HIGHLIGHTS

- Rate decisions in Latam and across the G10 await next week alongside a flood of key macroeconomic figures (CPI and GDP) that will vie for the market’s attention against developments in the Middle East.

- In today’s report, our team in Chile go over their out-of-consensus call for a strong expansion in economic activity in March, President Kast’s first month in office.

- Mexican GDP growth is estimated to have flatlined in Q1-26 and inflation held roughly steady in H1-April, but our economists argue that Banxico should err on the side of caution and hold policy unchanged at its early-May meeting.

- Peruvian inflation was likely little changed in April after a large fuel prices shock in March, with the end of Q1 also seeing a slowdown in economic growth. Peru’s strong performance was temporarily delayed from disruptions in natural gas supplies, as detailed by our local team in today’s note.

Chart of the Week

PACKED SHORTENED WEEK WITH CENTRAL BANKS, GDP, AND CPI ON TAP

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Rate decisions in Latam and across the G10 await next week alongside a flood of key macroeconomic figures (CPI and GDP) that will vie for the market’s attention against developments in the Middle East.

- In today’s report, our team in Chile go over their out-of-consensus call for a strong expansion in economic activity in March, President Kast’s first month in office.

- Mexican GDP growth is estimated to have flatlined in Q1-26 and inflation held roughly steady in H1-April, but our economists argue that Banxico should err on the side of caution and hold policy unchanged at its early-May meeting.

- Peruvian inflation was likely little changed in April after a large fuel prices shock in March, with the end of Q1 also seeing a slowdown in economic growth. Peru’s strong performance was temporarily delayed from disruptions in natural gas supplies, as detailed by our local team in today’s note.

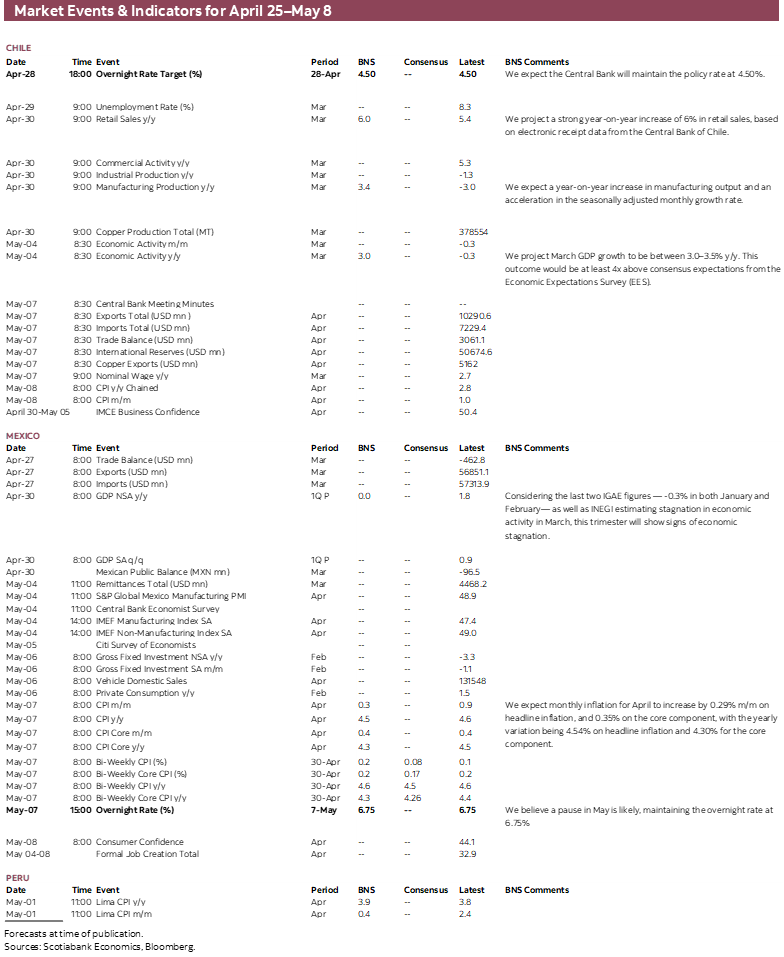

April closes out with a bang next week with all major economies in Latam and the G10 having key data and events on the calendar that will contend for the spotlight with Middle East developments. Thankfully, most countries outside of the anglosphere will have May 1st off for an extra day of recovery to come back to a quieter, though still busy, week that will include Latam CPIs, Banxico, and U.S. and Canadian jobs data, among other key events and data.

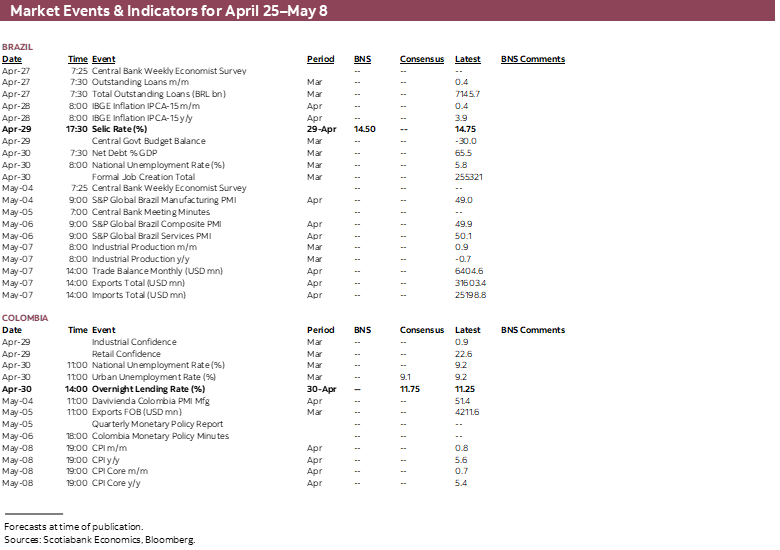

This week, we’ll have central bank decisions in Chile, Brazil, Colombia, the U.S., Canada, Eurozone, the U.K., and Japan with only the BCB and BanRep expected to shift their policy settings, with the former cutting by 25bps (more on this below) and the latter likely hiking by 50bps. On the data front, April CPI from Brazil and Peru are the highlight in Latam alongside Mexican Q1 GDP, with GDP releases also due in the U.S., the Eurozone, and Canada (monthly) while the Euro bloc, Japan, and Australia also release April inflation data. Chinese official PMIs await on Thursday.

On the political front, Peru’s vote count is slowly continuing (and expected to last until mid-May for official results) with no clear challenger to Fujimori for the early-June second round. Meanwhile, accusations of ‘irregularities’ are hanging over the legitimacy of April 5th vote, prompting the resignation of the head of the country’s national elections agency. In Colombia, the government’s order to fast track private pension funds transfers into the public system is weighing on local markets, while it is still unconfirmed whether Fin Min Ávila will attend next week’s BanRep decision (where a 50bps hike is expected if the meeting takes place).

Elsewhere, Canada’s Federal government presents its Spring Update, the confirmation of Warsh to Fed chair may continue to advance after the DoJ dropped its investigation into the Fed, and U.K. PM Starmer will remain under pressure to resign in relation to the Mandelson scandal.

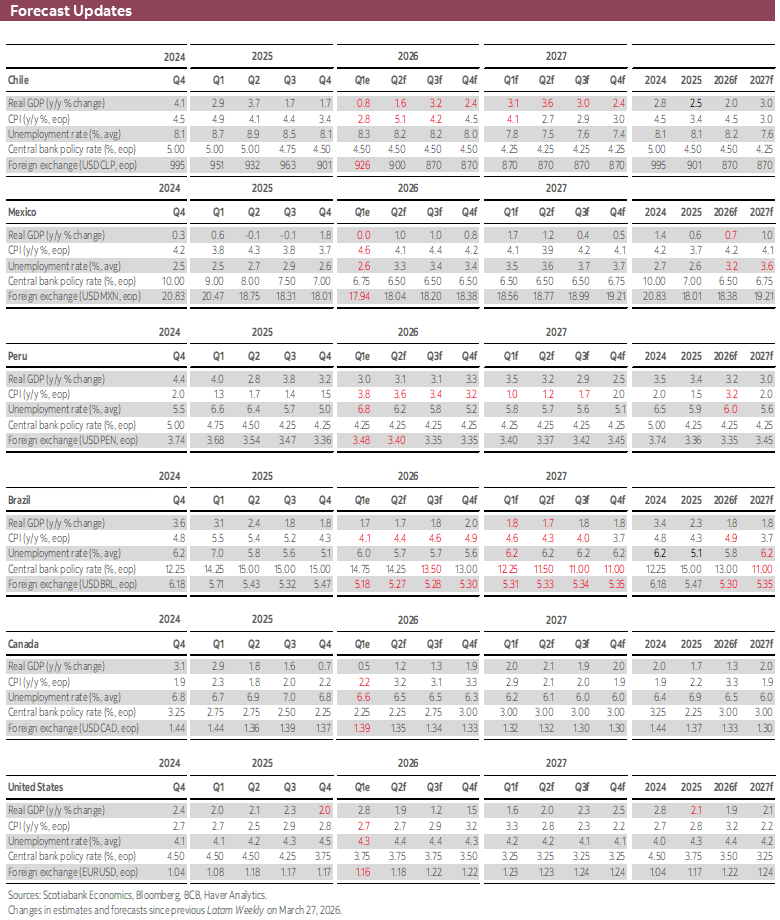

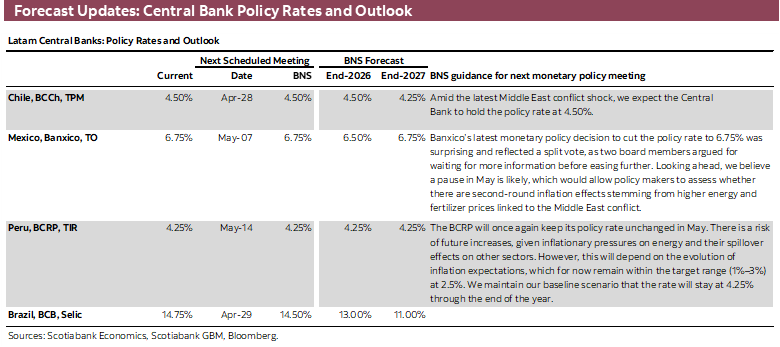

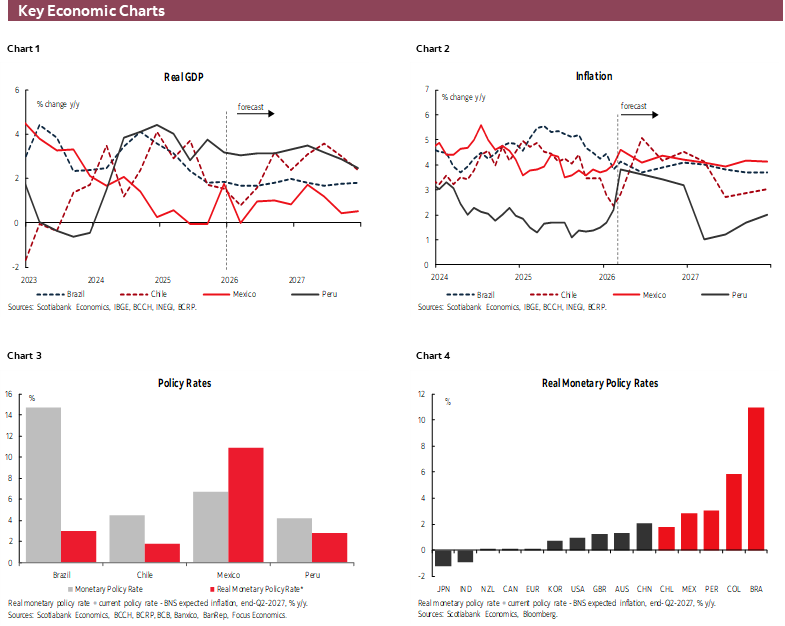

The BCCh is first out the gate among Latam central banks on Tuesday with a rate hold at 4.50% widely expected by economists and markets, with the latter not pricing in a first policy rate increase until the bank’s July or September announcement (our call is for steady rates through the balance of the year). In March, Chilean inflation jumped to 2.8% y/y from 2.4% in the previous month on the back of a 1% m/m rise in prices (double that of March 2025) driven by an 8.7% monthly increase in gasoline prices. We project that headline inflation could near the 5% mark at the end of Q2, i.e. roughly double its pre-war pace in February, but the BCCh will opt for rate stability rather than tighter policy—all conditioned on the evolution of external developments.

On the domestic front, we’ll get March unemployment rate, retail sales, and industrial/manufacturing industrial production figures on Thursday that are expected to show a firmer close to the quarter. In today’s Weekly, our local team go over their estimate for economic activity in March to have grown by 3–3.5% y/y based on their tracking of higher-frequency indicators and improving momentum across the main economic sectors. Such a print would deliver President Kast a strong start to his term, which could help rebuild some of the economic and business confidence that had grown ahead of his presidency but was shocked by Middle East conflict spillovers.

On Wednesday, the BCB is expected to announce another small 25bps reduction to 14.50% aimed at lessening its highly restrictive stance while still facing inflationary challenges that are now perhaps heightening due to the global energy prices shock. Brazilians saw a relatively modest ~5% increase in prices at the pump in March thanks to government tax cuts and subsidies on fuels, but these are having a growing impact on fiscal accounts and losses at Petrobras that are placing President Lula in an uncomfortable position ahead of the October general election.

The incumbent, however, seems likely to continue and possibly expand social spending/subsidy programs to strengthen his chances at re-election, which would in turn limit the BCB’s space to ease owing to firmed-up demand and fiscal risks. For now, Flavio Bolsonaro’s advance in head-to-head polls with Lula has seemingly stalled at a statistical tie, with the former president’s son now needing to appeal to a more middle-of-the-road share of the electorate for whom the Bolsonaro name brings back bad memories.

Next Tuesday’s mid-month IPCA inflation reading for April is expected to accelerate from the high-3s to the mid-4s as the data take into account a greater share of the increase in gasoline prices since late-February. The data will also show accelerating food inflation possibly reflecting rising transportation bills as well as seasonal factors. A ~4.5% print would take headline inflation to around its levels at the start of the year, with economists polled by the BCB projecting that it will close 2026 at 4.8% (nearly 1ppt above the 3.9% level they had at end-February). In line with this shift in inflation expectations, the median economist predicts that the BCB’s Selic rate will finish 2026 at 13.00%—up from 12.00% in the late-February poll—while markets think the BCB will only cut to 13.75% or 14.00% this year.

Mexico’s calendar highlight will be the release of Q1 GDP on Thursday, with data received so far pointing to a clear deceleration in economic momentum since the turn of the year, practically undoing the optimism that had built over the final quarter of 2025. February economic activity data published this morning showed a contraction of 0.3% y/y, matching January’s loss, with a marginal 0.1% m/m gain falling very short of undoing the previous month’s 0.7% monthly fall. Based on these figures and preliminary guidance from INEGI that the economy failed to materially pick up in March, we project that Mexican GDP flatlined in y/y terms and contracted on a q/q basis in Q1-26—a stark contrast to the 1.6% y/y and 0.8% q/q expansions of Q4-25.

These economic results would likely reinforce the dovish stance of the majority in Banxico’s board to favour a final rate cut to 6.50% as soon as its May rate announcement. However, our economists argue in today’s report that the central bank should opt for caution in the face of elevated uncertainty and upside risks to inflation, while inflation expectations are also failing to converge with the bank’s 3% goal and have recently risen.

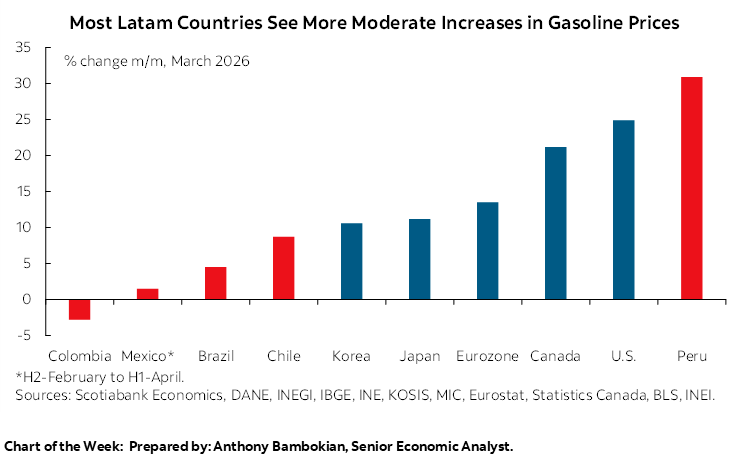

Peruvian CPI due on Friday (holidays or weekends are no challenge to the INEI’s release schedule) is seen ticking only slightly higher at 3.9% from 3.8% in March as the worst of higher energy prices (and food to some degree) was already apparent in the previous month’s reading. When compared to other countries in Latam, or major economies around the globe, Peruvians saw among the highest immediate shocks in gasoline prices, which soared by 31% m/m as per official CPI figures. According to Osinergmin, regular gasoline prices as of April 20th were practically unchanged from their late-March levels (though declining from higher levels earlier in the month).

In today’s note our colleagues cover their expectation for Q1-26 GDP growth to come in at 3% y/y (data are due for release in mid-May), slowing a touch from the 3.2% rise with which it closed 2025. Despite the moderation in growth, Peru’s economy continues to expand at a solid rate, outpacing its peers in the region, and with the cooling of growth in Q1 mostly reflecting the temporary suspension of gas supplies due to a pipeline leak.

COUNTRY UPDATES

Chile—We Expect March GDP Growth Between 3.0–3.5% y/y

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

Based on our nowcasting model, together with high-frequency indicators (electronic receipts and invoices, mining production results, mobility indicators and external accounts data), we project March GDP growth in the range of 3.0–3.5% y/y. This figure would significantly exceed the consensus expectation (EES: 0.7% y/y). Both our estimate and the consensus incorporate one additional working day compared to March last year.

The main drivers behind this strong y/y performance—more than four times the EES expectation—are the absence of negative supply shocks from primary sectors, together with a genuine improvement in seasonally adjusted monthly momentum across all economic sectors. The upper bound of our estimate would materialize if the seasonal adjustment were stronger than our conservative assumption, particularly given the unusually large negative seasonal effect observed in February.

This would be the first positive growth print to be widely associated with the new government, following two consecutive negative y/y readings (January: -0.5%; February: -0.3%). As such, it could generate positive feedback effects on confidence indicators and growth expectations for the year. In this context, the 2026 GDP growth consensus, currently at 2.0%, would likely be reinforced. Nevertheless, at this stage we see no room to argue for growth beyond that level, given the ongoing fiscal adjustment, the local impact of the external scenario, and the resulting erosion of purchasing power due to higher inflation.

From a monetary policy perspective, we expect the central bank to adopt a cautious interpretation of the print, avoiding an overreaction to a single upside surprise versus consensus and instead assessing the data jointly with the weak readings observed in January and February.

Mexico—Banxico Could Cut Rates in May, But Should It?

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

The inflation print for the first half of April was released earlier this week, in line with recent statements and public remarks by members of Banco de México’s Governing Board. Headline annual inflation stood at 4.53%, slightly below the 4.55% recorded in the second half of March, though above the 4.50% anticipated by consensus. Overall, this reading confirms that while inflation has moved past its peaks, inflationary pressures have persisted since the beginning of the year, remaining well above the central bank’s target of 3%.

From a component perspective, inflation continues to be driven mainly by the non-core component, while core inflation has begun to show slightly clearer signs of deceleration, particularly through the goods category. The latter has followed a downward trajectory since January of this year, suggesting a gradual moderation of pressures associated with supply chains and production costs.

Within the core component, processed food, beverages, and tobacco stand out. Although this category has shown some marginal deceleration, it remains at elevated levels—at 5.4% year-over-year—continuing to represent a significant source of pressure on headline inflation. Moreover, a potential rebound in this category cannot be ruled out in the short term should additional pressures materialize from higher energy prices. In contrast, non-food goods have shown a more encouraging trajectory, already falling just below the 3.0% target, reflecting a more consistent normalization in this segment.

On the non-core side, recent fortnights have observed a significant rebound in agricultural prices, particularly fruits and vegetables, which posted annual growth of 23.03%. This increase is, associated with adverse weather shocks as well as disruptions in production and distribution logistics. These factors are compounded by lingering risks from higher international prices of energy and fertilizers, which could further intensify price pressures in the coming months. Although the federal government has partially contained energy prices through subsidy schemes, we believe this containment may not be sustainable over time, particularly in an environment of heightened international volatility.

At first glance, the inflation reading for H1-Apr could open the door to an additional policy rate cut by Banxico in May, in line with the more dovish stance expressed by some deputy governors. However, it is important to emphasize that inflation expectations for 2026 and 2027 remain significantly above the 3% target and have been revised upward in the latest surveys. In fact, headline inflation expectations for 2026 are above the central bank’s tolerance range (2-4%). This factor has been repeatedly highlighted by members of the Governing Board as a key consideration in assessing the monetary policy stance, given the risk of expectations becoming unanchored.

In addition, relevant external risks persist. The war in the Middle East has not concluded, and energy and fertilizer prices continue to face upward pressure. While these pressures are primarily supply-driven, their persistence—combined with elevated inflation levels and expectations that are not yet fully anchored—could lead to second-round effects, especially if markets perceive a permissive monetary policy stance from Banco de México.

On the domestic front, although economic activity has shown signs of deceleration—reflected in weaker consumption dynamics, as evidenced by February retail sales—prices in the services component, and to a lesser extent goods, continue to grow at elevated rates. This behaviour suggests that despite slower economic momentum, domestically driven inflationary pressures remain present, increasing the risk that upward revisions to expectations could spill over more broadly.

In conclusion, we believe that a policy rate cut in May is a plausible scenario, consistent with recent comments from some deputy governors. Nevertheless, we consider it is best to adopt a subsequent pause, as uncertainty remains high and the risks to inflation persist. In this context, for now, we still expect a last cut in June meeting, ending the year at 6.50%.

Peru—GDP Would Have Grown by Around 3% in the First Quarter

Pablo Nano, Deputy Head Economist

pablo.nano@scotiabank.com.pe

Gross Domestic Product (GDP) is estimated to have grown by around 3% during the first quarter (Q1 2026), a slightly lower rate than the 3.2% recorded in Q4 2025, according to our estimates. While economic activity accumulated an expansion of 3.2% between January and February, GDP is estimated to have experienced a notable slowdown in March, to around 2%, because of the temporary suspension of Camisea gas supplies during the first half of the month. This affected not only hydrocarbon production but also indirectly impacted sectors such as industry and transportation.

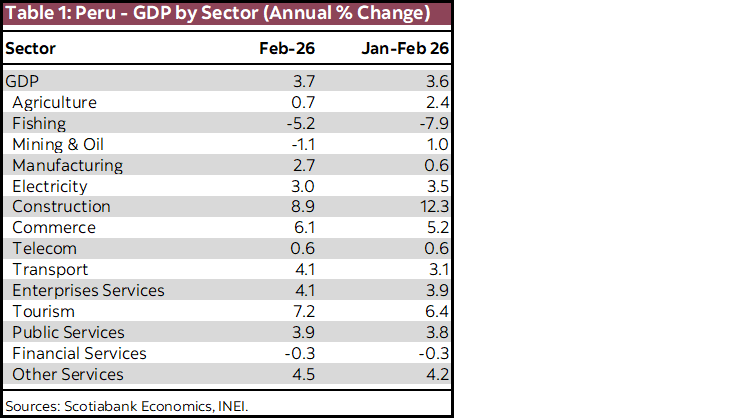

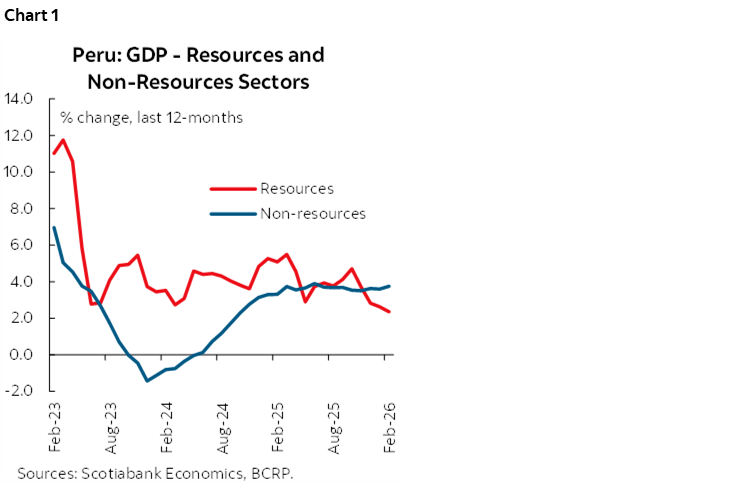

In February, GDP grew by 3.7% (table 1), above the 3.4% expected by the consensus of analysts, according to Bloomberg. The month’s growth was exacerbated by the increase in the Taxes category (+8.9%), which contributed 0.7 percentage points to February’s result (table 1). Aside from the above, GDP continued to be driven by non-primary sectors (chart 1) linked to domestic demand—given the dynamism of consumption and private investment—particularly construction (+8.9%), trade (+6.1%), and services (+3.4%).

On the other hand, the primary sectors showed negative growth, notably the fishing sector (-5.2%)—due to lower catches of species for direct human consumption, especially for the canning industry—mining and hydrocarbons (-1.1%)—due to a drop in the production of oil, molybdenum, and lead—and agriculture (-0.1%)—due to the early harvesting of crops such as grapes in previous months in anticipation of heavy rains associated with El Niño.

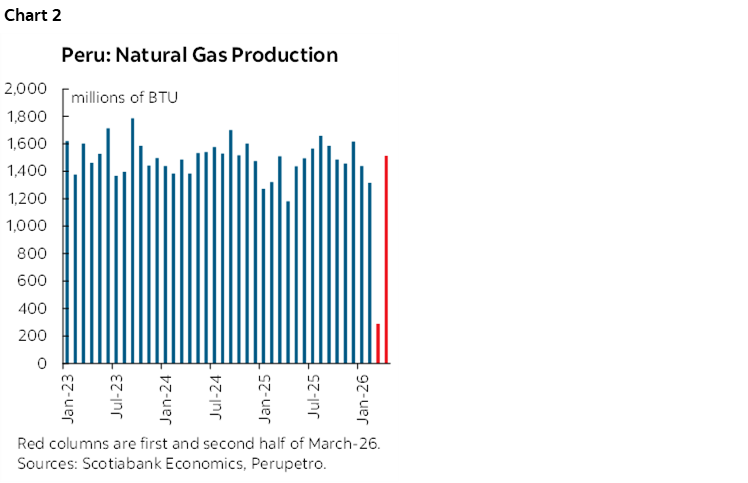

For March, we estimate that GDP grew by approximately 2%, its lowest level of expansion since November 2015. As is known, during the first half of the month, the supply of natural gas and natural gas liquids from Camisea was interrupted due to an incident on the pipeline. For this reason, hydrocarbon production registered a 35% drop in March (chart 2), which would subtract 0.6 percentage points from GDP growth for the month.

In addition, restrictions on the supply of natural gas and compressed natural gas (CNG) would have impacted the pace of activity in the manufacturing and transportation sectors, respectively. However, other leading indicators such as local cement consumption (+16.8%), the increase in imports (+19.7%), and sales of new light vehicles (+38.3%), would reflect that domestic demand maintained the momentum shown during the first two months of the year in March.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.