HIGHLIGHTS

- Another massive week of central bank decisions awaits with officials in Chile, Brazil, U.S, U.K., Japan, Australia, and a handful of others, on tap. A possible Middle East peace deal (or the broad framework of one) also seems to be taking shape and may be signed within days.

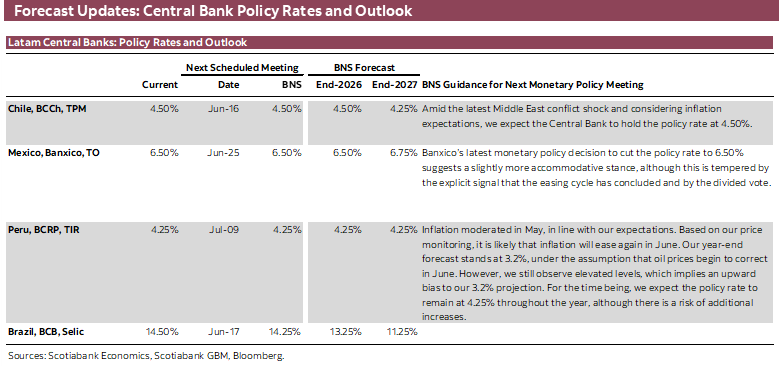

- For the BCCh, the balance of macroeconomic data and inflation risks remain aligned in favour of a rate hold at 4.50%, as our team in Chile discusses in today’s note. The central bank will also publish new forecasts alongside the decision.

- Amid lingering stickiness in underlying inflation metrics, and with Q1 economic strength used as a possible justification, the BCB is set to announce only a 25bps reduction to 14.25% accompanied by a hawkish message.

- In today’s note, our economists in Mexico analyse the possible impacts that the tri-country FIFA World Cup could have on the local economy, with estimates pointing to a modest 0.1–0.2% net positive impact on GDP growth in 2026 with the bulk of these benefits coming in June and July before quickly fading out.

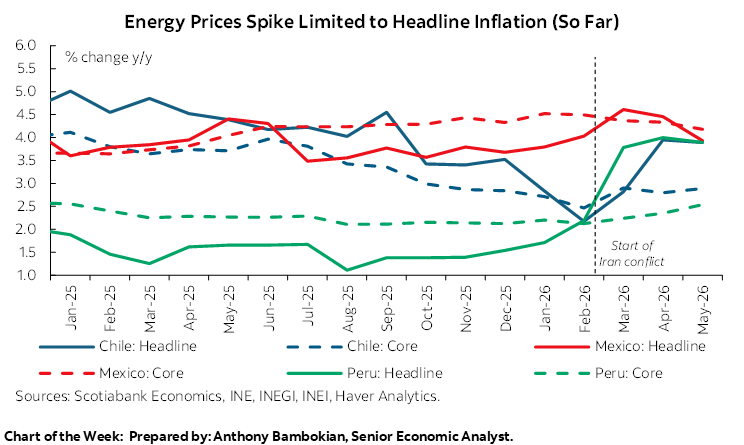

Chart of the Week

THE BCCh, BCB, AND FED ARE UP

Juan Manuel Herrera, Director

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Another massive week of central bank decisions awaits with officials in Chile, Brazil, U.S, U.K., Japan, Australia, and a handful of others, on tap. A possible Middle East peace deal (or the broad framework of one) also seems to be taking shape and may be signed within days.

- For the BCCh, the balance of macroeconomic data and inflation risks remain aligned in favour of a rate hold at 4.50%, as our team in Chile discusses in today’s note. The central bank will also publish new forecasts alongside the decision.

- Amid lingering stickiness in underlying inflation metrics, and with Q1 economic strength used as a possible justification, the BCB is set to announce only a 25bps reduction to 14.25% accompanied by a hawkish message.

- In today’s note, our economists in Mexico analyse the possible impacts that the tri-country FIFA World Cup could have on the local economy, with estimates pointing to a modest 0.1–0.2% net positive impact on GDP growth in 2026 with the bulk of these benefits coming in June and July before quickly fading out.

Another massive week of central bank decisions awaits with officials in Chile, Brazil, U.S, U.K., Japan, Australia, and a handful of others, on tap. A few among them are expected to shift policy settings (BoJ hike, BCB cut) while others’ decisions will be closely monitored for the timing of the next possible move (the Fed and BoE, most notably). A possible Middle East peace deal (or the broad framework of one) also seems to be taking shape and may be signed within days, but talks between the involved parties have quickly fallen apart multiple times since the beginning of the conflict, so perhaps tread carefully until pen is put to paper.

Data-wise, there is nothing noteworthy in Mexico’s and Chile’s calendars, while each of Peru, Brazil, and Colombia publish April economic activity figures next week, with the last two having retail sales readings ahead of the activity data to tighten expectations. The releases may be of secondary importance for Brazil, where economists and markets will focus on the BCB’s rate decision that same day, while in Colombia the focus is on next Sunday’s second-round vote with markets trading optimistically on the back of polls showing independent Abelardo de la Espriella leading President Petro’s ally Iván Cepeda by somewhere between 5–10ppts; the winner will take office on August 7th.

Outside of Latam, the U.S., U.K., Canada, and China all publish retail sales data. The U.K.’s schedule also has key CPI and employment readings ahead of the BoE’s decision on Thursday where no change is expected but the balance between growth concerns and inflation risks will be closely scrutinized for the possibility that the bank hikes (or not) later this year. China’s retail data is out at the same time as industrial production and investment data, all for May on Tuesday, as part of the once-a-month check on the pulse of the country’s economy. U.S. and Chinese markets are closed on Friday for domestic holidays.

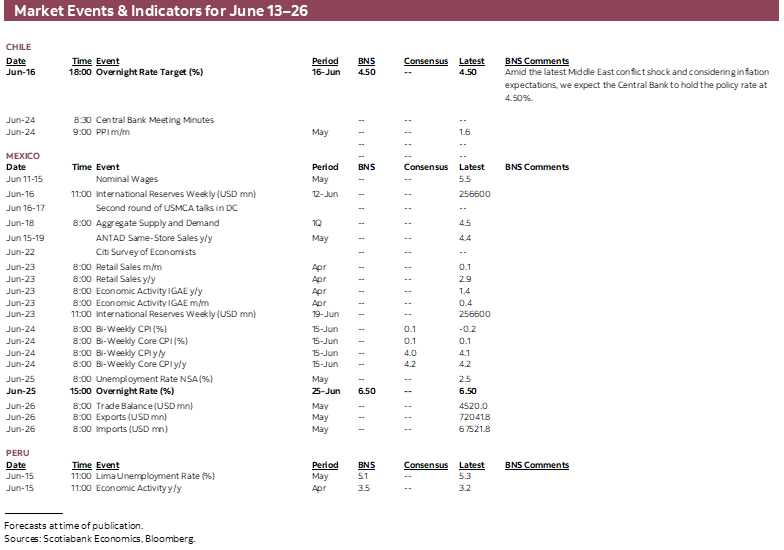

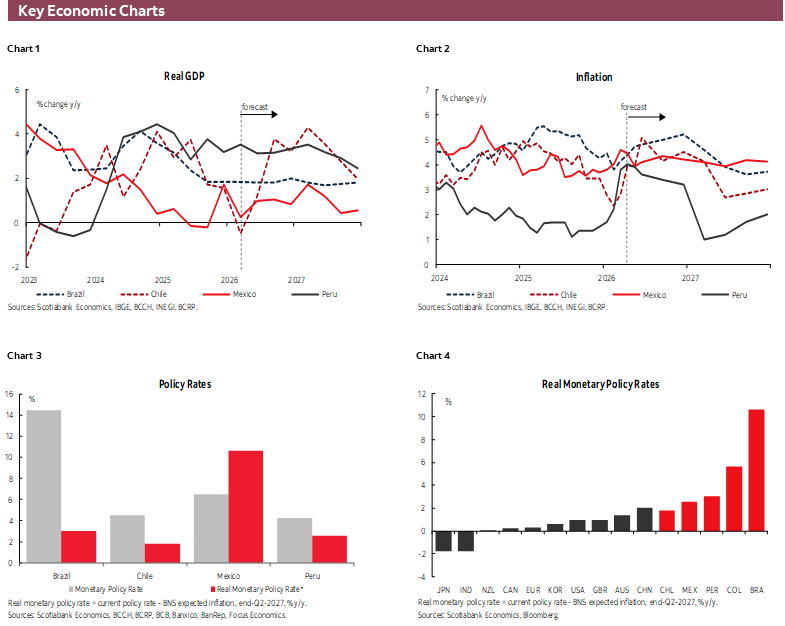

In today’s report, the team in Chile previews next week’s BCCh decision. The balance of macroeconomic data and inflation risks are aligned in favour of a rate hold at 4.50%. The bank’s staff will also update its macroeconomic projections which should give us a good idea of how the BCCh thinks conditions will evolve and thus help us narrow down expectations for the policy rate over the next few months. Following weak GDP/activity data since the start of the year, the bank will likely lower its annual growth projection to a 1.25–2% range, from 1.5–2.5% in its March Monetary Policy Report. On the other hand, its year-end forecast of 4% headline inflation remains reasonable in light of recent prices data. We project that the BCCh will keep to a 4.50% policy rate over the balance of 2026, a view that is shared by traders that are only pricing in marginal odds of a hike by December.

Peru’s central bank was first to the plate among those in Latam, opting for a third consecutive rate hold at its June 11th decision (see here), maintaining a view that inflation will converge to target with most of the recent upside (3.5% y/y in May) owing to temporary supply-side factors that should fade over the coming quarters. The country is enjoying a strong start for economic growth that continued in April GDP data out on Monday expected to show a 3.5% y/y expansion in activity. Investment strength, solid labour markets, and the effects of another round of pension withdrawals have more than stood up against electoral uncertainty.

On that last note, vote counts for last Sunday’s second-round presidential election have essentially stalled at 98.3% counted, with a marginal lead of ~600 votes for Fujimori over Sánchez. Now, about 1,600 ballots corresponding to hundreds of thousands of votes need to be counted and scrutinized after being flagged for review, with this process due to take a few weeks. Fujimori will likely widen her extremely narrow lead once these votes are tallied given that ~1,150 of these ballots correspond to votes from the Lima region and from abroad, which roughly favoured Fujimori 63% vs 37%. On Polymarket, Fujimori is at 95%+ odds of winning. If confirmed, Peru would shift from the left to the right of the political spectrum with the start of the new presidential term in late July.

There’s little to pay attention to next week as far as Mexico’s calendar goes, coming after a slight undershoot in May inflation data and a strong upside surprise in April industrial production figures published earlier this week. We’ll be looking for possible rumblings ahead of Banxico’s rate decision on the 25th, but it’s all but certain that settings and likely guidance will be left unchanged then. In today’s note, our economists analyse the possible impacts that the tri-country FIFA World Cup could have on the local economy, with estimates pointing to a modest 0.1–0.2% net positive impact on GDP growth in 2026 with the bulk of these benefits coming in June and July before quickly fading out. Overall, the tournament is unlikely to alter the soft medium-term growth dynamics plaguing the Mexican economy.

Last but not least, Brazil may have the busiest calendar in the region next week. On Tuesday, retail sales are estimated to have slowed considerably in April from a strong 4% y/y in March, though mainly as a result of a less favourable base of comparison rather than a clear weakening of activity. This will also show up in about a halving of economic activity growth in April data due on Wednesday, off a 3.1% y/y gain in March. Nonetheless, Brazil’s economy remains sluggish (notwithstanding a better start to the year) and fiscal impulses are waning or should do so soon, all challenged by highly restrictive BCB policy settings that will likely remain as such for several additional quarters, coupled with political uncertainty ahead of October’s general election.

Amid lingering stickiness in underlying inflation metrics, and with Q1 economic strength used as a possible justification, the BCB is set to announce only a 25bps reduction to 14.25% on Wednesday afternoon accompanied by a hawkish message and upward revisions to inflation and growth, all reinforcing expectations that the BCB will be slow in loosening monetary policy. We think a pullback in external risks (energy prices, mainly) will help the BCB speed up its easing cycle in the second half of the year, to close 2025 at a 13.25% rate target.

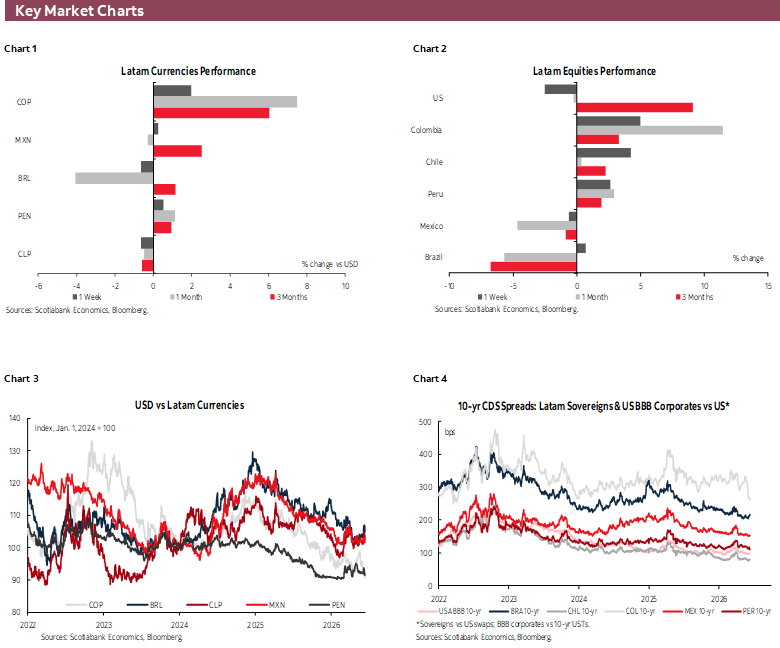

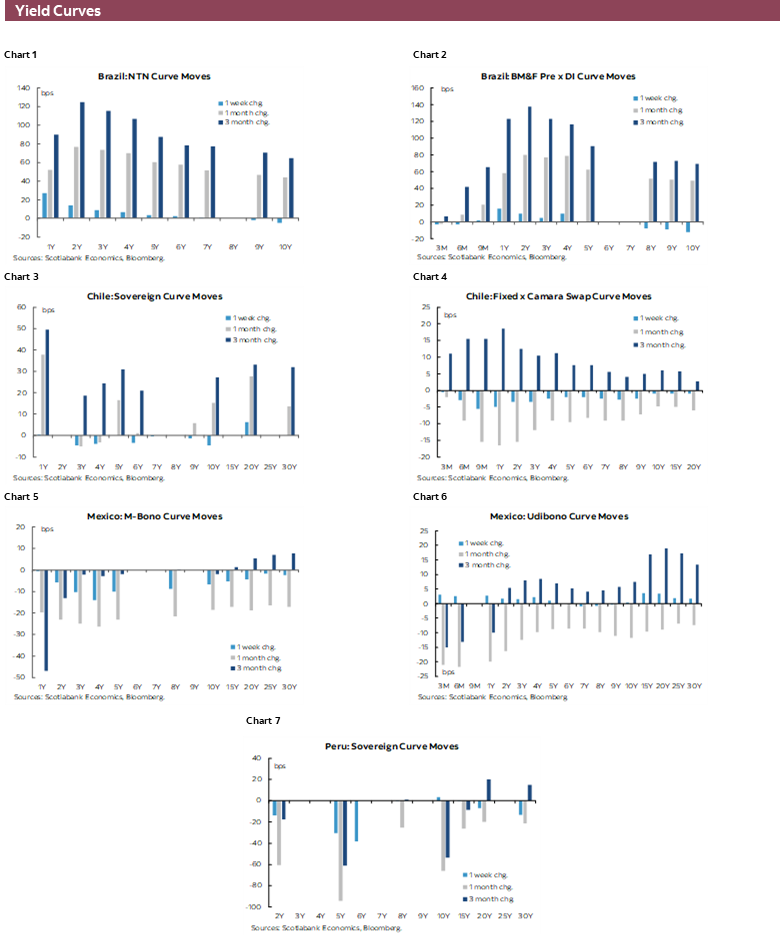

Markets, on the other hand, are even playing with the idea of a rate hike in the second half of the year, judging that the BCB will not get good news on the inflation front, or that electoral risks could spell trouble for Brazilian assets that require the BCB to stand pat. With Lula sitting at around 50% odds of winning compared to Bolsonaro’s ~25% (as per Polymarket), markets are worried that a re-elected Lula fails to mend the country’s fiscal trajectory. The ~70bps rise in Brazilian 10yr yields in the year-to-date is the largest among the major economies that we follow (compared to ~30bps in the U.S., Chile, and Peru).

COUNTRY UPDATES

Chile—Softer Inflation, Weak Activity and Labour Slack Support a Hold in June

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

We expect the Board to maintain the policy rate at 4.50% on June 16th. This hold decision would be consistent with the need to monitor potential inflation expectations de-anchoring and international volatility, despite the deepening weakness in activity and employment. Going forward, we expect the Board to maintain a neutral bias, as the significant downside risks to growth are balanced against the short-term spike in headline CPI.

The Central Bank would revise down its 2026 growth forecast to a 1.25–2.0% range. Activity conditions have deteriorated significantly, as evidenced by the -1.2% y/y print in April GDP, which marks a clear departure from previous momentum. The composition of this weakness is concerning; while mining remains a primary drag, the stagnation in non-mining sectors—impacted by supply shocks in agriculture and fishing—suggests that domestic demand remains weak. With a 2026 carry-over currently at 0%, achieving even the lower end of the Central Bank’s growth range is becoming increasingly challenging. From a policy perspective, this environment implies an output gap that remains wide and far from closing, as the economy has effectively been stagnant since early 2025.

The labour market continues to exhibit signs of worsening slack, reinforcing the view of cooling domestic demand. The SA unemployment rate has climbed to 8.9%, comfortably exceeding the Central Bank’s estimated NAIRU range of 8.0–8.5%. Crucially, the destruction of formal employment for the second consecutive quarter and the first interannual contraction in wage-earning jobs in five years suggest significant erosion in labour demand. This has directly translated into a persistent deceleration of the total wage bill, with null real labour income for wage earners for the first time since the pandemic. Such developments indicate that labour-driven inflationary pressures are virtually absent, as the broadening labour gap points toward further disinflationary pressure on the consumption side.

Recent inflation prints support maintaining the Central Bank’s 4% year-end projection, despite the prolonged geopolitical conflict. The May headline CPI print of 0.2% m/m (3.9% y/y) was a significant downside surprise, primarily driven by a historic deflation in food prices, including an unprecedented drop in bread prices. While core CPI diffusion has normalized, there is little evidence of second-round effects in services, which remain within historical ranges. Nonetheless, headline CPI is expected to approach 5% in June due to energy costs and indexation risks, which could potentially threaten the anchoring of long-term expectations. The primary challenge for the Central Bank is distinguishing between these temporary supply-driven fluctuations and the underlying trend, which is currently supported by a widening output gap.

In our view, recent signals from the Central Bank suggest a preference for prolonged stability in the policy rate to absorb external shocks, despite the clear need for greater stimulus shown by the April GDP and employment data. The upcoming June Monetary Policy Report will likely reflect this tension through a downward revision of GDP growth forecasts, even as the Board remains vigilant regarding the convergence of inflation to the target.

Mexico—The Potential Economic Impact of the World Cup in Mexico

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

The 2026 FIFA World Cup began last week, representing a highly visible international event for Mexico and a potential positive boost—albeit limited and temporary—to economic activity. Unlike previous editions, in which a single country hosted the entire tournament (except for Korea and Japan in 2002), Mexico will share hosting duties with the United States and Canada, meaning it will host only 13 of the 104 matches. In this context, the World Cup should be understood more as a temporary catalyst for certain sectors than as a factor capable of structurally altering the country’s growth trajectory in 2026.

International experience suggests that the macroeconomic effects of World Cups tend to be positive, but limited and concentrated in tourism, consumption, and infrastructure. In Brazil 2014, the estimated boost to GDP growth was only 0.2%, accompanied by an additional 0.5% pressure on inflation. In Russia 2018, organizers estimated a cumulative impact close to 1.1% of GDP between 2013 and 2018, equivalent to around US$14.5 billion. Meanwhile, for Qatar 2022, the IMF estimated that visitor spending and revenues associated with broadcasting contributed up to 1.0% of GDP that year.

Tourism will be the main transmission channel, although projections still show a wide margin of uncertainty. Some estimates anticipate the arrival of just over 800,000 visitors, while other scenarios project flows close to 2 million tourists. This increase in arrivals could mainly benefit services linked to visitor mobility and consumption, particularly hotels, restaurants, transportation, and entertainment. However, the final impact could be limited by a lower flow of regular tourists during this season due to factors such as insecurity and higher prices in the host cities.

In terms of investment, the effect will also be relatively contained. Spending associated with the World Cup is estimated at around US$2.5 billion, a moderate figure compared with that observed in other host countries. In the case of Mexico City, although around MXN 29.6 billion has reportedly been allocated to more than 2,000 projects linked to the event—including airport renovations, upgrades to subway stations, the expansion of the light rail, and mobility projects—much of this spending corresponds to remodeling, maintenance, and targeted urban improvements. As a result, rather than triggering a large-scale public or private investment cycle, the World Cup appears to be accelerating adjustments to existing infrastructure, with a limited impact on productive capacity and long-term structural connectivity.

At the sectoral and regional levels, the benefits will be concentrated. The services sector will be the main recipient of the boost, with possible increases in hotel occupancy, restaurant consumption, event-related sales, and temporary employment. Geographically, Mexico City would capture most of the impact, followed by Guadalajara and Monterrey to a lesser extent.

From a macroeconomic perspective, estimates point to a moderate effect on GDP, with an approximate increase of between 0.1% and 0.2%, concentrated mainly in June and July. In more optimistic scenarios, the impact could approach up to 0.25% of annual growth, depending on the scale of tourism spending, event-related consumption, and the absorption capacity of local services. However, even under these assumptions, the World Cup is unlikely to significantly alter the medium-term growth dynamics of the Mexican economy.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.