HIGHLIGHTS

- It’s all about inflation data next week in Latam, with June CPI releases on tap from Brazil, Chile, Colombia, and Mexico, alongside the BCRP’s rate decision where a rate hold is widely expected.

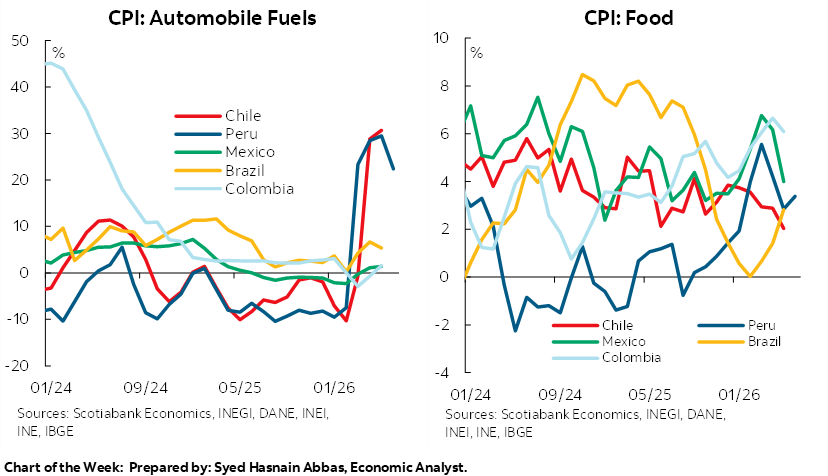

- Inflation is forecast to accelerate in Chile and Colombia, pick up less so in Brazil, and decelerate in Mexico as headline prices in the region dance to the tune of energy and food prices, impacted by external or weather developments.

- Mexican investment will likely break its long streak of year-on-year decline in April data due next week, but the overall investment backdrop remains depressed amid domestic and external headwinds. On the latter, the team in Mexico focuses on the latest CUSMA developments in today’s report.

- The pickup in Chilean inflation stands in contrast to recent weakness in economic figures in the country that complicate the BCCh’s stance. In today’s Weekly, our economists in Chile cover the latest labour market data showing the unemployment rate currently around a five-year high, while economic activity extended its losses in May.

Chart of the Week

REGIONAL CPI AND BCRP DECISION

Juan Manuel Herrera, Director

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- It’s all about inflation data next week in Latam, with June CPI releases on tap from Brazil, Chile, Colombia, and Mexico, alongside the BCRP’s rate decision where a rate hold is widely expected.

- Inflation is forecast to accelerate in Chile and Colombia, pick up less so in Brazil, and decelerate in Mexico as headline prices in the region dance to the tune of energy and food prices, impacted by external or weather developments.

- Mexican investment will likely break its long streak of year-on-year decline in April data due next week, but the overall investment backdrop remains depressed amid domestic and external headwinds. On the latter, the team in Mexico focuses on the latest CUSMA developments in today’s report.

- The pickup in Chilean inflation stands in contrast to recent weakness in economic figures in the country that complicate the BCCh’s stance. In today’s Weekly, our economists in Chile cover the latest labour market data showing the unemployment rate currently around a five-year high, while economic activity extended its losses in May.

It’s all about inflation data next week in Latam, with June CPI releases on tap from Brazil, Chile, Colombia, and Mexico, alongside the BCRP’s rate decision, all in contrast to a quieter calendar abroad, with global markets more liable to trade in reaction to Fed speakers, meeting minutes from the Fed and ECB, and whichever direction AI equities sentiment and Middle East risks shift toward. We’ll also be keeping an eye on any possible developments on the CUSMA front after the U.S. declined to renew the trade deal earlier this week, thus setting up annual reviews of the agreement—though we think an arrangement will be reached over the next few months. OPEC+ is expected to announce another output hike at its weekend gathering, just as flows from the Middle East quickly ramp up with the Strait of Hormuz reopening.

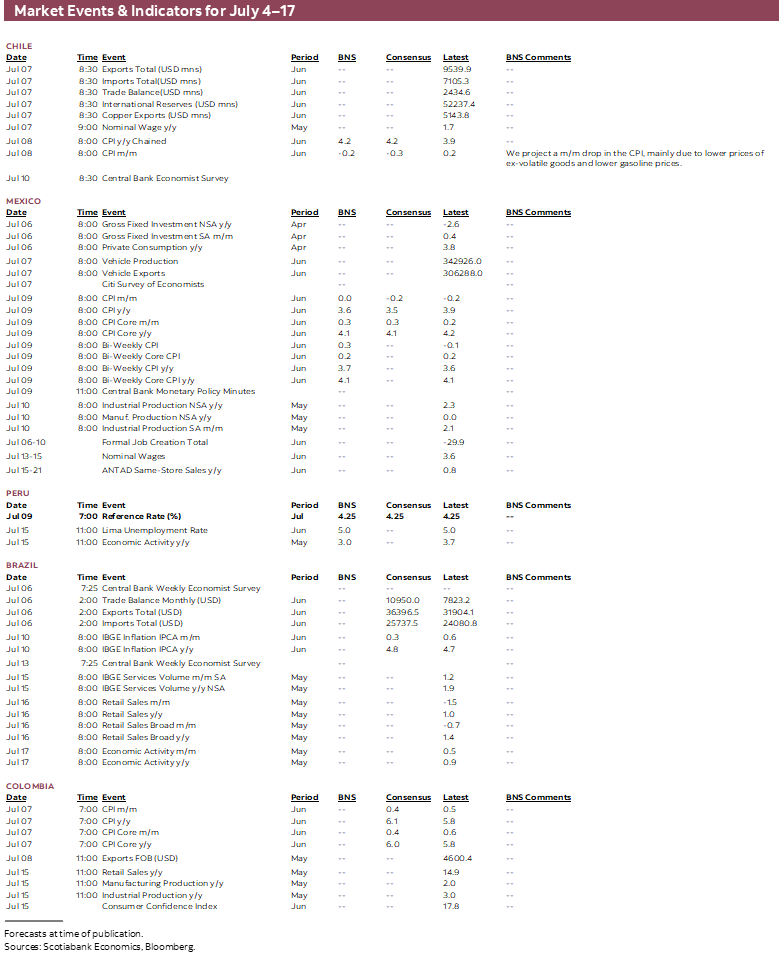

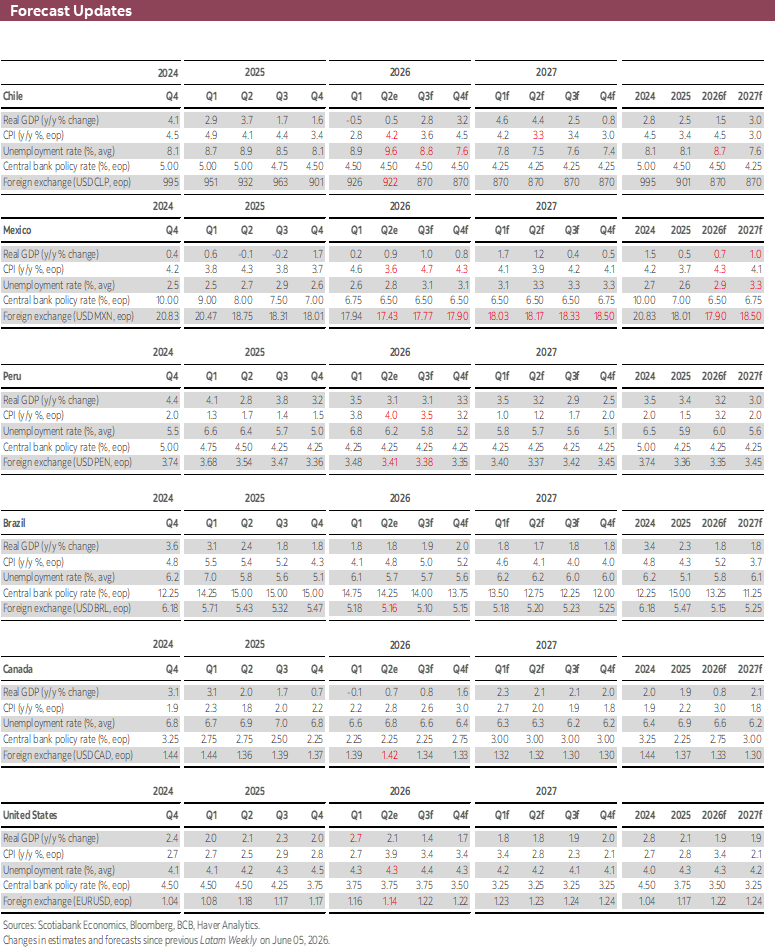

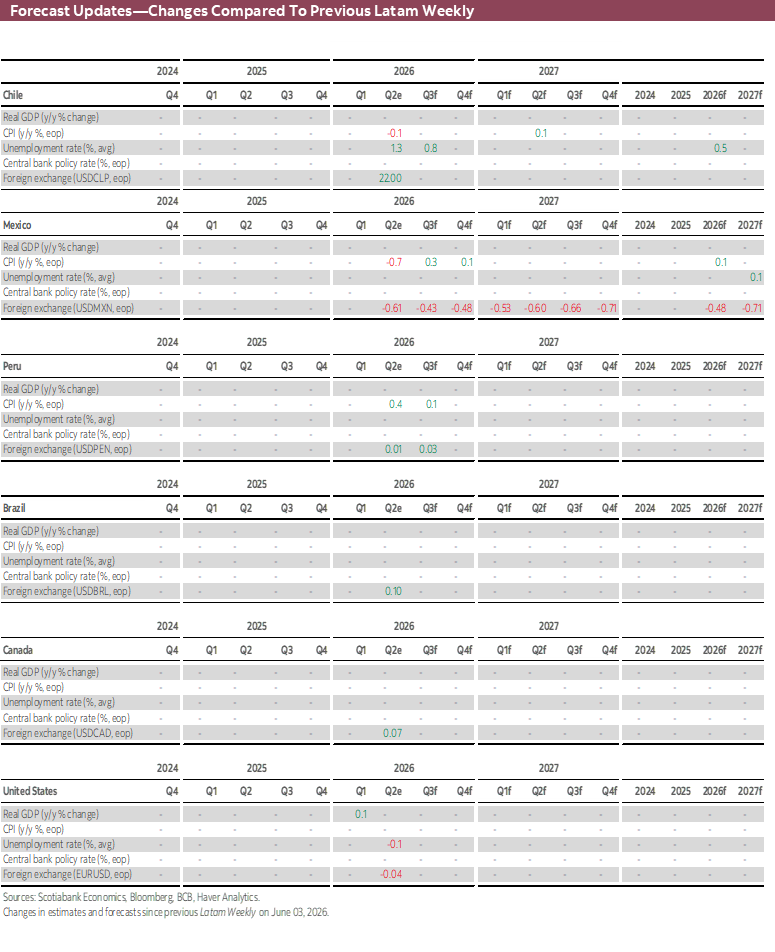

Our economists in Chile project that inflation accelerated to 4.2% y/y in June from 3.9% y/y, nearly 2 ppts above the recent low of 2.4% y/y in February. Prices are expected to fall by about 0.2% m/m, or half of last June’s 0.4% decline, as price gains in services and housing partly offset lower gasoline prices—in line with falling oil prices—and seasonal Cyber Day discounts. While energy price risks are fading, underlying inflation metrics remain relatively hot and CLP weakness is an important risk of ‘imported’ inflation, while El Niño will likely pressure food prices higher. All in all, we project that inflation will cool to 3.6% in Q3-26 but then pick up to 4.5% in Q4-26.

The BCCh may find a brief window to ease policy settings in the third quarter, given weak economic conditions—as seen with the 0.9% y/y decline in May economic activity data released earlier this week—although underlying inflation metrics and external factors would have to cooperate. In today’s report, our team in Chile covers the latest employment data in the country, with the jobless rate sitting at its highest level since mid-2021, prompting a revision higher to our unemployment rate forecast amid fading economic momentum, with GDP expected to grow by only 1.5% this year (a full percentage point slower than last year’s 2.5% expansion).

In Mexico, inflation should slow from the high 3s to the mid 3s in June data due on Thursday, in line with the downside surprise in H1-Jun CPI data released last week which came in at 3.55% versus 3.72% expected. All is fine and well (relatively) in headline inflation land as food inflation cools from steep 5%+ levels over the February to April period. The same cannot be said for core inflation, which continues to hang around the 4% mark and is only expected to marginally slow to 4.1% from 4.2% in May with core services caught around the 4.5% level since early-2025 and with no signs of easing.

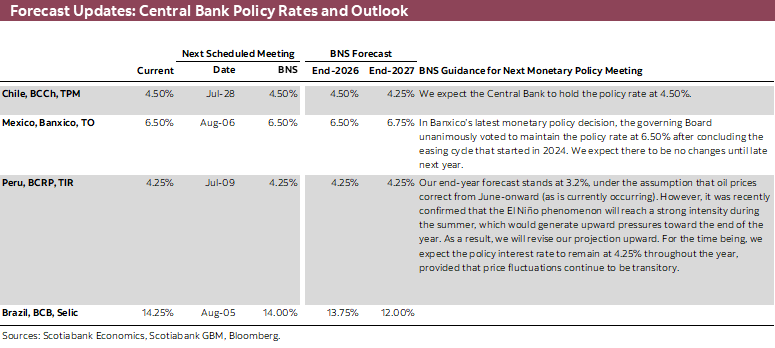

The stickiness in core inflation currently rules out any possible downside policy adjustments by Banxico, with the bank guiding rate stability over the medium-term. The bank’s meeting minutes out on Thursday should shed some light on the bank’s assessment of risks. On the flip side of inflation risks, economic metrics remain weak. Most notably, investment has contracted in year-on-year terms every single month since November 2024 amid depressed business confidence due to domestic policy decisions (AMLO/Sheinbaum reforms) and external risks (U.S. tariffs and CUSMA renegotiation). Our economists in Mexico briefly go over what awaits following the U.S.’s decision on CUSMA this week.

We may, however, see investment data for April out on Tuesday break its long negative streak. Construction output, as per industrial production data, rose by 10.4% y/y in April in its best gain in about two years on the back of residential construction (rebounding from a weak March). The residential sector has generally been the sole positive performer in investment, with the help of public programs, while now-stable public works (after steep declines) and depressed machinery and equipment outlays pull in the opposite direction. The weakness in machinery and equipment investment is a clear reflection of the uncertain domestic and external environment which constrains the country’s productive capacity over the coming quarters. So, while a positive y/y print for fixed investment is a positive, underlying details continue to paint a picture of muted sentiment and underperforming GDP growth.

On Friday, Brazilian inflation is seen slightly accelerating in June to 4.8% from 4.7% y/y, roughly in line with mid-month IPCA-15 results that showed a pickup in food inflation and a slight slowing in transportation inflation where higher airfares inflation counteracted most of the benefits from declining fuel inflation. Similarly to Banxico, the BCB is struggling with elevated underlying inflation metrics that are showing limited signs of letting up. An uptick in long-term inflation expectations that is drifting away from the 3% target (13–24 months at 3.9%) signals to the bank that economists believe settings may not be significantly restrictive or that would-be rate cuts would result in deviations from the inflation goal. With inflation elevated and the economy generally holding up—albeit at a soft pace as fiscal support is countered by restrictive policy conditions—there is little to motivate the BCB toward additional rate cuts. Currently, markets are pricing in an unchanged BCB rate of 14.25% at the close of 2026, compared to a 12–50–12.75% that was priced in at the beginning of the year.

There’s not much for the BCRP to do as things stand. Domestic inflation is elevated, at 3.6% as of June, and there are important price risks from El Niño that are building alongside rising expectations for a stronger weather event. But crude oil prices have significantly corrected in recent weeks, in line with our team’s expectations, and the BCRP will likely perceive the recent energy shock and the ongoing and future El Niño shocks on agricultural and fish prices as merely transitory, requiring a patient approach to policy settings. The policy rate may currently be somewhat accommodative considering the recent upward shift in inflation expectations, and the economy is running at a strong pace—more so when one sets aside El Niño headwinds and the impact of the Camisea gas pipeline leak. So, there may be a world at future meetings when the BCRP considers a hike if inflation (and expectations) fails to realign towards target quickly enough and the economy continues to exceed expectations, but that is not our baseline. For now, the BCRP remains in a data and weather dependent stance that would translate into rate stability were conditions to evolve in line with our forecasts.

COUNTRY UPDATES

Chile—Labour Market Weakens Further as Activity Loses Momentum

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

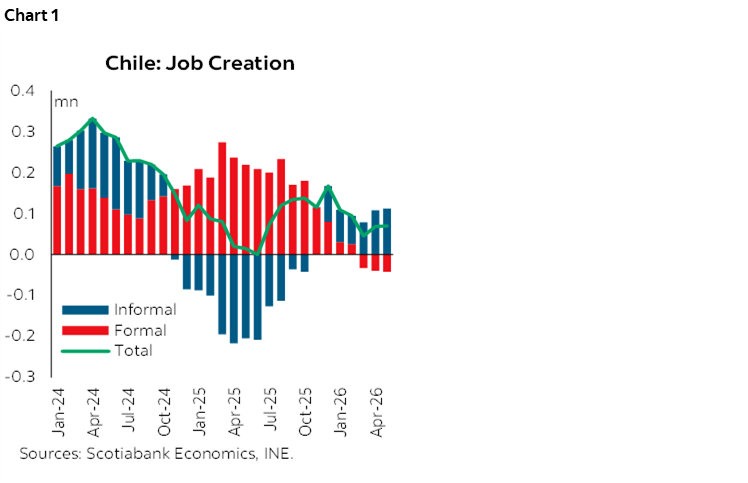

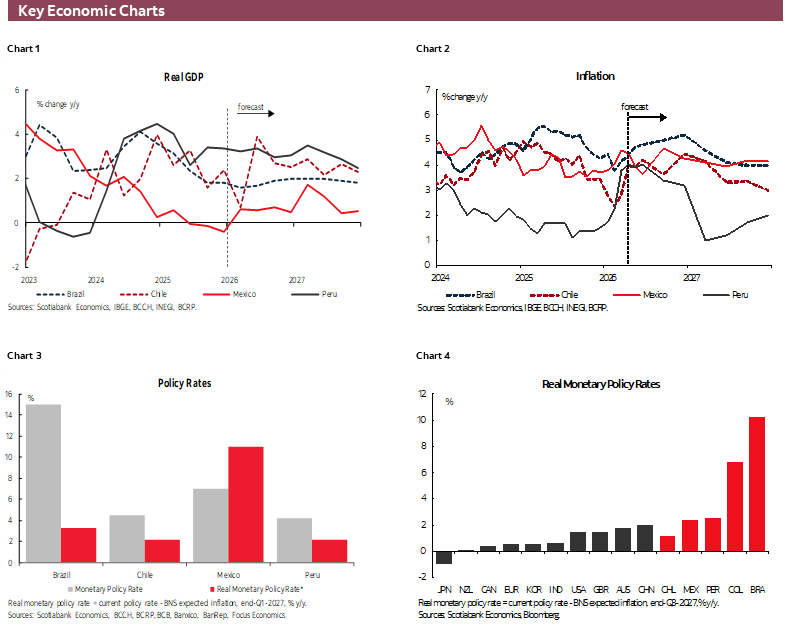

The unemployment rate increased to 9.4% in the rolling quarter ending in May (9.2% SA), exceeding both market expectations and our forecast. The result was explained by the destruction of 11k jobs relative to the previous rolling quarter, coupled with an increase of 25k people in the labour force. Widening labour market slack is translating into a continued deceleration of the wage bill, raising downside risks for private consumption in the coming months.

Meanwhile, formal employment posted a third consecutive year-on-year contraction in May (chart 1). Formal employment fell by 43k jobs y/y, with losses concentrated in real estate-related activities and construction. Indeed, the construction sector alone shed more than 30k jobs compared with the previous rolling quarter, marking the second-largest decline observed over the past ten years, excluding the pandemic period. Similarly, real estate activities lost more than 10k jobs in May, reflecting a slowdown in sales momentum following the boost provided by the mortgage interest-rate subsidy program implemented several quarters ago.

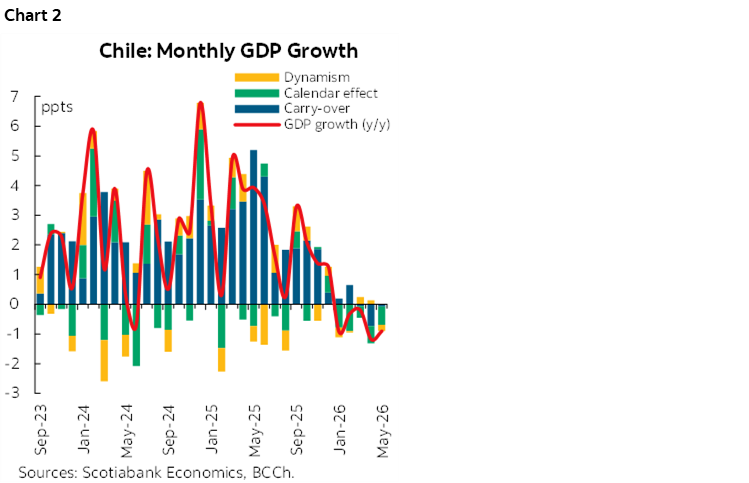

These labour market developments are consistent with an economy that continues to lose momentum. GDP contracted 0.9% y/y in May, broadly in line with our year-on-year and seasonally adjusted forecast, but noticeably weaker-than-market expectations. Nearly all sectors recorded either flat or negative seasonally adjusted growth relative to the previous month, a result we had anticipated based on high-frequency indicators and which was subsequently confirmed by the sectoral data released by the INE.

We observe a genuine deterioration in annual growth. For the second consecutive month, seasonally adjusted GDP contracted on a year-on-year basis, suggesting that the recent weakness extends beyond temporary seasonal factors or calendar effects (chart 2). Following a 0.2% m/m SA decline, non-mining GDP has now accumulated three consecutive quarters of stagnation, reinforcing signs of a broad-based loss of momentum across domestic activity.

Consistent with our 1.5% GDP growth forecast for this year, we have revised our near-term unemployment rate projections higher, reflecting a labour market that is likely to remain under pressure in the coming quarters. The weak May GDP reading reinforces this assessment, confirming that economic growth remains subdued and that underlying activity continues to lose traction.

Mexico—CUSMA Review: A Critical Milestone, but Limited Risk to North American Integration

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

On July 1st, 2026, the joint review of the Canada-United States-Mexico Agreement (CUSMA) formally began. The agreement underpins nearly US$2 trillion in annual trade and connects a market of more than 519 million consumers. While recent remarks by President Donald Trump have raised uncertainty over the agreement’s future, most analysts view a breakdown as unlikely, given the depth of economic integration already achieved across North America.

Since NAFTA came into force in 1994 and was later modernized through CUSMA in 2020, regional supply chains have become increasingly embedded in strategic sectors such as automotive, manufacturing, energy, and agrifood. Mexico and Canada now account for nearly 28% of U.S. foreign trade, while China’s share has declined significantly. This shift has positioned Mexico as the United States’ leading trading partner and reinforced North America’s role as an integrated production platform amid intensifying competition from Asia.

That said, trade tensions have intensified since 2025. The Trump administration has imposed several tariffs on Mexican and Canadian imports, particularly in steel, aluminum, and automotive products, citing national security concerns. Even so, most goods that comply with CUSMA rules of origin continue to benefit from tariff exemptions, underscoring the agreement’s economic relevance for businesses and consumers across the three countries.

The review process opens three potential paths: extending the agreement for another 16 years through 2042, keeping it in force subject to annual reviews, or, in a less likely scenario, triggering a withdrawal process. Following last Wednesday’s meeting, it became clear that the United States is not initially seeking an automatic renewal, arguing that trade imbalances and outstanding issues must first be addressed. Ebrard noted that this position had already been anticipated, adding that annual reviews could provide a framework to resolve differences among the three countries and reduce uncertainty around specific provisions of the agreement.

Negotiations are expected to focus on targeted adjustments rather than a broad renegotiation. The United States will likely push for stricter rules of origin to limit Chinese content in regional exports and increase U.S. content in manufactured goods. Mexico and Canada, in turn, will seek to preserve preferential access to the U.S. market and ease restrictions affecting strategic sectors.

For Mexico, the priority is to preserve the certainty that has supported its consolidation as the United States’ top trading partner and to further strengthen its role within North American value chains. Mexican exports exempt from tariffs have consistently remained between 80% and 85%. Despite the political noise, the scale of regional trade, the depth of productive integration, and the need to enhance competitiveness vis-à-vis China suggest that the most likely outcome is continuity of the USMCA with gradual adjustments, rather than a structural overhaul or the agreement’s eventual dissolution.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.