HIGHLIGHTS

- The June rate announcements cycle begins with the BCRP, BoC, and ECB on tap next week, where only the latter is expected to tweak policy with a 25bps hike (but don’t count out a BCRP surprise).

- A handful of May CPI releases from Chile, Mexico, Brazil, the U.S., and China also await, while markets continue to keep a close eye on Middle East developments with a peace deal remaining elusive. CUSMA renewal noise is also making the rounds as the countries near the July 1st deadline with seemingly little progress being made and high odds of missing this key date.

- In today’s report, our economists in Mexico go over the latest OECD forecasts for the global economy, with Mexico’s 2026 GDP growth seen underperforming all but a handful of Eurozone countries and Japan.

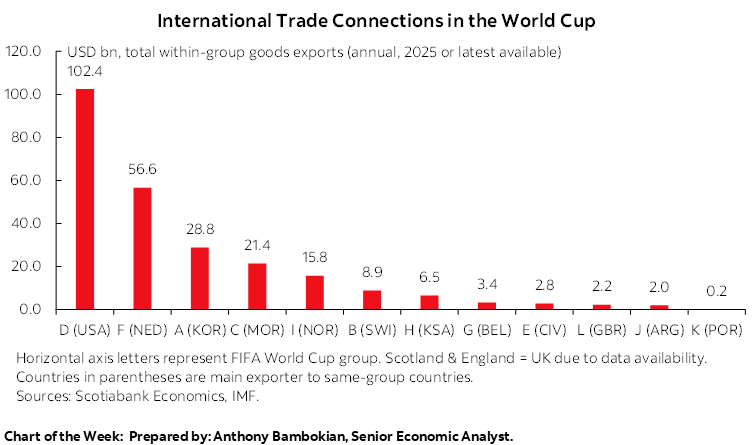

Chart of the Week

PERU ELECTION AND RATE DECISION, REGIONAL CPI

Juan Manuel Herrera, Director

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- The June rate announcements cycle begins with the BCRP, BoC, and ECB on tap next week, where only the latter is expected to tweak policy with a 25bps hike (but don’t count out a BCRP surprise).

- A handful of May CPI releases from Chile, Mexico, Brazil, the U.S., and China also await, while markets continue to keep a close eye on Middle East developments with a peace deal remaining elusive. CUSMA renewal noise is also making the rounds as the countries near the July 1st deadline with seemingly little progress being made and high odds of missing this key date.

- In today’s report, our economists in Mexico go over the latest OECD forecasts for the global economy, with Mexico’s 2026 GDP growth seen underperforming all but a handful of Eurozone countries and Japan.

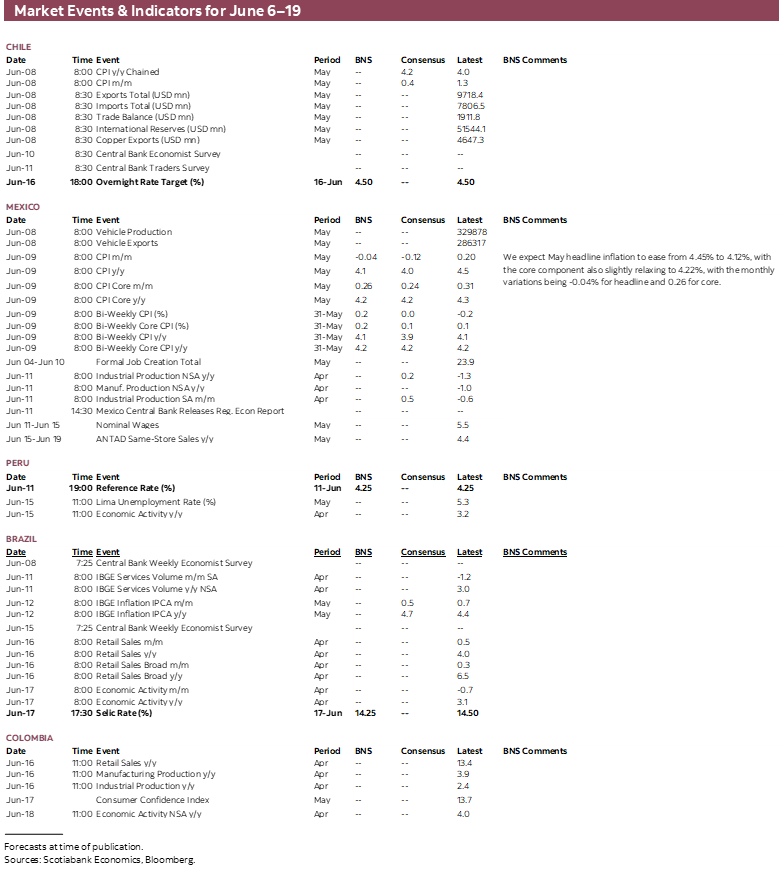

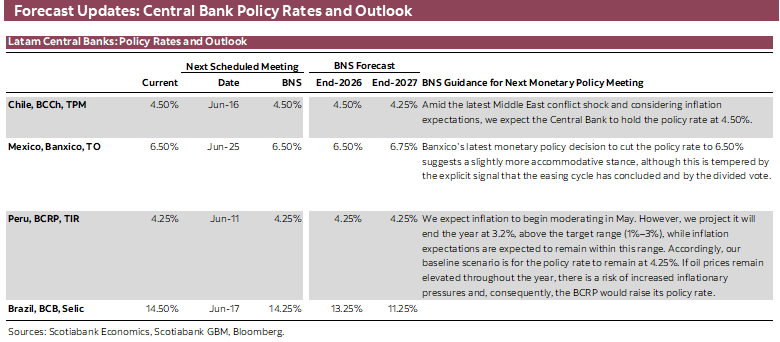

The BCRP, ECB, and BoC kick off the June cycle of global rate decisions next week, with Mexico and South Africa kicking off the 2026 FIFA World Cup on Thursday, and the week opening to preliminary counts of Peru’s tightly-contested second round presidential vote this Sunday. The BCRP and BoC are set to hold at 4.25% and 2.25%, respectively, while the ECB is seen hiking 25bps to 2.25% accompanied by new macroeconomic projections.

Alongside these central bank decisions, we also get a handful of May CPI releases from Chile, Mexico, Brazil, the U.S., and China, among others, but only second-tier data from across the globe otherwise. Chile will publish May international trade data and the BCCh’s economists’ and traders’ surveys, Mexico has April industrial production and Banxico’s regional economies report on tap, and the U.S.’s calendar also includes PPI and U. of Michigan figures.

As always, developments in Middle East peace talks will play a key role in market sentiment that is looking downbeat into the week’s close on the back of rising tensions as well as weakness in the technology space—with rising yields following the U.S.’s strong jobs report weighing further. CUSMA trade negotiations also seem to be moving slowly, leaving the July 1st renewal deadline at clear risk of being missed, but without any public confirmation that this may be the case nor any official announcements by any of the parties regarding how talks are shaping up or what the bases of negotiation are.

Uncertainty is high regarding the winner of Sunday’s vote in Peru. The latest polls place the right’s Fujimori and the left’s Sánchez in a statistical tie where the former enjoys only a slight polling advantage in surveys that, in Peru, have tended to be off the mark (Sánchez was not a leading candidate in surveys ahead of the first-round contest). As argued by our team last month, a victory for Sánchez could be highly transformative to the country’s economic model. There is greater confidence for the rematch of the 2010 opener (1–1). Polymarket gives about 70% odds to a Mexican victory, against 20% odds of a draw and only a 10% chance of a South African win.

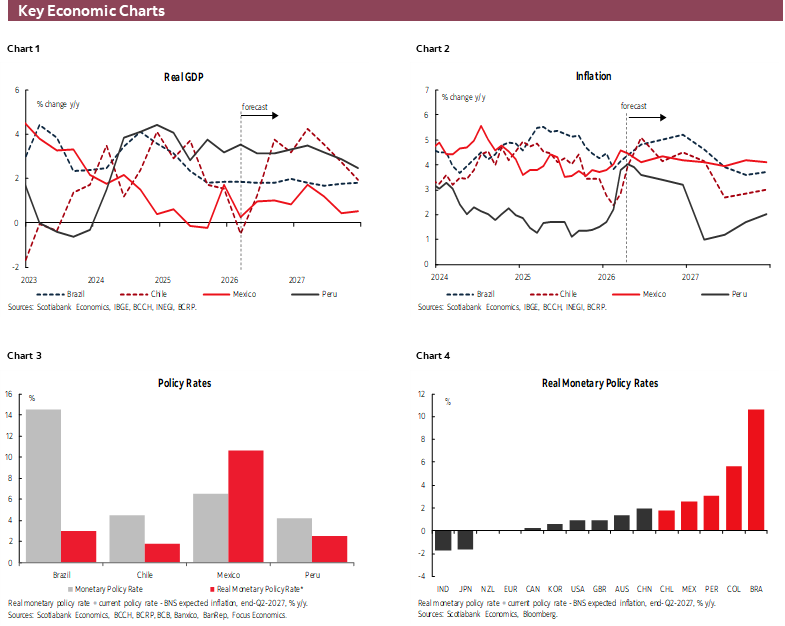

Now, while we don’t think the BCRP will surprise at its rate announcement next Thursday, economists and markets have been caught off-guard by the BCRP multiple times throughout the bank’s easing cycle which began in September 2023. This time around, risks are tilted towards the BCRP surprising with a rate hike, although this is not our baseline. Rather than shifting to a restrictive path that would tee up more hikes, a rate increase would be an adjustment in response to recent prices data (May’s reading undershot estimates, however) and rising inflation expectations. Twelve months ahead inflation expectations sit at 2.9%, as per the latest BCRP survey, thus taking the real policy rate to its lowest level since July/August 2022, at 1.36%, compared to 2.1/2.2% in the first two months of the year, prior to the beginning of the conflict in the Middle East and the surge in global energy prices. Meanwhile, Peru’s economy remained in strong standing in the early part of the year despite electoral uncertainty as underlying demand drivers (e.g. labour market) remain in solid shape and are getting a push from Peruvians deploying funds from pension withdrawals.

On Monday, Chilean CPI is expected to accelerate to 4.2% from 4.0% y/y on the back of a 0.5% monthly increase in prices (compared to +0.2% last May), for its highest reading since September 2024. Housing (bills and rents) and transportation prices should be the main drivers of the monthly increase, with airfares acting as the main contributor within the transportation sector complemented by a small increase in gasoline prices. Underlying drivers of inflation are also elevated, however, with inflation ex. volatile items forecast to increase 0.4% m/m (keeping around 3.4% y/y), partly reflecting second round or indirect effects from higher energy prices. Note that May inflation data can be influenced by large price increases ahead of Cyber Day discounts in early-June. These price hikes could result in a data surprise in Monday’s data since their magnitude is tough to pin down.

Mexico follows on Tuesday with May CPI which should cool to around the 4% mark (i.e. the upper bound of Banxico’s tolerance band) from 4.5% thanks to falling fresh food inflation that heated up headline readings in prior months. In the mid-May release, inflation slowed to 4.1% from 4.5% in H1-Apr, with core CPI ticking marginally lower to 4.2% from 4.3% over the same period. Stubborn underlying inflation, above 4% for two years running, is clear motivation to keep the overnight rate steady at 6.50%, but we don’t think the outlook for prices will motivate Banxico to hike later this year, as markets expect with over a full quarter-point increase priced in by year-end. The central bank’s regional economies report may not be market moving, but it provides interesting insights on how Mexico’s exports-oriented states are responding CUSMA (and broader) trade uncertainty.

Brazil, like Mexico, merely completes the CPI picture for May on Friday with mid-month prices data leaving little room for surprise. The IPCA-15 reading of 4.6% met the expectations of economists who now expect the full-month print to close slightly higher at 4.7% y/y, with food pressures continuing against the pull lower from gasoline subsidies announced on May 13th. Last Saturday, Brazil’s government also announced that emergency measures taken against the rise in global fuel prices would be extended by two months to end-July. Subsidies notwithstanding, headline and core inflation remains elevated and continues to be pressured by consumption buoyed by fiscal stimulus. Coupled with a resulting rise in inflation expectations and also some market concerns about Lula’s rising re-election odds, traders have sharply pulled back on BCB cut bets to now expect unchanged rates through year-end, even opening the door to the possibility of hikes. Economists polled by the BCB (and us) still expect that the bank will roll out considerable reductions by year-end considering that policy remains in a highly-restrictive spot (~10–10.5% in real terms).

COUNTRY UPDATES

Mexico—Global Outlook Under Pressure: Implications for Mexico

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

Last week, the OECD published its June 2026 Economic Outlook, in which it identifies the conflict in the Middle East as the main risk factor for the global economy. Although the year began with a more favourable outlook than previously anticipated, supported by the resilience of economic activity, looser financial conditions, and a moderation in trade tensions, the escalation of the conflict and its geopolitical consequences have once again weakened the global outlook.

Given the uncertainty generated by the conflict, the OECD presents two scenarios. In the first, the disruption caused by the conflict is contained and shorter in duration, with the effects on energy production and trade proving temporary and occurring in the context of progress toward a peace agreement, which would allow global growth of 2.8% in 2026 and a rebound to 3.1% in 2027. However, the more prolonged disruption scenario envisions persistent effects through 2027, under which the impact would be considerably more severe, with growth slowing to 2.1% in 2026 and 1.8% in 2027, along with higher recession risks, persistent inflation, and financial tensions, particularly in emerging economies dependent on imported energy.

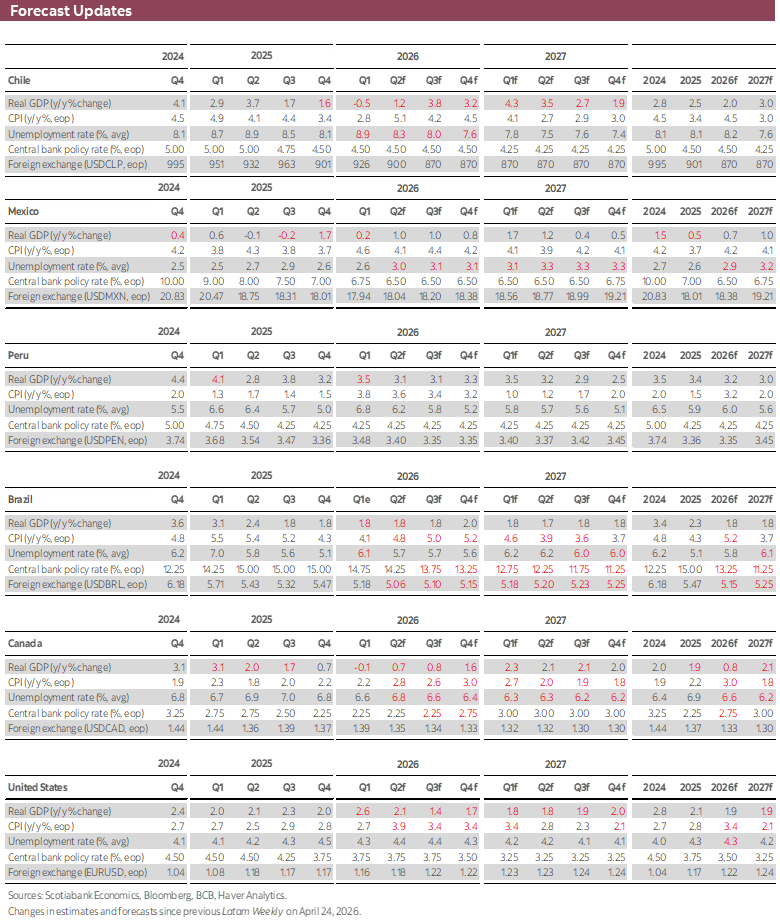

Under the baseline scenario (time-limited disruption), Mexico stands out for a considerably weaker performance in 2026. Global growth is projected at 2.8%, the G20 at around 3.0%, OECD economies would expand by 1.5%, and non-OECD economies by 3.8%. In Latin America, average growth would moderate to 1.7%, below the 2.2% recorded in 2025. Against this backdrop, the OECD estimates economic growth for Mexico at only 0.8%, placing it among the economies with the weakest relative momentum both regionally and internationally. Although this weakness appears to be part of a broader deterioration in growth prospects—with downward revisions averaging close to 0.3% for most countries—Mexico’s domestic weakness presents downside risks and structural challenges, such as the contraction in investment—which has been in negative territory for 19 months—the slowdown in consumption, weak formal employment growth, the security situation, among other factors.

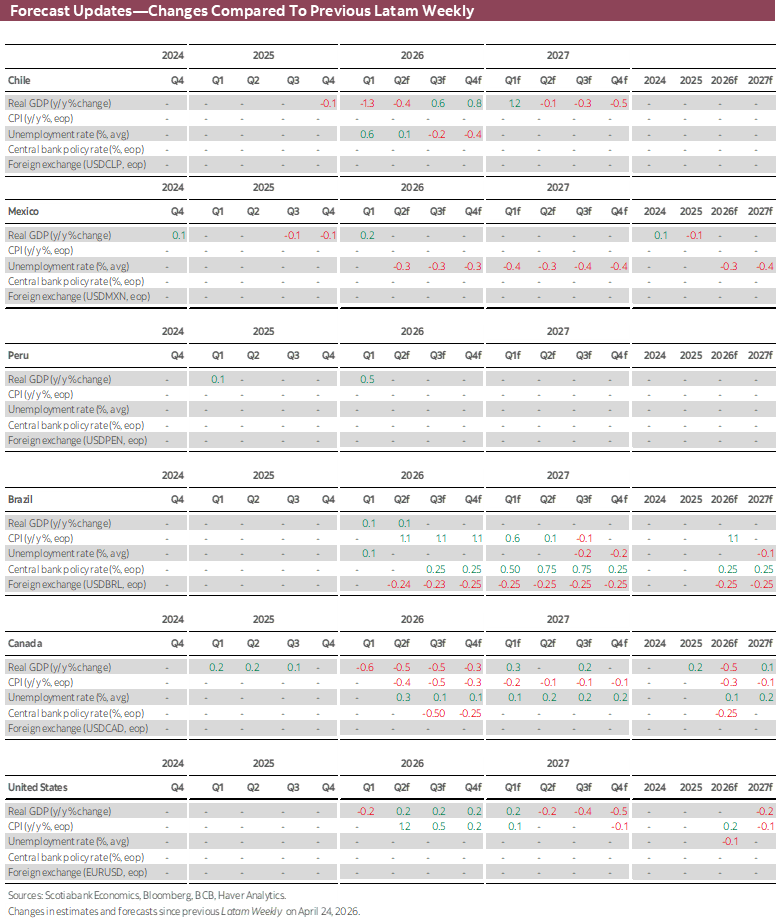

The revisions for Mexico also reflect this broad-based adjustment, with relevant differences across institutions. The Finance Ministry lowered its expectation from 3.0% in March to an estimate of 2.3%—within a range of 1.8% to 2.8%—Banxico cut its forecast from 1.6% to 1.1%, while the OECD adjusted it from 1.3% to 0.8%. The IMF, for its part, maintains an expectation of 1.6% (but is due to refresh its projections next month). In Scotiabank’s case, we have maintained a more cautious view for several months, with growth below 1%. During 2025, our forecast for the current year was 0.6% and it currently stands at 0.7%; although the favourable data at the end of 2025 temporarily led to an upward revision to 1.0%, the weakness observed in first-quarter GDP prompted a new adjustment to 0.7%. Taken together, these revisions confirm that the Mexican economy faces a particularly challenging outlook, in an adverse external environment and with increasingly limited growth margins, with uncertainty surrounding CUSMA and domestic political and economical conditions standing out.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.