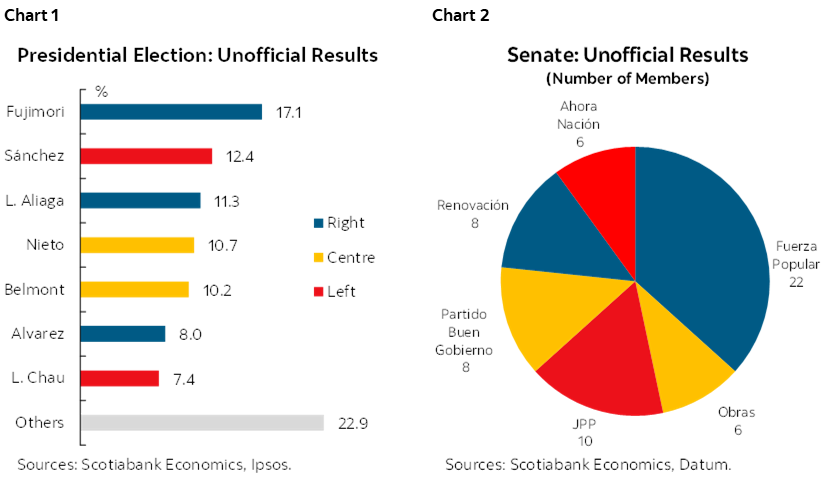

Preliminary results from Peru’s presidential election point to an unusually fragmented and volatile outcome. As expected, Keiko Fujimori (Fuerza Popular) secured a place in the June 7th runoff with approximately 17% of the vote, according to quick counts by major polling firms. However, the identity of the second finalist remains unclear, as the candidates ranked second through fourth are separated by very narrow margins and final voting has not yet fully concluded.

In an unprecedented decision, the country’s electoral authority extended voting through April 13th after logistical failures prevented the opening of 187 polling stations in Lima, Peru’s largest metropolitan area. This disruption affected roughly 52,000 voters, equivalent to 0.2% of the national electorate, and has contributed to delays in finalizing the results.

Unofficial tallies underscore the uncertainty regarding who will join Fujimori in the June contest. Ipsos data show Roberto Sánchez (Juntos por el Perú, JPP)—a left-wing candidate—unexpectedly taking 12.4% of the vote, alongside Rafael López Aliaga (Renovación Popular) at 11.3% and Jorge Nieto (Partido del Buen Gobierno) at 10.7%. All three results fall within the statistical margin of error. An alternative quick count by Datum presents a slightly different ranking, though similarly tight, reinforcing that the final outcome will depend on the official count.

Sánchez’s performance represents the most significant surprise of the election. As recently as early March, he registered low single-digit support in national polls. His late surge was driven by strong backing in the Andean regions, which historically tend to vote against candidates perceived as Lima-centric and reflect deeper regional and socio-economic divides within the country.

Rafael López Aliaga, a conservative former mayor of Lima, represents a right-wing platform that emphasizes fiscal discipline, private investment, and socially conservative policies. While his party had been a front-runner earlier in the campaign, its momentum weakened in recent weeks following controversial political alignments in Congress.

From a market and economic policy perspective, initial reactions to the overall results have been cautiously positive. The two main right-of-centre parties—Fuerza Popular and Renovación Popular—both broadly support Peru’s existing economic framework, which prioritizes macroeconomic stability, openness to private investment, and an independent central bank.

By contrast, Juntos por el Perú has proposed a substantially different economic model. Its platform includes drafting a new constitution, asserting state ownership over all underground natural resources, and reserving the direct management of strategic sectors—such as hydrocarbons, energy, water, and ports—to the state, explicitly ruling out private concessions. Were such proposals to advance, they would mark a fundamental shift in Peru’s policy regime.

The presidential runoff election is scheduled for June 7th, but next steps may not be immediate. The operational issues observed on election day could prompt legal challenges from political parties, potentially delaying the publication of final results and prolonging political uncertainty.

Beyond the presidency, attention has also turned to the newly reinstated 60-member Senate, which will play a central role in institutional governance. Its responsibilities include approving presidential removal proceedings and confirming appointments to key economic oversight bodies, including the central bank and financial regulator. Current projections suggest a fragmented Senate, with Fuerza Popular emerging as the largest bloc and the only party likely to reach the threshold required to act as a veto player in institutional disputes.

Overall, the election confirms a familiar pattern in Peru: late shifts in voter sentiment, fragmented outcomes, and prolonged uncertainty, with meaningful implications for governance and economic policymaking in the months ahead.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.