HIGHLIGHTS

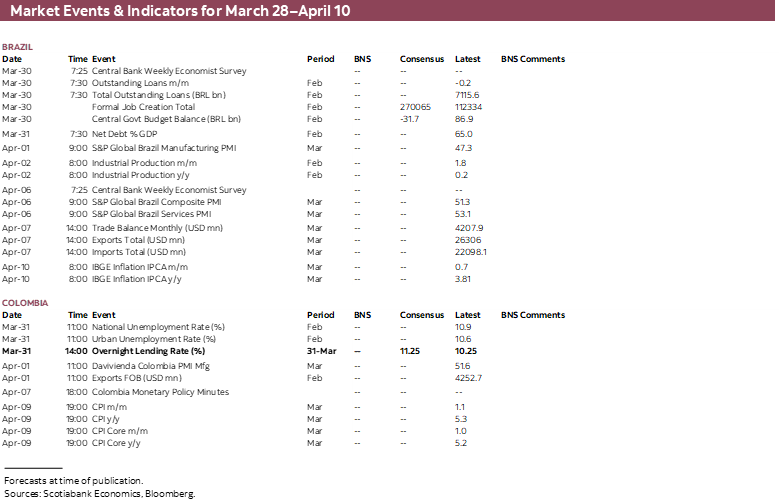

- Global CPI releases for March out over the coming week will give us the first official read into the (initial) inflationary impact of the Middle East conflict, with important implications for the April/May round of monetary policy decisions after the latest round saw the majority of central bankers take a hawkish stance. The U.S. releases a flood of macroeconomic data including March payrolls. Most countries’ markets will be closed on Friday for holidays, with Mexico and Peru also shut on Thursday.

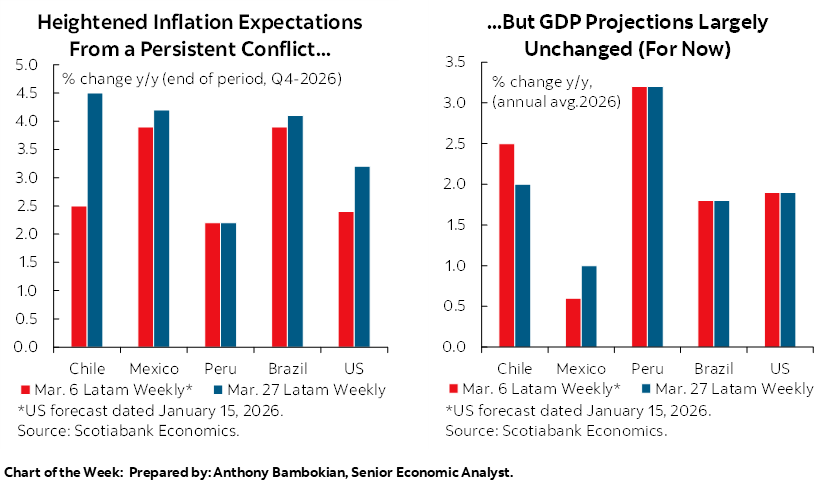

- In Latin America, Peruvian CPI is expected to jump to near 3%, following overshoots in mid-March inflation prints from Brazil and Mexico. The team discusses their projection in today’s Weekly, with the jump not only reflecting the effect of international energy prices, but also the impact of the Camisea gas pipeline leak and its temporary suspension, with the latter also expected to drag on economic activity in March.

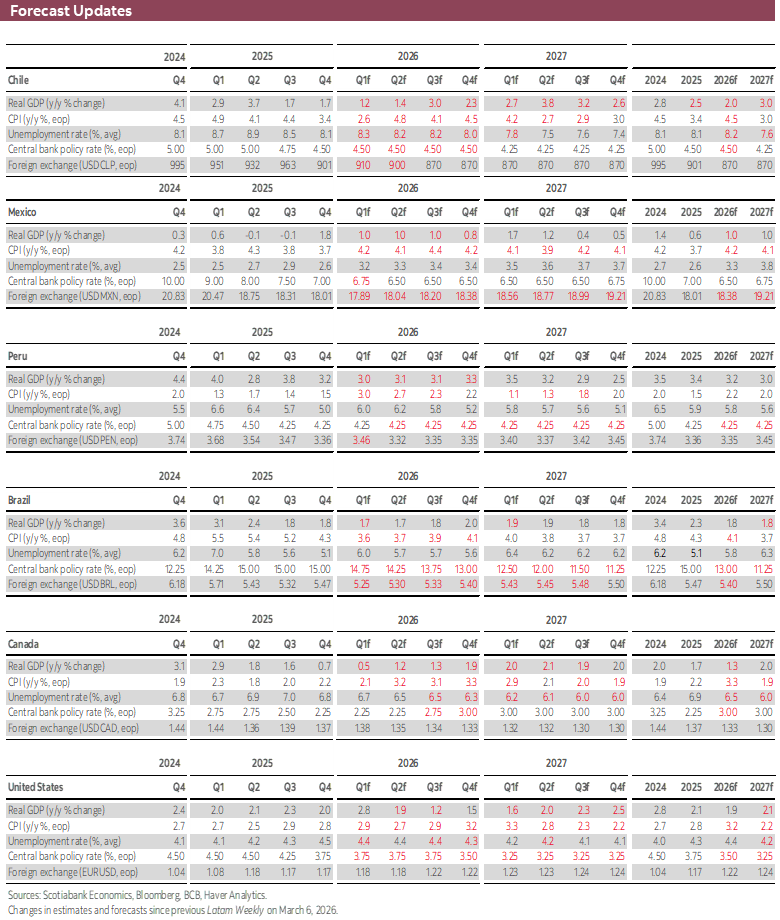

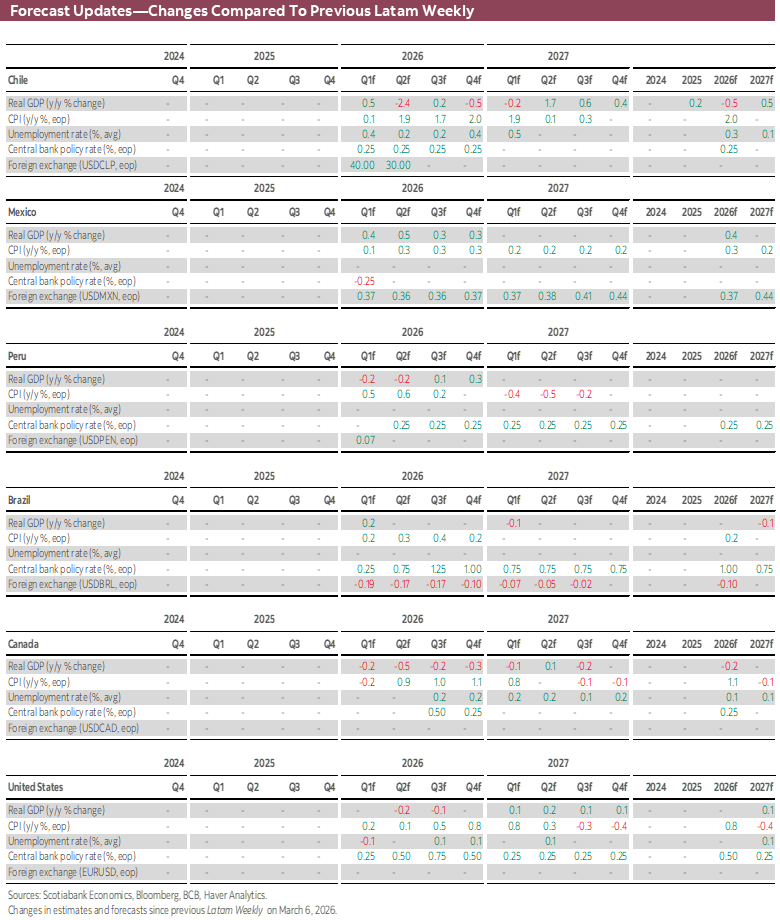

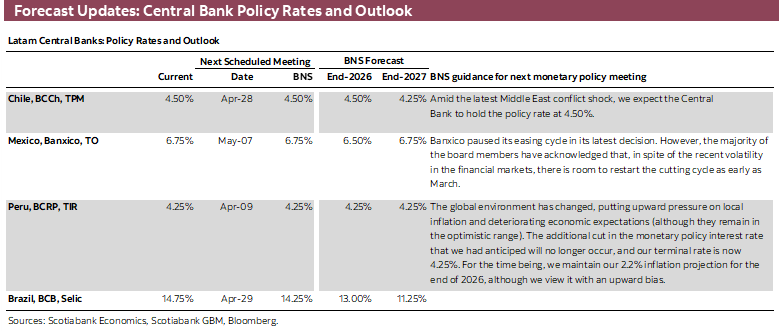

- Chile’s inflation picture took a sharp turn this week after the government modified its fuel stabilization scheme, resulting in steep 40%+ increases in retail gasoline prices. Ahead of Wednesday’s BCCh meeting minutes, our colleagues go over the BCCh’s latest forecast revisions in its Monetary Policy Report, with the bank’s staff lifting their end-2026 inflation forecast to 4% from 3.2% y/y.

- With a mostly empty release calendar in Mexico, we discuss how Banxico’s 3–2 cut decision (and opening the door to more easing) clashes with rising inflation risks at a time when headline inflation (as of H1-Mar) is already over 1.5ppts above the 3% target. We think the room for additional cutting has narrowed significantly, although the majority of the board seems to be leaning towards another rate cut.

Chart of the Week

GLOBAL CPIs TO SHOW INITIAL CONFLICT SHOCK; LATAM CENTRAL BANKS VIEWS

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Global CPI releases for March out over the coming week will give us the first official read into the (initial) inflationary impact of the Middle East conflict, with important implications for the April/May round of monetary policy decisions after the latest round saw the majority of central bankers take a hawkish stance.

- In Latin America, Peruvian CPI is expected to jump to near 3%, following overshoots in mid-March inflation prints from Brazil and Mexico. The team discusses their projection in today’s Weekly, with the jump not only reflecting the effect of international energy prices, but also the impact of the Camisea gas pipeline leak and its temporary suspension, with the latter also expected to drag on economic activity in March.

- Chile’s inflation picture took a sharp turn this week after the government modified its fuel stabilization scheme, resulting in steep 40%+ increases in retail gasoline prices. Ahead of Wednesday’s BCCh meeting minutes, our colleagues go over the BCCh’s latest forecast revisions in its Monetary Policy Report, with the bank’s staff lifting their end-2026 inflation forecast to 4% from 3.2% y/y.

- With a mostly empty release calendar in Mexico, we discuss how Banxico’s 3–2 cut decision (and opening the door to more easing) clashes with rising inflation risks at a time when headline inflation (as of H1-Mar) is already over 1.5ppts above the 3% target. We think the room for additional cutting has narrowed significantly, although the majority of the board seems to be leaning towards another rate cut.

Global CPI releases for March out over the coming week will give us the first official read into the (initial) inflationary impact of the Middle East conflict, with important implications for the April/May round of monetary policy decisions after the latest round saw the majority of central bankers take a hawkish stance—with Banxico’s being the clearest outlier, cutting 25bps and leaving the door open to more. At the very least, it will be a shorter week for most of the globe, with practically all markets closed on Friday (partial in the U.S.) and some others on Thursday (namely Mexico and Peru).

In Latin America, Peruvian CPI is expected to jump to near 3%, following overshoots in mid-March inflation prints from Brazil and Mexico. The Eurozone, Germany, France, Italy, the Netherlands, among others in the region, also publish preliminary HICP figures for the month, accompanied by Tokyo and South Korea readings. A Chilean macro flood of February activity data will be backward-looking but may show a recovery from March, while the focus will be on the BCCh’s meeting minutes. In Colombia, BanRep’s policy announcement is a call on how large of a hike they roll out (100bps median forecast). Mexico’s and Brazil’s calendars are relatively bare. In contrast, the U.S. also has nonfarm and ADP employment, JOLTS, retail sales, and ISM manufacturing data on tap.

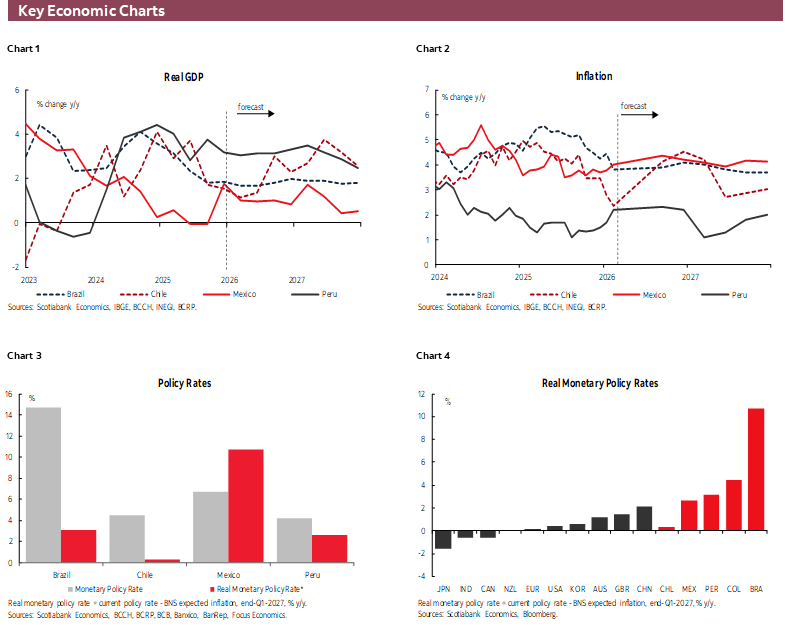

Starting with Peru’s March CPI release on Wednesday, our colleagues in the country outline their projection for headline inflation to clock in at 3% y/y from 2.2% in February, thus reaching the upper bound of the BCRP’s 1–3% target range. The jump will not only reflect the effect of international energy prices, but also the impact of the Camisea gas pipeline leak and its temporary suspension. The latter is also expected to drag on economic activity in March, after an encouraging start to the year with ~3.5% y/y expansion in Monday and February—as the team also discusses today.

Chile’s inflation picture took a sharp turn this week after the government modified its fuel stabilization scheme, resulting in steep 40%+ increases in retail gasoline prices from Thursday (26th). According to our economists, these adjustments would add 0.4ppts and 1.0ppts to March and April headline y/y inflation. In today’s note, the team goes over the BCCh’s latest forecast revisions in its Monetary Policy Report that followed its March 24th meeting, where officials held the overnight rate at 4.50%, as expected. The bank’s staff lifted their end-2026 inflation forecast to 4% y/y, 0.5ppts below our own projection of 4.5%.

In the MPR, the BCCh also showed an implied policy path that includes one hike and then one cut later in the year, which would represent an unlikely scenario. The minutes to the meeting, due on Wednesday, may shed some light on how the board perceives risks to inflation and whether these may warrant a rate hike. As of today’s close, markets are pricing in close to two full 25bps hikes by Chile’s central bank this year, with the first adjustment coming at one of the June or July meetings followed by October/December, or early-2027. Markets are not, however, pricing in rate cuts thereafter.

There is little to get excited about regarding Mexico’s week ahead, where the highlights are February remittances data and Banxico’s economists survey results, both out on Tuesday. The latter will likely show higher inflation forecasts for the quarters ahead and possibly see some respondents tweak their Banxico rate forecasts lower following the bank’s somewhat dovish rate cut announcement earlier this week. As the team argues in today’s Weekly, the board’s 3–2 decision in favour of lowering the overnight rate (and opening the door to more easing) clashes with rising inflation risks at a time when headline inflation (as of H1-Mar) is already over 1.5ppts above the 3% target. We think the room for additional cutting has narrowed significantly, although the majority of the board seems to be leaning towards another rate cut.

COUNTRY UPDATES

Chile—Central Bank Raises Inflation Outlook and Lowers GDP Growth Range

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

In its March Monetary Policy Report (MPR), the Central Bank of Chile revised upward its inflation forecast for December this year, from 3.2% to 4.0% y/y, mainly reflecting higher oil prices and their derivatives, as well as the rapid pass-through to local prices following the recent increase in gasoline and diesel prices announced by ENAP (national petroleum company) this week, amid escalating tensions in the Middle East. As a result, the Central Bank now incorporates a direct impact on CPI prints for March and April which, according to our estimates, would total an additional 1.4 ppts of inflation across both months. The revised inflation outlook is broadly aligned with Scotia’s view, where we recently adjusted our forecast to 4.5% in December 2026.

Within this context, the Board outlined a policy rate path that includes a 25 bp rate hike in the June meeting, followed by a cut of the same magnitude in October. We see this scenario as unlikely, as it would imply reversing the tightening decision shortly after its implementation, which appears inconsistent with recent communication by the Board’s Chairwoman before the Senate. Instead, we continue to project that the policy rate will remain at 4.5% throughout this year, resuming its easing cycle toward its neutral level of 4.25% in early 2027.

As widely expected, the Board also revised its GDP growth forecast lower for 2026, narrowing the range from 2.0–3.0% to 1.5–2.5%, with a mid-point of 1.9%, broadly in line with our 2.0% growth projection. The downward revision reflects the negative impact on household disposable income stemming from higher fuel prices, which is expected to weigh on private consumption. In addition, the scenario incorporates the significant fiscal adjustment announced by the government, which will lead to a contraction in public spending this year, affecting both investment and public consumption (goods and services).

Among other relevant highlights of the MPR, the Central Bank introduced a slight upward revision to its estimate of potential GDP growth, with non-mining potential growth increasing from 2.0% to 2.1%, implying a negative output gap over the projection horizon. Finally, the Central Bank marginally revised its estimated long-term real exchange rate (RER) range to 94–106 points, with a mid-point of 100.

Regarding economic activity, we project a broad-based monthly acceleration across economic sectors, which should allow for a recovery in the year-over-year GDP growth rate in February, following the decline observed in the first month of the year. Nevertheless, we maintain our 2026 GDP growth forecast at 2%.

Mexico—Banxico’s Rate Cut Contrasts with a Backdrop of Rising Inflation Risks

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

Banxico cut its policy interest rate at a time when analysts were divided. While several had anticipated a cut at this week’s meeting (including us), a slight majority expected the adjustment to occur at a later date. The decision nonetheless drew particular attention given that the inflation print for the first half of March, released just two days earlier, showed a sharp rebound in the non-core component, sufficient to push headline inflation to its highest level since October 2024. The print also underscored the increase in upside inflation risks stemming from the impact of the conflict in the Middle East.

Headline inflation reached 4.63% year-over-year in the first half of March, exceeding market expectations and further widening the gap relative to the 3.0% target. The increase was driven primarily by the non-core component, which exhibited significantly greater volatility than in the previous year. In particular, agricultural prices rose sharply, with fruit and vegetable prices posting annual increases close to 24%. These movements reflect meaningful supply-side shocks linked to both domestic and international disruptions, including security issues in key-producing regions and higher input costs amid heightened geopolitical tensions. Core inflation, by contrast, showed a modest deceleration, easing from 4.48% to 4.46% year-over-year, although it has remained above 4% since mid-2025. While there is still no clear evidence of second-round effects, inflationary pressures remain persistent and the balance of risks is tilted to the upside, especially if external shocks prove longer-lasting.

Against this backdrop, and despite headline inflation standing more than 1.5 percentage points above the target, Banxico’s Governing Board decided to cut the policy rate by 25 basis points to 6.75%, in a split decision, with three members voting in favour and two opting to keep rates unchanged. The divided vote was notable, particularly considering the recent inflation rebound.

At the same time, the policy statement acknowledged an upside-skewed inflation risk balance, driven by trade policy-related disruptions and the effects of geopolitical conflicts, while emphasizing that both external and domestic uncertainty remain elevated. In this context, the depth and duration of the Middle East conflict will be critical for upcoming inflation readings, given its potential impact on commodity markets.

Specifically, the destruction of key oil extraction infrastructure in the Persian Gulf region could prolong the normalization process in energy markets even after a potential ceasefire or negotiated settlement. Moreover, while production costs may rise immediately, increases in consumer prices tend to materialize with a lag of several months. As a result, recent communications from several central banks, including the Federal Reserve and the European Central Bank following meetings last week, have adopted a more cautious tone, explicitly conditioned on the conflict’s potential impact—particularly on energy prices.

In this environment, Banxico revised its forecasts for both headline and core inflation upward for the remainder of 2026, while still projecting convergence to the 3.0% target by the second quarter of 2027. Similarly, private-sector analysts have revised their year-end inflation expectations higher in recent months, now anticipating inflation to remain above 4.0% in December.

Looking ahead, the market’s attention will focus on the evolution of agricultural prices, the impact of the Middle East conflict on energy costs, and any additional signals from Banxico regarding the future course of monetary policy. In particular, March CPI and PPI releases will be key to assessing the extent to which higher commodity prices are filtering through the inflation pipeline. In addition, the publication of the meeting minutes on April 9th will be closely watched to gauge the degree of consensus within the Governing Board. Overall, recent developments reinforce the view that while a majority of the Board may still be considering an additional rate cut, the room for further monetary easing has narrowed significantly.

Peru—March: A Month of Temporary Economic Shifts

Ricardo Avila, Senior Analyst

ricardo.avila@scotiabank.com.pe

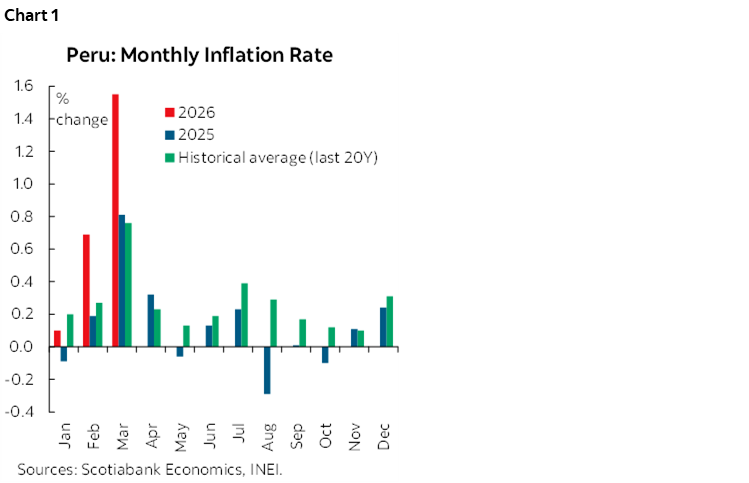

March inflation will be released on April 1st. We expect monthly inflation to significantly exceed both the figure recorded in March 2025 (0.8%) and the 20‑year historical average (0.8%) (chart 1). Our estimate places March inflation at 1.55% m/m, which would push annual inflation up to 3.0% y/y—the upper bound of the BCRP’s target range—from 2.2% in February. If confirmed, inflation would reach its highest level in two years (March 2024). We believe inflation will remain close to the upper bound of the target range for several more months, before easing during the third quarter of 2026.

Several factors are driving March inflation. First, seasonality: March typically records elevated inflation (0.8% on average), largely due to the education sector, as the school year begins in March. Energy is another important source of upside pressure, reflecting higher oil prices and the Camisea pipeline leak (and temporary suspension) incident, which restricted natural gas use during the first half of the month. Both factors have contributed to rising transportation costs. Finally, food prices continued to increase, driven by higher transportation costs and adverse weather conditions.

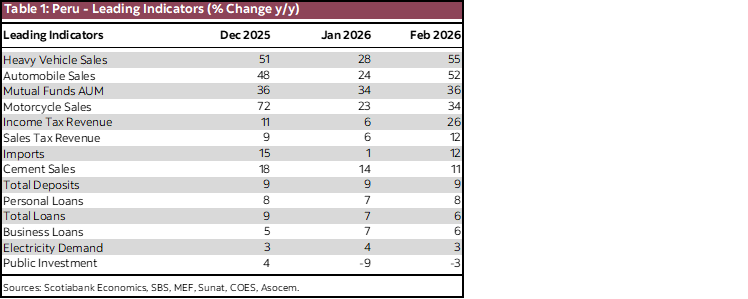

On the economic activity front, we updated our leading indicators related to domestic demand (table 1), which remain favourable and point to a solid start in 2026. Private investment continues to expand at a double‑digit pace, supported by cement demand and heavy vehicle sales, while electricity demand and corporate lending are accelerating. Private consumption also shows strength, with mutual funds and vehicle sales growing at double digits, alongside steady growth in personal credit. Tax revenues—both corporate and individual—also rose at a double‑digit rate. Taken together, we believe February’s economic dynamics were similar to January’s, and we estimate GDP growth at around 3.6%.

Looking ahead, the Camisea pipeline incident in early March is expected to reduce hydrocarbon production, leading to a slowdown in March GDP—not only in that sector but also through indirect effects on transport and industry. Nevertheless, we estimate that overall economic activity will expand by about 3.0% in the first quarter of 2026, broadly in line with potential output.

Separately, on March 20th the BCRP updated its projections for key economic variables in its Inflation Report for 1Q26, introducing significant changes compared with the 4Q25 report. GDP growth for 2026 was revised upward from 3.0% to 3.2%. While this adjustment may appear surprising given recent shocks, the Bank noted that absent external (weather, i.e. El Niño) and internal (natural gas disruption) factors, growth could have reached 3.6%. Moreover, sectors such as construction, services, and commerce have started the year stronger than expected. Another major revision was in domestic demand, raised from 3.5% to 4.9% for 2026. This reflects a sharp upward adjustment in private investment, from 5.0% to 9.5%, close to the 10.0% growth recorded in 2025, as well as stronger private consumption, now projected at 3.4% versus the previous 3.0%. These revisions are supported by high metal prices and optimistic business expectations. Regarding inflation, the Bank noted that the impact of the Middle East conflict will be temporary, with inflation expected to hover near the upper bound of the target range (3.0%) in the short term. The year‑end forecast was revised upward from 2.0% to 2.4%.

| LOCAL MARKET COVERAGE | ||

| CHILE | ||

| Website: | Click here to be redirected | |

| Subscribe: | anibal.alarcon@scotiabank.cl | |

| Coverage: | Spanish and English | |

| MEXICO | ||

| Website: | Click here to be redirected | |

| Subscribe: | estudeco@scotiacb.com.mx | |

| Coverage: | Spanish | |

| PERU | ||

| Website: | Click here to be redirected | |

| Subscribe: | siee@scotiabank.com.pe | |

| Coverage: | Spanish | |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.