HIGHLIGHTS

- Anxiety over the crumbling U.S.-Iran ceasefire and shaky AI sentiment dictated market moves in recent days and may continue to do so next week (alongside more Q2 earnings reports) given a fairly empty U.S. data calendar.

- In Latam, Mexico’s calendar has the most on offer with May retail sales and economic activity, mid-July CPI, and June unemployment data, while global PMIs, Canadian and U.K. CPI, and the ECB’s rate decision are the G10 highlights.

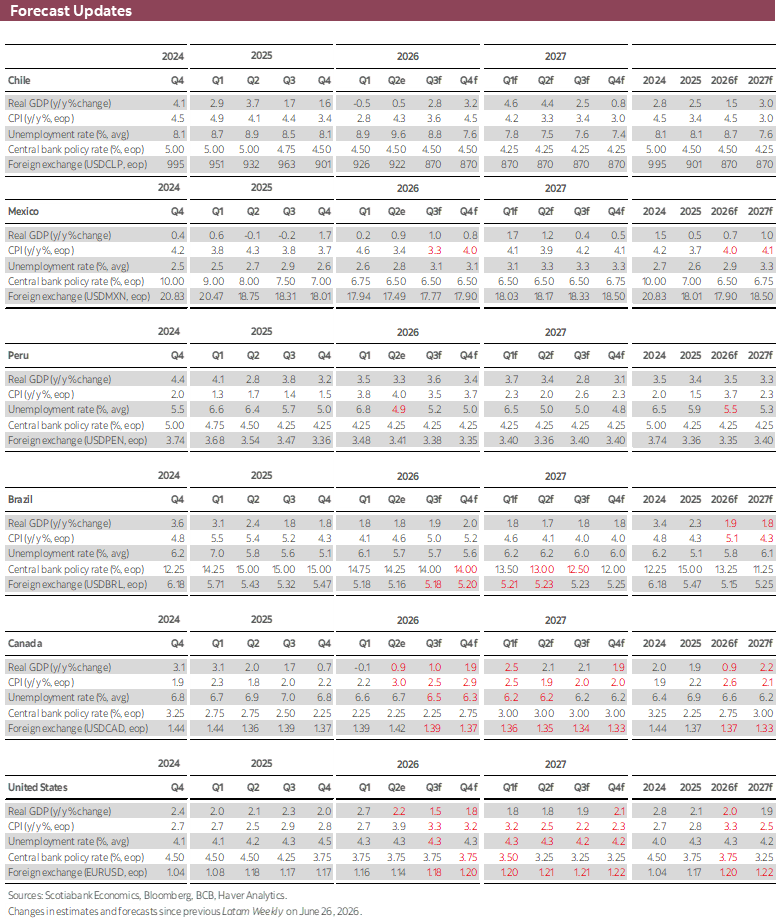

- In today’s report, the team in Mexico covers the country’s recent economic performance and prices trends. Two solid activity gains with underwhelming breadth point to a possible retreat in May data, while slowing inflation mostly reflects a correction of the surge in vegetable prices earlier in the year.

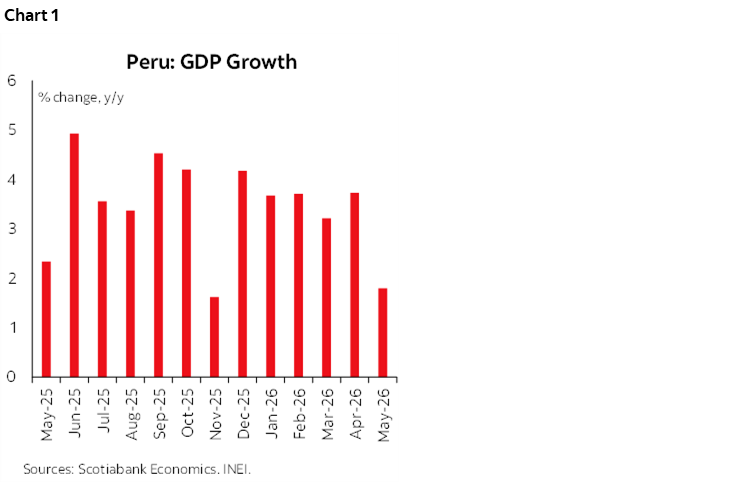

- Peru’s May growth stumble is the focus of our economists. The 1.8% y/y GDP increase was the slowest in six months at roughly half of April’s 3.7% expansion, but it mostly reflected a big drag from El Niño while demand metrics and drivers remain in strong shape.

Chart of the Week

MEXICO IN FOCUS, PERU’S GDP TAKES AN EL NIÑO HIT

Juan Manuel Herrera, Director

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Anxiety over the crumbling U.S.-Iran ceasefire and shaky AI sentiment dictated market moves in recent days and may continue to do so next week (alongside more Q2 earnings reports) given a fairly empty U.S. data calendar.

- In Latam, Mexico’s calendar has the most on offer with May retail sales and economic activity, mid-July CPI, and June unemployment data, while global PMIs, Canadian and U.K. CPI, and the ECB’s rate decision are the G10 highlights.

- In today’s report, the team in Mexico covers the country’s recent economic performance and prices trends. Two solid activity gains with underwhelming breadth point to a possible retreat in May data, while slowing inflation mostly reflects a correction of the surge in vegetable prices earlier in the year.

- Peru’s May growth stumble is the focus of our economists. The 1.8% y/y GDP increase was the slowest in six months at roughly half of April’s 3.7% expansion, but it mostly reflected a big drag from El Niño while demand metrics and drivers remain in strong shape.

It’s been a rocky few days for global markets, as AI-related risk aversion and the crumbling U.S.-Iran ceasefire trigger weekly losses for most of the globe’s major equity indices. Heading into the weekend with fears of a possible escalation of U.S. strikes against Iran, September WTI oil futures are on track for their first $80/bbl+ close since mid-June, nearing a 20% increase from the early-July lows.

While Fed hike bets took a step back in recent days thanks to a CPI undershoot, external price risks have clearly risen for global central banks in the middle of the rate decisions period; the BoC met a couple of days ago, the ECB decides on policy next Thursday, and the Fed’s communications blackout begins tomorrow ahead of its July 29th announcement.

With limited U.S. data to distract markets, we may see greater market sensitivity to geopolitical or company news headlines as well as a beefier 2Q earnings release schedule that includes Alphabet, Intel, and Tesla. Global PMIs due on Friday are the G10 data highlight alongside Canadian and U.K. CPI (and employment data for the latter), while the main economic event is the ECB’s expected rate hold on Thursday where guidance regarding a possible September hike will be the focus.

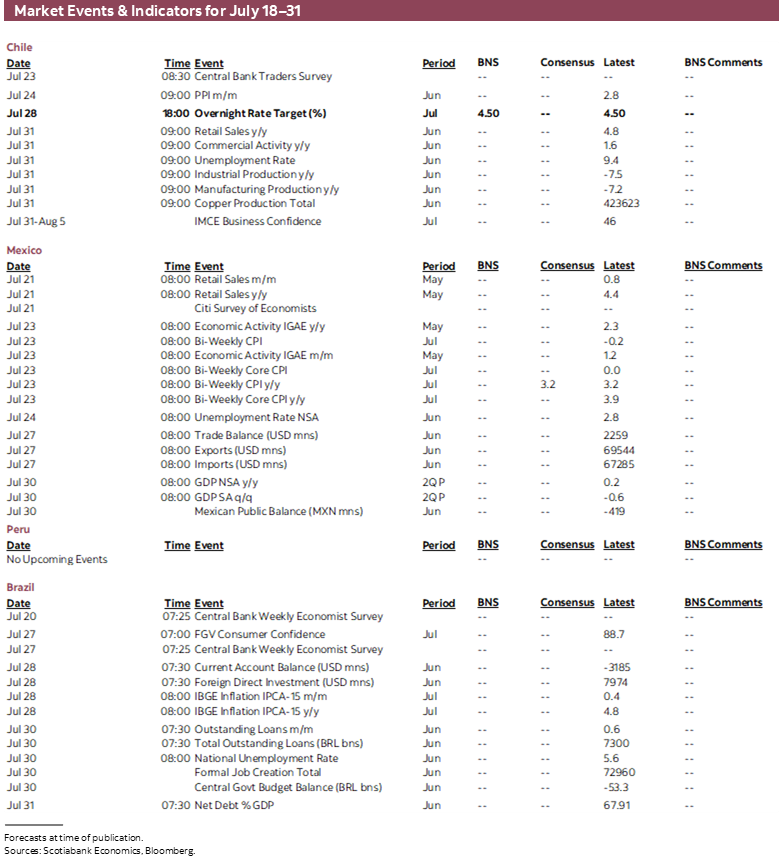

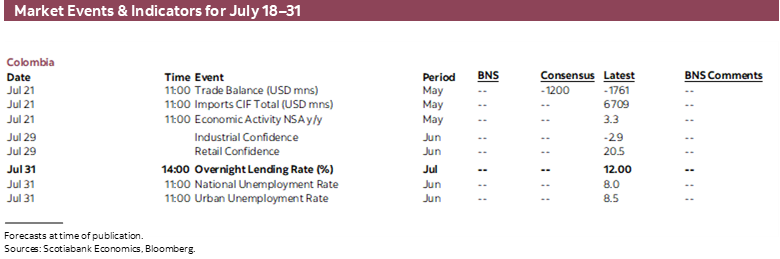

In Latam, Mexico’s calendar has the most on offer with May retail sales and economic activity, mid-July CPI, and June unemployment data. Elsewhere, Colombia also has May economic activity data on tap, and Chile’s schedule only includes June PPI and the BCCh’s traders survey. Brazil and Peru’s weeks have nothing noteworthy. Colombian markets are closed on Monday, and those in Peru are shut on Thursday; note that Keiko Fujimori takes the presidency on July 28th.

Mexico’s economy has shown tentative signs of recovery in recent months, averaging a 1% y/y expansion in the six months to April compared to practically null six-month average growth over the January to September 2025 period. In March and April, the economy expanded by 1.4% and 2.3% y/y thanks to respective 0.6% and 1.2% m/m gains that were the best two-month run since 2020. The broader uptrend was stained by a large 1% m/m drop in January, however, which contributed to a quarterly GDP decline, but recent data now point to a quarterly GDP rebound in Q2.

In today’s report, the team in Mexico go over the country’s recent economic performance and prices trends. When looking at the past two months, the secondary sector has got a lift from mining and construction output, with the latter supported by residential building (with public programs support) and a partial recovery in public works following steep annual declines after the end of large infrastructure projects (this time World Cup preparations acted as a tailwind, for instance). On the flip side, the recovery remains uneven, and the weak performance of the food and accommodation and restaurants sector (at least in pre-World Cup data) is particularly worrying—and perhaps more reflective of the muted hiring and weak confidence backdrop. It’s also tough to see Mexico stringing a third month of solid monthly gains so we will likely see a pullback next week; industrial production fell by 0.8% m/m in May after its strong 2.1% gain in April.

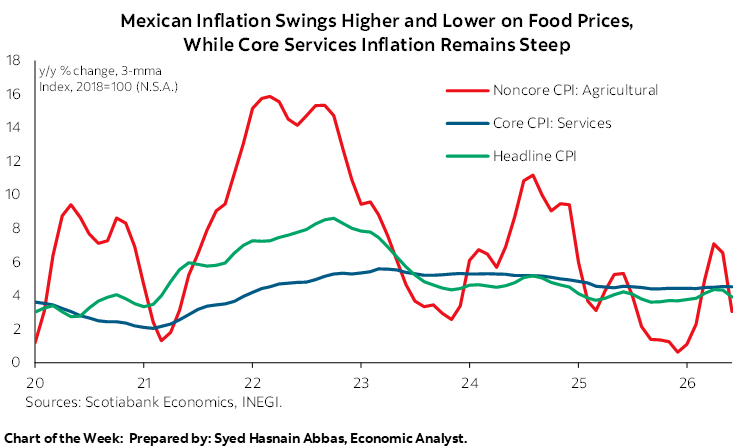

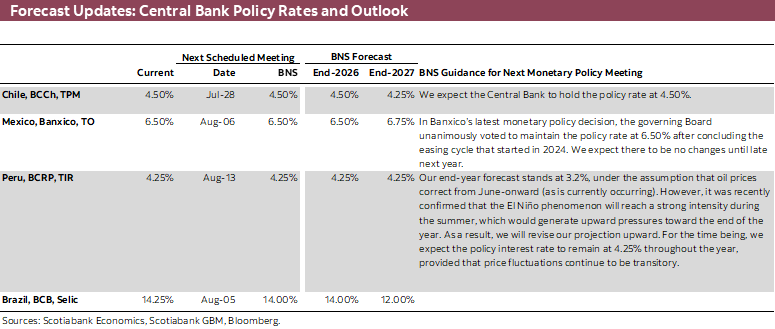

We project that Mexican inflation slowed a touch in the first half of July, at around 3.1% y/y compared to 3.2% in H2-Jun, thus roughly on Banxico’s target and way off the recent high of 4.6% y/y in the first half of March 2026. Just how fresh food prices pressured inflation higher a few months ago, their recent cooling has helped drag inflation lower with the added support of declines in core goods inflation that may reflect the resilience of the Mexican peso. Yet, core services inflation remains extremely sticky, failing to materially ease from the mid-4s zone it has found itself in since Q2-25. Without evidence of decelerating core services inflation, it’s tough to see Banxico choosing to loosen policy settings in the near future (with the added concern of the possibility of Fed hikes).

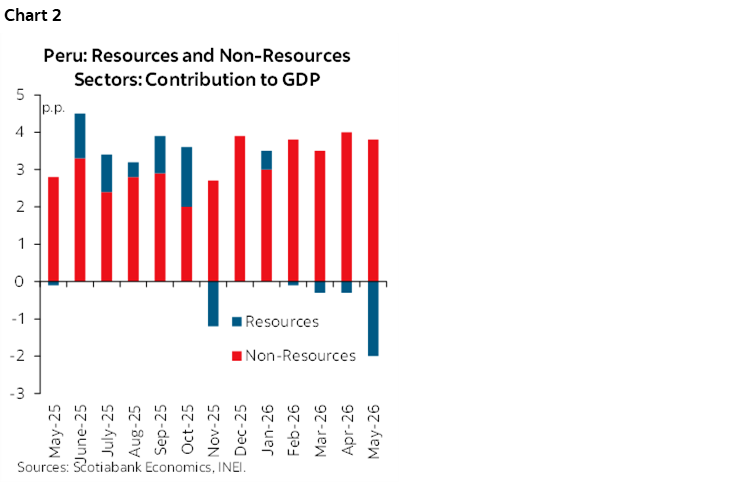

The team in Peru covers the country’s growth stumble in May GDP data published earlier this week. The 1.8% y/y GDP increase was the slowest in six months at roughly half of the April’s 3.7% expansion. While a deceleration was expected given leading indicators for the various sectors and a factoring in of El Niño headwinds, the reading still surprised to the downside. Combined, the fishing, primary manufacturing (mainly fishing-related), and agricultural sectors acted as a ~2ppts drag on economic activity growth for the month. This narrow-based weakness stands in contrast to the solid performance of domestic demand as per construction, wholesale and retail trade, or hospitality industry readings that are a better reflection of the underlying momentum in Peruvian GDP growth that should continue to lead its regional peers.

COUNTRY UPDATES

Mexico—Inflation and IGAE Could Send Positive Signals in Mexico

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

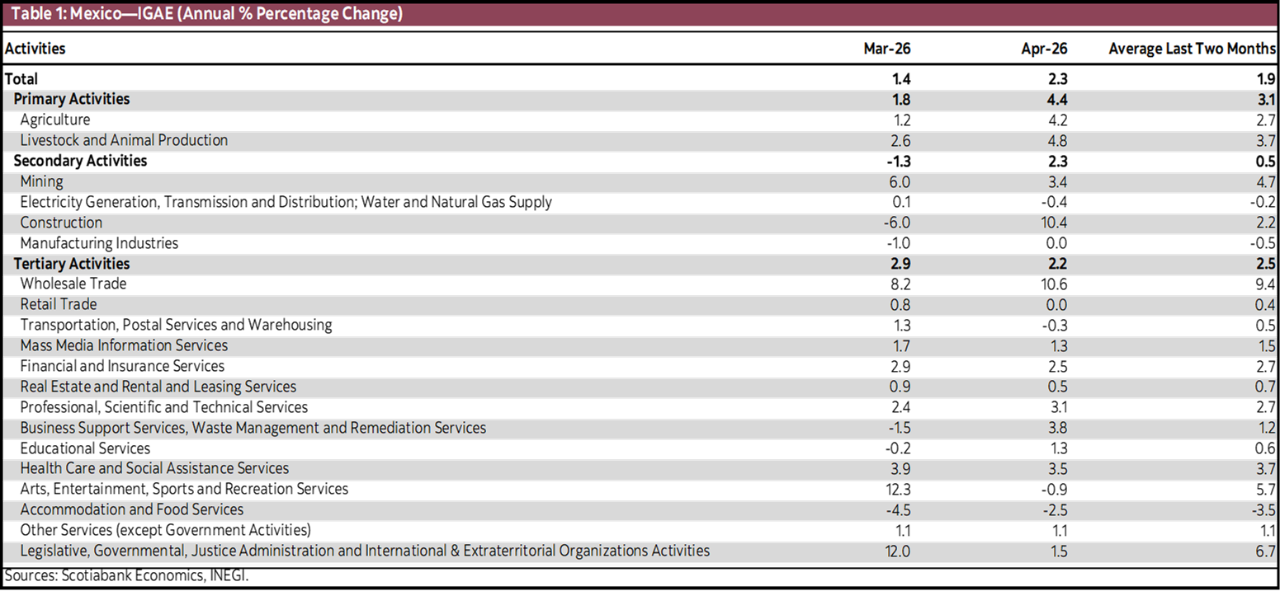

Next week, two indicators will be released that could help confirm whether the Mexican economy is entering a recovery phase. First, May’s IGAE will make it possible to assess whether the shift in the trend observed over the previous two months is consolidating, after economic activity grew 1.4% year-over-year in March and 2.3% in April. If this trajectory is confirmed, it could be interpreted as a sign of recovery after a first quarter that surprised to the downside, prompting downward revisions to 2026 growth expectations.

Part of this improvement is explained by the performance of specific sectors (table 1). Within secondary activities, mining and construction stood out. The former benefited from higher extractive output, particularly oil and mining production, after several months of weakness. Construction, meanwhile, consolidated its role as one of the main growth drivers, supported by infrastructure projects, works related to the 2026 FIFA World Cup, and the execution of previously committed public and private investments. In services, wholesale trade, recreational, cultural, and sports services, health services, and legislative, government, and justice-related activities stood out.

In detail, wholesale trade was the activity that contributed the most to the increase in the IGAE, likely reflecting inventory rebuilding, higher imports of inputs and equipment, and stronger logistics activity associated with investment projects. Recreational, cultural, and sports services may also have benefited from the 2026 FIFA World Cup, boosting demand for entertainment and recreational activities, particularly in Mexico City, Guadalajara, and Monterrey. Health and social assistance services also stood out, supported by higher demand for medical care and increased health spending, while legislative, government, and justice-related activities performed better in line with greater public-sector activity and spending.

However, the recovery remains uneven. Among the weakest-performing sectors are temporary accommodation and food and beverage preparation services, possibly affected by weaker tourism and consumption demand despite the FIFA World Cup; manufacturing, which continues to reflect industrial weakness, trade uncertainty, and subdued investment momentum; and public utilities such as electricity, water, and gas, which remain a bottleneck for productive activity. Overall, these results suggest that economic activity could rebound during the second quarter of 2026, supported by both a lower base of comparison and World Cup-related spending. Nevertheless, there are still no structural changes that would allow us to conclude that the economy has exited its stagnation phase, making it likely that growth will moderate again in the third quarter and return to the weak dynamics observed at the beginning of the year.

In addition, inflation for the first half of July will also be released next week. We expect annual inflation at 3.09%, below the 3.18% observed in the second half of June. If confirmed, this would be the lowest reading since December 2020 and would place inflation practically in line with Banco de México’s target.

This renewed slowdown would be mainly explained by lower pressures in the non-core component and by a more broad-based moderation in goods within core inflation. In June, the main source of relief came from agricultural and livestock products, particularly the 5.56% monthly decline in livestock products and sharp drops in tomatoes (-38.98%), serrano peppers (-26.88%), and poblano peppers (-40.43%), following the significant pressures recorded earlier in the year. At the same time, goods continued to decelerate, partly supported by peso appreciation, allowing core inflation to decline from 4.19% to 4.03% year-over-year.

Despite this improvement, inflationary pressures remain concentrated in services, where inflation eased only slightly from 4.52% to 4.49% year-over-year and continues to be Banco de México’s main source of concern. Within this component, persistent increases stand out in education (5.94%), housing (3.62%), and other services (5.12%), as well as owner-occupied housing, prepared foods, small restaurants and eateries, personal care products, and housing rents, all of which continue to exert pressure on core inflation.

Looking ahead, although headline inflation could continue to benefit temporarily from lower pressures in agricultural and livestock products, the disinflation process does not yet appear fully consolidated. In addition to the stickiness observed in services, energy prices and government-authorized tariffs recorded inflation of 3.46% in June, their highest level in eleven months, while products such as potatoes (9.32%) and avocados (24.53%) continued to post significant increases. In this context, Banco de México is likely to maintain a hold stance until it observes a clearer and more sustained moderation in core inflation, particularly in the services component.

Peruvian Economy Likely Expanded by Around 3.0% in Q2 2026

Pablo Nano, Deputy Head Economist

pablo.nano@scotiabank.com.pe

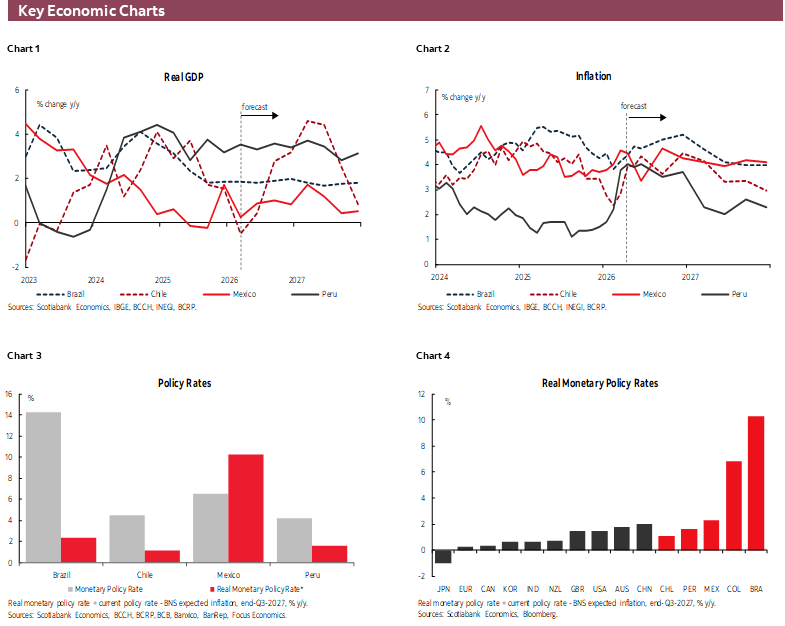

According to official data released by INEI, Peru’s GDP grew 1.8% y/y in May, marking its slowest pace of expansion in the last six months (chart 1). This figure came in slightly below our estimate of 2.3% and the 3.1% expected on average by market analysts.

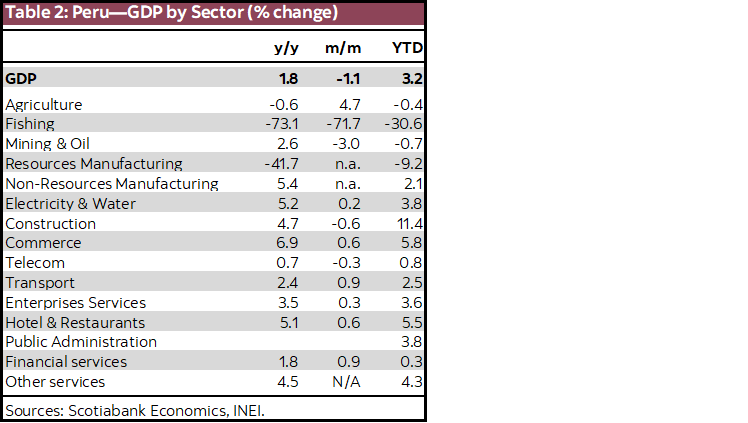

The slowdown relative to the 3.6% growth recorded during the first four months of the year was largely anticipated, given the impact of the El Niño phenomenon on the fishing, primary manufacturing, and agricultural sectors (table 2). Together, these sectors subtracted approximately 2 percentage points from GDP growth in May (chart 2). Meanwhile, sectors linked to domestic demand maintained their positive momentum, expanding by close to 5.0% year-over-year, with construction, commerce, and non-resources manufacturing standing out.

For June, we estimate that the impact of El Niño on economic activity was more moderate, reducing GDP growth by approximately 1 ppt. This reflects both lower anchovy landings and weaker agricultural output caused by reduced crop yields. As a result, the Peruvian economy would have closed Q2 2026 with growth of around 3.0% y/y, below the 3.5% y/y recorded in Q1 2026. Nevertheless, it is important to note that the second quarter is seasonally the period when primary sectors account for the largest share of GDP. Therefore, if El Niño continues to affect these sectors in the coming months, its impact on overall economic growth should become less pronounced.

DEVELOPMENTS IN MAY

As is well known, a weak Coastal El Niño event began in March 2026 and has since intensified to a strong event, according to forecasts from ENFEN, Peru’s official agency responsible for monitoring El Niño conditions. Current projections suggest that these conditions will persist through Q1 2027.

El Niño is characterized by unusually warm sea surface temperatures, which in turn raise atmospheric temperatures. The first of these effects has significantly impacted Peru’s anchovy fishery. Anchovy, the country’s most important fishing species, and the primary input for fishmeal production, typically thrives in colder waters. As ocean temperatures rise, anchovy stocks tend to migrate southward or move into deeper waters, making them more difficult to catch. Consequently, total catches fell to only 32 thousand metric tons in May 2026, compared with 1.33 million metric tons in May 2025. An additional indirect effect was a decline in fishmeal production, which weighed on resources manufacturing activity.

Agricultural production also began to feel the effects of higher temperatures. Domestic-market crops such as olives, quinoa, and onions faced adverse growing conditions, leading to lower output. Agricultural export crops were likewise affected, albeit to a lesser extent. In particular, the production of cocoa, coffee, and avocados declined, although this was partially offset by increased production of blueberries and grapes.

On a more positive note, non-resources sectors tied to domestic demand continued to perform strongly. The construction sector remained particularly dynamic, in line with double-digit growth in private investment driven by improving business sentiment. The commerce sector also posted robust growth, supported by higher employment, rising household incomes, and stronger consumer confidence. These favourable conditions have even pushed new vehicle sales to record levels. In addition, stronger household spending supported the hotels and restaurants sector (+5.1%), reflecting increased consumption of meals away from home.

Bottom line: While the intensification of El Niño significantly weighed on Peru’s primary sectors during Q2 2026, the resilience of domestic demand-driven activity continued to provide an important support for overall economic growth. With the direct impact of El Niño probably moderating in coming months, GDP growth should remain backed by private investment, employment gains, and stronger household consumption.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.