HIGHLIGHTS

- Banxico’s Thursday rate decision is next week’s highlight in Latam, as the last of the major central banks to decide on monetary policy in June following a parade of announcements over the past couple of weeks. A rate hold is all but certain, so guidance will again be in the spotlight.

- Mexican economic activity and retail sales data, as well as Mexican and Brazilian mid-month CPI figures are the regional data highlight, with generally empty release calendars in Chile, Peru, and Colombia. Global markets will focus on S&P PMIs, U.S. PCE, and Canadian CPI releases.

- In Peru, attention remains on the formalization of Fujimori’s likely victory in the second round presidential election. In Colombia, markets will open next week to the results of Sunday’s second round vote with odds heavily favouring conservative independent Abelardo de la Espriella.

- In today’s report, the team in Peru analyzes the latest expectations for El Niño, providing estimates for its possible economic impact. Our economists in Mexico cover the latest batch of aggregate demand figures for Q1-26 which showed a deepening of investment weakness.

Chart of the Week

BANXICO DECISION, COLOMBIA RESULTS, MIXED DATA SLATE

Juan Manuel Herrera, Director

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Banxico’s Thursday rate decision is next week’s highlight in Latam, as the last of the major central banks to decide on monetary policy in June following a parade of announcements over the past couple of weeks. A rate hold is all but certain, so guidance will again be in the spotlight.

- Mexican economic activity and retail sales data, as well as Mexican and Brazilian mid-month CPI figures are the regional data highlight, with generally empty release calendars in Chile, Peru, and Colombia. Global markets will focus on S&P PMIs, U.S. PCE, and Canadian CPI releases.

- In Peru, attention remains on the formalization of Fujimori’s likely victory in the second round presidential election. In Colombia, markets will open next week to the results of Sunday’s second round vote with odds heavily favouring conservative independent Abelardo de la Espriella.

- In today’s report, the team in Peru analyzes the latest expectations for El Niño, providing estimates for its possible economic impact. Our economists in Mexico cover the latest batch of aggregate demand figures for Q1-26 which showed a deepening of investment weakness.

It’s quieting down on the monetary policy front next week with most of the globe’s major central bank decisions behind us until the next round over the second half of July. There were no surprises over the past few weeks as far as policy rate adjustments are concerned, with all central banks meeting expectations for respective rate cuts, holds, or hikes except for Russia’s—which announced a smaller than expected cut. There were, however, a few surprises on the guidance front, most notably from the Fed with Warsh’s first decision at the head of the U.S. central bank turning out fairly more hawkish than traders or economists anticipated.

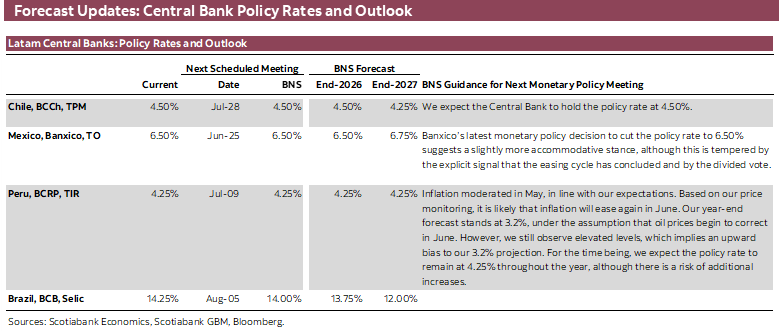

Next week, markets will be paying close attention to the parade of central bankers across media and speeches for guidance regarding the future path for policy rates. At writing, markets are pricing in cumulative hikes by year-end in the order of ~35–40bps from the Fed, ECB, and BoE, ~25bps from the BoJ, and ~15bps from the BoC and RBA among the key advanced economies. It’s a bit tougher to get a read on market-implied rate expectations for Latam given shallower derivatives markets, but these sit at around 50bps in total hikes from the BCB according to Bloomberg calculations, while our traders estimate that, by year-end, markets are eyeing no change in BCCh rates and roughly 25bps in tightening from Banxico.

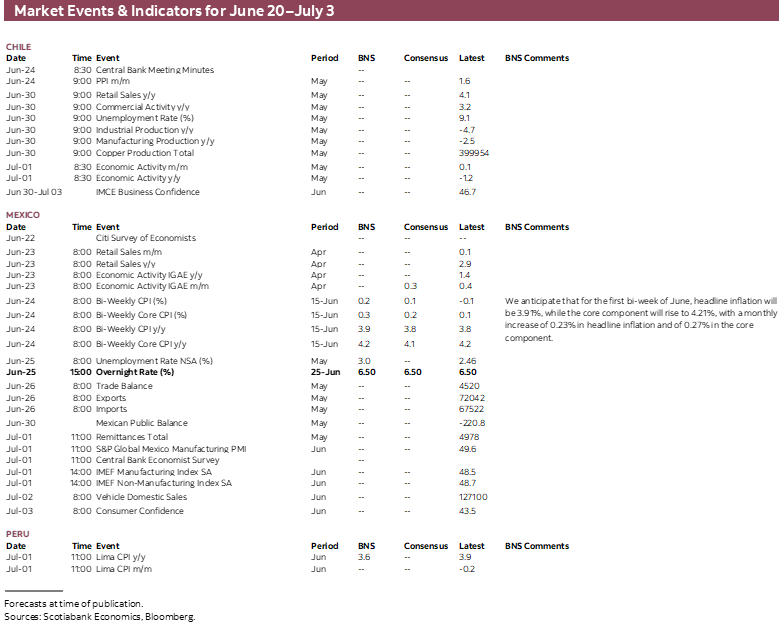

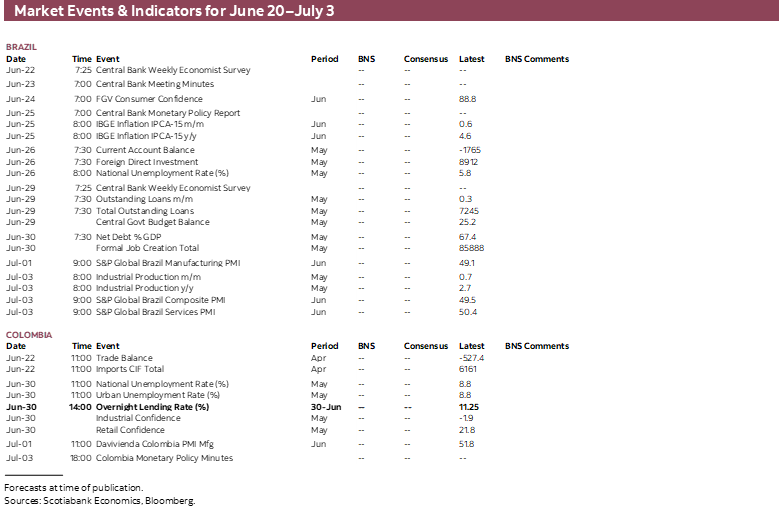

Banxico’s Thursday rate decision is next week’s highlight in Latam, with Mexico’s calendar also including April retail sales and economic activity data on Tuesday, H1-Jun CPI on Wednesday, May unemployment on Thursday, and May international trade on Friday. Brazil’s schedule follows as the next busiest, with the minutes to the latest BCB’s rate decision out on Tuesday followed on Thursday by the bank’s monetary policy report and June IPCA-15 inflation. Chile’s central bank minutes are also due on Wednesday alongside May PPI, while Peru’s and Colombia’s calendars are bare of key data, although markets are certainly much more focused on electoral developments. For the latter, odds are highly in favour of Abelardo de la Espriella (independent conservative) winning over Iván Cepeda (left-leaning, incumbent party) in Sunday’s presidential election, but there’s always at least a small chance that undecided voters shift the tide on election day. Beyond Sunday’s vote, the focus will be on policy plans and possible protests.

In Peru, Fujimori’s lead over Sánchez currently stands at ~45k votes with 99.5% of ballots counted with around 500 of these still due to be scrutinized and tallied by the national election jury (JEE). Statistically-speaking, Fujimori came out the winner of the second-round presidential election, but the JEE has taken up Sánchez’s appeal for the annulment of ballots from ~1,750 voting stations in Lima (~350k votes). A ruling is expected next week with a likely denial of this as well as some other unresolved matters paving the way for Fujimori to be declared the winner in early-July.

In today’s report, our economists in Peru discuss the latest developments on the El Niño front as well as its possible economic implications. The country’s agency responsible for monitoring El Niño as well as U.S. government experts concur in their assessment that the climate phenomenon is expected to intensify in the coming months and possibly level up to a “strong” magnitude next summer (December–March in the southern hemisphere). According to our team’s estimates, the current episode would shave off about 0.2ppts from 2026 GDP growth considering the effects that it is already having on the country’s fishing and agriculture sectors. On the flip side, demand-side economic data and an expected sentiment boost from the results of the presidential election translate into an upside bias for their 3.2% GDP growth forecast for the current year.

There should be no surprises at Banxico’s announcement on Thursday, with a rate hold at 6.50% all but certain. Mexican officials remain caught between upside inflationary risks and downside growth risks. On the inflation side, risks are present in relative isolation from developments in energy markets due to caps and subsidies on gasoline prices, so unlike other central banks Banxico does not get to turn more dovish on the back of the latest correction in crude oil prices. Some small downward impact should show up in inflation data, but Mexico’s inflationary risks are by and large driven structural frictions that are keeping prices growth elevated; core services inflation has hung around 4.5% since early-2025 with no signs of slowing. We estimate that inflation accelerated in H1-Jun data due on Wednesday, from 3.8% to 3.9% y/y, which should keep Banxico in a cautious stance pointing to no more rate cuts in store over the balance of the year.

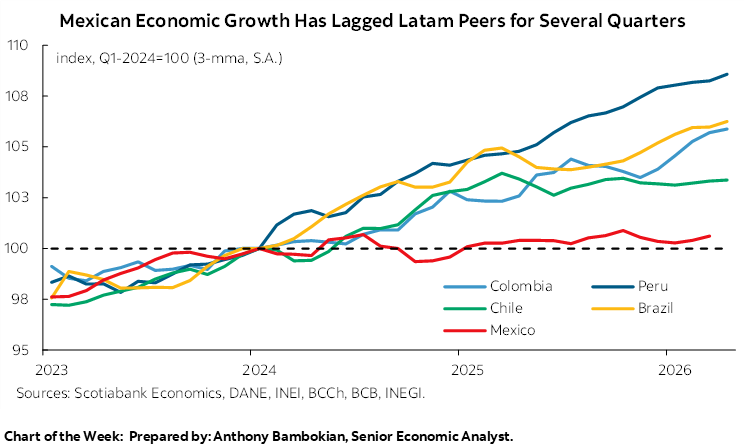

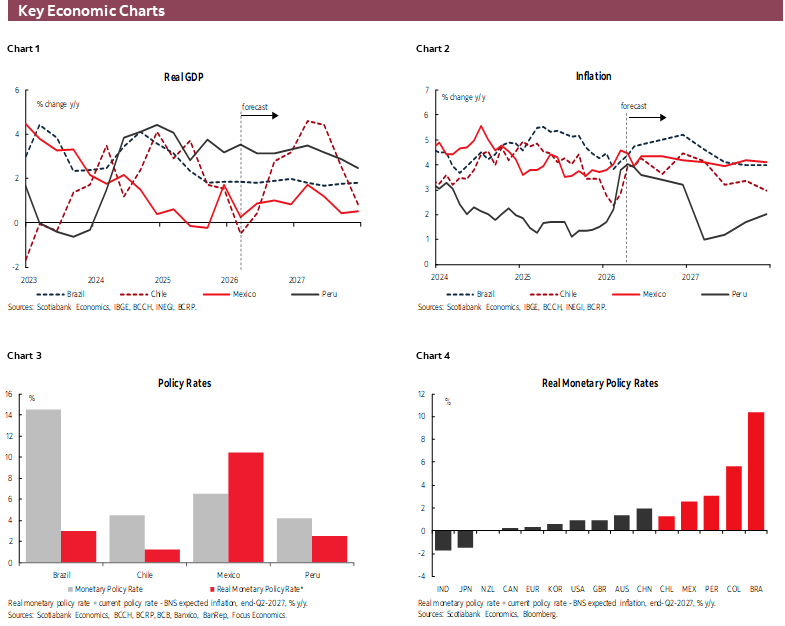

On the growth front, Tuesday’s April economic activity and retail sales data should both show a solid pick-up in y/y terms from respective 2.9% and 1.4% gains in March. However, this acceleration will mainly reflect a weak base of comparison in April 2025 when economic activity contracted by 1.6% y/y (its worst print since early-2021) and retail sales shrank 1.5% y/y. From a longer-term perspective, Mexican economic activity has barely grown since Q3-23 due to weakness in construction, mining, and manufacturing that has been only offset by some positive yet soft momentum in services output. In contrast, taking Q1-24 as the starting point (as shown in the front-page chart), Mexico’s Latam peers’ economies have expanded by as high as ~8% in the case of Peru to as low as ~3% in Chile—well above Mexico’s 0.3% gain over the period.

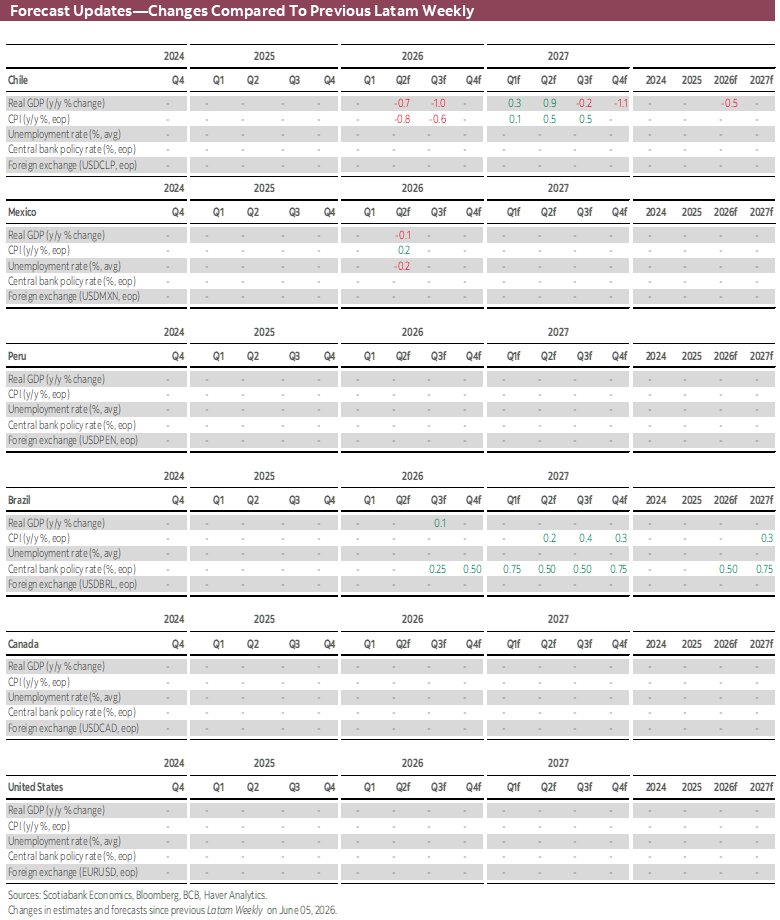

In today’s Weekly, our economists in Mexico look at Q1-26 aggregate demand data published earlier this week that provides details on GDP from an expenditure standpoint. The data showed that investment contracted further (down 1.9% q/q SA and 3.5% y/y) to reach its lowest level since 1Q-23 as it extended its run of quarterly declines that began in 4Q-24. This time around, however, it was a sharp drop in private investment of 3.5% q/q (worst since 2020) that weighed on overall capital formation. Private consumption also slipped by 0.8% q/q (but up 2.2% y/y NSA). Although this may have been more of an outsized temporary pullback after five straight quarterly increases, labour market developments also present downside risks.

Outside of Latam, the market’s attention will be on June global PMI figures out on Tuesday that come at a tricky time. The U.S.-Iran 60-day-negotiations peace deal announced earlier this week has sharply reduced energy prices and supply risks and cooled broad economic uncertainty, but S&P’s surveys may only partly reflect this lessening of risks so next week’s prints are likely more of an in-between read into global economic conditions; some improvement is nevertheless expected. It is likely that U.S. May PCE numbers out on Thursday will be the biggest market mover data-wise, coming on the heels of this week’s hawkish FOMC announcement that lifted Fed hike bets. Canada publishes May CPI data on Monday with the BoC’s meeting minutes scheduled for Wednesday. On the equities front, Micron’s results will be another test for AI optimism in markets, and Middle East headlines will remain an important influence on energy prices as traders monitor how quickly flows through the Strait of Hormuz are rebounding.

COUNTRY UPDATES

Mexico—Aggregate Demand Shows Limited Gains Amid Persistent Weakness in Investment

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

Last Thursday, data on Quarterly Supply and Use and Gross Savings for the first quarter of 2026 were released, confirming—along with the GDP figure published a few weeks ago—that the Mexican economy is experiencing a period of structural weakness and a slow start to the year.

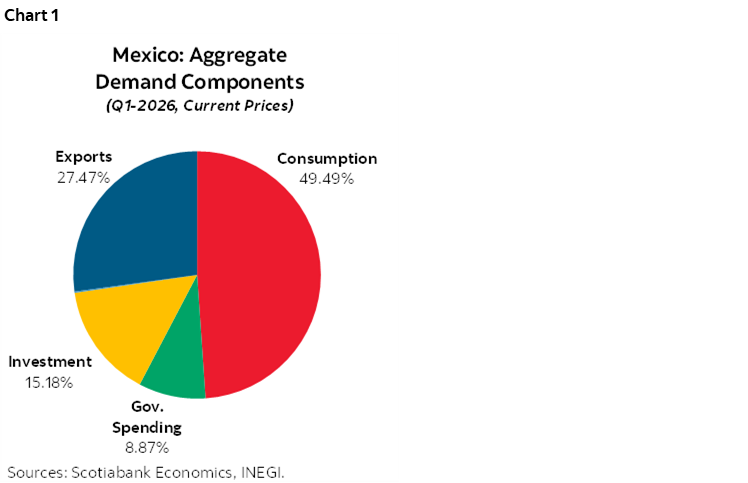

The composition of aggregate demand has remained relatively stable in recent quarters (chart 1); however, the deterioration in investment stands out. In the first quarter of 2026, investment returned to levels similar to those observed in 2021, reaching 15.18% of GDP. As a result, investment remains at one of its historically lowest levels in Mexico. This component has shown negative performance since the fourth quarter of 2024 and, in the latest reading, posted an annual decline of -3.29%. By type of good, the components of the Gross Fixed Capital Formation Indicator have also registered monthly setbacks, with declines in construction (-8.49% in March) and in machinery and equipment (-1.46%). At the same time, private investment has accumulated 19 months of declines or stagnation, while public investment has shown erratic behavior over the same period, with variations ranging from 6.55% to -10.95%.

Regarding private consumption, it continues to dominate the demand side, accounting for 49.49% of GDP, with some resilience in the latest quarter and growth of 3.19%. In the breakdown, the upward trend in recent months has stood out in imported goods—which reached a variation of 16.7% in March—compared with domestic goods, which have shown a less favourable outlook: they fell 0.3% in January and 1.5% in February before recovering to 0.7% in March. Given this share, it is clear that consumption will remain a relevant factor supporting aggregate demand in 2026; however, this mixed performance increases downside risks, alongside the low dynamism of the labour market and the reduction in real purchasing power observed in recent months.

Accounting for 27.8% of GDP, exports of goods and services fell -0.52% during the quarter. Although this figure may seem negative, the internal breakdown shows that goods exports in the first quarter of 2026 grew nearly 18% compared with the first quarter of 2025. Thus, the external sector remains a relevant support for aggregate demand, although it is subject to the evolution of the global environment and the trade relationship with the United States.

Meanwhile, government spending remained at 7.78% of GDP and recorded growth of 3.41%. Although its weight within aggregate demand is smaller compared with private consumption, this component provided some support to growth during the quarter, though it did not fully offset the weakness observed in private investment.

Overall, aggregate demand points to an economy with limited gains and a heterogeneous composition: private consumption and the external sector continue to support growth, while investment remains the main point of weakness and public spending provides only a limited boost. This suggests that growth in the coming quarters will remain conditioned by the ability to sustain consumption, recover investment, and maintain external momentum.

Peru—El Niño Intensification and its Economic Implications for Peru

Pablo Nano, Deputy Head Economist

pablo.nano@scotiabank.com.pe

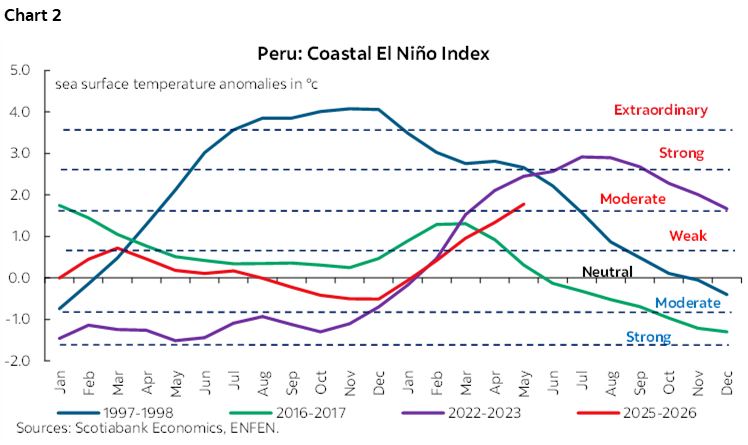

Recently, both the U.S. National Oceanic and Atmospheric Administration (NOAA) and ENFEN—the local authority responsible for monitoring the El Niño Phenomenon (FEN)—have concurred in indicating that this climate event, characterized by an increase in sea surface temperatures (SST), is expected to intensify in the coming months and may reach a “strong” magnitude along the Peruvian coast during the summer of 2027 (charts 1 and 2).

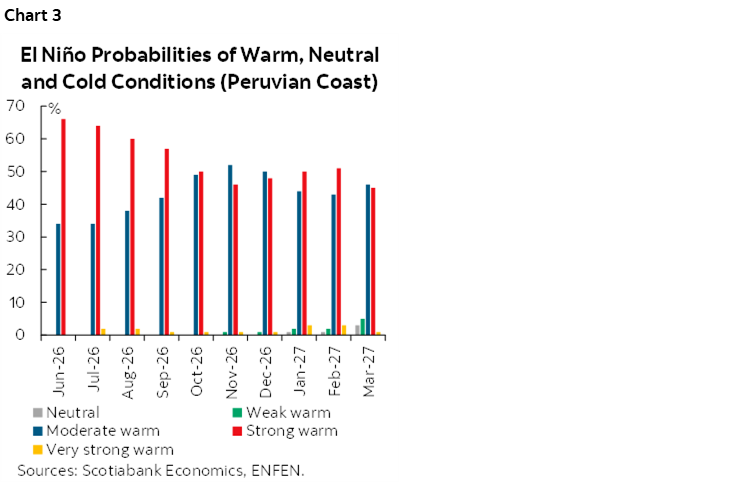

It is worth noting that, since March 2026, a positive SST anomaly has been observed, consistent with patterns seen in previous warm episodes (see “Peru Coastal El Niño Index” chart). In its latest communication, ENFEN indicated that the El Niño could persist until March 2027, with a 48% probability of reaching a “strong” magnitude. This represents a revision from its previous report, which projected a duration until February 2027 and a 36% probability of a “moderate” event.

The economic impact of each El Niño episode varies depending on its intensity and duration. Nevertheless, the likelihood that the event extends into Peru’s rainy season—beginning in December—could amplify its adverse effects. These may include temporary logistics disruptions, damage to agricultural areas, and, in severe cases, destruction of public and private infrastructure, particularly along the northern coast. A historical reference is the 2017 episode, when infrastructure losses approached USD 3 billion.

In terms of economic activity, the ongoing Coastal El Niño event—initiated in March 2026—is already affecting extractive sectors such as Fishing and, to a lesser extent, Agriculture. Warmer ocean waters have impacted anchovy biomass, causing it to migrate deeper and southward, thereby complicating catch efforts. Indeed, during the first anchovy fishing season in the north-central region, landings reached only 470,000 metric tons, equivalent to 25% of the established capture quota. Additionally, the agricultural sector recorded two consecutive months of contraction as of April, mainly due to reduced output of crops for the domestic market. The textile and apparel industry has also been adversely affected, as higher temperatures have significantly reduced sales of autumn–winter garments.

In conclusion, the current El Niño Phenomenon is expected to weigh on the performance of resource sectors—particularly Fishing and Agriculture—throughout 2026, subtracting an estimated 0.2 percentage points from our growth forecast for the year. However, GDP growth of 3.5% in the first quarter of 2026, sustained expansion in domestic demand exceeding expectations, and the potential improvement in business sentiment following the most likely outcomes of the electoral runoff suggest stronger-than-anticipated performance in non-resource sectors. Consequently, the balance of risks to our 2026 GDP growth forecast of 3.2% remains with an upward bias.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.