The National Jury of Elections (JNE) officially proclaimed on Sunday, May 17th, the results of the first round of Peru’s presidential elections held on April 12th. Keiko Fujimori (Fuerza Popular) secured first place with 2,877,678 votes (17.2% of valid votes), while Roberto Sánchez (Juntos por el Perú) obtained 2,015,114 votes (12.0%), ranking second. Rafael López Aliaga (Renovación Popular) placed third with 1,993,905 votes (11.9%).

As none of the 35 candidates obtained more than half of the valid votes, Fujimori and Sánchez will face each other in the second round of the presidential elections scheduled for June 7th.

Renovación Popular, which fell short of second place by only 21,209 votes, has announced its intention to request the annulment of the official results proclamation due to alleged irregularities. However, Roberto Burneo, president of the JNE, has stated that while political parties have the right to appeal to other institutions such as the Public Prosecutor’s Office or the Constitutional Court (TC), the JNE is the country’s highest electoral authority, and the proclaimed results are final and not subject to appeal.

As noted in a previous article, “Peru’s Presidential Election: Late Surprises and Elevated Uncertainty,” the two electoral options represent significant differences in economic policy. Fuerza Popular (FP) broadly supports Peru’s existing economic framework, which prioritizes macroeconomic stability, openness to private investment, and an independent central bank. By contrast, Juntos por el Perú (JPP) has proposed a substantially different economic model. Its platform includes drafting a new constitution, asserting state ownership over all underground natural resources, and reserving the direct management of strategic sectors—such as hydrocarbons, energy, water, and ports—to the state, explicitly ruling out private concessions.

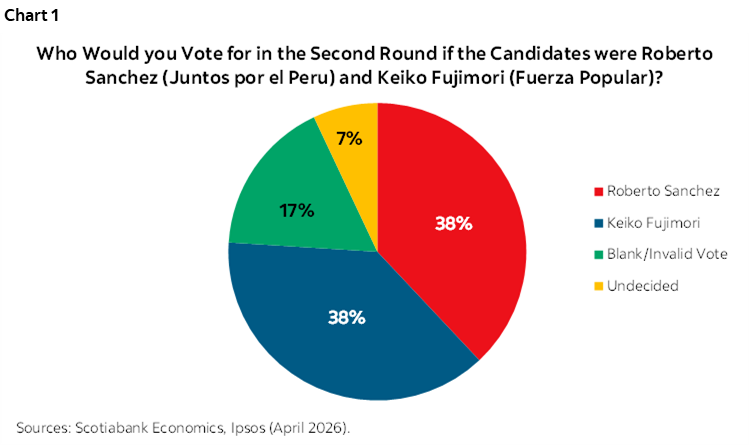

Ahead of the second round, initial polls show a statistical tie between Fujimori and Sánchez. According to a survey conducted by Ipsos Perú in late April, Keiko Fujimori registers 38% voting intention, matching Sánchez’s 38%, while 17% would cast blank or invalid ballots and 7% remain undecided (chart 1). It is worth highlighting the significant geographic divergence in voting patterns: FP enjoys strong support in Lima and in the northern coastal regions and Ica—areas with higher economic growth—whereas JPP has substantial backing in the Andean regions—which exhibit relatively lower levels of economic development.

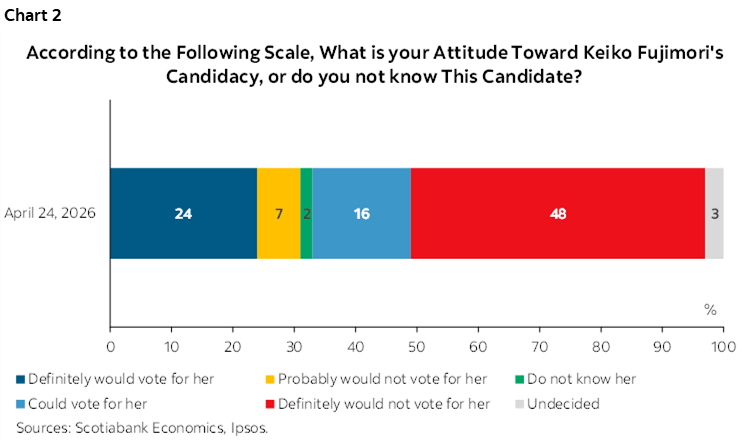

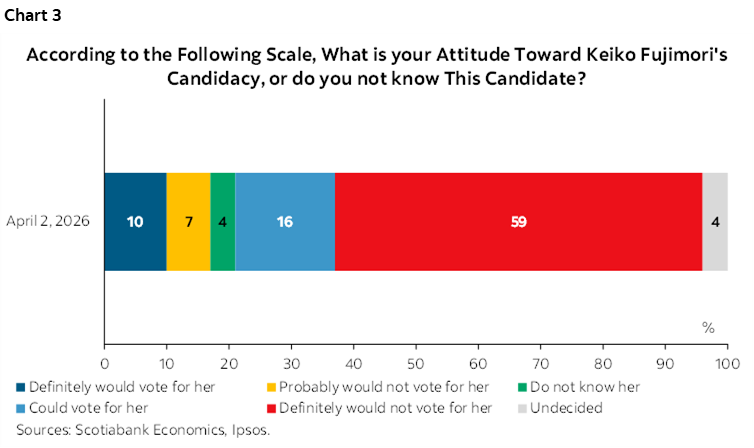

This marks the fourth time that Keiko Fujimori will compete in a second-round runoff, having lost the previous three. Unlike in 2021, when the first second-round poll showed Pedro Castillo leading Fujimori by 11 percentage points, she now enters the race on equal footing with Sánchez. Additionally, her rejection rate—the primary factor behind her prior electoral defeats—has declined and now stands below 50% (charts 2 and 3).

In conclusion, with three weeks remaining until the runoff, uncertainty persists not only regarding the eventual winner but also concerning the future direction of economic policy in Peru. Institutional safeguards ensure that both the economic chapter of the Constitution and the independence of the Central Reserve Bank can only be amended through constitutional reforms requiring a two-thirds majority in both the Senate and the Chamber of Deputies—support that Juntos por el Perú and its allies currently lack. Nevertheless, a potential JPP administration could entail greater state intervention in the economy, the introduction of higher taxes, and the withdrawal from free trade agreements signed by the country. In this context, Peru’s economic growth potential over the next five years could effectively be shaped by the outcome on June 7th.

—Pablo Nano

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.