovereign Borrowing Would Be Limited to No More than USD 2.6 bn

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

Government estimates a higher effective fiscal deficit in 2026. The Ministry of Finance released the Q1-26 Public Finance Report (IFP), which includes a relevant update of fiscal projections for this year. On the expenditure side, the government increased its 2026 estimate by USD 1.9 bn relative to the Q4-25 IFP, mainly reflecting the recognition of existing commitments typically not included, partly offset by the fiscal adjustment implemented to date. On the revenue side, projections were revised down by around USD 380 mn, largely due to lower non-mining tax revenues, only partially offset by higher mining revenues (copper and lithium) under the assumptions used in the IFP. As a result, the effective deficit widened by 0.6% of GDP, from -1.8% to -2.4%.

The IFP points to higher financing needs of USD 4.6 bn. In addition to the USD 2.3 bn increase in the estimated deficit for this year, the report incorporates higher debt amortizations of USD 0.5 bn, as well as the recognition of lower mortgage loan recoveries from the Ministry of Housing amounting to USD 1.5 bn, alongside other smaller financing needs and uses.

Accounting for higher copper and lithium prices would generate additional resources of USD 2.3 bn not included in Q1-26 IFP. The report assumes an average copper price of USD 5.46/lb for the year, below the current year-to-date average of USD 5.9/lb, implying a significant decline from current levels (USD 6.2/lb) is required to meet that assumption. This would mean copper averages USD 5.3/lb (BML) for the remainder of the year, an assumption we do not share at Scotiabank. A similar situation applies to lithium: while current prices are around USD 21/kg, the report implicitly assumes an annual average of USD 13/kg (year-to-date: USD 18/kg).

The Reconstruction bill would increase the deficit by around USD 0.9 bn this year, also not included in the report. According to the Financial Report and the Fiscal Council, the bill would reduce revenues by 0.17% of GDP in 2026 through measures such as employment tax credits and VAT reductions on housing purchases, while increasing spending by 0.06% of GDP. In total, this amounts to 0.23% of GDP, which should be incorporated as a deterioration in the deficit and is included in our estimates.

The government would need to finance only USD 2.6 bn, likely through additional debt issuance this year. Considering higher mining revenues and the Reconstruction bill, we estimate financing needs of USD 3.2 bn. However, beyond the USD 17.4 bn borrowing authorization in the Budget Law, the government also has access to the so-called “prudential margin” of USD 600 mn (Article 3, paragraph 2, Budget Law), which does not require Congressional approval and would partially offset financing needs.

Overall, our estimate of additional borrowing could decline further if ongoing expenditure containment efforts and fiscal execution lead to an improved fiscal balance. This takes place within the framework of the structural deficit convergence commitment, which must be presented by June 9th and, as announced, would imply a more demanding path than the current one. We expect this to include a faster convergence pace and, therefore, a lower deficit for this year.

The political timing for requesting additional sovereign borrowing is not trivial. Amid ongoing Senate discussions of the Reconstruction Plan, opposition scrutiny of the latest IFP projections, and ahead of the September 30th deadline to submit the 2027 Budget Bill to Congress, the government faces a constrained window to act.

Our estimate of the additional borrowing request is based on alternative assumptions for key 2026 variables, which we view as more realistic and likely to be reflected either in Congressional discussions or in the upcoming Q2-26 IFP (to be published in July). In particular, Congress is likely to challenge the assumptions for copper and lithium prices, arguing for more realistic inputs. If the borrowing discussion coincides with the next IFP release, we see it as likely that the Ministry of Finance/Budget Office adjust assumptions closer to our baseline, ultimately leading to an additional borrowing request broadly in line with our estimates.

Mexico—Fiscal Deterioration Raises Pressure on the Sovereign Rating

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

Mexico’s latest fiscal outlook points to a more challenging environment for public finances and, by extension, for the sovereign credit profile. While the country continues to benefit from important credit strengths, these are increasingly being offset by structural headwinds—namely weak economic growth, growing expenditure rigidities, and a sustained rise in debt servicing costs.

A key concern is the gap between the government’s fiscal assumptions and market expectations. The Ministry of Finance projects a deficit of around 3.6% of GDP, while consensus estimates place it above 4% and, in some cases, closer to 5%. This divergence reflects an official macro framework that appears relatively optimistic, particularly on growth. Given the sensitivity of fiscal accounts to both growth and interest rates, even a modest surprise could translate into further fiscal slippage.

This matters more in the context of structurally weak growth. Since 2018, Mexico’s economy has expanded at an average pace of less than 1%, and the medium-term outlook suggests only limited improvement. Weak growth not only constrains revenue generation, but also discourages investment, reinforcing a low-dynamism equilibrium. In addition, changes in the regulatory and institutional environment, including judicial reform and broader rule-of-law concerns, have weighed on investor sentiment. Persistent security challenges also continue to impose meaningful costs on firms, affecting productivity and raising operating expenses.

Investment trends reinforce this narrative. Fixed investment has been declining for more than a year, deepening the weakness of the cycle and limiting the economy’s capacity to recover momentum. The combination of subdued investment, low growth, and institutional uncertainty creates a negative feedback loop with direct implications for fiscal sustainability.

On the fiscal side, the deterioration appears gradual but persistent. Public debt continues to trend upward and could approach—or even exceed—60% of GDP in the coming years, a threshold that has often served as a reference point in sovereign risk assessments. This dynamic reflects not only elevated deficits, but also a significantly higher interest burden. At present, roughly 15%–18% of public revenues are being absorbed by interest payments, materially reducing the government’s available fiscal space.

More importantly, the debt dynamics have become increasingly difficult to stabilize. In an environment of low growth and high interest rates, debt stabilization would require a sizeable primary surplus—estimated at around 3.4% of GDP—which appears difficult to achieve under current conditions. A major constraint is the increasing rigidity of expenditure, particularly due to the larger share of social spending within the budget. This reduces the authorities’ room to adjust spending in response to adverse shocks and limits fiscal flexibility overall.

Mexico’s revenue structure adds to these vulnerabilities. Tax collection remains highly concentrated at the federal level, while state and local governments play only a limited role in revenue generation. At the same time, high informality continues to narrow the tax base, complicating the scope for a meaningful fiscal reform that could lift revenues without undermining investment or activity. Although there are areas with potential for improvement, including VAT, property taxation, and labour formalization, poorly calibrated measures could prove counterproductive.

Taken together, these factors help explain why rating agencies have become more cautious on Mexico’s sovereign profile. In some cases, outlooks have already turned negative or moved closer to the lower end of the investment-grade spectrum. Concerns around weak growth, rising debt, and constrained fiscal flexibility are now playing a more central role in the credit story.

That said, Mexico still retains important anchors. The external position remains broadly solid: the current account deficit is relatively low, financing continues to rely largely on foreign direct investment, and international reserves remain adequate. In addition, access to external funding remains favourable, helping contain short-term liquidity risks.

Overall, Mexico faces a more demanding fiscal backdrop, with the main risks stemming from domestic structural weaknesses rather than external imbalances. Looking ahead, the trajectory of the sovereign credit profile will depend on the authorities’ ability to align fiscal assumptions with macroeconomic realities, strengthen the revenue base, and improve spending efficiency without further undermining growth. In this setting, policy credibility and the capacity to deliver gradual but sustained fiscal adjustment will be critical to prevent additional pressure on the rating.

Peru—Economic Activity Remains Resilient Despite Electoral Uncertainty

Ricardo Avila, Senior Analyst

ricardo.avila@scotiabank.com.pe

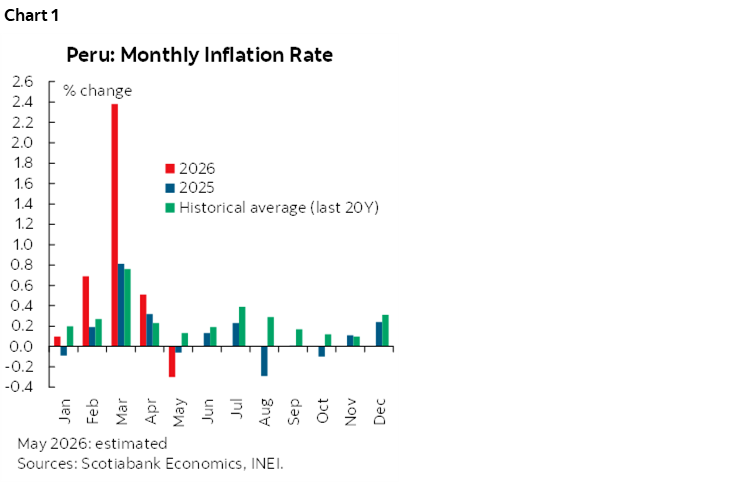

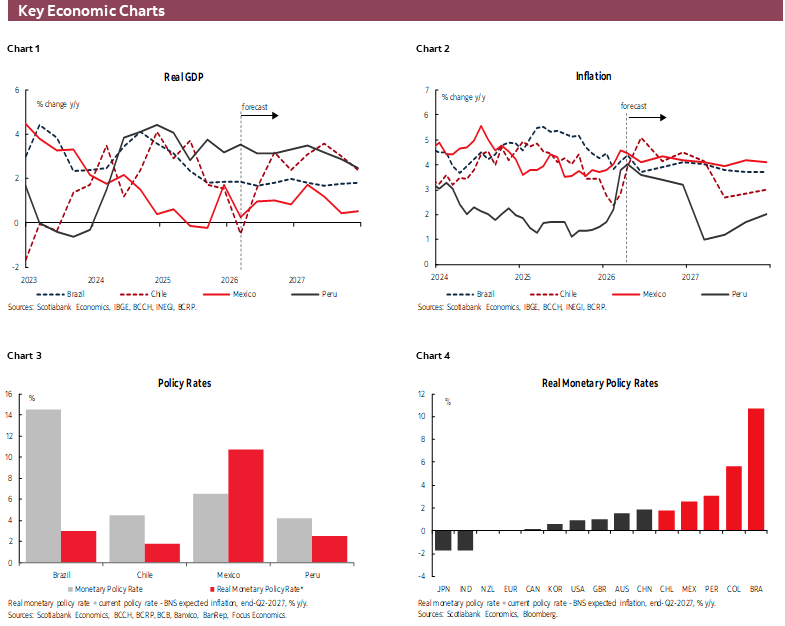

If you are reading this article in June, you have likely already seen May’s inflation data. We expect inflation to post a correction (chart 1), primarily driven by the food component, as the impact of adverse weather conditions (high temperatures) has begun to fade. This effect would be partially offset by an increase in electricity tariffs, which are linked to the exchange rate—the latter increased following the first round of elections, although it has already corrected much of that rise during May. As for the transportation component, which has driven inflation over the past two months due to higher international oil prices, we do not anticipate significant changes either upward or downward. Overall, we expect monthly headline inflation to be negative, with annual headline inflation declining from 4.0% in April to a range between 3.7% and 3.8% in May. We believe headline inflation will not return to the target range (1.0%–3.0%) until 1Q27, and we project it will stand at around 3.2% by the end of 2026.

On the other hand, economic growth in 1Q26 surprised to the upside, reaching a solid 3.5%, despite the disruption in natural gas supply in March. Domestic demand expanded by 6.6%, marking its strongest quarterly growth since 2013—excluding the post-pandemic rebound in 2021. This performance was mainly driven by the expansion of private investment, which grew by 13.2% supported by high metal prices and relatively low interest rates, as well as private consumption, which increased by 3.5% amid a recovery in the labour market and greater liquidity associated with the eighth pension fund withdrawal.

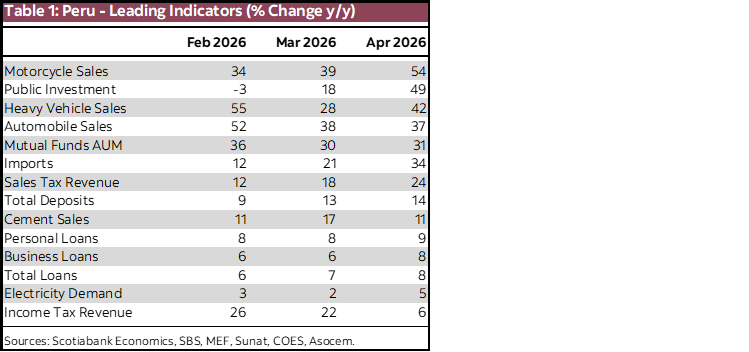

In April, despite ongoing political and electoral uncertainty, leading indicators continued to show solid economic momentum (table 1), particularly those related to domestic demand that we monitor closely, namely private investment and private consumption. This points to a strong start to 2Q26 for the economy. Regarding private investment, cement demand and heavy vehicle sales continue to grow at double-digit rates, while electricity demand and business loans remain on an upward trajectory. As for private consumption, investment funds and light vehicle sales maintained double-digit growth, while personal loans continue to expand. Finally, fiscal revenues (both from corporations and individuals) posted further growth, including double-digit increases in value-added tax collection.

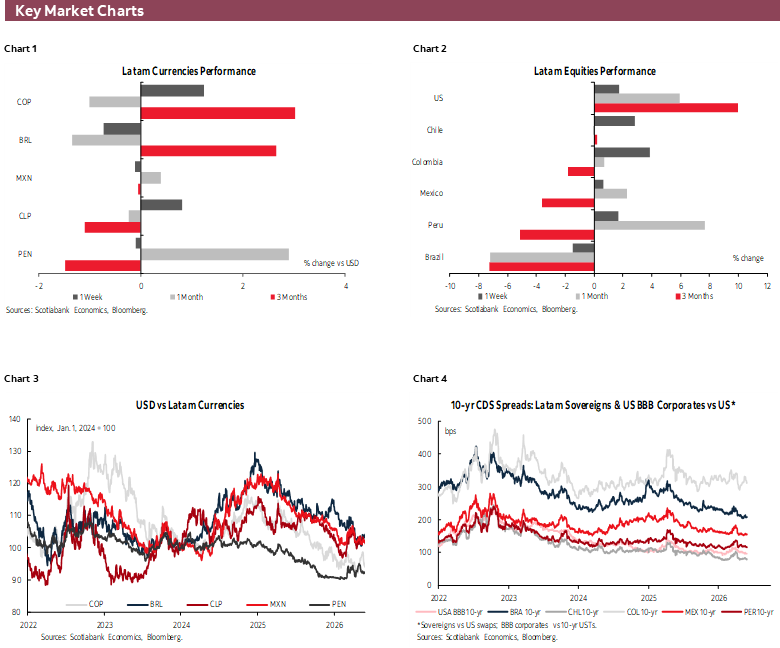

Regarding the exchange rate, as mentioned above, following the first round of elections, the PEN depreciated by 3.9%, moving from 3.39 to 3.52 soles per dollar, in contrast to its regional peers, which were appreciating. However, during May, the PEN reversed much of that depreciation, closing the month at around 3.41 soles per dollar. Looking ahead, our baseline scenario assumes that the next government will maintain an investment-friendly stance and a responsible fiscal policy. Under this scenario, we expect the exchange rate to fluctuate between 3.30 and 3.35 soles per dollar. Otherwise, it could reach levels around 3.70. We do not anticipate it reaching or exceeding 4.00, as seen in 2021, given currently favourable metal prices, higher levels of international reserves held by the central bank, and limited upward pressure from the DXY index.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.