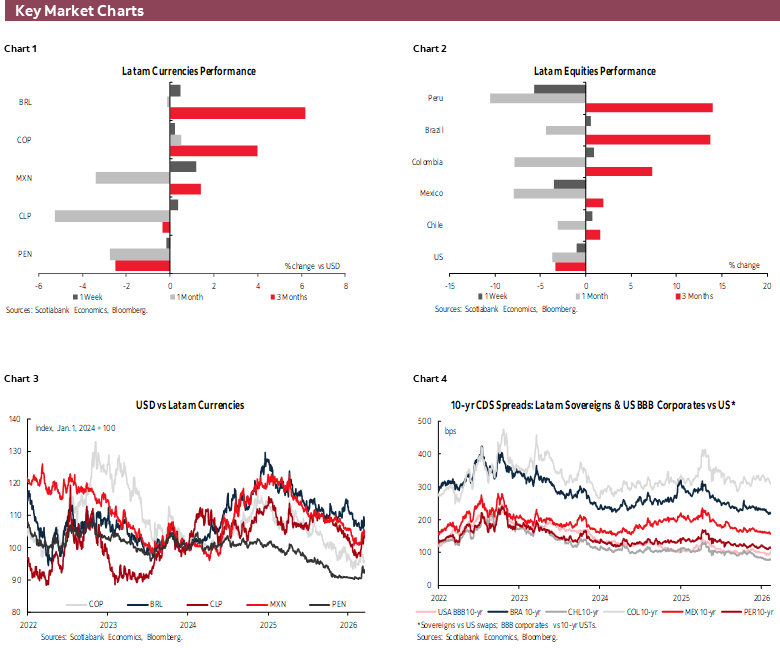

HIGHLIGHTS

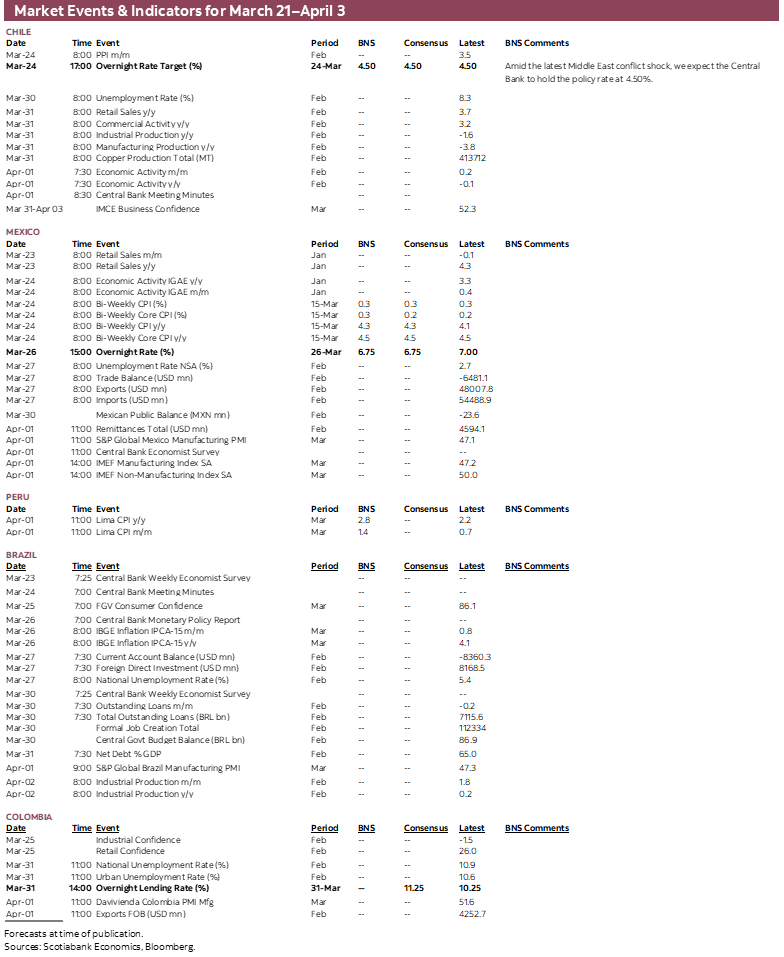

- Banxico and BCCh rate announcements, and the BCB’s minutes and quarterly report are next week’s Latam highlight with a strong focus on guidance and opinions on what the current energy price shock means for their respective economies.

- Backward-looking CPI data from Mexico and Brazil, and from some in the G10, may come and go while global markets focus on developments in the Middle East and an initial read of the economic impact of the conflict in global PMIs due on Tuesday.

- In today’s report, our economists in Mexico and Chile discuss their latest forecast changes, with the team in Mexico expecting that Banxico will stick to its dovish stance (despite growing inflation risks) and announce a rate cut next week. In Chile, the team expects rate stability over the balance of the year alongside upward revisions to their inflation forecast and a weaker growth outlook. The BCCh also publishes its Monetary Policy Report next week.

Chart of the Week

BANXICO AND BCCh DECISIONS, REARVIEW MIRROR INFLATION, FRESH PMIs

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Banxico and BCCh rate announcements, and the BCB’s minutes and quarterly report are next week’s Latam highlight with a strong focus on guidance and opinions on what the current energy price shock means for their respective economies.

- Backward-looking CPI data from Mexico and Brazil, and from some in the G10, may come and go while global markets focus on developments in the Middle East and an initial read of the economic impact of the conflict in global PMIs due on Tuesday.

- In today’s report, our economists in Mexico and Chile discuss their latest forecast changes, with the team in Mexico expecting that Banxico will stick to its dovish stance (despite growing inflation risks) and announce a rate cut next week. In Chile, the team expects rate stability over the balance of the year alongside upward revisions to their inflation forecast and a weaker growth outlook. The BCCh also publishes its Monetary Policy Report next week.

Hawkish G10 central bank announcements in recent days give way to announcements by Mexico’s and Chile’s central banks (and Norway’s) amid elevated uncertainty regarding the path for energy prices in the medium-term. In-region CPI releases, mid-March prints from Mexico and Brazil, as well as stale readings from the U.K., Japan, and Australia are on tap but should be generally dismissed by markets. On the macro front, S&P PMIs from around the globe due on Tuesday will give us an initial read by firms regarding the impact of the conflict in the Middle East. Peruvian and Colombian economic calendars are bare of major releases.

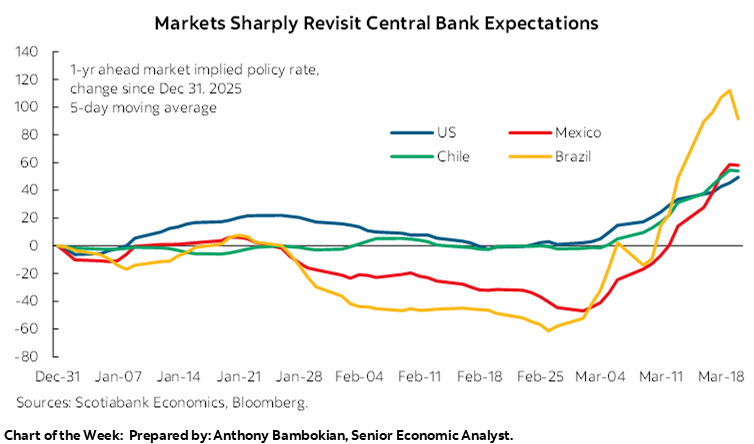

Markets are heading into the weekend with a pile-on in hike bets for the key central banks as soon as next month’s announcements. Attacks on Gulf energy infrastructure and no signs that the Strait of Hormuz is reopening soon are due to lengthen the period of elevated energy prices, thus risking larger and longer-lasting second-round effects on prices. Inflationary pressures will not just be present in energy prices, but in anything from agricultural goods—due to losses in fertilizers output and shipments—to manufactures—owing to soaring maritime fuel prices, and the possibility of fuel shortages in Asia—and to services—airfares above all, but broad services beyond that if high energy inflation lasts beyond a few months, impact inflation expectations and wages. The degree to which governments act to restrain energy prices will be key, but there’s only so much they can do, particularly with fiscal balances in a precarious position.

Mexico’s calendar is the busiest of all in the region. On the data front, the highlight is mid-March CPI on Tuesday, which will be accompanied by January economic activity data. The week starts with January retail sales figures and ends with February unemployment rate and international trade data. Inflation is seen accelerating from 4.1% y/y to 4.3% y/y in headline terms with core remaining around the mid-4s with both categories expected to rise by around 0.3% on a month-over-month basis—which is roughly twice the 0.14% headline rise this time last year but in line with the 0.24% core gain then. With prices for regular gasoline capped at MXN 24/litre, the impact of the run-up in global energy prices would be contained for now, but it remains to be seen how long the government can maintain this cap considering that WTI oil is up ~75% in the year-to-date.

Banco de México’s decision on Thursday is the main event, with us and most economists expecting the central bank to roll out another 25bps rate cut to take the overnight rate to 6.75%. Rather than believing that Mexico’s economy is in need of another rate reduction, and even less that now is the appropriate time to announce such a move, our call (and likely that of most economists) is predicated on comments by Banxico officials in recent days that—aside from Deputy Governor Heath—point to sticking to an easing stance. This is in opposition to markets that are pricing in very slim odds of a quarter-point reduction next week and are going as far as pencilling in hikes as soon as Banxico’s September announcement. A year from now, markets believe the overnight rate will be 100bps higher.

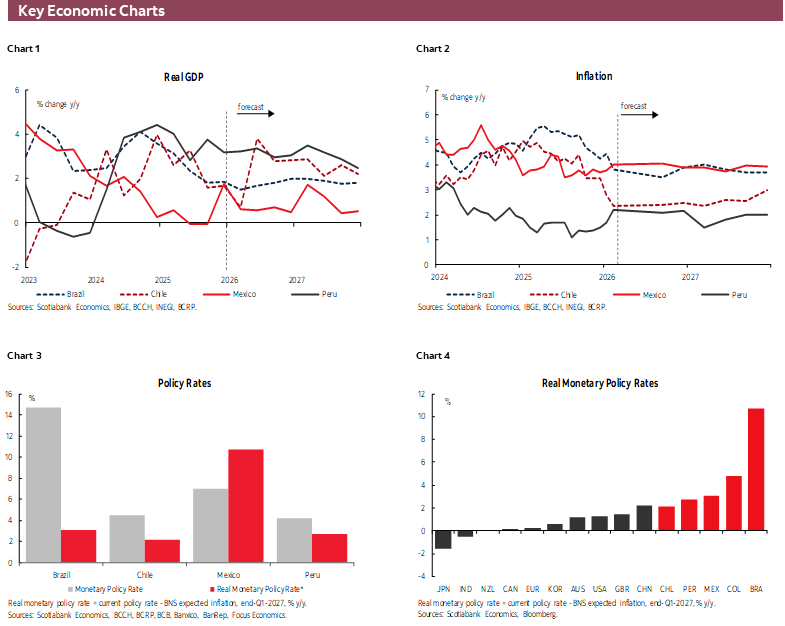

As our team discusses in today’s Weekly, their call is for Banxico to cut next week and once again over the balance of 2026 to close out the year at 6.50%, keeping with the bank’s dovish stance. GDP data for 4Q25 have also triggered an upward revision in our 2026 growth projection to a still-weak 1% expansion reflecting various headwinds including stagnant jobs creation and depressed private investment at home, and surging international energy prices and the USMCA review from abroad. Tuesday’s economic activity reading for January could ‘mathematically’ alter this call as a growth starting point, but the factors mentioned above, with a wide range of outcomes, will determine how Mexican growth fares this year.

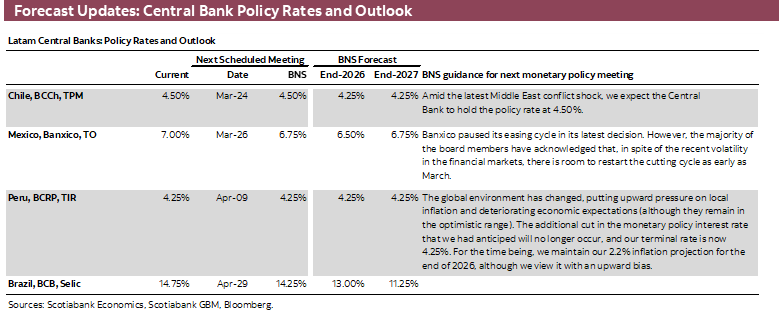

Our economists in Chile also go over their latest forecast changes ahead of the BCCh’s rate decision on Tuesday. In contrast to Mexico, recent economic data from Chile have surprised to the downside (and challenges have grown), resulting in a reassessment to a 2% GDP growth forecast in 2026 from 2.5% previously (slowing from 2.8% and 2.5% in 2024 and 2025, respectively). The BCCh’s guidance and updated forecasts in its Monetary Policy Report (MPR)—out the day after the rate decision and which will likely show higher inflation projections—will be in the spotlight with the bank widely expected to leave its rate unchanged at 4.50%. From the possibility of an additional rate cut in the near-term, local traders are contemplating the possibility of rate increases later in the year, although these wagers remained limited at one 25bps by year-end as of yesterday’s close.

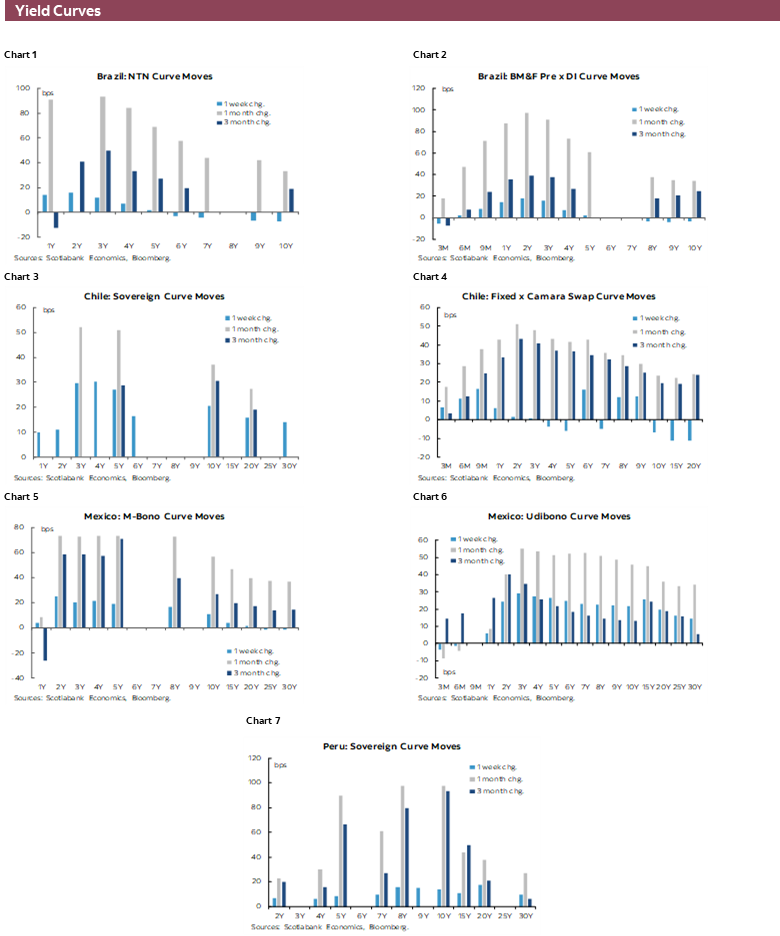

Brazil’s central bank will publish the minutes to this week’s meeting on Tuesday and release updated forecasts in its MPR on Thursday, with a focus on discussions regarding the future pace of easing after kicking off the cutting cycle with a 25bps reduction to 14.75% (focus also on the debate over the possibility of a larger cut or a rate hold). Unlike most major central banks around the globe, Brazil’s is heading into the current energy prices situation with a highly restrictive policy rate that even in the face of rising inflationary pressures may still require some loosening.

However, recent developments have materially limited room to the downside, particularly in the near-term (larger rate cuts may be pushed out to next year assuming energy prices normalize). By year-end, traders think that the BCB will only cut by between 75 and 100bps, compared to 250–275bps priced in at the end of February (latest cut inclusive). Brazil also releases IPCA-15 inflation data on Thursday, which is expected to decelerate to 3.7% from 4.1% in backward-looking figures that will not reflect the oil price shock.

COUNTRY UPDATES

Chile—Growth Revised Lower Amid Weak Early-2026 Activity

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

We’ve revised down our GDP growth forecast for 2026 to 2.0% from 2.5%. Beyond a more challenging external backdrop, recently released National Accounts figures point to a slowdown in activity at the beginning of the year. Achieving 2% growth in 2026 will require a faster pace of expansion in coming quarters. We continue to expect stronger activity dynamics driven by the materialization of strong private investment, which should support job creation and underpin private consumption. However, growth rates above 2% look difficult to achieve in light of recent weak activity data and persistent external headwinds.

Inflation Outlook Revised Up; Fuel Prices Pose Upside Risks

We revised up our December-2026 inflation forecast to 3.0%, from 2.5%, partly reflecting the recent oil price shock. We estimate a direct impact of around 0.5ppts on headline CPI this year. Importantly, we see rising risks of higher pass-through to domestic prices in the near term, as the Ministry of Finance has expressed concerns about lower fiscal revenues associated with continuing fuel price subsidies amid tight fiscal conditions. Should the government opt for a faster reduction in subsidies, fuel price increases would be passed through more rapidly to local prices, pushing inflation higher in the short term, particularly in March and April.

Monetary Policy: Rates On Hold, Macro Scenario Reassessed

In this context, we expect the Central Bank to keep the policy rate unchanged at 4.50% at its March 24th meeting. We also anticipate a reassessment of the macroeconomic scenario broadly in line with our forecast revisions, acknowledging higher short-term inflation pressures (4Q25 Monetary Policy Report: 3.2% y/y for December 2026) and slower GDP growth prospects for 2026 (4Q25 MPR: 2–3%).

Mexico—Revisiting the Numbers: 2026 Forecast Revision

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

The recent escalation of the conflict in the Middle East and its potential economic impact on Mexico, together with the 4Q25 GDP results, have led us to revise our forecasts for the main macroeconomic variables. This revision takes place amid rising uncertainty driven by the limited materialization of projects associated with the Plan México and, more broadly, by weak execution of both public and private infrastructure projects. On the public side, constrained fiscal space is likely to keep investment limited, while in the private sector the lack of clarity in operating rules for strategic industries, a weakening domestic legal framework, uncertainty surrounding the renegotiation of the USMCA, and fears over a possible U.S. military intervention in Mexico continue to weigh on investor sentiment.

Against this backdrop, we have revised our 2026 growth forecast upward from 0.6% to 1%. This adjustment mainly reflects the activity data observed in 4Q25, when GDP expanded 1.8% year over year, driven by a 7.8% increase in agricultural output and 2.1% growth in services, while industrial activity remained virtually stagnant at 0.3%. This outcome slightly raises the comparison base and mechanically improves the projected annual growth rate for 2026.

However, significant downside risks remain: formal employment shows signs of stagnation, business destruction is evident, and durable goods spending continues to contract, which could limit the contribution of private consumption. Consequently, our forecast remains conservative relative to market consensus, which expects growth closer to 1.5%.

On inflation, we view tensions in the Middle East as a source of persistent pressure on energy prices, with potential second-round effects on other goods and services. As a result, we have revised our 2026 inflation forecast upward from 3.9% to 4.2%, anticipating a peak between September and November of this year.

Regarding monetary policy, despite the upward revision to our inflation outlook, we have brought forward the timing of Banco de México’s next rate cut from May to March. This reflects the fact that most members of the Governing Board have emphasized that there is still room to ease monetary conditions, viewing inflationary pressures stemming from the war, tariff increases on countries without trade agreements, and higher health-related excise taxes as temporary supply shocks. Under this framework, we expect a 25 bps cut in March, a pause in May, and a possible additional adjustment during the summer, conditional on inflation expectations, exchange rate behaviour, and relative monetary conditions between Mexico and the United States. We therefore maintain our estimate for the terminal policy rate at 6.50% in 2026.

Finally, regarding the exchange rate, we made a marginal upward adjustment in line with market consensus. We expect the Mexican peso to trade within a relatively narrow range of 17.80 to 18.40 pesos per dollar during 2026, assuming no major risks materialize, such as an unfavourable USMCA renegotiation, an escalation in global geopolitical uncertainty, or episodes of domestic political instability.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.